- Bulk Chemicals

- Global Isobutane Market

Global Isobutane Market Size, Share, and Growth Forecast 2026–2033

Global Isobutane Market by Grade (Technical Grade, Pure Grade, Instrument Grade, Others), by Application (Refrigerant, Fuel Blending, Aerosol Propellant, Chemical Intermediate, Solvent & Others), by Distribution Channel (Direct Sales, Indirect Sales), by End Use (Refrigeration & Air Conditioning, Chemical & Petrochemical, Aerosols & Personal Care, Automotive, Pharmaceutical & Others), by Regional Analysis, 2026–2033

Global Isobutane Market Size and Trend Analysis

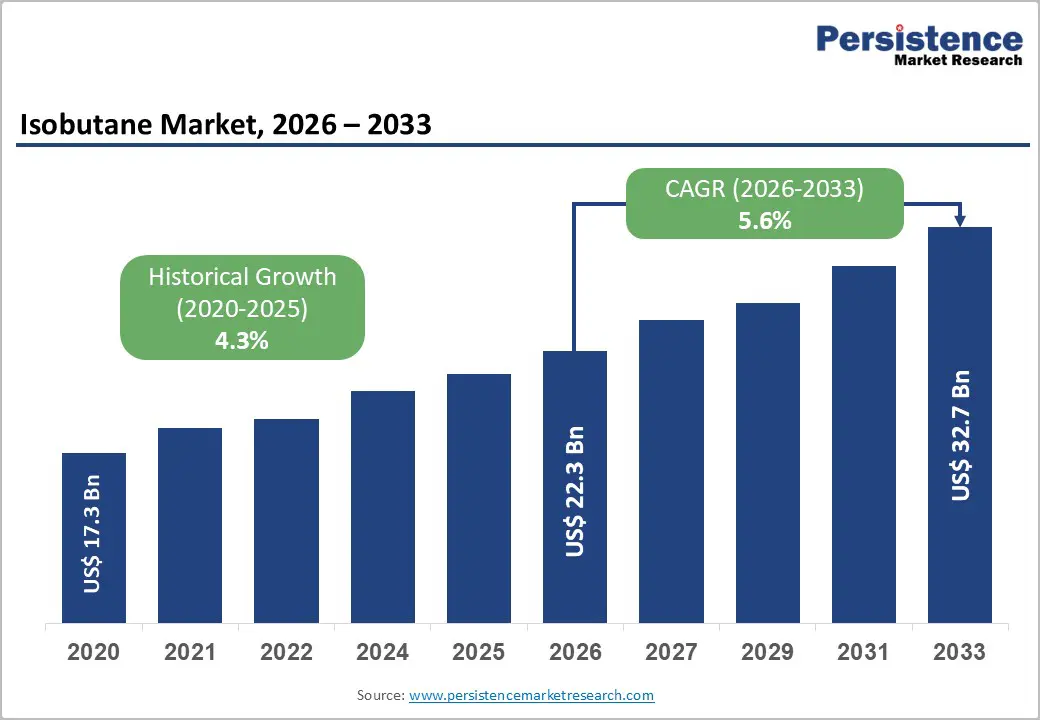

The global isobutane market is expected to be valued at US$ 22.30 Billion in 2026 and is projected to reach US$ 32.66 Billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. The global isobutane market is a vital segment of the hydrocarbon and specialty gas industry, driven by its extensive use in refrigerants, petrochemical feedstocks, fuel blending, and aerosol propellants. Growing demand for environmentally friendly refrigerants, expanding refinery operations, and increasing consumption across refrigeration and automotive sectors are supporting steady market growth worldwide.

Key Market Highlights

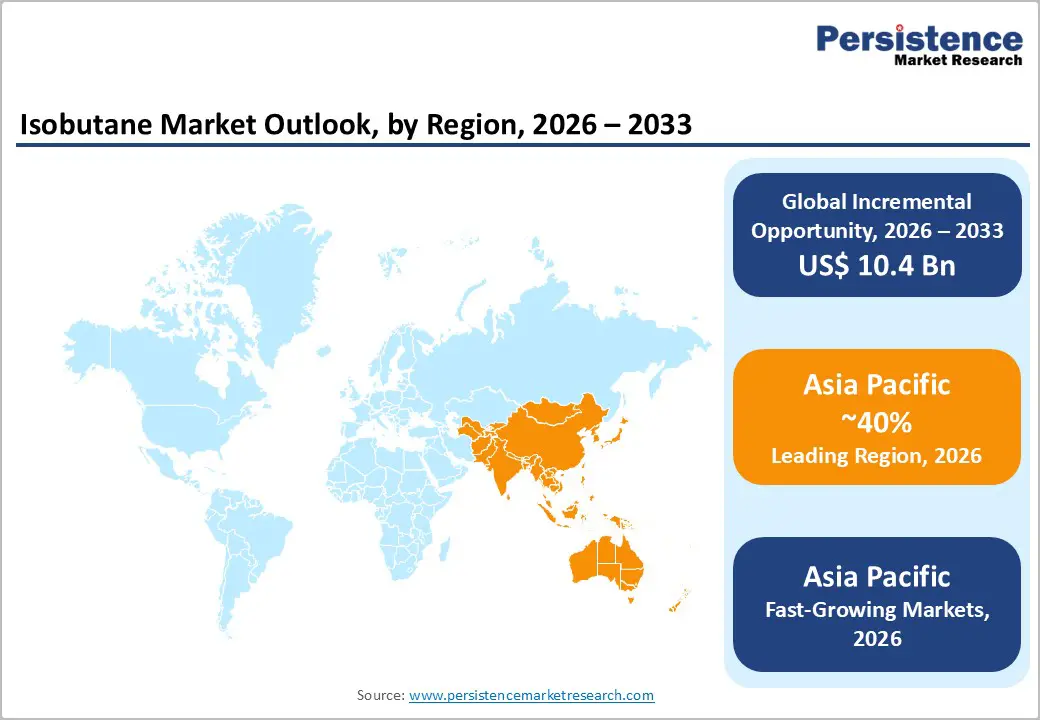

- Leading Region: Asia Pacific holds the largest share of the global isobutane market at 40.0% in 2026, valued at US$ 8.92 Billion. Growth is driven by expanding petrochemical capacity in China, cold-chain investments in India, and rising appliance manufacturing across Southeast Asia.

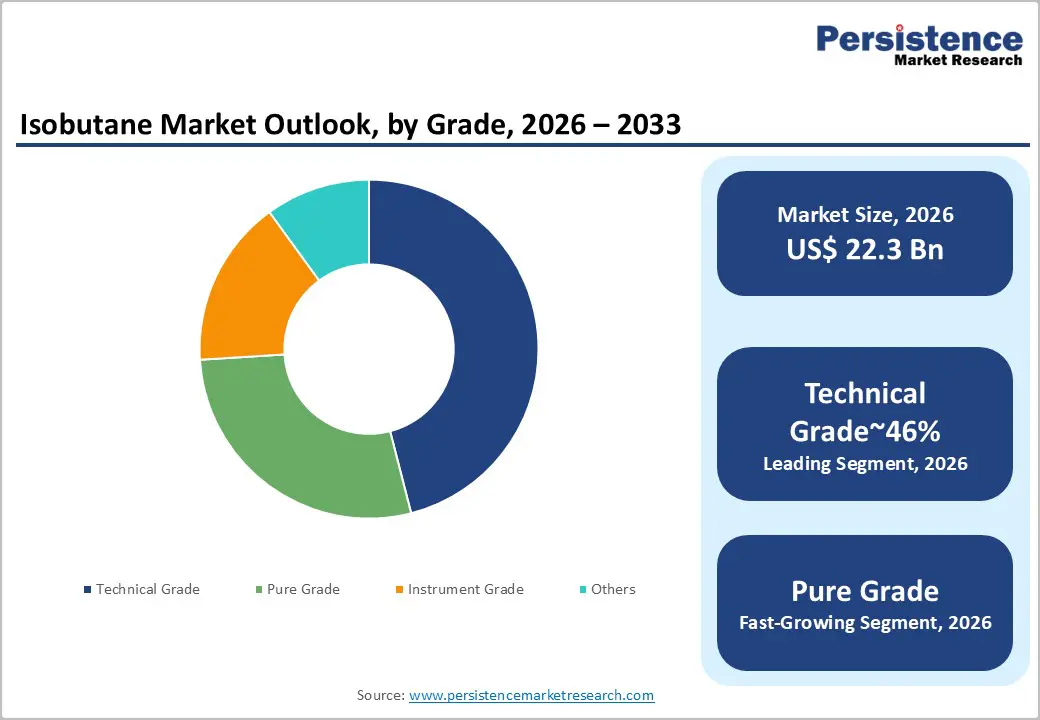

- Leading Segment: Technical Grade isobutane leads the market with a 46.0% share, supported by its extensive use in refinery alkylation and refrigerant applications where cost efficiency is a key purchasing factor.

- Fastest Growing Segment: Refrigeration & Air Conditioning accounts for the largest end-use share at 31.0%, driven by strong adoption of isobutane-based natural refrigerants in household refrigerators across Europe and Asia, with North America increasingly following this trend.

- Key Opportunity: Fuel Blending is emerging as a major growth opportunity. Stricter fuel regulations in the U.S. are increasing demand for alkylate gasoline, creating attractive growth prospects for refinery-integrated isobutane producers through 2033.

Market Dynamics

Market Growth Drivers

Accelerating Regulatory Phase-Out of High-GWP Refrigerants Creating Structural Demand for R-600a

Refrigerant transitions mandated by supranational climate frameworks are generating a non-discretionary demand floor for isobutane that appliance manufacturers cannot defer. The U.S. Environmental Protection Agency's (EPA) SNAP Rule 23, finalised in 2023, expanded the list of approved hydrocarbon refrigerants, including R-600a, for household refrigerators and freezers, formally unlocking the North American OEM conversion market.

Whirlpool Corporation announced in 2023 its commitment to converting North American refrigerator production lines to R-600a-compatible systems, a capital-intensive shift that signals multi-year isobutane offtake contracts with petrochemical feedstock suppliers. Over the next two to three years, similar OEM conversions cascading across Southeast Asian appliance manufacturers, particularly in Vietnam and Thailand, will amplify regional isobutane procurement volumes substantially.

Rising Aerosol Propellant Demand Driven by Personal Care and Pharmaceutical Spray Markets

Isobutane's role as a hydrocarbon solvent and aerosol propellant in personal care, deodorants, hairsprays, and dry shampoos, is expanding as formulators exit chlorofluorocarbon and hydrofluorocarbon propellants under global aerosol industry compliance timelines. The Consumer Specialty Products Association (CSPA) reported in 2024 that hydrocarbon propellants now account for an estimated 65% of aerosol propellant volume used in U.S. personal care products, with isobutane and n-butane blends dominating that share.

Henkel AG reformulated its Schwarzkopf professional haircare aerosol line in 2023 to replace HFC-152a with isobutane-based propellant blends, illustrating the scale of reformulation activity underway across Tier-1 FMCG players. Pharmaceutical dry-powder inhaler manufacturers are expected to follow a parallel transition path as the FDA finalises propellant guidance updates through 2026, opening an additional high-margin application channel.

Market Restraints

Flammability Classification Limiting Isobutane Adoption in Large Commercial and Industrial Refrigeration

Isobutane's A3 flammability classification under IEC 60335-2-89, the international safety standard for commercial refrigeration appliances, imposes strict charge-size limits, currently capped at 150 grams per circuit in most commercial configurations that technically exclude R-600a from large-format supermarket display cases and industrial chillers.

This ceiling confines the addressable refrigerant market for isobutane to household and small commercial units, compressing the total serviceable demand relative to the broader refrigeration industry. New entrants targeting the commercial refrigeration segment face disproportionate engineering and certification costs to design around these charge-size constraints, effectively reinforcing the incumbency of HFO blends such as R-448A in large commercial installations.

Supply Chain Concentration and Crude Oil Price Volatility Compressing Refiner Margins

Isobutane is primarily recovered as a refinery gas stream during petroleum refining and natural gas processing, making its supply intrinsically linked to crude oil throughput decisions by major integrated refiners.

When crude margins tighten, as experienced during the OPEC+ production cut cycles of 2023–2024, which reduced global refinery run rates at certain facilities, isobutane availability tightens disproportionately, creating spot price spikes that erode the cost advantage isobutane holds over synthetic alternatives. For downstream formulators operating on fixed-price aerosol or refrigerant supply contracts, this feedstock volatility translates directly into margin compression, particularly for smaller regional blenders lacking the hedging infrastructure of integrated chemical majors.

Market Opportunities

Isobutane as Petrochemical Feedstock for Alkylation Units Offering Premium-Value Offtake Channel

Refinery operators and independent alkylation unit owners should actively develop isobutane supply agreements with petrochemical producers seeking to expand alkylate gasoline output, as this application commands significantly higher netbacks than commodity LPG blending.

The U.S. Department of Energy's (DOE) Bipartisan Infrastructure Law (2021) allocated funding for clean fuel infrastructure that indirectly stimulates alkylate demand by supporting high-octane, low-volatility gasoline blending, a specification where isobutane-derived alkylate excels. Integrated refiners with captive isobutane recovery streams, such as Valero Energy Corporation, are best positioned to capture this opportunity, provided they invest in isomerisation capacity expansions that convert normal butane into the isobutane feedstock required by alkylation reactors.

Emerging Natural Refrigerant Adoption in Asia Pacific Cold Chain Infrastructure

Equipment manufacturers and gas distributors supplying Southeast and South Asian cold chain operators represent the highest-growth isobutane demand pocket through 2033, given the region's nascent but rapidly expanding organised retail refrigeration infrastructure.

India's National Cold Chain Policy, updated in 2022 under the Ministry of Commerce and Industry, prioritised energy-efficient refrigeration systems for fresh produce storage, a mandate that is pulling forward adoption of hydrocarbon refrigerants in standalone coolers and small walk-in units across tier-2 and tier-3 cities. Industrial gas distributors with last-mile cylinder logistics networks in India and Vietnam are best positioned to capture this opportunity, contingent on safety standard harmonisation between national bodies such as the Bureau of Indian Standards (BIS) and international IEC norms progressing through 2026.

Category-wise Insights

Grade Analysis

Technical Grade accounts for 46.0% of the global isobutane market in 2026, equivalent to US$ 10.26 Billion, making it the leading purity segment across high-volume industrial applications. Refinery-recovered isobutane with 95 to 98% purity is widely used in refrigerant blending, LPG blending, and alkylation feedstock applications where ultra-high purity is not required. Major appliance manufacturers using R-600a and fuel additive producers depend on long-term supply contracts from integrated petrochemical companies. According to the American Petroleum Institute (API), U.S. refinery operations consistently produce technical-grade isobutane, ensuring stable and reliable supply for this segment.

Pure Grade isobutane is the fastest growing segment, supported by rising demand from pharmaceutical aerosol and precision cooling applications requiring purity levels above 99.5%. Growth is also driven by the need for controlled impurity profiles in metered-dose inhalers (MDIs) and specialty refrigerants. In 2024, Linde plc expanded its specialty gas purification capacity in Singapore to support pharmaceutical-grade hydrocarbon propellants across Asia. As manufacturers shift toward low-climate-impact inhalers under updated WHO guidance, demand for pure-grade isobutane is expected to grow steadily through 2028.

Application Analysis

Refrigerant accounts for 34.0% of the global isobutane market in 2026, equivalent to US$ 7.58 Billion, driven by the widespread use of R-600a in household refrigerators and freezers across Europe, Asia, and North America. Leading appliance manufacturers such as Electrolux and Miele have adopted R-600a across most refrigeration products. Each unit typically requires 30–100 grams of isobutane, creating strong cumulative demand. The International Institute of Refrigeration (IIR) reports that over 95% of new household refrigerators in Europe already use hydrocarbon refrigerants, strengthening long-term market stability.

Fuel Blending is the fastest growing application segment, supported by rising refinery demand for alkylate and high-octane LPG blends that meet stricter fuel standards. Refiners are increasingly using isobutane to comply with gasoline volatility and octane regulations under U.S. EPA Tier 3 standards. In 2023, Phillips 66 expanded alkylation capacity at its Ponca City refinery to boost premium gasoline production, increasing isobutane consumption. Growing adoption of Reid Vapor Pressure (RVP) regulations, particularly supported by the California Air Resources Board (CARB), will continue driving demand through 2030.

Distribution Channel Analysis

Direct Sales accounts for 71.0% of the global isobutane market in 2026, equivalent to US$ 15.83 Billion, reflecting the market’s strong reliance on large-volume contract-based procurement. Refrigerant manufacturers, appliance OEMs, and petrochemical companies source isobutane directly from producers such as ExxonMobil Chemical and Chevron Phillips Chemical Company through long-term agreements covering supply volume, purity, delivery, and pricing. These contracts ensure uninterrupted supply and lower transaction costs. Bulk transport systems regulated by the Pipeline and Hazardous Materials Safety Administration (PHMSA) further support the dominance of direct distribution networks.

Indirect Sales is the fastest growing distribution channel, driven by increasing demand from small and medium-sized businesses involved in aerosol manufacturing, pharmaceutical compounding, and cold-chain refrigeration. Distributors and specialty gas suppliers play an important role by offering smaller delivery volumes, technical support, and regulatory assistance. Since 2023, Matheson Tri-Gas, Inc. has expanded its specialty cylinder distribution network across Latin America and Southeast Asia to serve growing regional demand. Rising SME participation in India, Indonesia, and Brazil is expected to support strong indirect channel growth through 2033.

End Use Analysis

Refrigeration & Air Conditioning accounts for 31.0% of the global isobutane market in 2026, equivalent to US$ 6.91 Billion, supported by the appliance industry’s long-term adoption of R-600a as a preferred natural refrigerant. Manufacturers producing household refrigerators and commercial freezers continue to rely heavily on isobutane-based cooling systems. Companies associated with Haier Group supply large volumes of chest freezers across Asia and Africa, with each unit requiring 50 to 90 grams of isobutane. According to the United Nations Environment Programme (UNEP), household refrigeration remains the largest global application for natural refrigerants, ensuring stable long-term demand.

Chemical & Petrochemical is the fastest growing end-use segment, driven by increasing investments in isobutane dehydrogenation (IDH) projects across China and the Middle East. Isobutane is widely used to produce isobutylene, an important raw material for MTBE, butyl rubber, and polyisobutylene manufacturing. In 2023, Wanhua Chemical Group started operations at its large propane and butane dehydrogenation complex in Shandong Province, significantly increasing isobutane feedstock consumption. Rising demand for synthetic rubber, adhesives, and specialty chemicals from Asia’s automotive and industrial sectors will continue supporting market expansion through 2033.

Regional Insights

North America Isobutane Market Trends and Insights

North America accounts for 32.0% of the global isobutane market in 2026, representing US$ 7.14 Billion, supported by the continent's deep refinery infrastructure, robust aerosol manufacturing base, and the EPA's accelerating approval of hydrocarbon refrigerants across new appliance categories. The U.S. Energy Information Administration (EIA) reported that U.S. natural gas plant liquids production, which includes isobutane recovery, reached approximately 6.7 million barrels per day in 2023, providing an abundant domestic feedstock base. Expanding alkylation capacity investments at Gulf Coast refineries are expected to sustain North America's position as both the largest isobutane-producing and one of the highest-consuming regions through 2030.

- United States Isobutane Market Size

The United States commands an estimated 78% of the North American isobutane market, driven by its concentration of petroleum refining capacity, aerosol product manufacturing in the Midwest and Southeast, and a rapidly growing household refrigerator conversion market following EPA SNAP Rule 23 approvals. Forward demand from the appliance sector, where GE Appliances and Samsung Electronics America are engineering R-600a-compatible refrigerator platforms for U.S. retail, will progressively add structured volume to isobutane procurement over the 2025–2028 product cycle.

Europe Isobutane Market Trends and Insights

Europe accounts for 18.0% of the global isobutane market in 2026, representing US$ 4.01 Billion, shaped decisively by the EU's F-Gas Regulation (EU) 2024/573, which mandates a near-complete phase-out of HFCs above GWP 150 in new stationary refrigeration equipment by 2027. The European Fluorocarbon Technical Committee (EFCTC) has documented an accelerating market share gain for natural refrigerants, including R-600a, in European household appliance markets since 2022, with isobutane-charged models now representing the majority of new refrigerator shipments in Germany, France, and the UK. Europe's established aerosol industry, centred on the FEICA supply chain, further sustains regional isobutane propellant demand.

- Germany Isobutane Market Size

Germany represents an estimated 28% of the European isobutane market, anchored by its position as Europe's largest household appliance manufacturing hub and home to BSH Hausgeräte, which produces R-600a-charged refrigerators at its Giengen and Nauen facilities for both domestic and export markets. Germany's Climate Action Programme 2030 provides fiscal incentives for energy-efficient appliances, accelerating replacement cycles and pulling forward R-600a demand from OEM factory fill and after-sales service channels.

- United Kingdom Isobutane Market Size

The United Kingdom holds an estimated 16% of European isobutane market revenue, supported by a mature aerosol personal care manufacturing sector, the UK is one of Europe's top-five aerosol-producing nations per the British Aerosol Manufacturers' Association (BAMA), and active participation in the post-Brexit UK F-Gas Regulation framework, which mirrors EU HFC phase-down timelines. Growing demand for hydrocarbon-propelled dry shampoos and deodorants from UK-based consumer goods manufacturers is providing a stable incremental pull on isobutane propellant volumes through 2030.

- France Isobutane Market Size

France represents approximately 14% of the European regional isobutane market, with demand concentrated in the aerosol cosmetics and pharmaceutical spray sectors centred around the Paris and Lyon industrial corridors. L'Oréal S.A., headquartered in Clichy, France, has publicly committed to eliminating high-GWP propellants from its global aerosol portfolio by 2025, driving reformulation activity that is increasing isobutane and butane blend offtake from French aerosol contract fillers. France's RE2020 thermal regulation, which mandates energy performance improvements in new buildings, is also prompting HVAC system upgrades that favour low-GWP refrigerants including R-600a in residential split systems.

Asia Pacific Isobutane Market Trends and Insights

Asia Pacific accounts for 40.0% of the global isobutane market in 2026, representing US$ 8.92 Billion, and is the fastest growing region at a projected CAGR of 7.5%, powered by China's massive petrochemical dehydrogenation investment programme, India's cold chain expansion, and Southeast Asia's aerosol manufacturing growth. China's 14th Five-Year Plan explicitly prioritised propylene and butylene capacity additions through dehydrogenation routes, directly increasing demand for isobutane as a petrochemical feedstock across the Shandong, Jiangsu, and Guangdong petrochemical clusters. As Asian appliance brands continue to scale R-600a-charged refrigerator exports into Africa and Latin America, the region's isobutane consumption profile will increasingly reflect both domestic and export-oriented OEM demand.

- China Isobutane Market Size

China commands an estimated 52% of Asia Pacific isobutane market revenue, underpinned by its role as the world's largest appliance manufacturer and its rapidly expanding isobutane dehydrogenation and alkylation complex footprint. Rongsheng Petrochemical's Zhoushan integrated refining and chemical project, one of the world's largest greenfield petrochemical complexes, includes butane processing units that generate significant isobutane streams available for downstream chemical and refrigerant applications. Continued urbanisation driving household appliance penetration in inland provinces will sustain domestic refrigerant-grade isobutane demand well beyond the current forecast horizon.

- India Isobutane Market Size

India accounts for an estimated 17% of Asia Pacific isobutane market revenue, with demand accelerating across refrigerant, aerosol propellant, and cold chain refrigeration end uses as urbanisation and organised retail penetration deepen. Indian Oil Corporation (IOC) operates refinery-integrated LPG fractionation units at Haldia and Panipat that recover isobutane streams, providing a domestic supply foundation for the growing aerosol and refrigerant blending industry. India's Faster Adoption and Manufacturing of Electric Vehicles (FAME III) policy trajectory and expanding cold storage infrastructure under the PM Kisan Sampada Yojana scheme are jointly accelerating isobutane demand from both automotive-adjacent and food cold chain sectors.

- Japan Isobutane Market Size

Japan holds an estimated 12% of Asia Pacific isobutane market revenue, driven by its precision-oriented industrial gas sector and the pharmaceutical aerosol manufacturing concentration in the Osaka and Nagoya corridors. Iwatani Corporation, Japan's leading industrial gas distributor, supplies high-purity isobutane to domestic aerosol and electronic gas calibration customers under specialty cylinder programmes, with demand for instrument-grade product growing alongside Japan's semiconductor process gas quality requirements. Japan's Green Growth Strategy Through Achieving Carbon Neutrality in 2050 has also prompted Panasonic to accelerate its residential air conditioner lineup transition toward low-GWP refrigerants, creating structured R-600a demand in the small split-system segment.

Competitive Landscape

The global isobutane market operates as a moderately concentrated oligopoly at the production level, with ExxonMobil Corporation, Linde plc, and Air Liquide collectively commanding leading positions through integrated refinery recovery, purification, and specialty gas distribution capabilities. The primary basis of competition centres on supply chain integration, producers with captive isobutane recovery streams from refinery operations hold structural cost advantages over pure-play specialty gas distributors.

The dominant strategic theme entering 2026 is grade diversification: integrated players are investing in purification capacity to serve high-margin pharmaceutical and instrument-grade segments alongside their commodity refrigerant and fuel blending volumes. INEOS Group represents the most notable competitive disruptor, having expanded its hydrocarbon refrigerant blending and distribution footprint across Europe and North America since 2022 specifically to capture OEM refrigerant conversion volumes driven by F-Gas regulatory pressure.

Key Market Developments:

- January 2024: Linde plc commissioned a new specialty isobutane purification unit at its Singapore facility, targeting pharmaceutical aerosol propellant customers across Asia Pacific seeking ≥99.5% purity R-600a for metered-dose inhaler reformulation programmes.

- March 2024: Chevron Phillips Chemical Company announced a capacity expansion at its Cedar Bayou, Texas facility to increase isobutane recovery and processing throughput, responding to growing alkylate gasoline demand from Gulf Coast refinery customers seeking to comply with tightening U.S. EPA Tier 3 octane specifications.

- October 2023: INEOS Group finalised a long-term isobutane supply agreement with a major European household appliance manufacturer, supporting the customer's full transition of refrigerator factory-fill operations from HFC-134a to R-600a across three Central European production sites.

Companies Covered in Global Isobutane Market

- Exxon Mobil Corporation

- Linde plc

- Air Liquide

- Chevron Phillips Chemical Company

- ConocoPhillips

- Sinopec

- TotalEnergies

- Shell Chemicals

- INEOS Group

- LyondellBasell

- Valero Energy Corporation

- Praxair Technology, Inc.

- TPC Group

- Evonik Industries

- MATHESON Tri-Gas, Inc.

- Iwatani Corporation

- Rongsheng Petrochemical

- Indian Oil Corporation (IOC)

- Wanhua Chemical Group

- Honeywell International

- SHV Energy

Frequently Asked Questions

The global isobutane market is valued at US$ 22.30 Billion in 2026 and is forecast to reach US$ 32.66 Billion by 2033, advancing at a CAGR of 5.6%. The primary growth catalyst is the accelerating regulatory phase-out of high-GWP synthetic refrigerants under multilateral climate frameworks, driving structural OEM conversion to R-600a across household appliance manufacturing globally.

Two specific drivers dominate: first, expanding alkylation feedstock demand stimulated by U.S. EPA Tier 3 fuel standards requiring higher-octane, lower-volatility gasoline blendstocks; and second, pharmaceutical aerosol propellant reformulation activity accelerating as the World Health Organisation promotes low-climate-impact metered-dose inhaler propellants across its member state healthcare systems. Both drivers are generating new, structurally durable demand channels beyond traditional bulk LPG blending.

Technical Grade isobutane holds the largest grade segment share at 46.0%, driven by its suitability for bulk refrigerant blending, alkylation feedstock, and LPG blending applications where cost efficiency outweighs purity requirements. This segment's dominance is structurally stable because refinery-recovered isobutane inherently meets technical grade specifications, aligning supply economics with the largest demand pools without additional purification capital expenditure.

Asia Pacific dominates the global isobutane market with a 40.0% share in 2026, driven by two structural factors: China's world-scale isobutane dehydrogenation and petrochemical complex investment, including projects under the country's 14th Five-Year Plan, and the region's status as the global centre of gravity for household appliance manufacturing. Asia Pacific's isobutane demand trajectory is set to strengthen further as India's organised cold chain infrastructure scales and Southeast Asian aerosol manufacturing capacity expands through 2033.

The highest-conviction opportunity is the pharmaceutical-grade isobutane propellant segment, where MDI reformulation programmes across Asia Pacific and Europe are creating premium-priced, specification-driven demand that integrated specialty gas producers with dedicated purification assets are best positioned to serve. This opportunity materialises most fully if national pharmacopoeia bodies, including the European Pharmacopoeia Commission, codify hydrocarbon propellant purity specifications that create a defensible quality compliance barrier against commodity-grade material entering the pharmaceutical supply chain.

ExxonMobil Corporation, Linde plc, Air Liquide, and Chevron Phillips Chemical Company lead the global isobutane market, competing primarily on supply chain integration, purification capability, and long-term contract relationships with OEM refrigerant and petrochemical customers. The competitive landscape is moderately concentrated at the production tier but fragments significantly at the distribution level, where regional specialty gas distributors such as MATHESON Tri-Gas, Inc. compete on service capability, cylinder logistics, and technical support rather than feedstock cost.