- Bulk Chemicals

- Methanol Market

Methanol Market Size, Share, and Growth Forecast 2026 - 2033

Methanol Market by Product Type (Conventional Methanol - Coal, Natural Gas; Bio-methanol; E-methanol), by Derivative (Formaldehyde, Acetic Acid, MTBE & TAME, Dimethyl Ether (DME), Methanol-to-Olefins (MTO), Methanol-to-Gasoline (MTG), Biodiesel, Methylamines, Solvents, Others), by Grade (Fuel Grade, Chemical Grade, Pharmaceutical Grade), End-user (Automotive & Transportation, Construction & Infrastructure, Chemicals & Petrochemicals, Others, and Regional Analysis, 2026 - 2033

Methanol Market Size and Trend Analysis

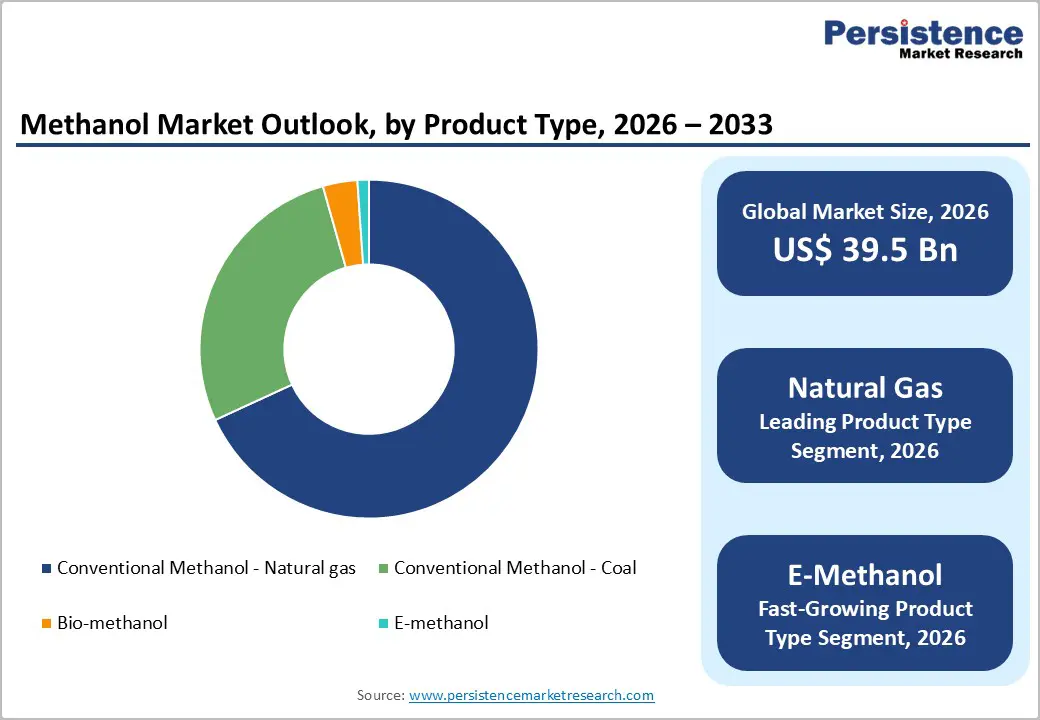

The global methanol market size is expected to be valued at US$ 39.5 billion in 2026 and projected to reach US$ 65.1 billion by 2033, growing at a CAGR of 7.4% between 2026 and 2033. This robust growth is primarily driven by surging demand from Methanol-to-Olefins (MTO) facilities in China, expanding marine fuel applications under the International Maritime Organization (IMO) decarbonization mandates, and rising investments in green and blue methanol production. The integration of methanol into energy transition pathways, particularly as a hydrogen carrier and low-carbon fuel, further underpins market expansion.

Key Industry Highlights:

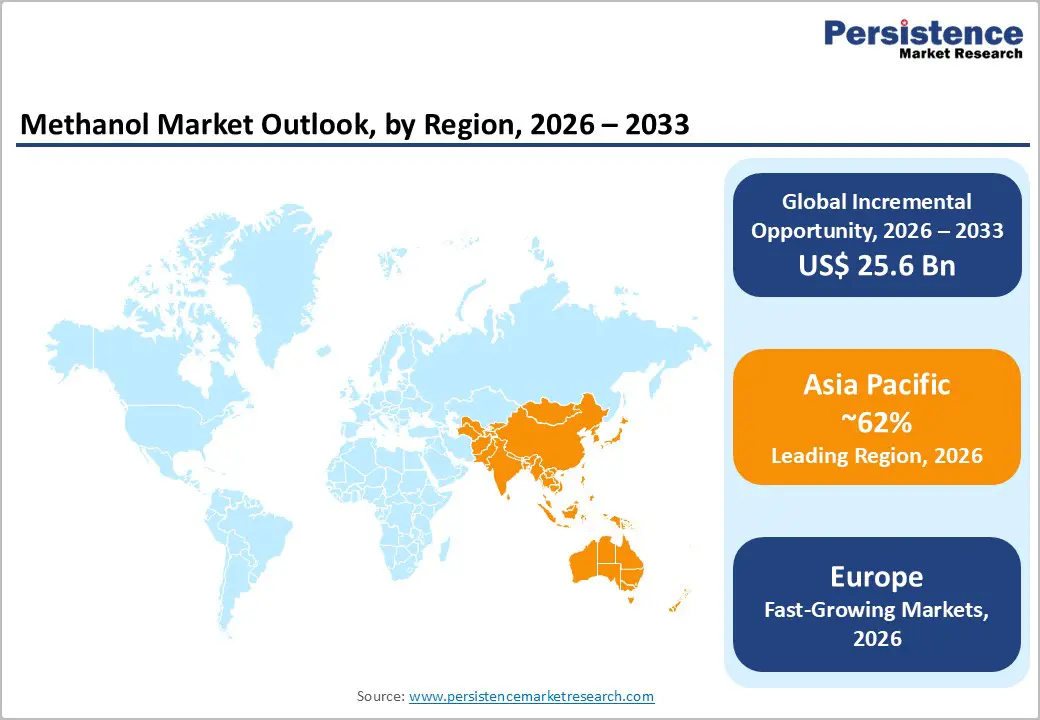

- Leading Region: Asia Pacific dominates the global methanol market with approximately 62% share in 2025, underpinned by China's massive MTO capacity, rising chemical production, and deepening coal-to-chemicals industrial base.

- Fastest Growing Region: Europe is the fastest-growing region through 2033, driven by e-methanol investments aligned with the EU Green Deal, FuelEU Maritime regulation, and surging demand from green shipping decarbonization programs.

- Dominant End-user: The chemicals & petrochemicals end-use segment leads with 48% share in 2025, supported by formaldehyde resin demand, MTO facilities, and acetic acid production in Asia and the Middle East.

- Fastest Growing Product Type: E-methanol is the fastest-growing product type through 2033, spurred by marine sector green fuel mandates, EU carbon pricing, and accelerating electrolyzer cost reductions enabling competitive green methanol production.

- Key Opportunity: The methanol marine fuel opportunity, catalyzed by IMO 2050 decarbonization targets and major shipping company commitments, represents the most significant incremental demand driver for new methanol capacity through 2033.

Market Dynamics

Drivers - Expanding Methanol-to-Olefins (MTO) Capacity in Asia

The rapid scale-up of Methanol-to-Olefins (MTO) technology remains a primary structural demand driver for methanol globally. China, which commands over 55% of global methanol demand, has aggressively expanded MTO-based propylene and ethylene production, reducing dependence on naphtha crackers. According to data from the China Petroleum and Chemical Industry Federation (CPCIF), domestic methanol consumption in the chemicals sector grew significantly between 2018 and 2023, with MTO capacity additions exceeding 10 million metric tons per annum (MTPA). This technology-driven demand trajectory positions methanol as an indispensable petrochemical feedstock, especially as Asian economies prioritize cost-effective olefin production, creating sustained long-term consumption growth across the Asia Pacific region.

Methanol as a Marine Fuel Under IMO Decarbonization Mandates

The maritime shipping industry's transition toward low-emission fuels is generating a transformative demand wave for methanol. The International Maritime Organization (IMO) has mandated a 40% reduction in carbon intensity by 2030 and net-zero greenhouse gas emissions by 2050, prompting major shipping companies to pivot toward methanol-fueled vessels. Maersk, the world's second-largest container shipping company, had ordered 25 methanol-powered vessels by early 2024. Japan's Mitsui O.S.K. Lines and Stena Line have similarly committed to methanol-compatible fleets. The Society of International Gas Tanker and Terminal Operators (SIGTTO) estimates that methanol as a marine fuel could account for a meaningful share of alternative fuel adoption by 2030, directly fueling incremental methanol demand globally.

Restraints - Volatility in Natural Gas Feedstock Prices

Approximately 65% of global methanol is produced from natural gas, rendering production economics highly sensitive to fluctuations in gas prices. The European energy crisis of 2021-2023, wherein natural gas prices surged by over 300% at peak, forced multiple European methanol plants to curtail or suspend operations. According to the International Energy Agency (IEA), natural gas price volatility directly compresses producer margins and creates supply uncertainty, discouraging downstream customers from securing long-term supply contracts. This feedstock price risk is a persistent restraint, limiting capacity investments in gas-based methanol plants and creating regional supply imbalances that can destabilize global methanol trade flows.

Toxicity and Safety Regulations Limiting End-Use Expansion

Methanol's toxicity profile, including risks of blindness or death upon ingestion, imposes significant regulatory restrictions on its direct use in consumer-facing applications, including blended fuel products. Regulatory bodies such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) maintain strict handling, labeling, and transportation requirements under frameworks such as REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals). These compliance burdens raise operational costs for producers and distributors, constraining adoption in markets where safety infrastructure is underdeveloped, particularly in certain parts of Latin America and Sub-Saharan Africa.

Opportunities - Green and E-Methanol: Capitalizing on the Renewable Energy Transition

The emergence of e-methanol, produced by combining green hydrogen from electrolysis with captured CO2, represents one of the highest-growth opportunities in the global methanol landscape. The Methanol Institute reports that over 90 green/e-methanol projects were announced or under development globally as of 2024, with combined capacity targeting millions of tonnes annually by 2030. European Union policies under the Renewable Energy Directive (RED III) and the FuelEU Maritime regulation actively incentivize e-methanol adoption in shipping.

With carbon pricing mechanisms tightening globally, companies investing in green methanol production infrastructure today, particularly in regions with low-cost renewable electricity such as Chile, Morocco, and Northern Europe, are positioned to command premium pricing and first-mover advantages in a rapidly scaling market segment.

Methanol Economy in Power Generation and Energy Storage

Methanol's utility as a liquid hydrogen carrier and direct fuel for Direct Methanol Fuel Cells (DMFCs) is unlocking significant opportunities in decentralized power generation. The U.S. Department of Energy (DOE) has actively funded research into methanol reforming for hydrogen extraction and fuel cell integration. Methanol's high energy density, ambient-temperature liquid state, and existing distribution infrastructure give it a competitive edge over compressed hydrogen in portable and backup power applications.

In Japan, Mitsubishi Gas Chemical Company Inc. has advanced methanol-based power solutions, while South Korea's national energy strategy increasingly incorporates methanol as a bridging fuel. As global power generation increasingly shifts toward cleaner fuels, methanol's versatility positions it as a critical energy vector capable of serving both industrial and grid-scale applications through 2033.

Category-wise Analysis

Product Type Insights

Conventional methanol derived from natural gas dominates the global product type segment, accounting for approximately 62% of total share in 2025. Natural gas-based methanol remains the lowest-cost production route, with steam methane reforming (SMR) being a mature and capital-efficient technology. Leading producers including Methanex Corporation, SABIC, and Zagros Petrochemical Company (ZPC) rely predominantly on gas-based assets located near low-cost feedstock reserves in Trinidad, the Middle East, and Southeast Asia. According to the Methanol Institute, natural gas accounts for the majority of global methanol feedstock consumption. E-methanol is, however, the fastest-growing segment, supported by EU clean fuel mandates and marine sector demand, with capacity investments accelerating across Europe and the Americas through 2033.

Derivative Analysis

Formaldehyde remains the leading derivative segment, holding approximately 30% of the global methanol derivatives market in 2025. Formaldehyde, produced through methanol oxidation, serves as a foundational chemical in resins (urea-formaldehyde, melamine-formaldehyde, and phenol-formaldehyde), which are critical for construction, furniture, automotive components, and adhesives. The American Chemistry Council (ACC) identifies formaldehyde as one of the top industrially produced chemicals in the United States.

Rising construction activity across Asia Pacific, particularly government-driven housing programs in India and Southeast Asia, sustains formaldehyde demand. Meanwhile, Dimethyl Ether (DME) and MTO derivatives are the fastest-growing applications, propelled by clean fuel policies and olefin capacity additions in China and the Middle East.

Grade Insights

Chemical grade methanol commands the dominant share of the market, accounting for approximately 68% of total volume in 2025. Chemical grade methanol (meeting ASTM D1152 or equivalent standards) serves as the core feedstock for formaldehyde, acetic acid, MTBE, and MTO processes. Its widespread industrial applicability across chemicals, petrochemicals, and energy sectors ensures consistently high volumes. According to the American Chemical Society (ACS), methanol ranks among the top five globally produced chemicals. Pharmaceutical grade methanol, though a smaller segment, represents the fastest-growing grade category, driven by expanding generic drug manufacturing in India, ASEAN countries, and Mexico, where GMP-compliant methanol is essential for synthesis and purification processes.

End-user Insights

The chemicals & petrochemicals segment leads the end-use landscape, accounting for approximately 48% of global methanol consumption in 2025. This dominance reflects methanol's irreplaceable role as a C1 building block in organic synthesis, feeding formaldehyde, acetic acid, methylamines, and MTO pathways. China's large-scale coal-to-chemicals industry, a cornerstone of which involves methanol as an intermediate, anchors this segment's leadership.

According to Yankuang Energy Group Company Limited, one of China's leading coal chemical enterprises, methanol-to-olefins facilities continue scaling as the country reduces crude oil dependency. Marine & Shipping is the fastest-growing end-use, driven by the IMO's 2050 Net Zero targets and the accelerating orderbook of methanol-powered vessels globally.

Regional Insights

North America Methanol Market Trends and Insights

North America holds approximately 14% of the global methanol market share in 2025, supported by cost-competitive natural gas production from the U.S. shale revolution. The region is witnessing increased investment in methanol export infrastructure and emerging green methanol projects, particularly in Canada and the U.S. Gulf Coast, aligned with Inflation Reduction Act (IRA) incentives for clean energy production.

U.S. Methanol Market Size

The United States accounts for approximately 80% of North American methanol consumption, supported by large-scale formaldehyde and MTBE production clusters in the Gulf Coast. U.S. methanol demand is further bolstered by growing interest in methanol as a hydrogen carrier and marine fuel, with the IRA's clean fuel provisions unlocking incremental investment in low-carbon methanol facilities.

Europe Methanol Market Trends and Insights

Europe accounts for approximately 11% of global methanol demand in 2025 and is positioned as the fastest-growing region through 2033, driven by aggressive e-methanol investments. The European Green Deal and FuelEU Maritime regulation are structurally reshaping European methanol demand toward renewable and low-carbon variants, with the Netherlands, Norway, and Germany emerging as green methanol production hubs.

Germany Methanol Market Size

Germany represents the largest methanol market in Europe, contributing approximately 25% of regional consumption in 2025. Strong chemical industry demand, particularly from BASF SE for formaldehyde and methylamines, sustains volumes. Germany is also advancing e-methanol pilot plants under its National Hydrogen Strategy, positioning the country as a future green methanol production center.

U.K. Methanol Market Size

The United Kingdom accounts for approximately 12% of European methanol consumption in 2025. The U.K.'s methanol demand is increasingly shaped by marine shipping decarbonization, given its major ports at Felixstowe, Southampton, and Liverpool. U.K. Government investments in clean maritime fuels under the Clean Maritime Plan support long-term methanol demand growth.

France Methanol Market Size

France contributes approximately 10% of European methanol market revenues in 2025. Chemical manufacturing, particularly resins, adhesives, and specialty chemicals from companies such as Arkema, drives consistent demand. France's renewable energy expansion under the Multiannual Energy Plan (PPE) is also creating early-stage opportunities for bio-methanol and e-methanol production leveraging biomass and offshore wind resources.

Asia Pacific Methanol Market Trends and Insights

Asia Pacific is the dominant region, commanding approximately 62% of global methanol demand in 2025, with China alone representing over 55% of worldwide consumption through MTO, formaldehyde, and DME applications. China's coal-to-methanol pathway, though facing environmental scrutiny, remains cost-competitive, with over 100 million metric tons per annum (MTPA) of installed capacity. India, South Korea, Japan, and Southeast Asia are emerging as secondary demand centers, particularly for chemical-grade and fuel-grade methanol.

India accounts for approximately 8% of Asia Pacific methanol consumption in 2025. The government's Methanol Economy Programme, promoted by NITI Aayog, aims to blend methanol with petrol and diesel to reduce import bills. Planned methanol production from high-ash coal and agricultural residue reinforces India's long-term self-sufficiency ambitions, supporting significant incremental demand growth through 2033.

Japan Methanol Market Size

Japan contributes approximately 5% of Asia Pacific methanol demand in 2025. The country is a net importer of methanol, sourcing volumes for formaldehyde resins, MTBE blending, and specialty chemical production. Mitsubishi Gas Chemical Company Inc. remains a major domestic producer and technology licensor. Japan's methanol demand is poised to grow through marine fuel adoption, supported by the Japan Maritime Bureau's clean shipping roadmap.

Southeast Asia Methanol Market Size

Southeast Asia accounts for approximately 7% of Asia Pacific methanol demand in 2025. PETRONAS (Malaysia) and Indonesia's state-owned gas companies are key producers, with natural gas-based methanol serving regional export markets. Vietnam, Thailand, and Indonesia are expanding chemical manufacturing capacity, creating sustained incremental methanol consumption demand, particularly for formaldehyde and biodiesel applications, through the forecast period.

Competitive Landscape

The global methanol market is moderately consolidated, with a limited number of large producers controlling a significant share of global capacity. Market structure is strongly influenced by access to low-cost feedstock, leading to regional concentration in gas-rich and coal-abundant economies. Competitive advantage is primarily driven by strategic plant location, economies of scale, and long-term supply agreements with downstream chemical and fuel customers.

Business strategies are increasingly centered on diversification into sustainable production pathways, particularly green and bio-methanol. Companies are forming joint ventures, technology partnerships, and long-term offtake agreements with end users such as shipping and energy firms to secure future demand. Emerging models such as tolling arrangements and carbon credit monetization are gaining traction, reflecting a shift toward sustainability-linked revenue streams. Additionally, players are investing in capacity expansion and integration across the value chain to enhance cost efficiency and strengthen market positioning.

Key Developments:

- December 2025: KBR secured a contract from Fikrat Al-Tadweer to deploy its PureM green methanol technology for Saudi Arabia’s first biomethanol plant, converting landfill gas into renewable fuel and supporting the Kingdom’s sustainability and emissions reduction goals.

- August 2025: Mitsui & Co. launched the world’s first commercial-scale e-methanol plant in Denmark with European Energy, producing low-carbon fuel from green hydrogen and CO2 to support decarbonization in shipping and industrial applications.

- August 2025: Toyo Engineering India commissioned a 10 TPD green methanol plant at NTPC’s Vindhyachal facility in Madhya Pradesh, producing methanol using captured CO2 and green hydrogen, marking India’s first successful demonstration of CO2-to-methanol technology.

Methanol Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 27.2 Billion |

| Current Market Value (2026) | US$ 39.5 Billion |

| Projected Market Value (2033) | US$ 65.1 Billion |

| CAGR (2026 - 2033) | 7.4% |

| Leading Region | Asia Pacific, 62% market share (2025) |

| Dominant Product Type | Conventional Methanol (Natural Gas), 62% share |

| Top-Ranking Derivative | Formaldehyde, 30% share |

| Incremental Opportunity (2026 - 2033) | US$ 25.6 Billion |

Companies Covered in Methanol Market

- Methanex Corporation

- HELM Proman Methanol AG

- SABIC

- Yankuang Energy Group Company Limited

- Zagros Petrochemical Company (ZPC)

- Celanese Corporation

- BASF SE

- PETRONAS

- Mitsubishi Gas Chemical Company Inc.

- Mitsui & Co., Ltd.

- LyondellBasell Industries B.V.

- OCI N.V.

- Metafrax Chemicals

- SIPCHEM

- China National Petroleum Corporation (CNPC)

- Proman AG

- Natgasoline LLC

- Saudi Kayan Petrochemical Company

Frequently Asked Questions

The methanol market is expected to reach US$ 39.5 billion in 2026, driven by strong demand from chemicals and fuel applications.

Demand is driven by MTO/MTG expansion, marine fuel adoption, and investments in green and e-methanol.

Asia Pacific leads with around 62% share, supported by strong demand from China and other emerging Asian economies.

Green and e-methanol for marine shipping presents a major growth opportunity driven by decarbonization targets.

Key players include Methanex, SABIC, OCI N.V., and BASF among others.