- Medical Devices

- Infectious Disease In-vitro Diagnostics Market

Infectious Disease In-vitro Diagnostics Market Size, Share, and Growth Forecast, 2026 – 2033

Infectious Disease In-vitro Diagnostics Market by Product Type (Instruments, Reagents & Kits, Software & Services), Technology (Immunoassay, Molecular Diagnostics, Others), Application (HIV, Hepatitis B & Hepatitis C, Others), and Regional Analysis for 2026 - 2033

Infectious Disease In-vitro Diagnostics Market Share and Trends Analysis

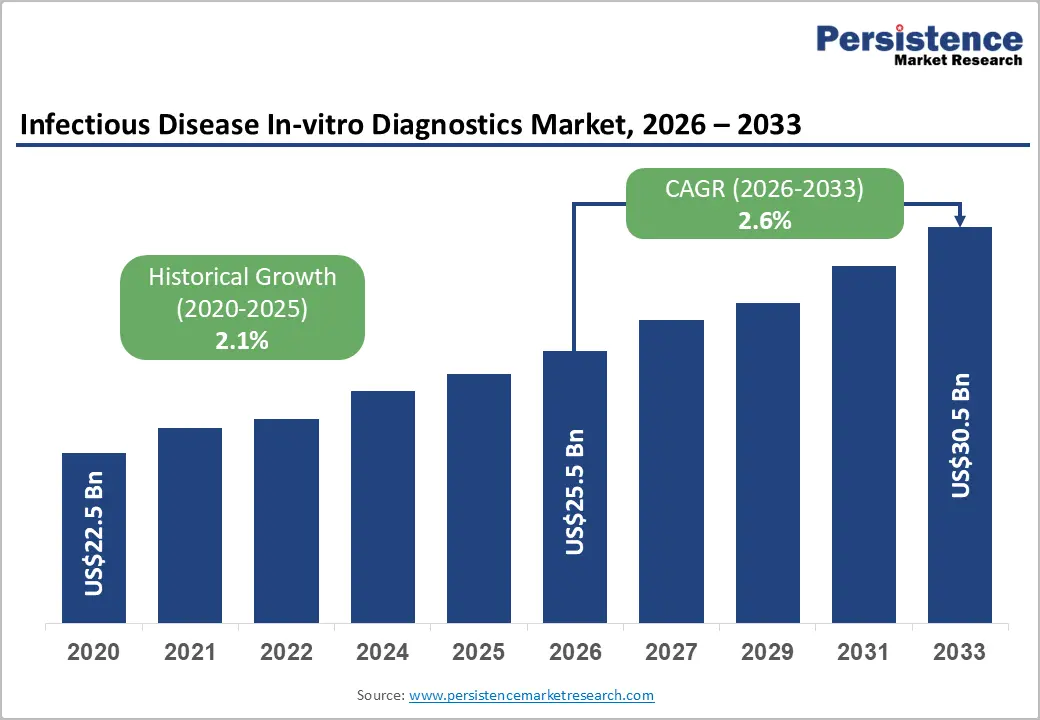

The global infectious disease In-vitro diagnostics market size is likely to be valued at US$25.5 billion in 2026 and is estimated to reach US$30.5 billion by 2033, growing at a CAGR of 2.6% during the forecast period from 2026 to 2033, driven by rising infectious disease surveillance requirements, increasing diagnostic testing volumes, and wider deployment of rapid testing platforms across healthcare systems. Aging populations and rising immunocompromised patient pools are strengthening demand for continuous disease monitoring and early-stage diagnosis.

Key Industry Highlights:

- Leading Technology: Molecular diagnostics is set to hold around 35% revenue share in 2026, driven by superior clinical sensitivity in hospital and public health laboratory settings.

- Fastest-Growing Technology: Next-generation sequencing is projected as the fastest-growing segment, supported by declining sequencing costs and expanding antimicrobial resistance profiling applications.

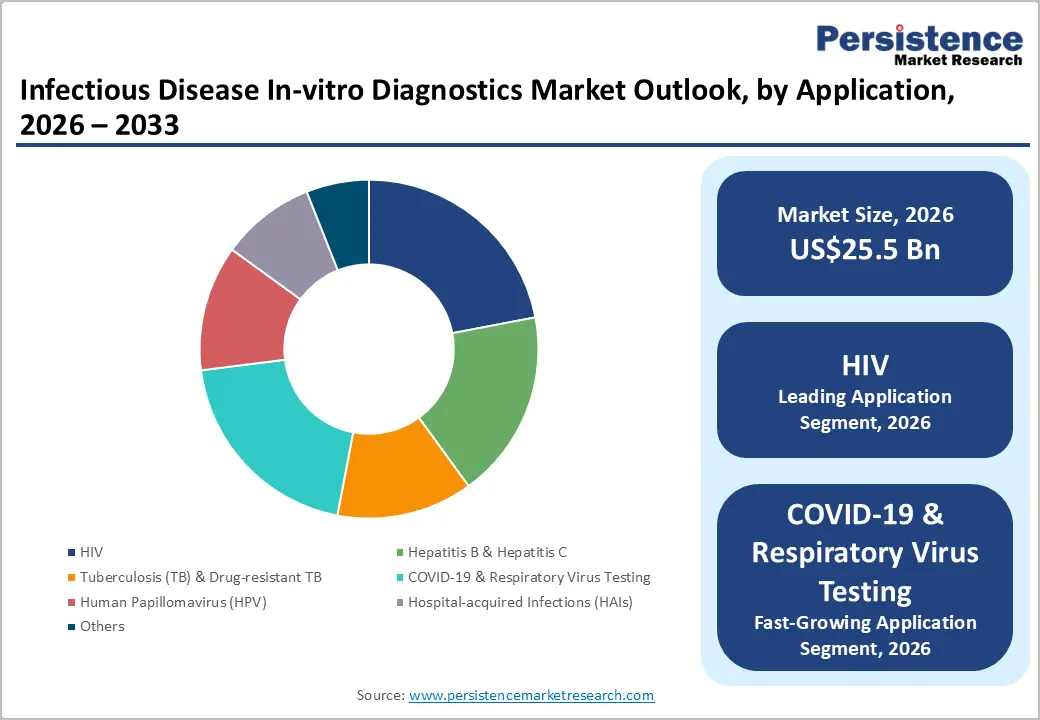

- Leading Application: HIV is estimated to hold roughly 22% revenue share in 2026, driven by globally mandated testing and treatment monitoring programs across high-burden geographies.

- Fastest-growing Application: COVID-19 and respiratory virus testing is forecast to record the fastest growth, driven by rising multiplex PCR panel adoption across emergency and ambulatory care settings.

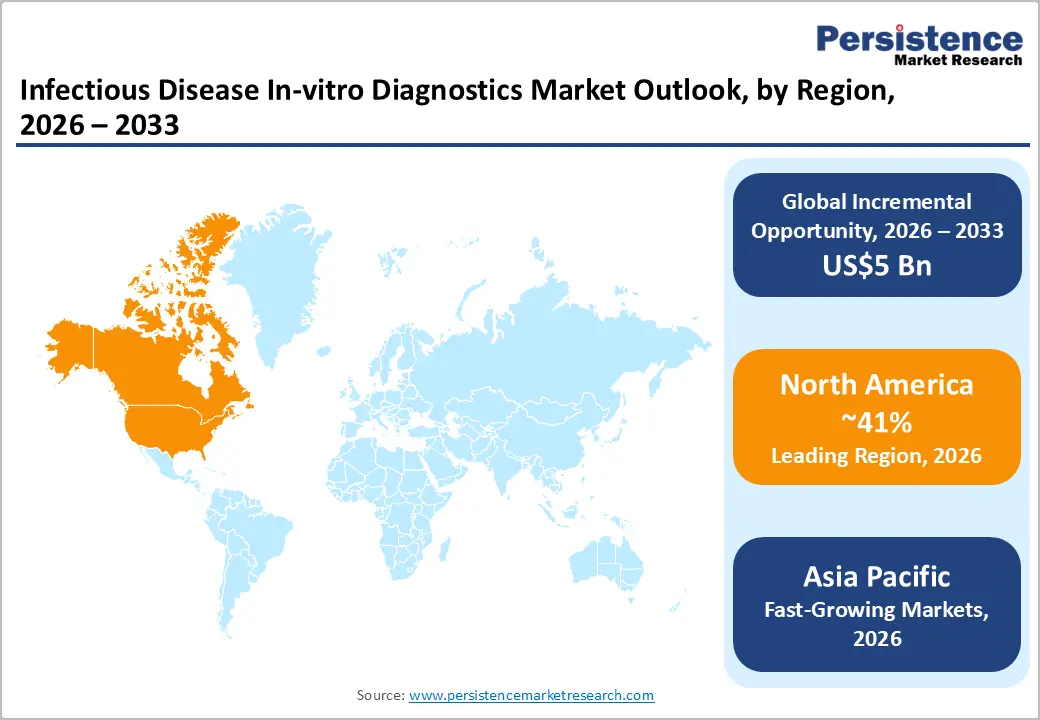

- Regional Leadership: North America is projected to capture roughly 41% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to expanding healthcare infrastructure.

- Competitive Environment: The market is moderately consolidated, with Roche, Abbott, Danaher, bioMerieux, and Siemens Healthineers collectively accounting for the majority of global revenue.

DRO Analysis

Driver - Expansion of Government-led Infectious Disease Surveillance Programs

Public health authorities are increasing investment in national disease surveillance systems to strengthen early detection capabilities and outbreak response efficiency. Expansion of laboratory networks and mandatory screening programs is creating sustained demand for molecular and immunoassay diagnostic products. The U.S. Centers for Disease Control and Prevention reported more than 10,260 tuberculosis cases in the United States during 2025, indicating continued diagnostic testing demand across public healthcare laboratories.

Large-scale procurement initiatives for respiratory virus, HIV, hepatitis, and antimicrobial resistance testing are improving utilization rates of automated diagnostic instruments. Healthcare agencies are implementing real-time reporting infrastructure, leading laboratories to adopt interoperable software and high-throughput testing systems. Integration of surveillance databases with hospital laboratories is increasing routine testing frequency, supporting long-term reagent consumption and recurring service revenues for diagnostic manufacturers.

Restraint - High Dependence on Complex Supply Chains

Diagnostic manufacturers rely heavily on specialized raw materials, semiconductor components, enzymes, and precision optics sourced through international supply chains. Disruptions in transportation networks or component availability can delay instrument production and reagent delivery schedules. Rising procurement costs are reducing manufacturing margins and limiting scalability for mid-sized suppliers operating with lower inventory flexibility.

Cold-chain storage requirements and strict quality validation processes increase operational expenses across distribution networks. Healthcare providers in cost-sensitive regions often postpone equipment upgrades due to budget limitations and maintenance expenses. Limited local manufacturing capacity for advanced molecular consumables creates dependency on imports, increasing exposure to currency fluctuations and trade-related procurement instability.

Opportunity - Expansion of Point-of-Care and Decentralized Testing Infrastructure

Healthcare systems are increasingly focusing on decentralized diagnostic access to improve disease detection in outpatient and community settings. Portable molecular analyzers and rapid immunoassay platforms are enabling testing closer to patients, reducing laboratory congestion and treatment initiation delays. Integration of cloud-based reporting systems is creating scalable opportunities for remote infectious disease management and epidemiological monitoring.

Manufacturers can expand revenue streams by developing compact multiplex platforms tailored for primary care centers and emergency settings. Public health agencies are supporting the deployment of rapid diagnostic infrastructure to strengthen pandemic preparedness and antimicrobial resistance surveillance. Partnerships between diagnostic companies and telehealth providers are improving accessibility of decentralized infectious disease testing services across underserved healthcare networks.

Category-wise Analysis

Product Type Insights

Reagents and kits are expected to lead the infectious disease in-vitro diagnostics market, accounting for approximately 58% of revenue in 2026. The segment benefits from recurring procurement cycles, as consumables require continuous replenishment. Roche Diagnostics reported in its 2024 annual disclosure that reagent revenues consistently outpaced instrument revenues across its infectious disease portfolio. Consumable dependency ensures stable volume demand throughout the diagnostic testing lifecycle.

Software and services are likely to represent the fastest-growing segment, propelled by cloud-based Laboratory Information Management System (LIMS) integration and AI-enabled diagnostic interpretation tools. bioMérieux has expanded its software service portfolios by embedding predictive analytics within the existing instrument ecosystems. This transition toward digital service revenue reflects broader laboratory modernization trends accelerating across hospital networks globally.

Technology Insights

Molecular diagnostics is projected to lead the market, capturing around 35% of the revenue share in 2026. Superior analytical sensitivity compared with immunoassay-based methods drives adoption in hospital-based testing programs. Cepheid demonstrated the clinical utility of its GeneXpert platform for simultaneous HIV viral load and TB detection across high-burden settings. This platform's scalability supports molecular diagnostics market leadership through the forecast period.

Next-generation sequencing (NGS) is likely to be the fastest-growing segment, fueled by expanding clinical applications in antimicrobial resistance profiling and outbreak surveillance. Illumina disclosed in its 2024 investor materials that infectious disease sequencing represented one of the highest-growth clinical verticals. Declining sequencing costs are progressively making NGS economically viable for routine diagnostic use in tertiary care centers.

Application Insights

HIV is likely to be the leading segment with a projected 22% of the market share in 2026, due to globally mandated testing and treatment monitoring programs. Joint United Nations Programme on HIV/AIDS (UNAIDS) reported in 2024 that 39.9 million people were living with HIV globally. Abbott Laboratories disclosed expansion of its HIV viral load testing capacity across public health programs in Eastern and Southern Africa.

COVID-19 and respiratory virus testing is anticipated to be the fastest-growing segment, fueled by sustained investment in multiplex respiratory panel testing. The Centers for Disease Control and Prevention (CDC) in 2025 recommended multiplex PCR panels as the preferred diagnostic approach for respiratory illness surveillance. This directly expanded institutional adoption across emergency and ambulatory care settings. Platform manufacturers are investing in rapid turnaround formats that serve both hospital and community-based testing environments.

Regional Insights

North America Infectious Disease In-vitro Diagnostics Market Trends

North America is anticipated to be the leading region, accounting for a market share of 41% in 2026, driven by an established network of high-complexity clinical laboratories and widespread adoption of advanced molecular diagnostic systems. The presence of sophisticated healthcare infrastructure, combined with favorable federal reimbursement policies, ensures continuous utilization of high-value testing platforms.

U.S. Infectious Disease In-vitro Diagnostics Market Insights

The U.S. is projected to account for a country share of 84% within the North America regional ecosystem in 2026, driven by high investments in advanced pathogen genomics and rapid diagnostic adoption. The national healthcare infrastructure leverages large-scale automated networks, keeping per-test processing times low.

Canada Infectious Disease In-vitro Diagnostics Market Insights

Canada is forecast to account for a country share of 16% within the North America regional ecosystem in 2026, supported by systematic public healthcare funding allocations and coordinated infectious disease monitoring programs. Provincial health networks prioritize the deployment of decentralized point-of-care instruments to address rural patient populations efficiently.

Europe Infectious Disease In-vitro Diagnostics Market Trends

Europe is projected to capture a regional market share of 27% in 2026, influenced by the strict execution of the in vitro diagnostic medical devices regulation, which shapes manufacturing and distribution compliance. Regional healthcare authorities focus heavily on antimicrobial resistance tracking, forcing laboratories to purchase advanced identification systems.

Germany Infectious Disease In-vitro Diagnostics Market Insights

Germany is expected to account for a country share of 23% within the European regional ecosystem in 2026, propelled by an extensive network of specialized reference laboratories and strong diagnostic engineering expertise. The implementation of automated pre-analytical sample preparation systems drives high operational throughput across laboratory networks.

U.K. Infectious Disease In-vitro Diagnostics Market Insights

The U.K. is likely to account for a country share of 19% within the European regional ecosystem in 2026, stimulated by strategic national investments in decentralized diagnostic hubs and public health sequencing infrastructure. Centralized procurement structures within the National Health Service enable large-scale, cost-effective acquisition of long-term assay consumables.

Asia Pacific Infectious Disease In-vitro Diagnostics Market Trends

Asia Pacific is forecast to be the fastest-growing market for infectious disease in-vitro diagnostics, stimulated by the rapid expansion of healthcare infrastructure, escalating public health expenditures, and broadening insurance coverage across emerging economies. Accelerating urbanization alongside rising clinical awareness regarding early pathogen detection fuels large-scale testing adoption.

China Infectious Disease In-vitro Diagnostics Market Insights

China is expected to account for a regional share of 38% in 2026, driven by extensive provincial hospital construction initiatives and rising localization of diagnostic manufacturing capabilities. Tiered healthcare reforms encourage the distribution of modern diagnostic machinery to secondary and tertiary medical facilities.

India Infectious Disease In-vitro Diagnostics Market Insights

India is likely to account for a regional share of 22% in 2026, supported by widening public-private partnerships aimed at controlling infectious disease vectors like tuberculosis and hepatitis. Expanding corporate healthcare chains invest heavily in setting up centralized, accredited diagnostic laboratories across urban areas.

Competitive Landscape

The global infectious disease in-vitro diagnostics market is moderately fragmented, with market shares distributed among several established global medical technology corporations alongside specialized diagnostic developers. Key industry participants driving global market positioning include F. Hoffmann-La Roche Ltd, Abbott Laboratories, Danaher Corporation, BD (Becton, Dickinson and Company), and bioMérieux SA.

Strategic entry by regional manufacturers alters cost dynamics within emerging territories, putting long-term pressure on standard asset pricing models. Large entities leverage extensive instrument installation footprints to secure high-margin consumable contracts, creating high competitive barriers for new entrants.

Key Industry Developments:

- In April 2026, Bruker Corporation launched the MyGenius PRO high-throughput molecular diagnostics system at ESCMID 2026, reinforcing automated infectious disease testing and rapid pathogen detection capabilities.

- In December 2025, Roche Diagnostics launched the next-generation cobas 6800/8800 systems in the United States, reinforcing high-throughput infectious disease molecular testing and laboratory automation capabilities.

- In September 2025, QIAGEN N.V. received U.S. FDA clearance for the higher-throughput QIAstat-Dx Rise syndromic testing system, reinforcing rapid infectious disease diagnostic capacity across hospital and reference laboratories.

Companies Covered in Infectious Disease In-vitro Diagnostics Market

- F. Hoffmann-La Roche Ltd

- Abbott Laboratories

- Danaher Corporation

- BD

- bioMérieux SA

- Siemens Healthineers AG

- Sysmex Corporation

- Thermo Fisher Scientific Inc.

- QIAGEN N.V.

- Hologic, Inc.

- QuidelOrtho Corporation

- Revvity, Inc.

- DiaSorin S.p.A.

Frequently Asked Questions

The global infectious disease in-vitro diagnostics market is projected to reach US$25.5 billion in 2026.

Rising infectious disease prevalence, expanding molecular diagnostic adoption, and increasing government investment in disease surveillance programs are driving the infectious disease in-vitro diagnostics market.

The infectious disease in-vitro diagnostics market is poised to witness a CAGR of 2.6% from 2026 to 2033.

Expansion of decentralized testing infrastructure and integration of artificial intelligence-enabled diagnostic platforms are creating key growth opportunities in the infectious disease in-vitro diagnostics market.

Some of the key market players include F. Hoffmann-La Roche Ltd, Abbott Laboratories, Danaher Corporation, BD (Becton, Dickinson and Company), and bioMérieux SA.