- Hardware & Software IT Services

- Last-Mile Delivery Software Market

Last-Mile Delivery Software Market Size, Share, and Growth Forecast 2026–2033

Last-Mile Delivery Software Market by Offering (Platform / Software, Services), Deployment (Cloud-Based, On-Premises, Hybrid), Application (Route Optimization & Planning, Fleet Management, Order Management & Dispatching, Real-Time Tracking & Visibility, Customer Communication & Notifications, Reverse Logistics Management, Others), Vertical and Regional Analysis, 2026–2033

Global Last-Mile Delivery Software Market Size and Trend Analysis

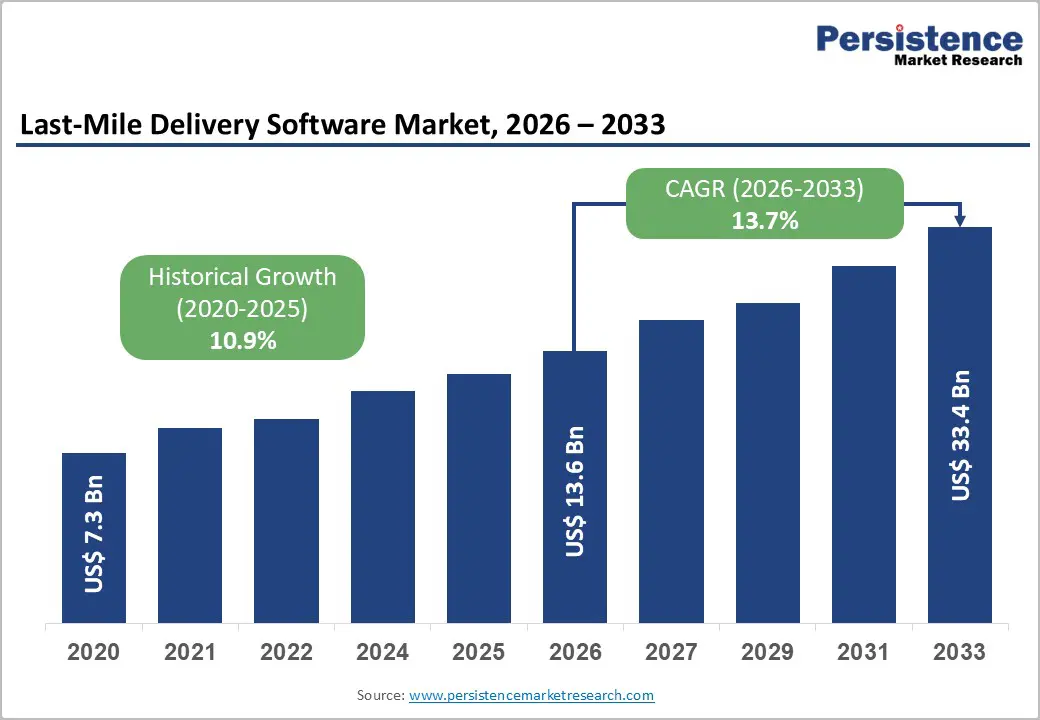

The global last-mile delivery software market is expected to be valued at US$ 13.6 billion in 2026 and is projected to reach US$ 33.4 billion by 2033, growing at a CAGR of 13.7% between 2026 and 2033, due to the rapid expansion of e-commerce, quick-commerce, and on-demand delivery ecosystems, which require real-time route optimization and delivery visibility. Retailers, logistics providers, and food delivery platforms are increasingly investing in AI-enabled dispatching, fleet tracking, and automated scheduling solutions to reduce delivery costs and improve customer experience. Rising urbanization and same-day delivery expectations are further accelerating adoption of cloud-based delivery management platforms.

Key Industry Highlights:

- Leading Offering: Platform / Software dominates the market with over 60.0% share in 2026, valued at approximately US$ 8.16 Bn, driven by enterprise demand for unified delivery orchestration, real-time visibility, route optimization, dispatch automation, and integrated analytics.

- Leading Deployment: On-Premises deployment holds more than 43.0% market share in 2026, valued at approximately US$ 5.85 billion, due to increasing enterprise focus on data security, regulatory compliance, and integration with legacy ERP and transportation systems.

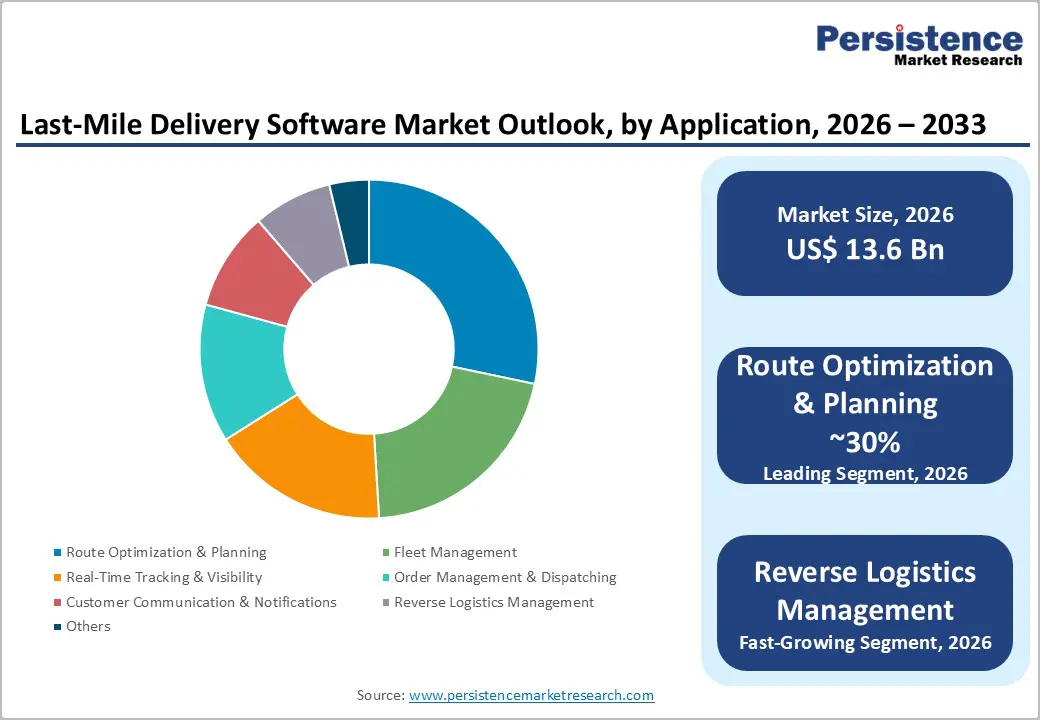

- Leading Application: Route optimization & planning accounts for around 30.0% of global market share in 2026, exceeding US$ 4.08 Bn, fueled by rising same-day delivery expectations, urban congestion challenges, and the need to reduce fleet operating costs through AI-driven routing intelligence.

- Fast-Growing Application: Reverse logistics management is the fast-growing application, supported by rapidly increasing e-commerce return volumes and rising demand for seamless return pickup and inventory reintegration workflows.

- Leading Vertical: Retail & E-commerce lead with over 38.0% market share in 2026, reaching approximately US$ 5.17 Bn, driven by explosive online shopping growth, increasing order volumes, and rising consumer expectations for rapid and transparent deliveries.

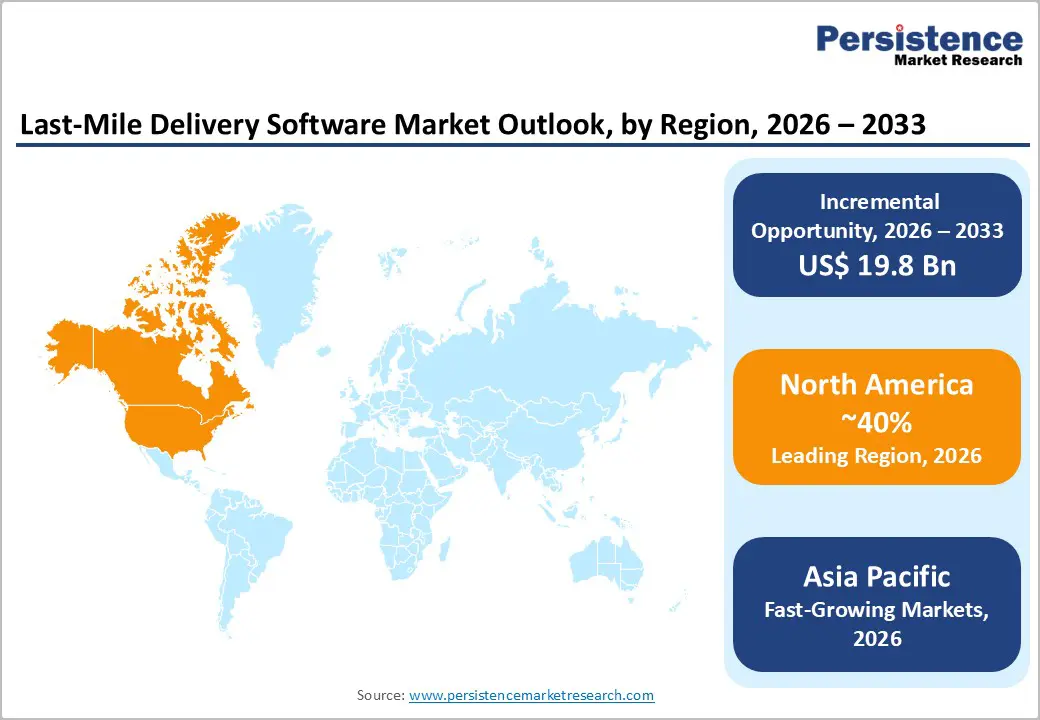

- Leading Region: North America dominates the market with approximately 40.0% share in 2026, valued at over US$ 5.44 Bn, supported by advanced logistics ecosystems, strong e-commerce penetration, and large-scale investments in AI-enabled delivery management technologies.

- Fast-Growing Market: Asia Pacific is the fast-growing regional market, projected to expand at a CAGR of 18.2% driven by smartphone-led commerce growth, rapid logistics digitization, quick-commerce expansion, and government-backed freight infrastructure modernization initiatives.

Market Dynamics

Drivers - Proliferation of E-Commerce Fulfilment Mandates Requiring Real-Time Delivery Intelligence

Retailers increasingly view real-time delivery visibility as a revenue-protection capability rather than a logistics convenience, as delayed or opaque deliveries directly impact customer retention and repeat purchase rates. In 2025, the U.S. Federal Trade Commission (FTC) continued stricter enforcement of the Mail, Internet, or Telephone Order Merchandise Rule, compelling online sellers to provide accurate delivery timelines and proactive delay notifications.

Walmart’s GoLocal network expanded its software-orchestrated last-mile operations across more than 11,000 pickup and delivery points in North America, enabling third-party merchants to access enterprise-grade fulfilment infrastructure. This transition is creating long-term, API-integrated software contracts that favour vendors with scalable orchestration and real-time analytics capabilities.

Urban Congestion Regulations Mandating Algorithmic Route Compliance

Urban low-emission and congestion-control regulations are transforming route optimization software from a fuel-efficiency tool into a mandatory compliance infrastructure layer for logistics operators. London’s expanded Ultra Low Emission Zone (ULEZ) continued imposing daily penalties of up to £100 on non-compliant commercial vehicles, accelerating the adoption of AI-driven routing systems among parcel and courier fleets.

More than 35 major European cities, including Paris, Amsterdam, Brussels, and Milan, are expected to enforce stricter zero-emission or restricted-access delivery zones by 2026 under broader EU decarbonisation initiatives. As compliance complexity rises across urban freight networks, demand is accelerating for last-mile delivery software that integrates regulatory intelligence, fleet telematics, and predictive route optimisation into a unified operational platform.

Restraints - Fragmented Data Infrastructure Across Multi-Carrier Delivery Networks

The lack of standardized data interchange protocols across carriers, shippers, and delivery platforms continues to restrain the adoption of last-mile delivery software, particularly among mid-sized logistics operators. In 2025, GS1 highlighted that inconsistent logistics data structures and poor data synchronization remain a major source of operational inefficiencies across global supply chains.

The absence of a universally adopted last-mile API framework forces software vendors to allocate nearly 15–25% of deployment budgets toward custom integration and data normalization layers. Vendors with pre-built carrier connector ecosystems maintain a strong competitive advantage, while newer entrants face longer implementation cycles and margin pressure during customer onboarding.

Cybersecurity Liability Exposure in Cloud-Connected Delivery Platforms

Last-mile platforms absorb sensitive customer location data, payment records, and real-time vehicle telemetry; they become high-value targets under frameworks such as the EU General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), where breach penalties scale with the volume of personally identifiable records exposed. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) flagged transportation software systems as critical infrastructure in its 2023 National Cybersecurity Strategy, adding compliance overhead that smaller vendors struggle to absorb.

This dynamic disproportionately burdens early-stage SaaS entrants, which cannot amortize SOC 2 Type II audit costs and enterprise-grade security architecture across a large installed base, compressing net retention and extending break-even timelines.

Opportunities - Autonomous and Semi-Autonomous Delivery Robotics Integration Layer

Software vendors positioning their platforms as the orchestration layer for autonomous delivery hardware, including drones, sidewalk robots, and autonomous delivery vans, are expected to capture recurring integration, monitoring, and fleet-management revenue as commercial robotics deployments scale beyond pilot programs.

Route optimization providers and middleware vendors with open API architecture are particularly well positioned to monetize this opportunity by enabling interoperability between robotics hardware, warehouse systems, and retailer fulfilment platforms. As retailers and logistics operators seek scalable automation to offset labour shortages and rising delivery costs, demand will increase for software capable of coordinating mixed autonomous and human-operated fleets in real time.

Healthcare and Pharmaceutical Last-Mile Compliance Software

Healthcare logistics operators managing temperature-sensitive pharmaceutical deliveries represent a structurally underpenetrated buyer segment with both high software willingness-to-pay and stringent regulatory compliance requirements that commoditised platforms cannot serve. The U.S. Drug Supply Chain Security Act (DSCSA), which reached its full enforcement milestone in November 2024, mandates end-to-end electronic traceability of prescription drug shipments, a requirement that pharmaceutical distributors such as McKesson Corporation are addressing through purpose-built last-mile tracking and chain-of-custody software. Vendors capable of combining cold-chain monitoring, regulatory audit trails, and real-time exception management within a unified delivery platform are best positioned to capture this segment, as long as they achieve 21 CFR Part 11 electronic records compliance.

Category-wise Analysis

Offering Insights

Platform/software is likely to command over 60% of the global last-mile delivery software market in 2026, as enterprises require a unified operational layer to manage deliveries, fleets, customer communication, and order visibility in real time. Operators increasingly prefer centralized systems that integrate routing, dispatch, proof-of-delivery, and analytics into one platform to reduce operational complexity.

Businesses also need scalable digital infrastructure capable of handling seasonal order spikes and multi-city delivery networks. Integration with ERP, warehouse management, and transportation systems further strengthens adoption among enterprise buyers.

Services is the fast-growing segment, as many mid-sized logistics operators lack internal expertise to configure, customize, and maintain advanced delivery platforms. Businesses increasingly depend on external partners for implementation, API integration, fleet onboarding, workflow optimization, and real-time operational support.

As delivery networks become more technology-intensive, enterprises require consulting and managed services to ensure smooth deployment and faster return on investment.

Deployment Insights

On-premises deployment is likely to account for more than 43% share in 2026, valued at US$ 5.85 Billion, due to enterprises prioritizing data security, operational control, and regulatory compliance. Companies handling sensitive shipment information, customer data, healthcare deliveries, or financial transactions prefer maintaining infrastructure within internal environments.

Many established operators also rely on legacy ERP and transportation systems that integrate more efficiently with on-premises architecture. Internal hosting provides greater customization flexibility and minimizes dependence on external cloud providers.

Hybrid deployment is the fastest-growing mode, as logistics operators require both cloud scalability and secure internal data management. Hybrid models also help businesses scale rapidly during high-demand periods while maintaining compliance with regional data governance policies. The need for flexible, cost-efficient, and interoperable logistics infrastructure is making hybrid deployment the preferred modernization pathway for many delivery enterprises.

Application Insights

Route optimization & planning captures 30% of the global last-mile delivery software market in 2026, exceeding US$ 4.08 billion, due to delivery operators need to minimize fuel costs, delivery delays, and driver inefficiencies across increasingly dense urban networks. Rising same-day and next-day delivery expectations require software capable of dynamically adjusting routes based on traffic, weather, order priority, and vehicle capacity. Businesses also use route optimization tools to improve fleet utilization and reduce operational expenses while maintaining service-level agreements.

Reverse Logistics Management is the fastest-growing application, as e-commerce expansion has significantly increased product return volumes across retail categories. Businesses require specialized software to coordinate return pickups, inventory inspection, refund processing, and warehouse reintegration efficiently. Consumers increasingly expect seamless and convenient return experiences, especially for apparel, electronics, and grocery deliveries. Companies also aim to reduce losses associated with failed returns and excess inventory holding costs.

Vertical Insights

Retail & e-commerce accounts for over 38% share in 2026, due to the explosive growth of online shopping and rising consumer expectations for rapid, transparent, and flexible delivery experiences. E-commerce platforms require advanced last-mile software to manage high daily order volumes, real-time shipment visibility, proof-of-delivery workflows, and customer communication across geographically distributed delivery networks. Peak seasonal demand fluctuations further increase the need for scalable software infrastructure capable of optimizing routes and delivery capacity instantly.

Food & grocery delivery is the fast-growing vertical, due to the rapid expansion of quick-commerce and hyperlocal delivery models promising grocery fulfilment within minutes rather than hours. Food delivery operators require highly responsive software capable of managing live order inflow, rider dispatch, perishable inventory coordination, and traffic-aware route optimization simultaneously. Consumer demand for convenience, restaurant aggregation, and instant grocery delivery have increased operational complexity beyond what traditional dispatch systems handle.

Regional Insights

North America Last-Mile Delivery Software Market Trends and Insights

North America accounts for approximately 40% of the global market share in 2026, reaching over US$ 5.44 billion, supported by the strong presence of large-scale e-commerce retailers, parcel carriers, grocery delivery networks, and advanced digital logistics ecosystems.

High consumer expectations for same-day and next-day delivery have accelerated investments in route optimization, fleet visibility, dispatch automation, and AI-enabled delivery management platforms. The U.S. Infrastructure Investment and Jobs Act, which allocated substantial funding toward transportation and freight infrastructure modernization, is strengthening demand for integrated logistics and last-mile technology solutions.

The United States last-mile delivery software market is expected to exceed US$ 4.62 billion by 2026, driven by large-scale spending from national parcel operators, third-party logistics providers, food delivery platforms, and omnichannel retailers managing millions of daily delivery transactions. Companies continue investing heavily in AI-driven route planning, driver productivity analytics, predictive ETA systems, and automated dispatch technologies to improve delivery efficiency and reduce operating costs. The adoption of electric delivery fleets, micro-fulfilment centres, and pilot drone delivery programs is further increasing the need for sophisticated software orchestration platforms.

Europe Last-Mile Delivery Software Market Trends and Insights

Europe accounts for over 27% of the global last-mile delivery software market in 2026, representing approximately US$ 3.67 Billion, supported by strong e-commerce penetration, stringent urban mobility regulations, and rapid logistics digitalization across major economies. Regulatory frameworks such as the EU Urban Mobility Framework and expanding Zero Emission Zones across Germany, France, and the Netherlands are accelerating the adoption of AI-enabled routing, fleet monitoring, and emissions-tracking software platforms.

Germany last-mile delivery software market is expected reach over US$ 840 million, driven by its position as Europe’s largest parcel logistics and fulfilment hub. Germany’s dense multi-carrier courier, express, and parcel (CEP) ecosystem generates substantial operational complexity, encouraging widespread deployment of route optimization, dispatch automation, and predictive delivery software. The country’s high parcel volumes, supported by strong B2C e-commerce activity and industrial supply chain integration, make manual fleet coordination economically inefficient for large operators.

United Kingdom last-mile delivery software market is expected to exceed over US$ 800 million, while France contributes nearly US$ 700 million. The UK market benefits from one of Europe’s highest online retail penetration rates, alongside growing consumer expectations for same-day and time-slot deliveries, which are increasing demand for AI-assisted route planning and proof-of-delivery platforms. France’s market growth is supported by national logistics modernization initiatives and rising urban population density, particularly in Paris and other metropolitan clusters. French logistics operators are increasingly deploying cloud-based delivery management systems to improve dispatch visibility, reduce delivery cycle times, and optimize high-density urban delivery routes, supporting continued expansion of the regional software ecosystem.

Asia Pacific Last-Mile Delivery Software Market Trends and Insights

Asia Pacific Last-Mile Delivery Software market is expected to exceed over US$ 3.40 Billion in value in 2026 and is projected to remain the fastest-growing regional market with an estimated CAGR of 18.2% through 2033, driven by the rapid expansion of smartphone-led e-commerce, increasing penetration of quick-commerce platforms, and accelerated logistics digitization across emerging Asian economies. Governments across the region are strengthening logistics infrastructure through large-scale national initiatives. These programmes are expanding freight connectivity into Tier-2 and Tier-3 cities, thereby increasing the addressable market for route optimization, fleet orchestration, and delivery execution software.

China represents the largest Asia Pacific market, accounting for more than 43.0% of regional revenue in 2026, equivalent to nearly US$1.46 billion, owing to its dominant position in global parcel delivery volumes and highly digitalized commerce ecosystem.

Japan valued at approximately US$ 610 million in 2026, due to structural labour shortages and stricter driver overtime regulations introduced under Japan’s 2024 logistics reforms. These pressures are compelling parcel carriers to deploy advanced route optimization, delivery scheduling, and load-consolidation software to sustain operational efficiency with constrained workforce availability.

India is expected to reach high by accelerating among hyperlocal delivery operations, D2C brands, and organized retail logistics providers. Expansion of the Open Network for Digital Commerce ecosystem is encouraging logistics firms to integrate interoperable APIs and digitally standardized fulfilment workflows, thereby increasing software penetration among regional and mid-sized carriers. South Korea represents approximately US$ 480 million in 2026, supported by dense urban delivery networks and extremely high e-commerce adoption rates. Operators such as Coupang are leveraging predictive routing, AI-driven dispatch systems, and ultra-fast fulfilment infrastructure to strengthen delivery capabilities, creating sustained demand.

Competitive Landscape

The global last-mile delivery software market operates within a tiered competitive structure where large enterprise providers dominate through deep integration capabilities and long-term platform contracts, while specialized vendors compete through advanced routing intelligence and vertical-specific workflow flexibility.

Competition has increasingly shifted toward AI-driven route optimization and real-time exception management, with delivery response speed becoming a critical differentiator. Mid-market platforms are gaining traction by enabling faster and lower-complexity deployments for retailers and logistics operators. Predictive ETA accuracy, scalability of carrier integrations, and operational visibility are now the primary benchmarks influencing customer retention and platform renewal decisions.

Key Developments:

- In May 2026, Amazon launched Amazon Supply Chain Services (ASCS), allowing businesses to use its end-to-end logistics network for inventory storage, fulfillment, shipping, and last-mile delivery operations. The move highlights growing convergence between logistics infrastructure and AI-enabled last-mile delivery software platforms, intensifying competition across the global delivery ecosystem.

- In June, 2025: Descartes Systems Group acquired PackageRoute to strengthen its final-mile delivery management capabilities, including route optimization, driver mobility, and real-time delivery visibility. The acquisition enhances Descartes’ SaaS logistics ecosystem and reflects ongoing consolidation in the global last-mile delivery software market driven by e-commerce growth and delivery automation.

Global Last-Mile Delivery Software Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 7.31 Billion |

|

Current Market Value (2026) |

US$ 13.60 Billion |

|

Projected Market Value (2033) |

US$ 33.41 Billion |

|

CAGR (2026–2033) |

13.7% |

|

Leading Region |

North America, 40.0% Share |

|

Dominant Offering |

Platform / Software, 60.0% Share |

|

Top-ranking Application |

Route Optimization & Planning, 30.0% Share |

|

Incremental Opportunity |

US$ 19.81 Billion |

Companies Covered in Last-Mile Delivery Software Market

- Oracle Corporation

- SAP SE

- Descartes Systems Group

- Microsoft Corporation

- Amazon.com Inc.

- FedEx Corporation

- United Parcel Service (UPS)

- DHL Group

- Zebra Technologies Corporation

- Onfleet Inc.

- FarEye Technologies

- Locus.sh

- LogiNext Solutions Inc.

- Bringg Delivery Technologies

- Others

Frequently Asked Questions

The global last-mile delivery software market is valued at US$ 13.60 billion in 2026 and is projected to reach US$ 33.41 billion by 2033, driven by rising demand for same-day and next-day delivery. E-commerce companies and logistics providers increasingly require software to improve delivery speed, visibility, and customer experience.

The growth is driven by stricter urban emissions regulations and rising compliance requirements in pharmaceutical logistics. Businesses increasingly need route optimization and electronic traceability software to reduce operational costs, meet regulatory standards, and improve delivery efficiency.

Route Optimization & Planning holds the largest application segment share over 30.0% as it directly reduces fuel consumption and driver costs, which are the biggest last-mile delivery expenses. Companies adopt these solutions to improve operational efficiency, delivery accuracy, and profit margins.

North America dominates the global last-mile delivery software market with more than 40.0% revenue share in 2026, due to the strong presence of large e-commerce, retail, and logistics companies adopting advanced delivery technologies. High digital infrastructure investment and increasing focus on faster delivery services continue to strengthen regional demand.

A major opportunity lies in software platforms supporting autonomous and human delivery fleets together. Growing adoption of drones and autonomous delivery vehicles is creating demand for intelligent fleet orchestration, real-time monitoring, and API-based integration platforms.

Oracle Corporation, SAP SE, Descartes Systems Group, Microsoft Corporation, Amazon.com Inc., FedEx Corporation, DHL Group, Zebra Technologies Corporation among Others.