- Nutraceuticals & Functional Foods

- Grass-fed Protein Market

Grass-fed Protein Market Size, Share, and Growth Forecast, 2026 - 2033

Grass-fed Protein Market by Product Type (Protein Powders, Protein Bar, Others), Source (Grass-fed Dairy, Grass-fed Beef Protein, Others), Application (Sports Nutrition, Weight Management, Dietary Supplements, Functional Food & Beverages, Infant Nutrition), and Regional Analysis for 2026 - 2033

Grass-fed Protein Market Share and Trends Analysis

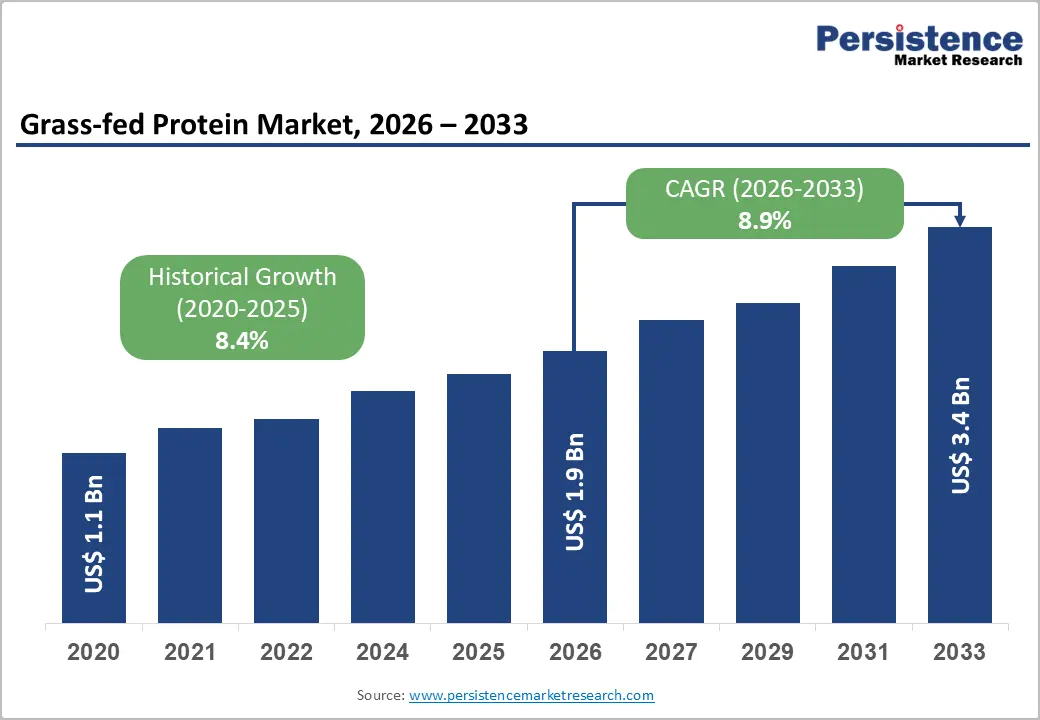

The global grass-fed protein market size is likely to be valued at US$1.9 billion in 2026 and is estimated to reach US$3.4 billion by 2033, growing at a CAGR of 8.9% during the forecast period 2026−2033, driven by increasing consumer preference for clean-label nutrition and transparent, traceable sourcing practices. Recommendations from organizations such as the World Health Organization and the Food and Agriculture Organization are further supporting demand for minimally processed protein products.

Rising disposable incomes in urban areas are encouraging consumers to opt for premium, sustainably sourced options, while expanding middle-class populations are broadening the overall customer base. Additionally, advancements in cold-chain logistics, traceability technologies, and e-commerce platforms are strengthening supply chain efficiency and market accessibility.

Key Industry Highlights:

- Leading Product Type: Protein powders are expected to hold around 38% market share in 2026, driven by clinical acceptance and dosage precision.

- Fastest-growing Product Type: Ready-to-drink (RTD) beverages are projected as the fastest-growing segment from 2026 to 2033, supported by convenience demand and on-the-go consumption.

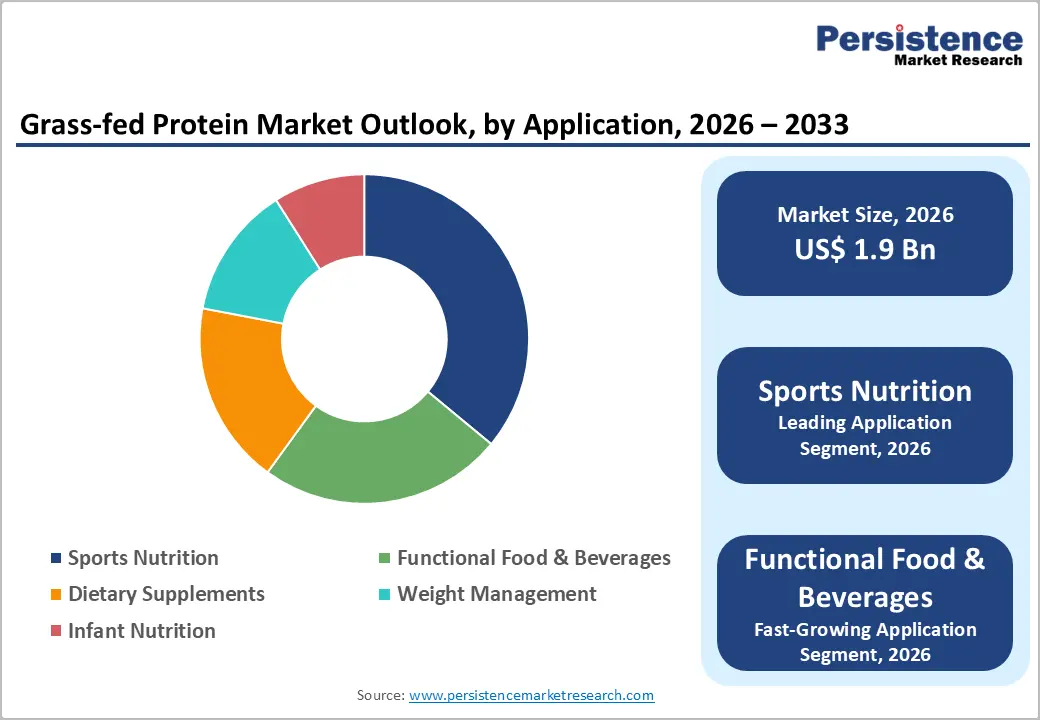

- Leading Application: Sports nutrition is projected to hold around 36% market share in 2026, driven by structured fitness adoption and performance-focused nutrition needs.

- Fastest-growing Application: Functional food & beverages are expected to be the fastest-growing segment from 2026 to 2033, supported by daily nutrition integration and fortified food innovation.

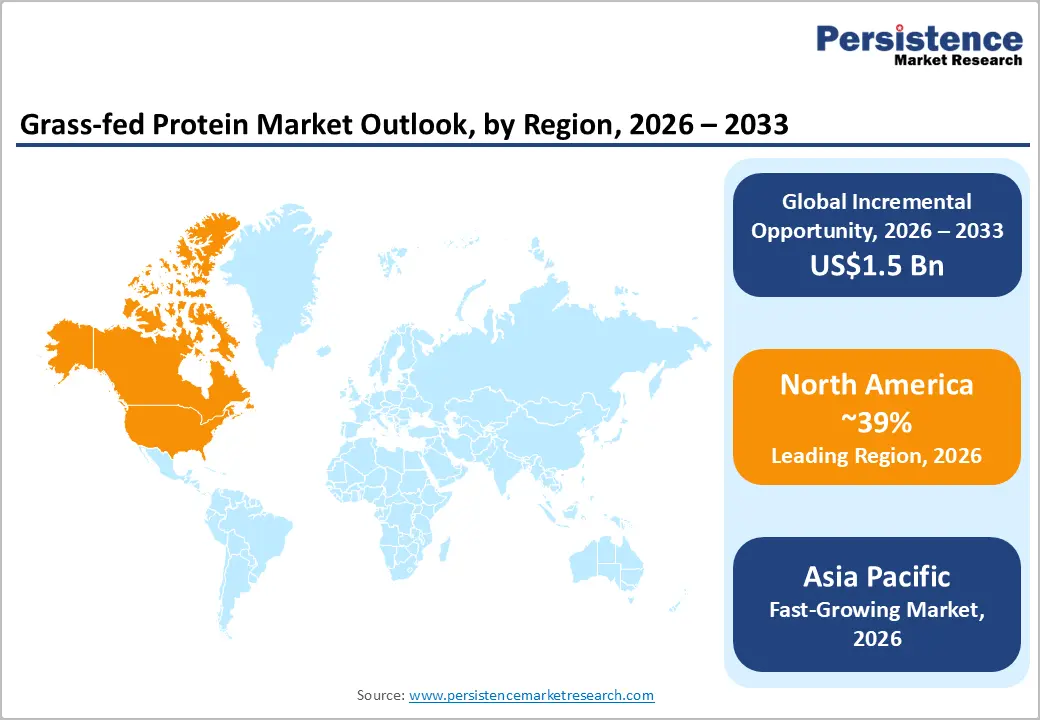

- Regional Leadership: North America is projected to hold approximately 39% market share in 2026, while Asia Pacific is forecasted to record the fastest growth due to urbanization and rising disposable income.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as Fonterra Co-operative Group, Glanbia plc, Nestlé S.A., Arla Foods, and Danone S.A. focusing on certification-driven differentiation and functional product innovation.

- Innovation Trends: Market evolution is shaped by clean-label formulation advancement and traceability technologies, supporting wider adoption across nutrition applications.

DRO Analysis

Driver - Growing Adoption in Sports Nutrition and Fitness Industries

Rising participation in structured fitness programs drives demand for high-quality protein inputs that support muscle recovery and performance optimization. Athletes and active consumers prioritize nutrient density, amino acid profile, and clean sourcing, which positions grass-fed protein as a preferred option within premium nutrition portfolios. Product differentiation enables higher price realization and strengthens brand positioning across specialized retail and online channels. According to the Centers for Disease Control and Prevention, 52.3% of the U.S. adults met aerobic activity guidelines in 2025, indicating a broad and expanding consumer base seeking performance-oriented nutrition solutions.

Commercial fitness expansion increases the consumption frequency of protein supplements, functional beverages, and fortified foods, creating consistent volume demand. Gyms, training centers, and sports institutions integrate nutrition products into membership offerings, which supports recurring sales cycles. Supply chains respond with targeted formulations designed for endurance, strength training, and recovery phases, improving product segmentation and operational efficiency. Premium consumers demonstrate lower price sensitivity, enabling margin stability despite higher production costs.

Rising Health Consciousness and Clean-label Demand

Consumer preference shifts toward transparency and simple ingredients reshape protein purchasing behavior. Clean-label positioning aligns with demand for products free from synthetic additives, hormones, and antibiotics. Grass-fed protein gains traction as sourcing practices reflect natural feeding systems and minimal processing. This perception supports premium pricing and strengthens margins across value chains. Retail expansion of labeled and traceable products reflects sustained demand pressure. Data from the United States Department of Agriculture indicates that over 60% of consumers in 2025 review ingredient labels before purchase, reinforcing the economic value of transparency in protein selection.

Health-focused consumption patterns drive the expansion of premium protein categories within wellness and functional nutrition segments. Demand increases for nutrient-dense options associated with digestibility and protein quality. Grass-fed protein aligns with these expectations through natural production attributes. Food manufacturers reformulate portfolios to meet clean-label standards, increasing procurement of such inputs. This shift supports supply chain differentiation and strengthens contract sourcing models.

Restraint - Competition from Alternative Protein Sources

Competition from alternative protein sources limits expansion by shifting consumer demand toward scalable and cost-efficient substitutes. Plant-based proteins, fermentation-derived proteins, and cultured protein formats attract investment due to lower production intensity and shorter development cycles. These alternatives align with evolving dietary trends focused on sustainability and ethical sourcing. Price positioning plays a critical role, as many substitutes enter the market at competitive price points. Retailers allocate shelf space toward high-velocity products, reducing visibility for premium animal-based offerings.

Operational efficiency gaps reinforce this restraint through supply-side pressure and margin constraints. Alternative proteins benefit from controlled production environments that enable consistent output and reduced dependency on natural variables. In contrast, pasture-based systems depend on land availability, climate stability, and longer livestock growth cycles, limiting throughput. Investors and food manufacturers prioritize scalable inputs that support large-volume production and predictable cost structures.

Limited Supply due to Land and Resource Constraints

The market faces structural limitations linked to land availability and resource intensity. Pasture-based livestock systems require large grazing areas, which restrict herd expansion and output scaling. Arable land competes with crop cultivation and urban development, creating supply pressure. Productivity per acre remains lower than in intensive systems, reducing yield efficiency. Climate variability influences pasture quality, affecting animal growth rates and protein output consistency. Water usage and soil management demands further constrain operational capacity, creating supply rigidity and limiting response to rising demand.

Operational costs rise due to extended animal rearing cycles and lower stocking density. Producers face higher capital requirements for land acquisition and grazing management practices. Limited economies of scale restrict cost optimization, reducing competitiveness against conventional protein sources. Supply shortages create pricing premiums, which narrow accessibility in price-sensitive segments. Import dependency increases in regions with limited grazing land, exposing supply chains to trade fluctuations and logistics costs.

Opportunity - Innovation in Bioactive-rich Protein Derivatives

Bioactive-rich protein derivatives enable brands to move beyond basic nutrition into differentiated value tiers. These innovations embed peptides, immunoglobulins, and growth factors that support muscle preservation, immune function, and metabolic health across age segments. U.S. federal nutrition guidance emphasizes diets built on nutrient-dense proteins, reinforcing clinical and consumer preference for such products. This alignment with public-health priorities expands the addressable base for premium protein formats, particularly in active-lifestyle and aging-population segments where functional benefits justify higher price points.

Operational leverage emerges as producers scale bioactive extraction alongside primary protein output, reducing the per-unit cost of enrichment. The U.S. Department of Agriculture notes rising emphasis on whole, nutrient-dense foods in the 2025–2030 Dietary Guidelines, anchoring demand for bioactive-enriched proteins. Capital-efficient innovation platforms allow faster reformulation cycles, enabling rapid response to new scientific findings and shifting consumer expectations around health performance.

Plant-based Alternatives and Hybrid Protein Formulation Convergence

Plant-based protein growth creates new opportunities by combining it with grass-fed protein in blended products. These hybrid formulations improve product appeal across a wider group of consumers, including flexitarian and health-focused buyers. Blending allows companies to balance nutrition quality with cost efficiency, making products more accessible. According to the USDA Economic Research Service, U.S. soybean production reached about 4.3 billion bushels in 2025, ensuring a steady plant protein supply. This stable input base supports consistent production and helps companies scale hybrid product offerings efficiently.

Operational benefits increase as companies reduce dependence on a single protein source. Hybrid formulations improve supply stability and help manage raw material cost fluctuations. Plant proteins enhance texture, shelf life, and processing flexibility, making products easier to manufacture across categories. This approach supports innovation in ready-to-eat foods, supplements, and beverages. Retail demand rises as these products align with sustainability trends and changing dietary habits.

Category-wise Analysis

Product Type Insights

Protein powders are anticipated to secure around 38% of the grass-fed protein market share in 2026, reflecting strong alignment with structured nutrition consumption patterns and established integration within fitness and clinical dietary regimes. High protein concentration and extended shelf life support daily supplementation and targeted nutrition programs. Dietitians recommend powders for dosage control and digestion efficiency. WHO guidance supports structured intake.

Ready-to-drink (RTD) beverages are expected to be the fastest-growing segment, propelled by increasing demand for convenience-oriented nutrition solutions and on-the-go consumption patterns. RTD formats eliminate preparation, supporting busy urban lifestyles. According to the World Health Organization, 55% of the global population lives in urban areas, strengthening demand for convenient nutrition. For example, FORALL Nutrition introduced Water+Protein, a clear grass-fed whey protein beverage, reflecting growing innovation in simplified RTD functional hydration formats.

Application Insights

Sports nutrition is likely to be the leading segment with a projected 36% of the grass-fed protein market share in 2026, due to the strong integration of protein supplementation within athletic performance and fitness routines. Structured training drives consistent protein intake for recovery and strength, with athlete requirements reaching 1.4–2.0 grams per kilogram daily. Guidance from WHO supports balanced protein intake. Trainer recommendations, clean-label positioning, and gym distribution strengthen adoption, while targeted formulations improve adherence and repeat usage.

Functional food & beverages are anticipated to be the fastest-growing segment, fueled by increasing integration of protein into everyday dietary consumption. Consumers seek multifunctional foods supporting energy and immunity. Guidance from European Food Safety Authority encourages functional ingredient use. Processing advances enable protein inclusion in snacks and beverages without taste compromise. Retail and e-commerce improve accessibility. For example, protein-fortified snacks and drinks gain traction among urban consumers, supporting routine intake and expanding adoption.

Regional Insights

North America Grass-fed Protein Market Trends

North America is expected to lead with an estimated 39% of the grass-fed protein market share in 2026, supported by strong alignment between premium nutrition demand and established consumer purchasing power. Government dietary data from the United States Department of Agriculture indicates that protein contributes around 16% of total daily energy intake among adults, with animal sources forming nearly two-thirds of consumption. This intake pattern reflects entrenched dietary reliance on high-quality protein sources.

Structured demand from fitness ecosystems and clinical nutrition programs reinforces consistent consumption levels. For example, widespread integration of protein supplements within gym routines and medical nutrition plans supports repeat purchase cycles. Advanced retail infrastructure and digital commerce platforms ensure continuous product availability. Strong livestock production systems aligned with pasture-based practices enable reliable sourcing of grass-fed raw materials. Investment in branded formulations and certification standards enhances product differentiation.

Europe Grass-fed Protein Market Trends

Europe reflects a mature landscape for grass-fed protein, supported by strict regulatory frameworks and a strong emphasis on traceability. Standards from the European Food Safety Authority reinforce labeling transparency and product credibility. Germany and France show stable demand driven by clean-label preferences. The U.K. demonstrates strong adoption within sports nutrition and functional foods. Ireland supports high-quality sourcing through pasture-based livestock systems, ensuring consistent protein quality and supply reliability across established consumption channels.

Consumption patterns shift toward integration into everyday foods such as dairy, snacks, and beverages. Italy and Spain show increasing interest in protein-enriched traditional products aligned with health awareness. Retail consolidation and private-label expansion improve affordability across broader consumer groups. Investment in sustainable agriculture supports alignment with environmental policies. Advanced logistics and cross-border trade networks enable efficient distribution. Innovation in fortified and clean-label formulations strengthens differentiation and supports premium positioning across diverse dietary segments.

Asia Pacific Grass-fed Protein Market Trends

Asia Pacific is forecast to be the fastest-growing market for grass-fed protein, stimulated by rapid dietary shifts toward high-quality nutrition and expanding middle-income population segments. Urban consumers show increasing preference for premium and traceable protein sources. According to the World Bank, the East Asia and Pacific urban population exceeds 60%, reflecting strong demand for convenient nutrition formats. Australia supports supply through pasture-based livestock systems. China shows rising demand for clean-label protein. India reflects growth in fitness participation and supplementation trends across urban populations.

Rising integration of protein into functional foods and beverages supports diversified consumption beyond supplements. Japan demonstrates a strong demand for fortified nutrition aligned with active aging trends. South Korea shows increasing adoption of convenient protein formats within urban lifestyles. For example, protein-enriched beverages and snacks gain traction in retail chains across Singapore and Indonesia, supporting daily consumption habits. Investment in cold chain and localized processing improves product stability and availability.

Competitive Landscape

The global grass-fed protein market reflects a moderately fragmented structure, with a combination of global nutrition companies and specialized clean-label protein manufacturers. Leading players such as Fonterra Co-operative Group, Glanbia, Nestlé S.A., Saputo, Arla Foods, Danone S.A., Lactalis Group, and Kerry Group maintain strong positions through integrated dairy supply chains and established distribution networks.

Mid-sized and emerging brands focus on niche positioning through organic certification, clean-label claims, and direct-to-consumer strategies. Product differentiation centers on functional nutrition formats, including powders, beverages, and fortified foods. Competitive strength depends on sourcing transparency, protein quality, and innovation in formulation technologies.

Key Industry Developments:

- In April 2026, Clean Simple Eats expanded distribution of its grass-fed whey protein isolate products through a nationwide retail launch across major outlets, strengthening mainstream accessibility for clean-label and performance nutrition consumers and reinforcing the growing integration of grass-fed protein into mass retail functional food channels.

- In March 2026, PepsiCo introduced Good Warrior, a protein snack brand featuring grass-fed beef sticks delivering 10 grams of protein per serving, expanding its portfolio into functional, high-protein convenience foods designed for busy consumers and strengthening the integration of grass-fed protein into mainstream snacking formats.

- In October 2025, Shaklee introduced a sparkling beverage containing 40 grams of grass-fed whey protein, highlighting innovation in functional ready-to-drink nutrition formats and expanding clean-label protein applications within the grass-fed protein market.

Companies Covered in Grass-fed Protein Market

- Fonterra Co-operative Group

- Glanbia plc

- Nestlé S.A.

- Saputo Inc.

- Arla Foods

- Danone S.A.

- Lactalis Group

- Kerry Group plc

- Now Health Group Inc.

- Garden of Life

- Orgain Inc.

- Vital Proteins LLC

- True Nutrition Inc.

Frequently Asked Questions

The grass-fed protein market is projected to reach US$1.9 billion in 2026.

Rising demand for clean-label, sustainable, and high-quality protein sources across sports nutrition, functional foods, and clinical dietary applications drives the grass-fed protein market.

The grass-fed protein market is poised to witness a CAGR of 8.9% from 2026 to 2033.

Expansion in functional food innovation, premium nutrition adoption, and e-commerce-driven direct-to-consumer channels creates key market opportunities for grass-fed protein.

Some of the key market players include Fonterra Co-operative Group, Glanbia, Nestlé S.A., Saputo, Arla Foods, Danone S.A., Lactalis Group, and Kerry Group.