- Biotechnology

- Liposomes Market

Liposomes Market Size, Share, and Growth Forecast 2026 - 2033

Liposomes Market by Product (Simple Liposomes, Formulated Liposomes: Doxorubicin, Amphotericin B, Paclitaxel, Cytarabine Liposomes; Vaccines), Application (Drug Delivery: Cancer, Fungal Infection, Viral & Parasite Infection, Others; Gene Delivery/Transfection; Contrast Agents for Medical Imaging; Model Cell Membranes), End-user (Hospitals, Specialty Clinics, Research Institutes, Pharmaceutical & Biotechnology Companies, Cosmetic Industry), and Regional Analysis, 2026 - 2033

Liposomes Market Share and Trends Analysis

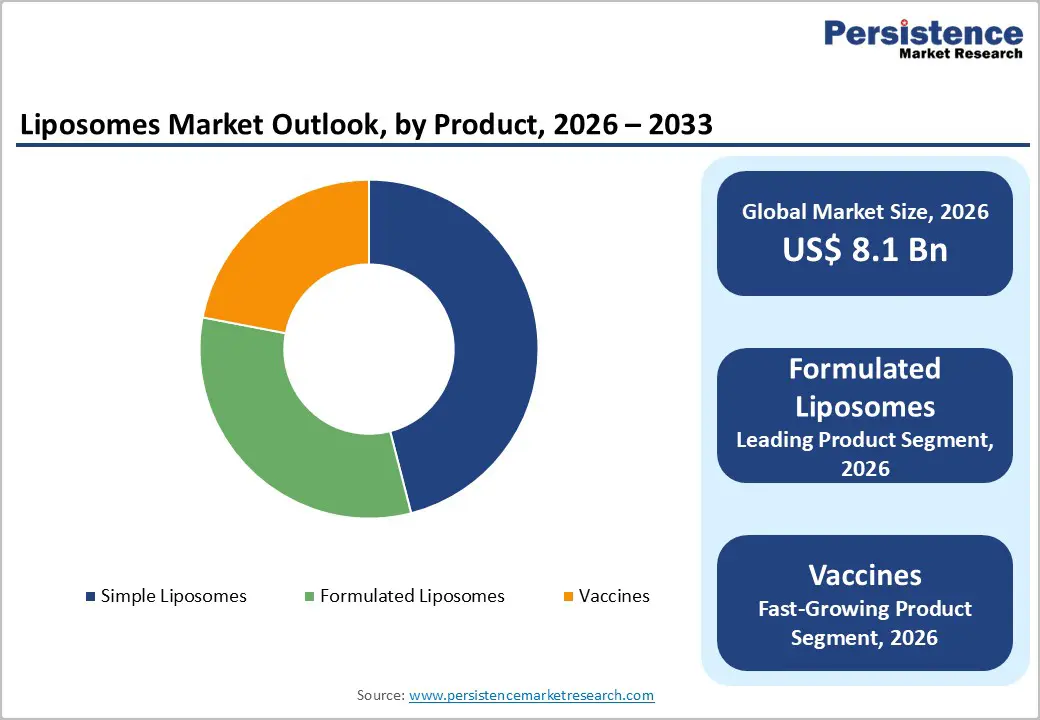

The global liposomes market size is expected to be valued at US$ 8.1 billion in 2026 and projected to reach US$ 12.3 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

This consistent growth is driven by the expanding clinical deployment of liposomal drug delivery systems across oncology and infectious disease therapeutics, the transformative validation of lipid nanoparticle technology through mRNA COVID-19 vaccines, and intensifying pharmaceutical R&D investment in targeted drug delivery to overcome chemotherapy toxicity and multidrug resistance challenges.

The U.S. FDA has approved over 15 liposomal drug formulations for clinical use, spanning oncology, antifungal therapy, and analgesics. Growing biopharma pipeline activity in liposomal gene delivery and mRNA vaccine development is simultaneously opening high-growth commercial trajectories well beyond traditional small-molecule oncology applications through 2033.

Key Industry Highlights:

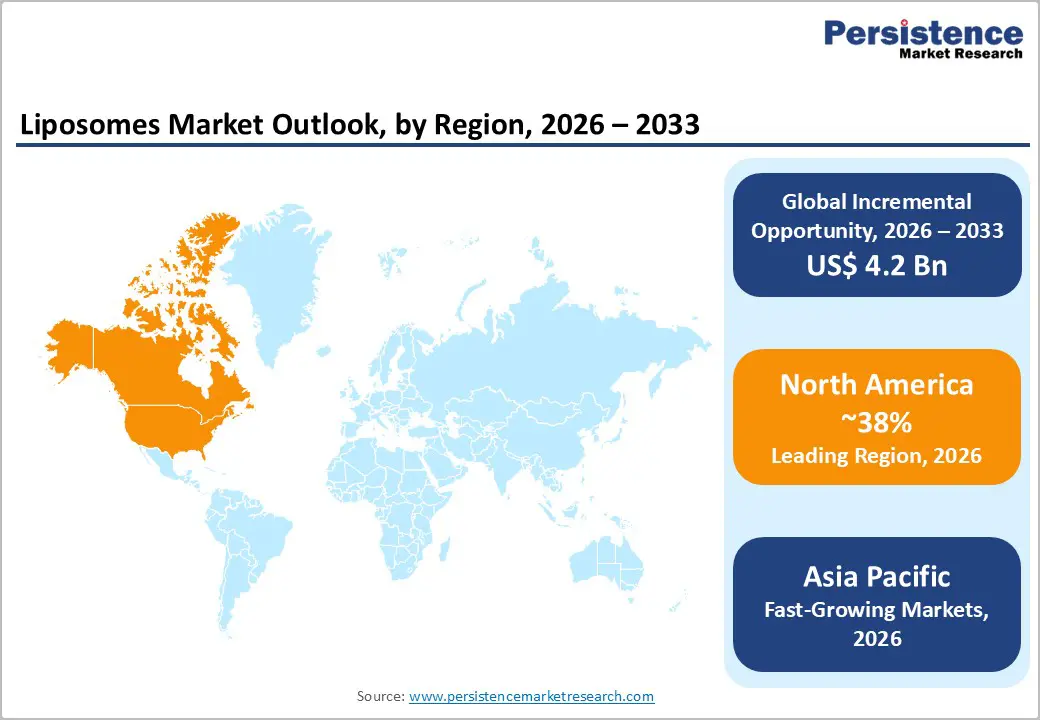

- Leading Region - North America holds approximately 38% of the global Liposomes market share in 2025, driven by over 15 FDA-approved liposomal formulations, world-leading biopharma R&D investment exceeding USD 100 billion annually, and U.S.-headquartered mRNA vaccine LNP manufacturing leaders Pfizer and Moderna

- Fast-Growing Market - Asia Pacific is the fastest-growing region, powered by China NMPA domestic liposomal drug approvals, Luye Pharma and Sun Pharma pipeline expansion, India's growing cancer burden, and Singapore's A*STAR-funded nanomedicine manufacturing hub development.

- Dominant Product Segment - Formulated liposomes lead with approximately 46% share in 2026, anchored by globally approved liposomal doxorubicin (Doxil/Caelyx) and AmBisome deployment in ESMO- and IDSA-endorsed oncology and antifungal treatment protocols.

- Fast - Growing Product Segment - Vaccines are the fastest-growing product segment, catalyzed by WHO mRNA Technology Transfer Hub initiatives in 15+ countries, NIAID-funded LNP vaccine programs targeting HIV and cancer neoantigens, and the post-COVID mRNA platform commercialization wave.

Market Dynamics

Drivers - Expanding Liposomal Oncology Drug Portfolio and Growing Cancer Burden Driving Clinical Demand

The rising global burden of cancer and the well-established clinical efficacy of liposomal chemotherapy formulations are the primary structural drivers of the liposomes market. The World Health Organization (WHO) reported approximately 20 million new cancer cases globally in 2022, with projections indicating this will rise to 35 million by 2050. Liposomal formulations of established chemotherapy agents most notably liposomal doxorubicin (Doxil/Caelyx) and liposomal amphotericin B (AmBisome) remain first-line or standard-of-care options for multiple cancer types and invasive fungal infections due to their superior safety profiles relative to conventional formulations.

The National Cancer Institute (NCI) and European Society for Medical Oncology (ESMO) guidelines endorse liposomal formulations in breast cancer, ovarian cancer, Kaposi's sarcoma, and multiple myeloma treatment protocols. Continued expansion of approved clinical indications for existing liposomal drugs, combined with new entrants in the pipeline, is reinforcing institutional procurement demand.

mRNA Lipid Nanoparticle Validation Catalyzing Next-Generation Liposomal Vaccine and Gene Delivery Growth

The unprecedented global deployment of mRNA-based COVID-19 vaccines delivered via lipid nanoparticle (LNP) systems functionally related to liposomes has fundamentally transformed industry and regulatory confidence in lipid-based nucleic acid delivery. The FDA authorizations and subsequent full approvals of Pfizer-BioNTech's Comirnaty and Moderna's Spikevax validated LNP manufacturing scalability at a global level, creating a broad technology transfer and intellectual property foundation that is now being applied to therapeutic mRNA, siRNA, and gene editing delivery programs.

The NIH has invested heavily in nucleic acid delivery research, with the NIAID funding multiple next-generation vaccine programs using lipid nanoparticle platforms targeting influenza, HIV, RSV, and cancer neoantigens. This validation wave is accelerating biopharma investment in liposome-based gene delivery, transfection reagents, and vaccine adjuvant applications, representing a step-change in addressable market scope for liposome technology providers.

Restraints - Complex Manufacturing Processes and High Production Costs Limiting Scalability

Liposome manufacturing requires highly specialized equipment, including high-pressure homogenizers, extrusion membranes, and cryogenic lyophilization systems operating under stringent aseptic conditions to achieve consistent particle size distribution, encapsulation efficiency, and stability. The capital and operational costs of GMP-compliant liposome production facilities are substantially higher than conventional pharmaceutical manufacturing, with estimates suggesting liposomal drug production costs are 3 to 5 times greater per unit than equivalent conventional formulations. These economics create barriers to entry for smaller manufacturers, slow capacity expansion, and contribute to elevated drug pricing that may limit formulary access in cost-sensitive healthcare systems.

Physical and Chemical Instability Challenges in Storage and Distribution

Liposomal formulations are inherently susceptible to physical and chemical degradation during storage and distribution, including membrane fusion, aggregation, drug leakage, phospholipid oxidation, and hydrolysis. Most liposomal drug products require refrigerated storage conditions between 2-8°C, with some formulations requiring frozen storage, creating cold-chain logistics requirements that add cost and complexity to global distribution. The International Council for Harmonisation (ICH) stability guidelines require extensive stability validation packages for liposomal formulations, extending development timelines. These storage and handling requirements represent a significant challenge for market penetration in low-resource healthcare settings and limit opportunities for ambient-temperature product formats.

Opportunities - Liposomal Vaccines: The Fastest-Growing Segment Propelled by mRNA and Therapeutic Vaccine Pipelines

Liposomal and lipid nanoparticle-based vaccines represent the fastest-growing product segment, fueled by the post-COVID commercialization wave of mRNA vaccine technology and an expanding pipeline of prophylactic and therapeutic vaccine programs. The WHO's mRNA Technology Transfer Hub is supporting capacity building for mRNA vaccine manufacturing in 15+ countries, broadening the global addressable market for lipid nanoparticle components.

The National Institute of Allergy and Infectious Diseases (NIAID) has launched multiple liposomal and LNP-based vaccine programs targeting HIV, tuberculosis, malaria, and influenza. In oncology, therapeutic cancer vaccines using liposomal neoantigen delivery systems are entering Phase II and Phase III clinical trials, with programs at BioNTech, Moderna, and Gritstone Bio potentially representing multi-billion-dollar commercial opportunities. Manufacturers providing pharmaceutical-grade lipid components and formulation development services are ideally positioned to capture this high-growth segment.

Category-wise Analysis

Product Insights

Formulated Liposomes lead the Product category, accounting for approximately 46% of total market share in 2025. This leadership is anchored by the commercial maturity and widespread clinical adoption of FDA- and EMA-approved liposomal drug products spanning oncology and infectious disease. Liposomal doxorubicin (Doxil/Caelyx) by Janssen Pharmaceutical Companies remains one of the most widely prescribed liposomal agents globally, indicated for ovarian cancer, breast cancer, multiple myeloma, and Kaposi's sarcoma.

AmBisome by Gilead Sciences is the leading liposomal antifungal agent endorsed by IDSA (Infectious Diseases Society of America) guidelines for invasive aspergillosis and cryptococcal meningitis. Multiple generic liposomal doxorubicin entrants and the pipeline of novel formulated liposomes in clinical development, including thermosensitive and targeted antibody-conjugated liposomes, are further diversifying the formulated segment's revenue base and reinforcing its category leadership.

Application Analysis

Drug Delivery specifically for cancer treatment is the dominant application category, accounting for approximately 58% of the total liposomes market share in 2026. Cancer drug delivery constitutes the largest single application of liposomal technology, given the well-established advantages of liposomal encapsulation in improving drug pharmacokinetics, reducing systemic toxicity via the enhanced permeability and retention (EPR) effect, and enabling higher tolerated doses of potent chemotherapy agents.

The WHO's projection of 35 million new cancer cases by 2050 and NCI-endorsed clinical guidelines recommending liposomal formulations across multiple tumor types ensure structural, long-term demand dominance. Gene Delivery/Transfection is the fastest-growing application, buoyed by the RNA therapeutic pipeline, while contrast agent and cosmetic industry applications represent emerging diversification vectors for liposome technology providers.

End-user Insights

Pharmaceutical & biotechnology companies represent the leading end -user segment with approximately 42% of global market share in 2026. This dominance reflects the critical role of liposomal systems throughout pharmaceutical drug development, from preclinical formulation research to clinical-grade GMP manufacturing of approved liposomal therapeutics and vaccines. Biopharma companies are the largest volume buyers of phospholipid raw materials, formulation development services, and contract manufacturing capacity for liposomal products.

The PhRMA biopharma R&D pipeline, exceeding USD 100 billion annually, ensures sustained demand for liposomal formulation development and scale-up services. Research Institutes the second-largest segment, deploy liposomal platforms extensively in NIH, ERC, and MRC-funded drug delivery, gene therapy, and vaccine research programs, representing a significant recurring demand base for non-clinical liposomal reagents and kit products.

Regional Insights

North America Liposomes Market Trends and Insights

North America leads the global Liposomes market with approximately 38% share in 2026, supported by the highest concentration of FDA-approved liposomal drugs, world-leading biopharma R&D investment, robust NIH funding for drug delivery and vaccine research, and a mature oncology clinical infrastructure that systematically deploys liposomal therapeutics as standard of care across major academic medical centers.

U.S. Liposomes Market Size

The United States dominates North America with approximately 91% revenue share in 2026, estimated at around US$ 2.8 billion. With over 15 FDA-approved liposomal formulations, NCI-designated cancer centers deploying liposomal chemotherapy as standard protocols, and leading LNP vaccine manufacturers, including Pfizer and Moderna, headquartered domestically, the U.S. maintains commanding global market leadership.

Europe Liposomes Market Trends and Insights

Europe is the second-largest regional market, driven by strong EMA approval frameworks for liposomal drug products, EU Horizon Europe-funded nanomedicine research programs, and well-developed oncology treatment networks across Germany, the U.K., France, and Italy. Growing adoption of liposomal formulations in hospital formularies under national health system procurement agreements sustains consistent institutional revenue.

Germany Liposomes Market Size

Germany is Europe's largest liposomes market, estimated at approximately US$ 510 million in 2025, representing around 26% of European revenue. Germany's pharmaceutical manufacturing leadership, GKV insurance coverage for approved liposomal cancer therapies, and strong DFG-funded nanomedicine research programs at Helmholtz institutes drive consistent demand across both clinical and research end-users.

U.K. Liposomes Market Size

The United Kingdom holds approximately 18% of the European market share in 2026, valued at around US$ 353 million. NHS formulary approvals for liposomal doxorubicin and AmBisome, the UK Research and Innovation (UKRI)-funded drug delivery research ecosystem, and AstraZeneca's UK-based mRNA and LNP pipeline programs underpin strong market demand.

France Liposomes Market Size

France accounts for approximately 14% of the European liposomes market in 2026, estimated at around US$ 274 million. France's robust oncology hospital network, HAS-approved reimbursement for liposomal cancer drugs, and INSERM-funded nanomedicine research programs collectively drive consistent clinical and research segment demand for liposomal formulations.

Asia Pacific Liposomes Market Trends and Insights

Asia Pacific is the fastest-growing regional liposomes market, driven by rapidly expanding biopharma manufacturing capabilities, growing cancer patient populations, and substantial government investment in pharmaceutical innovation.

China is the dominant and fastest-growing national market, with the NMPA approving multiple domestic liposomal drug formulations and Chinese biopharma companies, including Luye Pharma Group and Shanghai New Asia Pharmaceutical, developing proprietary liposomal drug pipelines targeting both domestic and international markets.

India Liposomes Market Size

India is a high-growth liposomes market within Asia Pacific, estimated at approximately US$ 185 million in 2025, representing around 10% of regional revenue. India's large and growing cancer patient population, domestic generic liposomal drug manufacturing capabilities at companies including Sun Pharma Industries, and the CSIR-funded nanomedicine research ecosystem drive both clinical and R&D segment demand.

Competitive Landscape

The global liposomes market is highly competitive, supported by strong demand for targeted drug delivery, oncology treatments, and advanced vaccine formulations. Companies compete through innovation in lipid-based formulations, improved drug encapsulation efficiency, and enhanced stability for therapeutic applications. Strategic collaborations with pharmaceutical and biotechnology firms accelerate product development and commercialization. Continuous investments in nanotechnology, controlled-release systems, and personalized medicine strengthen market presence.

Key Developments

- In May 2026, Natural Field showcased its NFco-Loading® liposomal platform and introduced NF TriSolve® at Vitafoods Europe 2026 in Barcelona. The new formulation combined co-loaded Coenzyme Q10 and NMN liposomes with ergothioneine and sialic acid to support healthy aging, cellular vitality, skin radiance, and hydration.

- In September 2025, LipoActive, a spin-off from the University of Birmingham, partnered with Sibelius Natural Products to launch its novel liposomal technology, EncapSure, for the Asia-Pacific market. The technology was developed without silicon dioxide, PEG, and other restricted excipients, making it more suitable for clean-label nutraceutical applications in countries such as Japan.

- In February 2024, Pacira Biosciences signed a national group purchasing agreement with Brand Pharmaceuticals to distribute its liposome-based injectable products. They aim to increase access to pain management therapies and improve drug release and delivery for post-surgical pain care.

Companies Covered in Liposomes Market

- Novartis AG (Liposoma BV)

- Precision NanoSystems Inc

- Janssen Pharmaceutical Companies (Johnson & Johnson)

- Encapsula Nano Sciences

- Synpac-Kingdom Pharmaceutical Co., Ltd

- Celsion GmbH

- Gilead Sciences, Inc

- Pacira BioSciences, Inc.

- Luye Pharma Group

- Sun Pharma Industries Ltd

- Shanghai New Asia Pharmaceutical Co., Ltd.

- ENERGY DELIVERY SOLUTIONs

- Creative Biolabs

- Nanovex Biotechnologies SL

Frequently Asked Questions

The global liposomes market is estimated at US$ 8.1 billion in 2026.

The primary demand drivers for the Liposomes market include the rising need for targeted drug delivery systems that improve therapeutic efficacy while reducing side effects, especially in cancer treatment and antifungal therapies.

North America leads with approximately 38% of the global market share in 2025. The U.S. dominates at an estimated US$ 2.8 billion, driven by FDA-approved liposomal drug market leadership, NCI-endorsed clinical protocols deploying liposomal chemotherapy, NIH-funded LNP research, and U.S.-headquartered mRNA vaccine manufacturers.

The highest-growth opportunity lies in liposomal vaccines and gene delivery, with the WHO mRNA Technology Transfer Hub expanding LNP manufacturing to 15+ countries, NIAID-funded next-generation vaccine programs, and over 80 RNA-based therapies in clinical development per IQVIA 2024. CDMO services for liposomal gene therapy formulation development represent a high-margin, scalable revenue model.

Leading players include Gilead Sciences (AmBisome), Janssen Pharmaceutical Companies (Doxil), Pacira BioSciences (EXPAREL), Luye Pharma Group, Sun Pharma Industries, Novartis AG, Precision NanoSystems (Cytiva), and Creative Biolabs.