- Specialty & Fine Chemicals

- Isophthalic Acid Market

Isophthalic Acid Market Size, Share and Growth Forecast, 2026 - 2033

Isophthalic Acid Market by Application (PET copolymer, Unsaturated polyester resins, Surface coating, Others), End-user (Textile industry, Automotive industry, Construction, Marine, Others), and Regional Analysis for 2026 - 2033

Isophthalic Acid Market Share and Trends Analysis

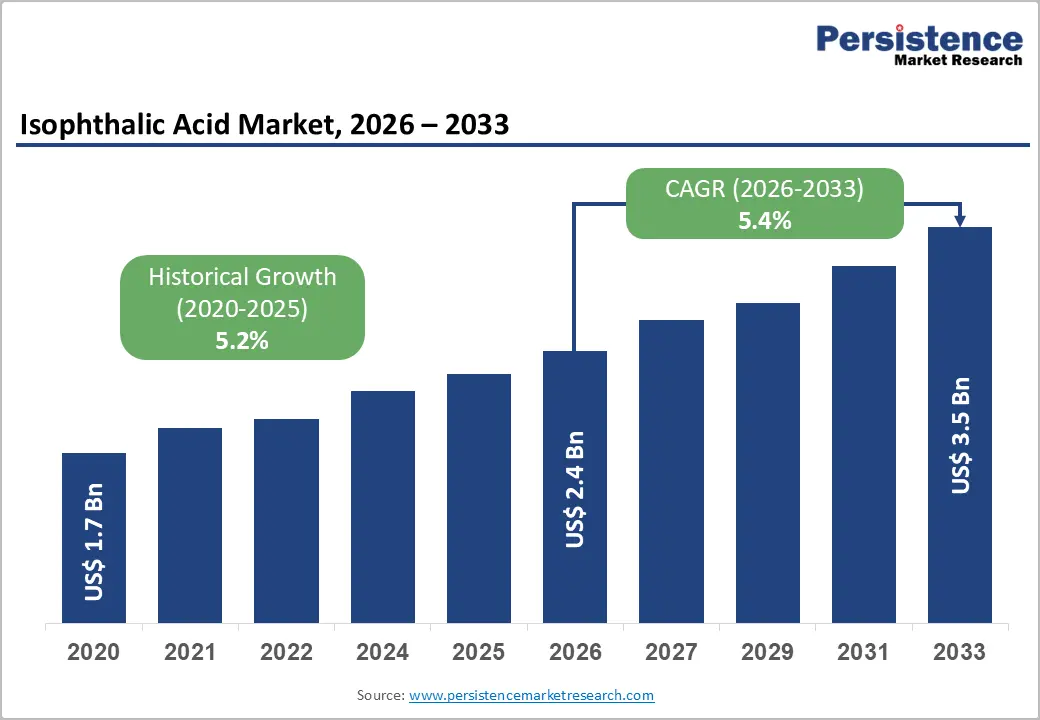

The global isophthalic acid market size is likely to be valued at US$ 2.4 billion in 2026 and is projected to reach US$ 3.5 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026 - 2033, driven by increasing demand for PET copolymer solutions, which enhance thermal stability and clarity in packaging applications.

Expanding use of unsaturated polyester resins (UPR) in construction and marine composites further strengthens consumption. Additionally, rising infrastructure development and automotive lightweighting trends are accelerating adoption. The market also benefits from consistent demand in surface coating applications, where chemical resistance and durability are critical performance requirements.

Key Industry Developments:

- Application Segment Trend: PET copolymer is expected to lead with around 42% share in 2026, while unsaturated polyester resins are projected to grow the fastest, driven by demand for lightweight and corrosion-resistant composites in packaging, construction, and automotive sectors.

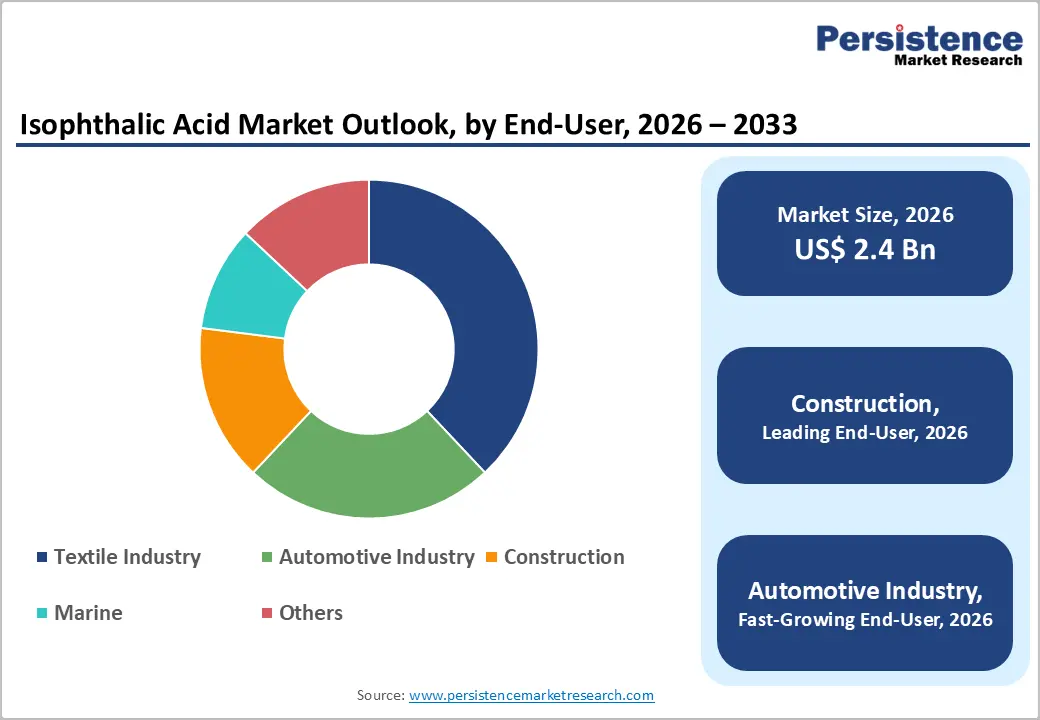

- End-use Industry Trend: Construction is set to hold about 38% share in 2026, while automotive is expected to be the fastest growing through 2033, supported by lightweighting, emission norms, and rising composite adoption.

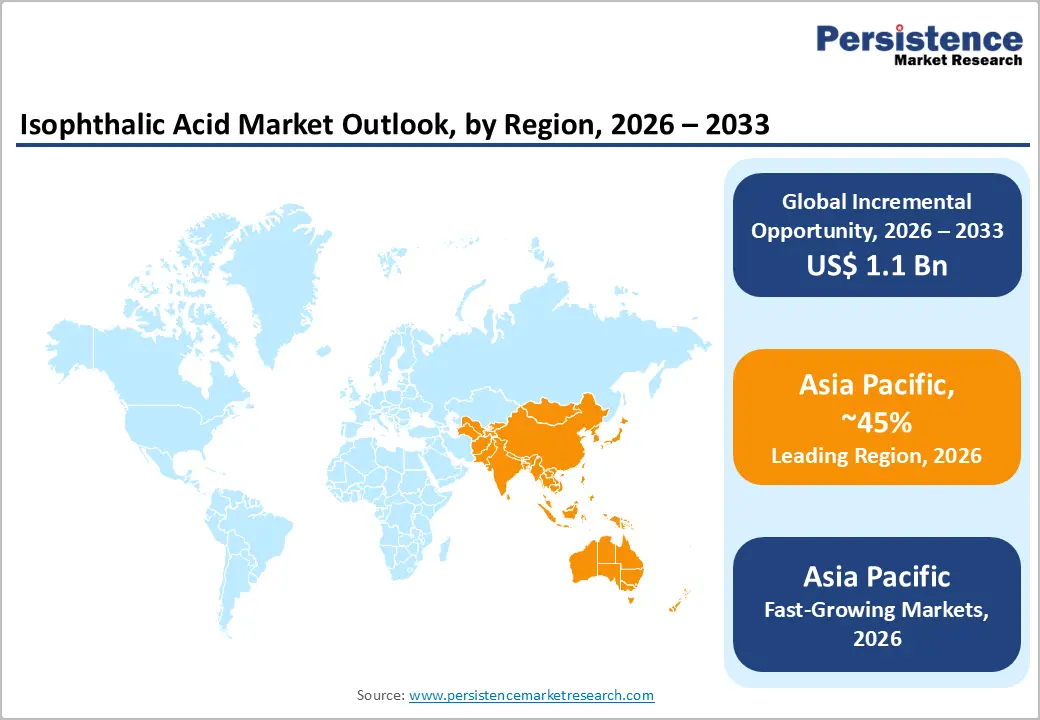

- Regional Leadership: Asia Pacific is likely to dominate with nearly 45% share in 2026 and is expected to grow the fastest through 2033, led by strong petrochemical capacity, industrialization, and infrastructure expansion in China and India.

- Key Growth Drivers: Growth is driven by rising demand for sustainable polymers, increasing use of high-performance resins, and accelerating global infrastructure development.

- Competitive Landscape: The market is moderately consolidated, with top players holding a majority share, competing through capacity expansion, integration, and resin innovation.

DRO Analysis

Driver - Rising Demand for PET Copolymer in Packaging and Industrial Applications

The increasing global demand for high-performance packaging materials is a key driver for the market, particularly in PET copolymer production. According to industry assessments aligned with packaging consumption trends reported by the OECD and plastics associations, PET demand has grown steadily due to recyclability and lightweight properties. Isophthalic acid enhances clarity, strength, and thermal resistance in PET bottles, making it highly valuable for beverage and food packaging industries.

The shift toward sustainable packaging, reinforced by regulatory frameworks such as the EU Single-Use Plastics Directive, is increasing adoption. As global packaged food consumption rises with urbanization and e-commerce expansion, demand for PET copolymers containing isophthalic acid continues to expand significantly.

Manufacturers and packaging producers are focusing on improving material performance while reducing environmental impact, which is strengthening the adoption of isophthalic acid-based formulations. Its ability to enhance product stability and processing efficiency makes it highly suitable for high-volume manufacturing environments.

Restraint - Volatility in Raw Material Prices and Petrochemical Dependency

One of the most critical constraints for the isophthalic acid market is the volatility of raw material prices, particularly paraxylene and crude oil derivatives, which are essential feedstocks. According to energy market insights from the International Energy Agency (IEA), crude oil price fluctuations directly impact aromatics supply chains, increasing production uncertainty. Additionally, supply chain disruptions, especially in Asia Pacific petrochemical hubs, further exacerbate procurement instability. These structural dependencies on fossil-based inputs limit long-term pricing stability and pose sustainability challenges amid global decarbonization initiatives.

This volatility creates cost unpredictability, making it difficult for manufacturers to maintain stable pricing and long-term contracts. It also disrupts downstream planning in industries such as packaging and coatings due to fluctuating input costs. Frequent price swings reduce operational efficiency across the value chain and delay procurement decisions. Exposure to geopolitical and supply chain risks further intensifies uncertainty.

Opportunity - Expansion of Bio-based and Sustainable Polymer Applications

A major opportunity for isophthalic acid lies in the development of bio-based and sustainable polymer systems. With global regulatory bodies such as the European Chemicals Agency (ECHA) promoting low-emission materials, manufacturers are increasingly shifting toward recyclable and hybrid polyester systems. Isophthalic acid is being widely used in advanced resin formulations that enhance durability while supporting sustainability goals. This is creating strong growth potential across packaging, automotive composites, and coatings, with significant incremental demand expected over the forecast period.

Recent regulatory actions, particularly in Europe, are accelerating this transition, especially in Europe. The European Union’s Packaging and Packaging Waste Regulation is enforcing higher recyclability and recycled-content requirements, pushing packaging producers such as major FMCG beverage companies to redesign PET bottles using performance-enhancing additives such as isophthalic acid.

Similarly, global automotive OEMs are increasing the adoption of lightweight composite materials to meet stricter emission norms, supporting resin innovation. In parallel, Japan’s green manufacturing initiatives and corporate net-zero commitments from leading food packaging brands are reinforcing demand for sustainable polyester systems. These real-world transitions are directly strengthening long-term growth opportunities for the market.

Category-wise Analysis

The PET copolymer segment is estimated to lead the isophthalic acid market with 42% share in 2026, supported by rising demand for recyclable, high-performance packaging systems. A key shift is the tightening of packaging sustainability regulations, including California’s SB 54 implementation phase and the UK’s evolving deposit return scheme rollout, which is expected to accelerate redesign of FMCG and beverage packaging toward higher recyclability and performance PET systems.

The unsaturated polyester resins segment is estimated to be the fastest growing through 2033, driven by increasing use in infrastructure and renewable energy composites. The continued expansion of offshore wind capacity additions across Europe and the U.S. is expected to increase demand for resin-based composite blades and structural components used in turbine systems. This is anticipated to significantly strengthen high-performance thermoset resin consumption across industrial applications.

End-user Insights

The construction industry is estimated to lead the isophthalic acid market with 38% share in 2026, driven by infrastructure modernization and urban expansion. The ongoing execution of large-scale public infrastructure investment programs such as the U.S. Infrastructure Investment and Jobs Act and India’s National Infrastructure Pipeline is expected to boost demand for durable, corrosion-resistant composite materials in construction and utility applications.

The automotive industry is estimated to be the fastest-growing through 2033, supported by electrification and tightening emission regulations. A key shift includes enforcement of updated EU Battery Regulation requirements and stricter vehicle emission compliance frameworks in multiple regions, which is expected to accelerate the adoption of lightweight composite materials in EV platforms and structural components for improved efficiency and emission reduction.

Regional Analysis

North America Isophthalic Acid Market Trends

North America is estimated to account for 22% of the global market share in 2026, supported by a mature petrochemical ecosystem and strong downstream demand from packaging and industrial coatings. The region is witnessing a gradual shift toward recyclable and low-emission polymer systems, driven by regulatory tightening and corporate sustainability commitments. This transition is expected to reinforce PET copolymer adoption and maintain steady, innovation-led demand across end-use industries.

U.S. Isophthalic Acid Market Trends

The U.S. is estimated to contribute nearly 48% of regional demand, driven by large-scale packaging and automotive composite applications supported by integrated chemical hubs along the Gulf Coast. In 2025-2026, the rollout and expansion of extended producer responsibility (EPR) packaging frameworks across multiple U.S. states is expected to accelerate the shift toward recyclable PET-based packaging formats.

Canada Isophthalic Acid Market Trends

Canada is estimated to hold around 15% regional share in 2026, with steady growth supported by infrastructure modernization and material efficiency programs, where investments in construction upgrades and recycling systems are likely to improve the adoption of durable polymer-based materials in coatings and infrastructure applications.

Europe Isophthalic Acid Market Trends

Europe is estimated to hold 25% of the market share in 2026, driven by stringent environmental regulations and a strong transition toward circular and low-emission material systems. Demand is expected to remain concentrated in unsaturated polyester resins for construction and marine applications, supported by ongoing sustainability-led material substitution across industries. This regulatory-driven shift is anticipated to strengthen Europe’s position as a high-value, innovation-driven market.

Germany Isophthalic Acid Market Trends

Germany is estimated to lead with nearly 28% of regional demand in 2026, supported by its advanced automotive and chemical manufacturing base. The expanding industrial decarbonization initiatives and EV supply chain localization programs are expected to accelerate the adoption of lightweight composite materials in automotive production.

France Isophthalic Acid Market Trends

France is estimated to contribute around 18% of the regional demand in 2026, driven by infrastructure renewal and coastal protection projects, where investments in coastal resilience and water infrastructure modernization are likely to increase the use of corrosion-resistant resin systems in civil engineering applications.

Asia Pacific Isophthalic Acid Market Trends

Asia Pacific is estimated to dominate the global market with a 45% share in 2026, driven by large-scale manufacturing, rapid urbanization, and strong downstream polymer consumption. The region is expected to remain the key global demand center, supported by expanding petrochemical capacity and cost-efficient production ecosystems. Growth is likely to be reinforced by rising demand across the packaging, infrastructure, and automotive sectors.

China Isophthalic Acid Market Trends

China is estimated to account for nearly 40% of regional consumption in 2026, supported by extensive petrochemical infrastructure and strong demand from the packaging and construction industries. The ongoing industrial upgrading initiatives and expansion of low-carbon manufacturing zones are expected to increase the adoption of advanced polyester materials across packaging and industrial applications.

India Isophthalic Acid Market Trends

India is estimated to hold close to 20% share in 2026, driven by infrastructure expansion and rising packaging consumption, where the continued rollout of national infrastructure corridor projects and expansion of domestic manufacturing clusters are likely to strengthen demand for resin-based construction materials and packaging-grade polymers.

Competitive Landscape

The global isophthalic acid market is moderately consolidated, with major players such as BASF, Eastman Chemical Company, ExxonMobil Chemical, INEOS Group, SABIC, and Mitsubishi Chemical Group collectively holding an estimated 55-60% share. Their dominance is supported by strong feedstock integration, large-scale production capacity, and established downstream linkages with PET copolymer and polyester resin industries. Competitive advantage is primarily driven by scale efficiency and long-term supply contracts with key end-use sectors.

Market leaders are focusing on capacity expansion, backward integration, and the development of high-performance and sustainable resin solutions to strengthen their downstream presence. Regional producers, particularly in Asia Pacific, are expanding rapidly through cost-efficient production and new capacity additions in China and India. High entry barriers, such as capital intensity and raw material dependency, limit new entrants, while strategic partnerships and consolidation continue to shape competitive dynamics in the market.

Companies Covered in Isophthalic Acid Market

- BASF SE

- Eastman Chemical Company

- ExxonMobil Chemical

- INEOS Group

- Mitsubishi Chemical Group

- SABIC

- Reliance Industries Limited

- Dow Inc.

- Lotte Chemical Corporation

- LG Chem

- Solvay S.A.

- Polynt Group

- Chang Chun Group

- Formosa Chemicals & Fibre Corporation

Frequently Asked Questions

The global isophthalic acid market is projected to reach US$ 2.4 billion in 2026.

Rising demand for PET copolymer packaging, expanding use of polyester resins in construction, and increasing automotive lightweighting needs drive the market.

The isophthalic acid market is expected to grow at a CAGR of 5.4% from 2026 to 2033.

Growing adoption of sustainable polymers and expansion of high-performance resin applications across packaging and infrastructure create key opportunities.

Key players include BASF SE, Eastman Chemical Company, ExxonMobil Chemical, INEOS Group, SABIC, and Mitsubishi Chemical Group.