- Home Appliances

- Home Appliances Market

Home Appliances Market Size, Share, and Growth Forecast 2026 - 2033

Home Appliances Market by Product Type (Major Appliances/White Goods [Refrigerators, Dishwashers, Washing Machines, Water Heaters, Air Conditioners, Others], Small Appliances [Microwave, Coffee Makers, Toasters, Juicers and Blenders, Hair Dryers, Others]), Distribution Channel (Online, Offline [Hypermarkets/Supermarkets, Specialty Stores, Department Stores, Brand Outlets, Others]), Power Source, and Regional Analysis for 2026 - 2033

Home Appliances Market Size and Trend Analysis

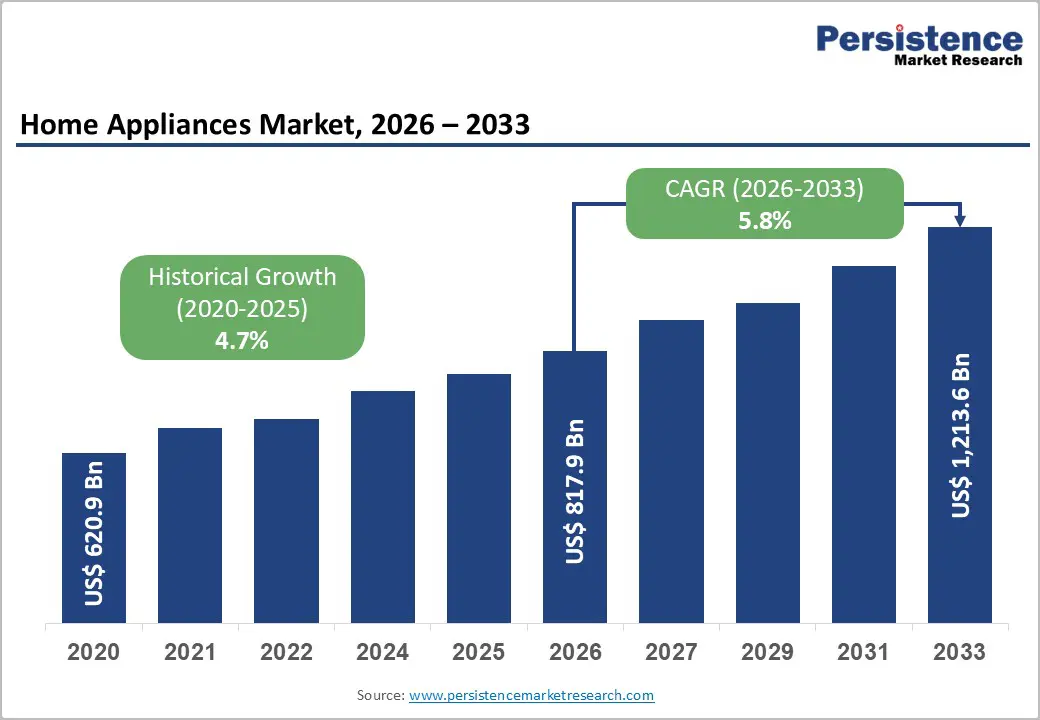

The global home appliances market size is estimated to be valued at US$ 817.9 billion in 2026 and is projected to reach US$ 1,213.6 billion growing at a CAGR of 5.8% between 2026 and 2033.

The home appliances market is on a sustained upward trajectory, driven by rapid urbanization, rising disposable incomes across emerging economies, and accelerating consumer preference for energy-efficient and smart-connected appliances. The global urban population is projected to reach 5 billion by 2030, according to the United Nations, directly expanding the addressable consumer base for household appliances.

Key Industry Highlights:

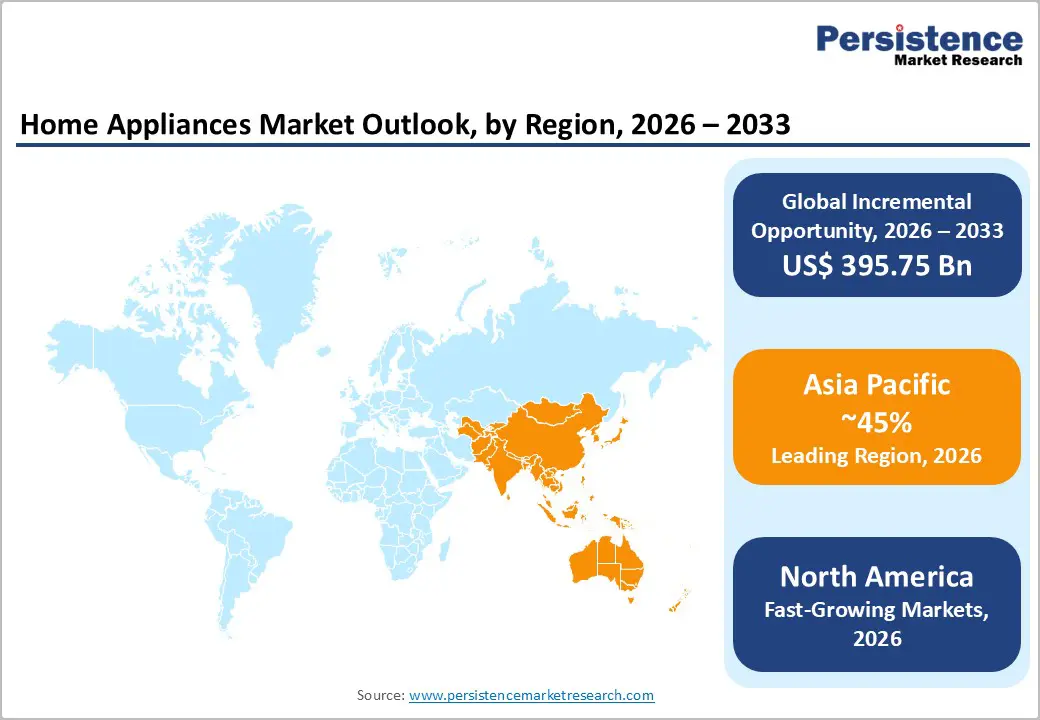

- Leading Region - Asia Pacific dominates the global home appliances market with over 45% of consumption, powered by China's massive manufacturing and consumption base, India's rapidly expanding middle class, and Southeast Asia's accelerating urbanization and household electrification programs.

- Fast-Growing Region - North America represents a mature, high-value home appliances market characterized by strong replacement demand, sophisticated consumer preferences, and robust regulatory standards.

- Dominant Product: Major appliances command approximately 65% of the market, led by air conditioners and refrigerators. High per-unit value, recurring replacement demand, and near-universal household necessity underpin the segment's dominant revenue contribution globally.

- Fast-Growing Distribution Channel - The online channel is the fastest-growing distribution segment, accelerated by e-commerce platform expansion, digital payment adoption, and post-pandemic consumer behavior shifts toward convenient home shopping for small and mid-range appliances.

- Key Opportunity - With approximately 675 million people lacking access to electricity globally, solar-powered appliances targeting off-grid households in Africa and South Asia represent a substantial, structurally underserved growth opportunity for forward-looking manufacturers.

DRO Analysis

Drivers - Urbanization and Rising Middle-Class Consumption Fueling Appliance Demand

Rapid urbanization across Asia Pacific, Africa, and Latin America is one of the most powerful structural drivers of the home appliances market. The United Nations projects that the global urban population will increase by approximately 2.5 billion people by 2050, with most of this growth concentrated in China, India, and Sub-Saharan Africa.

Urban households exhibit substantially higher appliance penetration rates than rural households due to improved access to electricity, higher incomes, and smaller living spaces requiring compact, multifunctional appliances. The World Bank estimates that the global middle class will expand to nearly 5.3 billion people by 2030, creating an unprecedented consumer base for refrigerators, washing machines, and air conditioners.

Energy Efficiency Regulations Accelerating Product Replacement Cycles

Stringent government energy efficiency standards are systematically driving consumers and businesses to replace older appliances with newer, compliant models, creating durable replacement demand. The U.S. Department of Energy (DOE) has implemented mandatory efficiency standards across major appliance categories, including refrigerators, washing machines, dishwashers, and water heaters, with standards periodically tightened.

The European Union's Ecodesign Regulation similarly mandates minimum energy performance criteria for a broad range of household appliances, covering over 40 product groups. According to the International Energy Agency (IEA), appliances and lighting account for approximately 30% of global electricity consumption, making efficiency improvements a high-priority policy focus.

Restraints - High Product Costs and Affordability Constraints in Developing Markets

Despite large potential consumer bases, affordability remains a significant barrier to appliance penetration in lower-income segments of emerging markets. Premium smart appliances incorporating IoT connectivity, inverter technology, and advanced sensors carry retail price premiums of 30-60% over conventional counterparts, placing them beyond the reach of a substantial portion of consumers in markets such as Sub-Saharan Africa, South Asia, and parts of Southeast Asia.

Limited consumer credit access and high import duties in several developing nations further compound affordability challenges, restricting market expansion to premium urban segments and constraining volumetric growth potential.

Supply Chain Disruptions and Raw Material Price Volatility

The home appliances industry is highly exposed to supply chain disruptions and volatility in raw material costs, particularly for steel, copper, aluminum, and semiconductors. The global semiconductor shortage that emerged in 2020-2022 severely impacted smart appliance production timelines, with leading manufacturers including Whirlpool and LG Electronics reporting production delays.

According to the World Trade Organization (WTO), disruptions to global goods trade rose sharply during the COVID-19 pandemic, exposing vulnerabilities in just-in-time manufacturing strategies. Ongoing geopolitical tensions and freight cost fluctuations continue to challenge cost management for manufacturers, pressuring margins and constraining competitive pricing strategies.

Opportunities - Smart Home Integration and IoT-Connected Appliances

The rapid adoption of smart home ecosystems represents a transformational growth opportunity for home appliance manufacturers. According to the Consumer Technology Association (CTA), smart home device ownership in the United States has grown steadily, with a significant share of households now owning at least one smart home device.

IoT-enabled appliances such as smart refrigerators, connected washing machines, and AI-powered air conditioners offer consumers remote monitoring, predictive maintenance alerts, and energy usage optimization. Major platforms including Amazon Alexa, Google Home, and Apple HomeKit are accelerating ecosystem integration, incentivizing manufacturers to develop compatible product lines.

Solar-Powered and Energy-Harvesting Appliances in Off-Grid Markets

The electrification gap in rural and off-grid regions, particularly across Sub-Saharan Africa and South Asia, presents a compelling untapped opportunity for solar-powered home appliances. The International Energy Agency (IEA) estimates that approximately 675 million people globally still lacked access to electricity as of 2021, with the majority concentrated in Africa.

Solar direct-drive refrigerators, solar water heaters, and solar-powered fans are gaining traction as viable solutions for off-grid consumers. The World Bank's Lighting Africa and Energizing Finance initiatives are actively funding off-grid energy and appliance access programs. Manufacturers that develop affordable, durable solar-compatible appliances designed for tropical climates and low-income consumer budgets stand to capture first-mover advantage in a structurally underserved market with a combined consumer base of hundreds of millions.

Category-wise Analysis

Product Type Insights

Major appliances, commonly referred to as white goods, dominate the home appliances market by product type, commanding approximately 65% of total market share in 2026. Within this segment, air conditioners and refrigerators are the highest-revenue sub-categories, driven by rising global temperatures, expanding food preservation needs, and increasing household income levels.

The International Institute of Refrigeration (IIR) estimates that over 2 billion refrigerating appliances are in operation globally, underscoring the category's massive installed base and replacement cycle demand. Air conditioner penetration rates in countries such as India remain below 10% of households despite high cooling demandreflecting significant headroom for volume growth.

Distribution Channel Insights

Offline channels collectively retain the leading share in home appliance distribution, accounting for approximately 62% of total revenue in 2026. Within offline, specialty stores and brand outlets remain the dominant sub-channels, as consumers purchasing high-value appliances such as refrigerators, washing machines, and air conditioners prefer in-store demonstrations, professional guidance, and hands-on product evaluation before committing to purchase. However, the online channel is the fastest growing distribution mode, accelerated by the COVID-19 pandemic-induced shift in consumer purchasing behavior.

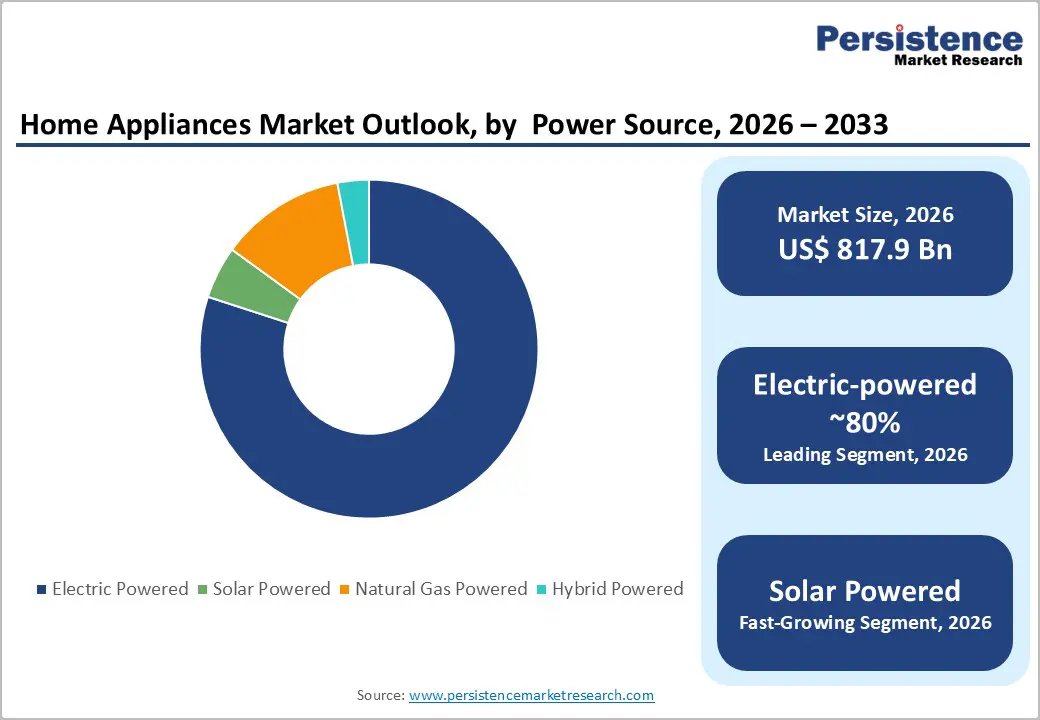

Power Source Insights

Electric-powered appliances dominate the home appliances market by power source, accounting for approximately 80% of total market share. The near-universal electrification of households in developed economies and rapidly improving electricity access in developing markets sustain this overwhelming dominance.

The International Energy Agency (IEA) reports that global electricity access rates reached approximately 91% in 2021, providing a broad infrastructure base for electric appliance adoption. Technological advancements, particularly in inverter motor technology, variable-speed compressors, and heat pump systems, have significantly improved the energy efficiency of electric appliances, reinforcing consumer and regulatory preference for this power source.

Regional Analysis

North America Home Appliances Market Trends & Analysis

North America represents a mature, high-value home appliances market characterized by strong replacement demand, sophisticated consumer preferences, and robust regulatory standards. The U.S. Department of Energy continues to tighten appliance efficiency standards, driving sustained product replacement cycles across refrigerators, dishwashers, washing machines, and air conditioners.

The residential construction recovery following the post-pandemic housing boom has generated significant demand for new appliance installations. Smart appliance adoption is particularly advanced in North America, with the Consumer Technology Association (CTA) reporting growing smart home device penetration across U.S. households.

U.S. Home Appliances Market Size

The United States is the dominant country market within North America, accounting for approximately 80% of regional home appliances revenue. With high household appliance saturation, market growth is primarily replacement-driven, reinforced by DOE efficiency mandates and a large premium smart appliance segment.

Europe Home Appliances Market Trends, Drivers, & Insights

Europe is a highly regulated, sustainability-conscious home appliances market where the EU Ecodesign Regulation and Energy Labelling Framework are central market drivers. These regulations mandate minimum efficiency standards for key product categories and require clear energy label disclosures, systematically phasing out inefficient appliances and creating replacement demand. The European Commission's Green Deal and Renovation Wave strategytargeting the renovation of 35 million buildings by 2030is expected to generate substantial appliance replacement demand.

Germany Home Appliances Market Size

Germany is Europe's largest home appliances market, accounting for approximately 18-20% of regional revenue. High consumer purchasing power, stringent energy efficiency preferences, and robust retail infrastructure underpin Germany's leading position. The German Electrical and Electronic Manufacturers' Association (ZVEI) tracks consistently strong appliance shipment volumes, supported by active product upgrade cycles among quality-conscious German consumers.

U.K. Home Appliances Market Size

The United Kingdom represents approximately 12-14% of the European home appliances market. The Association of Manufacturers of Domestic Appliances (AMDEA) reports consistent demand across major appliance categories, with strong consumer preference for A-rated energy-efficient products. Post-Brexit regulatory alignment with EU Ecodesign standards continues to influence product cycles.

France Home Appliances Market Size

France accounts for approximately 12% of European home appliance demand. The French market benefits from government energy renovation subsidies, including the MaPrimeRénov' scheme, which incentivizes the replacement of inefficient heating and cooling appliances with modern heat pump solutions, sustaining above-average growth in connected white goods categories.

Asia Pacific Home Appliances Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing regional market for home appliances, driven by urbanization, rising middle-class population, and government electrification programs. The region accounts for over 45% of global home appliance consumption, with China and India as the dominant demand centers. China's market is characterized by a sophisticated domestic manufacturing ecosystem, with companies such as Haier, Midea, and Gree Electric Appliances competing aggressively on technology and price.

China Home Appliances Market Size

China is the world's single largest home appliances market, accounting for approximately 28-30% of global revenue. The China Household Electrical Appliances Association (CHEAA) reports annual appliance production volumes of several hundred million units across all categories. Domestic brands dominate the market, with Haier, Midea, and Hisense collectively commanding over half of the national revenue in major appliance categories.

India Home Appliances Market Size

India is one of the fast-growing national markets globally, with home appliance penetration rates well below developed market averages, offering substantial headroom for volume expansion. The Consumer Electronics and Appliances Manufacturers Association (CEAMA) projects continued double-digit growth in select categories, including air conditioners and washing machines.

Japan Home Appliances Market Size

Japan is a mature, innovation-led home appliances market where advanced product features, including AI-powered operation, ultra-high energy efficiency, and compact design for space-constrained urban homes drive consumer premiumization. Japan accounts for approximately 7% of the Asia Pacific revenue.

Competitive Landscape

The global home appliances market is moderately consolidated at the top, with a small number of multinational manufacturers, including Whirlpool, Samsung, LG Electronics, Haier, and Midea, commanding significant global market shares, while hundreds of regional and niche players compete at the national level.

Key competitive strategies include aggressive product portfolio expansion into IoT-connected smart appliances, sustainability-led innovation targeting energy labelling improvements, and direct-to-consumer digital sales channel investments. Market leaders are differentiating through proprietary smart home ecosystems, extended warranty programs, and after-sales service networks.

Key Developments:

- In June 2025, Samsung launched its 2025 Bespoke AI appliance lineup in India, featuring AI-powered refrigerators, washing machines, and air conditioners integrated with its new AI Home interface. The range emphasizes energy efficiency, personalized user experience, and enhanced security through Samsung Knox and SmartThings connectivity.

- In February 2025, Versuni introduced the new Philips Airfryer 3000 Series Single Basket, featuring a reimagined top-down cooking window, 16-in-one cooking functions, and RapidAir Plus Technology for healthier, faster meals. Available in two large-capacity sizes, it also supports up to 70% energy savings.

Companies Covered in Home Appliances Market

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Haier Smart Home Co., Ltd. (including GE Appliances, Fisher & Paykel, Candy)

- Whirlpool Corporation

- Midea Group Co., Ltd.

- Electrolux AB

- Panasonic Holdings Corporation

- BSH Hausgeräte GmbH (Bosch, Siemens brands)

- Arçelik A.Ş.

- Hitachi, Ltd.

- Sharp Corporation

- Daikin Industries, Ltd.

- Gree Electric Appliances, Inc.

- Hisense Group Co., Ltd.

- iRobot Corporation (Amazon)

- Dyson Ltd.

- Miele & Cie. KG

- Vestel Elektronik Sanayi ve Ticaret A.Ş.

- IFB Industries Ltd.

- Voltas Limited (Tata Group)

Frequently Asked Questions

The global home appliances market size is estimated to be valued at US$ 817.9 Bn in 2026 and is projected to reach US$ 1,213.6 Bn by 2033, expanding at a CAGR of 5.8% during the forecast period of 2026 - 2033.

The market is primarily driven by rapid urbanization in emerging economies, rising middle-class disposable incomes, and increasingly stringent government energy efficiency regulationssuch as the U.S.

Major appliances (white goods) dominate the home appliances market, commanding approximately 65% of total revenue. Within this segment, air conditioners and refrigerators are the highest-revenue categories, driven by global temperature rise, food preservation needs, and low penetration rates in high-growth markets such as India, offering significant volume expansion potential.

Asia Pacific is the leading region, accounting for over 45% of global home appliance consumption. China, as the world's largest appliance producer and consumer, and India, as one of the fastest-growing markets driven by urbanization and rising incomes, are the primary demand engines within the region.

Leading companies in the global Home Appliances market include Samsung Electronics, LG Electronics, Haier Smart Home (including GE Appliances and Fisher & Paykel), Whirlpool Corporation, Midea Group, Electrolux AB, BSH Hausgeräte GmbH (Bosch and Siemens brands), Panasonic, Daikin Industries, and Miele, among others, competing across product innovation, smart connectivity, energy efficiency, and global distribution network strength.