- Semiconductor Materials & Components

- IGBT and Super Junction MOSFET Market

IGBT and Super Junction MOSFET Market Size, Share, and Growth Forecast 2026 - 2033

IGBT and Super Junction MOSFET Market by Semiconductor Type (IGBT, Super Junction MOSFET), Voltage Class (Low (<600V), Medium (600V–1200V), High (>1200V)), Application (Energy & Power, Automotive, Industrial Automation, Consumer Electronics, Inverter & UPS, Medical Equipment, Others), and Regional Analysis for 2026 - 2033

IGBT and Super Junction MOSFET Market Size and Trend Analysis

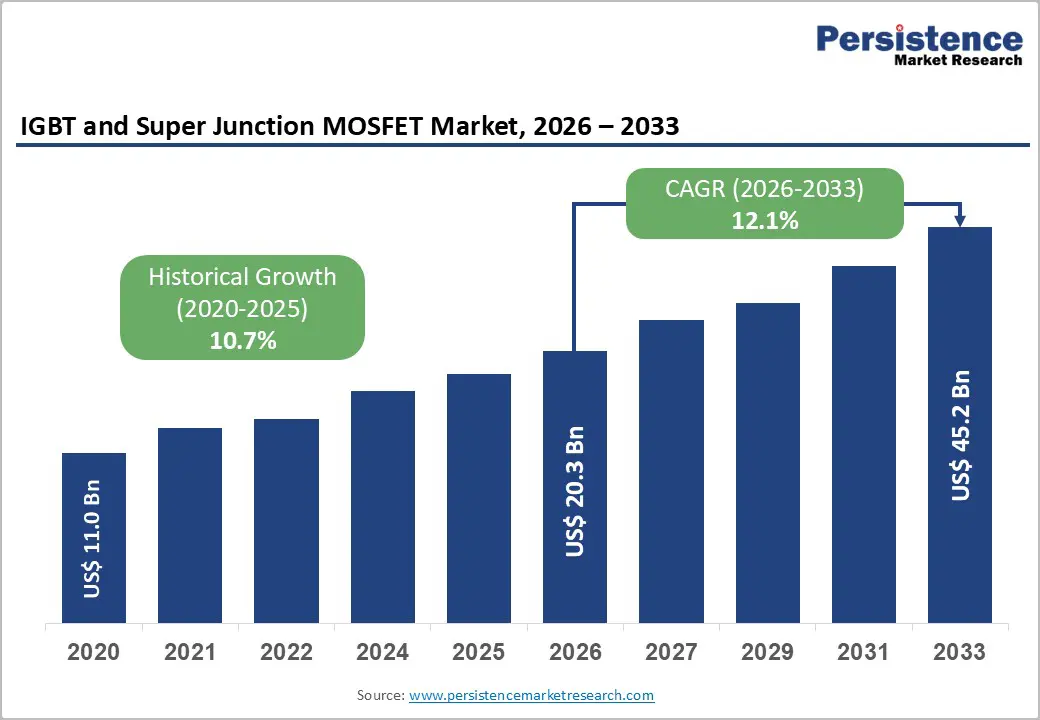

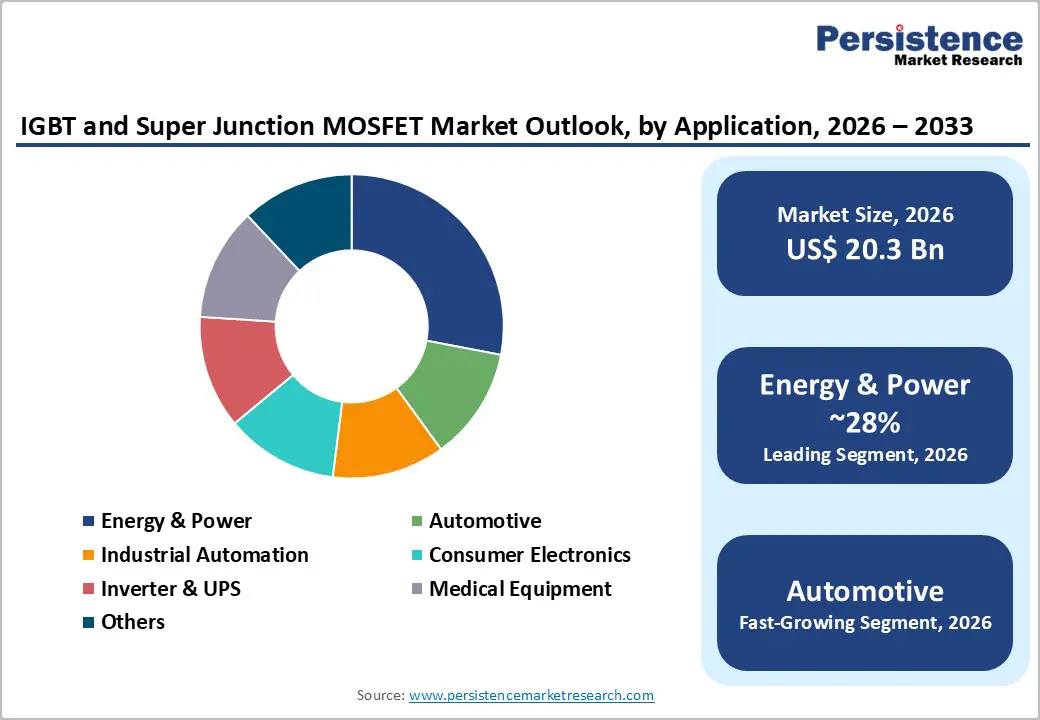

The global IGBT and Super Junction MOSFET market size is valued at US$ 20.3 billion in 2026 and is projected to reach US$ 45.2 billion by 2033, growing at a CAGR of 12.1% between 2026 and 2033.

The market's robust expansion is underpinned by accelerating automotive electrification, unprecedented additions in renewable energy capacity, and widespread investments in industrial automation under Industry 4.0 frameworks. According to the International Energy Agency (IEA), global electric vehicle sales surpassed 14 million units in 2023, accounting for approximately 18% of all new car sales, thereby directly stimulating demand for high-efficiency power semiconductor switching devices.

Key Industry Highlights:

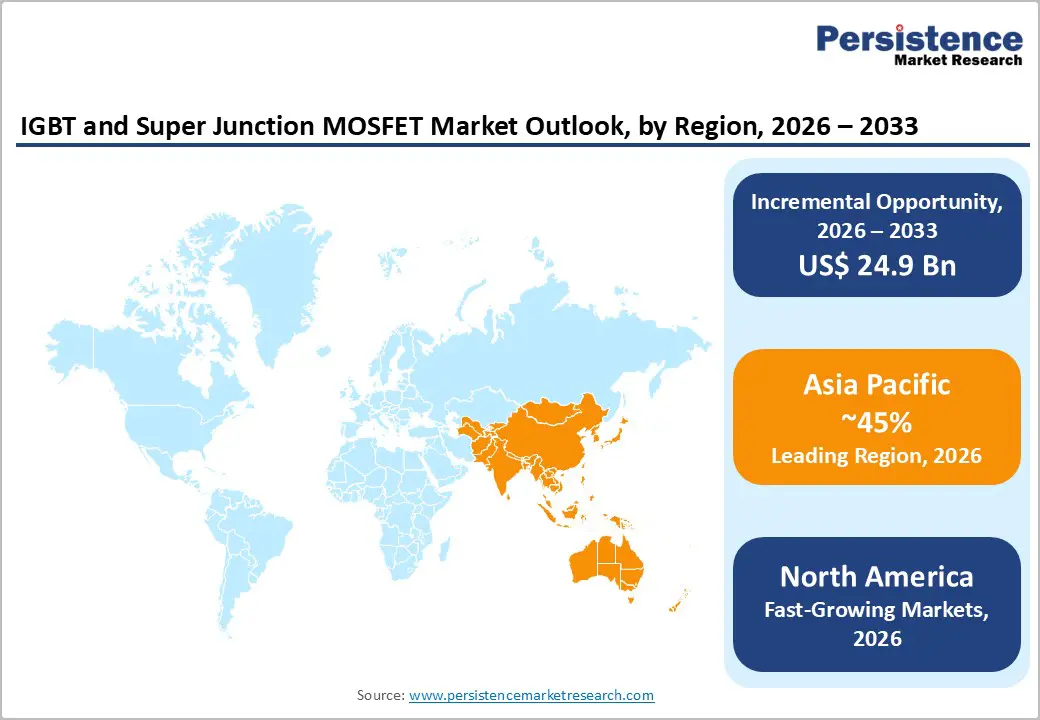

- Regional Leader: Asia Pacific leads the global IGBT and Super Junction MOSFET market with approximately 45% revenue share in 2026, powered by China's world-largest EV and solar manufacturing ecosystem, Japan's advanced power module industry, and India's rapidly scaling renewable energy deployment programs across utility-scale solar and wind sectors.

- Fast-Growing Market: North America is one of the fast-growing markets, underpinned by robust policy frameworks and an accelerating industrial electrification agenda.

- Dominant Segment: The IGBT-type segment dominates, with approximately 63% revenue share in 2026, reflecting its unmatched high-voltage and high-current capabilities for EV traction inverters, industrial motor drives exceeding 10 kW, and utility-scale renewable energy power conversion systems, where reliability and efficiency at high power levels are paramount.

- Fastest Growing Segment: The Automotive application segment is the fastest-growing end-use category, expanding at an estimated ~16% CAGR through 2033, as global EV production scales rapidly and the industry-wide transition to 800V powertrain architectures demands more sophisticated IGBT and Super Junction MOSFET content per vehicle across traction, charging, and auxiliary systems.

- Key Opportunities: Battery energy storage systems (BESS) and smart grid modernization represent the market's most compelling incremental opportunity, generating massive, sustained demand for IGBT-based bidirectional power conversion systems across utility, commercial, and industrial segments worldwide.

DRO Analysis

Drivers - Accelerating Electric Vehicle Adoption and Automotive Power Electronics Demand

The global transition toward electric mobility is the most transformative driver of demand for IGBT and Super Junction MOSFET devices. The International Energy Agency (IEA) reported that global EV sales reached 17 million units in 2024. IGBTs are mission-critical in EV traction inverters, with each battery electric vehicle consuming 20 to 36 IGBT chips depending on powertrain architecture. The rapid adoption of 800V battery architectures by automakers, including Porsche, Kia, and General Motors, is substantially increasing per-vehicle semiconductor content.

The European Union legislated a ban on internal combustion engine vehicles by 2035, while the U.S. Environmental Protection Agency (EPA) finalized emissions rules targeting 67% EV share of new car sales by 2032. These converging regulatory tailwinds are creating a structurally elevated and durable demand environment for power semiconductor devices across the forecast period.

Renewable Energy Expansion and Grid Modernization Investments

The global renewable energy sector represents a sustained and growing pool of demand for IGBT modules and Super Junction MOSFETs. According to the International Renewable Energy Agency (IRENA), global renewable capacity additions reached a record 295 GW in 2022 and remained elevated in 2023. Solar PV inverters, each requiring multiple IGBT modules, rank among the largest consumers of power semiconductor devices globally.

The IEA projects that solar and wind will account for over 90% of new power capacity additions through 2030. Complementing generation expansion, grid modernization programs constitute critical additional demand vectors. The U.S. Infrastructure Investment and Jobs Act committed US$65 billion to grid upgrades, while the European Union's REPowerEU plan targets 600 GW of solar capacity by 2030.

Restraints - Supply Chain Concentration and Extended Manufacturing Lead Times

The IGBT and Super Junction MOSFET supply chain exhibits significant geographic concentration risks. Manufacturing capacity for power devices is heavily concentrated in Japan, Germany, and China, with specialized 6-inch and 8-inch wafer fabrication facilities reporting lead times typically exceeding 52 weeks during periods of elevated demand. The global semiconductor supply disruptions of 2020–2022 starkly demonstrated how rapidly automotive and industrial OEMs can face critical device shortages.

According to the Semiconductor Industry Association (SIA), capacity additions for mature-node power semiconductor fabs require capital investments of US$ 1-3 billion and a 3-5 year commissioning timeline, severely limiting short-term supply elasticity and creating persistent procurement risk for end-market manufacturers dependent on uninterrupted device supply.

Rising Competition from Wide Bandgap Power Semiconductors

Silicon Carbide (SiC) and Gallium Nitride (GaN) power semiconductors represent a growing competitive challenge to conventional IGBT and Super Junction MOSFET devices, particularly in high-frequency and high-temperature applications. SiC MOSFETs demonstrate switching losses 5-10 times lower than equivalent silicon IGBTs, enabling lighter and more compact power systems highly valued in premium EV and aerospace electronics applications.

Tesla was among the first automakers to adopt SiC-based inverters in mass-produced vehicles, a trend now widely adopted. While SiC devices currently carry a 3–5 times cost premium over silicon counterparts, ongoing capacity expansion by Wolfspeed, STMicroelectronics, and onsemi is progressively narrowing this gap, posing a measurable long-term substitution risk for silicon power devices in premium application segments.

Opportunities - Industrial Automation, Robotics, and Industry 4.0 Expansion

The global surge in industrial automation presents a compelling incremental growth opportunity for IGBT and Super Junction MOSFET market participants. The International Federation of Robotics (IFR) reported that global industrial robot installations reached a record 553,052 units in 2022, with China, Japan, Germany, South Korea, and the United States accounting for approximately 79% of total deployments.

Each industrial robot system employs multiple IGBT modules in its servo drive subsystem. Government-backed manufacturing revival initiatives, including the U.S. CHIPS and Science Act, the EU Chips Act committing €43 billion in semiconductor investment, and China's industrial upgrade programs, are expected to drive significant capital deployment in factory automation infrastructure over the 2026–2033 forecast period, directly benefiting IGBT and Super Junction MOSFET demand.

Battery Energy Storage Systems (BESS) and Smart Grid Infrastructure

Battery energy storage systems represent one of the highest-growth deployment areas for IGBT technology in the coming decade. The U.S. Inflation Reduction Act (IRA) provides investment tax credits of up to 30% for standalone battery storage projects, while the European Union's Net Zero Industry Act accelerates domestic storage deployment.

India's ambition to deploy 500 GW of renewable energy by 2030 under its National Electricity Plan will necessitate commensurate investments in grid-scale storage. This emerging application domain offers market participants a large incremental revenue opportunity, distinct from traditional automotive and industrial end-markets.

Category-wise Analysis

Semiconductor Type Insights

The IGBT segment commands the leading position in the market, capturing approximately 63% of total revenue in 2026. This dominance is attributable to IGBT's unique combination of high-voltage blocking capability, up to 6.5 kV, high-current handling, and relatively low conduction losses that render it irreplaceable in applications demanding power levels above 10 kW. Utility-scale solar inverters typically require between 6 and 18 high-power IGBT modules each, while a single 100 kW EV traction inverter utilizes up to 36 IGBT chips.

The ongoing electrification of commercial vehicles, expansion of offshore wind power converters rated above 5 MW, and growth of high-speed rail traction systems continue to reinforce IGBT's market leadership. Super Junction MOSFETs hold approximately 37% share and are accelerating in lower-power consumer electronics, auxiliary automotive applications, and telecom power supplies where high-frequency operation is the primary design priority.

Voltage Class Insights

The medium-voltage class (600V–1200V) segment leads in voltage classification, representing approximately 46% of total revenues in 2026. This voltage range encompasses the broadest application spectrum, serving standard industrial motor drives, EV onboard chargers, DC-DC converters, solar microinverters, and uninterruptible power supplies (UPS). The 650V rating has emerged as an industry standard for automotive switching applications compliant with 400V battery architectures, while 1,200V devices dominate industrial drives and renewable energy converter applications.

The International Electrotechnical Commission (IEC) standards governing medium-voltage switchgear and drive systems further reinforce device standardization within this voltage range. The low-voltage segment (<600V) holds approximately 32% share, primarily in consumer electronics and telecom, while the high-voltage segment (>1,200V) captures the remaining 22% in railway traction and grid-connected power conversion applications.

Application Insights

The Energy & Power segment leads by application with approximately 28% market share, driven by the global renewable energy transition and grid infrastructure modernization programs. According to IRENA, global solar PV additions reached 268 GW in 2022, with wind additions contributing a further 77.6 GW. Each gigawatt of utility-scale solar requires approximately 3,500-4,500 IGBT modules for inverter applications.

The Automotive segment represents the fastest-growing application, propelled by surging EV production globally, but Energy & Power maintains its leading position due to the accumulated scale of renewable generation assets and continuous infrastructure investment cycles. Inverter & UPS and Medical Equipment segments collectively represent approximately 18% of revenues, with medical applications growing steadily due to demand for precision power electronics in advanced imaging and surgical systems.

Regional Analysis

North America IGBT and Super Junction MOSFET Market Trends & Analysis

North America constitutes a significant and technology-driven regional market for IGBT and Super Junction MOSFET devices, estimated at 4.4 Bn in 2026, underpinned by robust policy frameworks and an accelerating industrial electrification agenda. The U.S. Inflation Reduction Act's (IRA) US$ 369 billion clean energy investment framework is directly stimulating solar, wind, and battery storage deployments that consume substantial IGBT content.

U.S. IGBT and Super Junction MOSFET Market

The U.S. market is estimated at approximately US$ 3.8 Bn in 2026, representing approximately 87% of the North American regional total, supported by utility-scale solar and wind deployments, EV incentive programs, and defense electronics modernization initiatives.

Europe IGBT and Super Junction MOSFET Market Trends, Drivers, & Insights

Europe represents a mature yet dynamically evolving market for IGBT and Super Junction MOSFET devices, shaped by stringent climate legislation and a deeply embedded industrial base. The European Green Deal and REPowerEU plan collectively mandate a comprehensive energy transition, targeting 600 GW of solar and 510 GW of wind capacity by 2030, both representing large and growing consumption pools for IGBT modules in power conversion equipment.

Germany IGBT and Super Junction MOSFET Market

Germany's market is estimated at approximately US$ 1.1 billion in 2026, underpinned by its world-class industrial automation sector, automotive electrification programs, and concentration of power electronics OEMs, including Infineon Technologies AG and Semikron Danfoss GmbH & Co. KG.

U.K. IGBT and Super Junction MOSFET Market

The U.K. market is estimated at approximately US$ 700 million in 2026, driven primarily by offshore wind power expansion, one of the world's largest offshore wind fleets, alongside defense electronics and industrial automation applications.

France IGBT and Super Junction MOSFET Market

France's market is estimated at approximately US$ 500 million in 2026, supported by nuclear power modernization programs, growing EV manufacturing capacity within the domestic automotive sector, and renewable energy infrastructure investments.

Asia Pacific IGBT and Super Junction MOSFET Market

Asia Pacific dominates the global IGBT and Super Junction MOSFET market, accounting for approximately 45% of total revenues in 2026. China is the epicenter of global power semiconductor demand, housing the world's largest solar manufacturing ecosystem and the most extensive EV production base, with over 9 million EVs sold domestically in 2023, according to the China Association of Automobile Manufacturers (CAAM).

China IGBT and Super Junction MOSFET Market Trends

China's market is estimated at approximately US$ 4.6 billion in 2026, representing approximately 51% of the Asia Pacific regional total, driven by the world's largest EV manufacturing base and an unrivaled solar panel production ecosystem.

India IGBT and Super Junction MOSFET Market Trends

India's market is estimated at approximately US$ 1.4 billion in 2026, growing at an estimated ~15% CAGR through 2033, driven by solar and wind capacity expansion mandates and Production-Linked Incentive (PLI) schemes for advanced electronics and electric vehicles.

Japan IGBT and Super Junction MOSFET Market

Japan's market is estimated at approximately US$ 1.6 Bn in 2026, anchored by its globally significant power module manufacturing industry and robust domestic demand for industrial automation across the automotive, electronics, and robotics sectors.

Competitive Landscape

The IGBT and Super Junction MOSFET market exhibits a moderately consolidated competitive structure, with the top five companies, Infineon Technologies AG, Mitsubishi Electric Corporation, STMicroelectronics N.V., Fuji Electric Co., Ltd., and ABB Ltd., collectively accounting for approximately 55-60% of global revenues.

R&D investment is concentrated on next-generation Trench Field-Stop IGBT architectures, thin-wafer power chip processing, and high-density multi-chip power modules. Companies increasingly differentiate through co-engineering partnerships with automotive OEMs, lifecycle service agreements for industrial customers, and regional manufacturing expansion strategies to mitigate geopolitical supply chain exposure across key end-markets.

Key Developments:

- April 2025: Infineon Technologies AG announced the launch of its 600V CoolMOS™ 8 super junction MOSFET family, designed to enhance efficiency and performance in high-power applications such as AI servers, chargers, solar systems, and EV charging infrastructure. The new generation MOSFET technology delivers 18% lower gate charge, faster switching speeds, and 14–42% improved thermal performance, enabling higher power density and reduced energy losses.

- December 2025: Mitsubishi Electric Corporation announced the launch of two new XB Series high-voltage IGBT (HVIGBT) modules (4.5kV/1200A), designed to enhance efficiency and reliability in inverter systems used in rail transport and large industrial equipment.

- March 2026: Danfoss announced the acquisition of the remaining shares in Semikron Danfoss, increasing its ownership from 62% to 100%, thereby gaining full control of the global power electronics company. The move transitions Semikron Danfoss from a joint venture (formed in 2022) into a wholly owned subsidiary, enabling Danfoss to accelerate investments in advanced power modules and industrial-scale power electronics solutions aligned with its LEAP 2030 electrification strategy.

Top Companies in the IGBT and Super Junction MOSFET Market

Infineon Technologies AG (Neubiberg, Germany) is the undisputed global market leader in power semiconductors, commanding the broadest portfolio of IGBTs and Super Junction MOSFETs across automotive, industrial, and consumer segments. Infineon's global manufacturing network and deep application engineering capabilities sustain its leading market position.

Mitsubishi Electric Corporation (Tokyo, Japan) is a premier designer and manufacturer of high-power IGBT modules, maintaining strong market footholds in railway traction, industrial drives, and renewable energy converter markets globally. Its proprietary 7th Generation IGBT technology and J-Series power modules are widely adopted in MW-class solar inverters and high-speed rail traction applications, supported by a robust global distribution and application support network.

STMicroelectronics N.V. (Geneva, Switzerland) addresses both automotive and industrial end-markets through its MDmesh™ Super Junction MOSFET platform and automotive-grade PowerMESH™ IGBT family. The company's global wafer fabrication network and active co-design engagements with leading EV OEMs and industrial drive manufacturers position it as a key technology challenger, particularly in the 600V–1,200V voltage class that dominates the broadest application segments.

Companies Covered in IGBT and Super Junction MOSFET Market

- Infineon Technologies AG

- Mitsubishi Electric Corporation

- STMicroelectronics N.V.

- Fuji Electric Co., Ltd.

- ABB Ltd.

- Semikron Danfoss GmbH & Co. KG

- ROHM Co., Ltd.

- Toshiba Electronic Devices & Storage

- Vishay Intertechnology, Inc.

- Hitachi Energy Ltd.

- Alpha & Omega Semiconductor

- NXP Semiconductors N.V.

Frequently Asked Questions

The global IGBT and Super Junction MOSFET market is valued at US$ 20.3 Bn in 2026 and is projected to reach US$ 45.2 Bn by 2033, growing at a CAGR of 12.1% over the forecast period of 2026–2033.

The principal demand drivers are the global electrification of the automotive sector, with the IEA reporting over 14 million EV sales in 2023, and record renewable energy capacity additions led by solar and wind. Grid modernization programs, including the U.S. Infrastructure Investment and Jobs Act's US$ 65 billion grid investment, and industrial automation investments under Industry 4.0 frameworks, provide additional structural demand support through the forecast period.

The IGBT segment leads with approximately 63% market share, driven by its superior high-voltage and high-current characteristics that make it indispensable for EV traction systems, industrial motor drives above 10 kW, and utility-scale renewable energy power conversion systems. Super Junction MOSFETs hold the remaining approximately 37% share, growing in high-frequency consumer electronics and auxiliary automotive applications.

Asia Pacific is the leading region with approximately 45% revenue share in 2026, dominated by China's massive solar, EV, and industrial electronics manufacturing base, including over 9 million domestic EV sales in 2023 per the China Association of Automobile Manufacturers (CAAM), supplemented by Japan's world-class power module manufacturing industry and India's rapidly expanding renewable energy infrastructure deployment.

The most significant incremental opportunity lies in battery energy storage systems (BESS) and smart grid infrastructure. The global BESS capacity is expected to grow from approximately 45 GWh in 2022 to over 400 GWh by 2030, a more than 9x expansion, creating massive sustained demand for IGBT-based bidirectional power conversion systems across utility, commercial, and industrial segments globally.

Leading companies include Infineon Technologies AG, Mitsubishi Electric Corporation, STMicroelectronics N.V., Fuji Electric Co., Ltd., ABB Ltd., Semikron Danfoss GmbH & Co. KG, ROHM Co., Ltd., Toshiba Electronic Devices & Storage, Vishay Intertechnology, Inc., Hitachi Energy Ltd., Alpha & Omega Semiconductor, and NXP Semiconductors N.V., among others operating across the global power semiconductor ecosystem.