- Sporting Goods & Equipment

- Golf Equipment Market

Golf Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Golf Equipment Market by Product Type (Golf Clubs, Golf Balls, Golf Gear & Accessories, Apparel & Footwear), Price Range (Premium, Mid-Range, Economy), Distribution Channel (Offline, Online), and Regional Analysis, 2026 - 2033

Golf Equipment Market Size and Trend Analysis

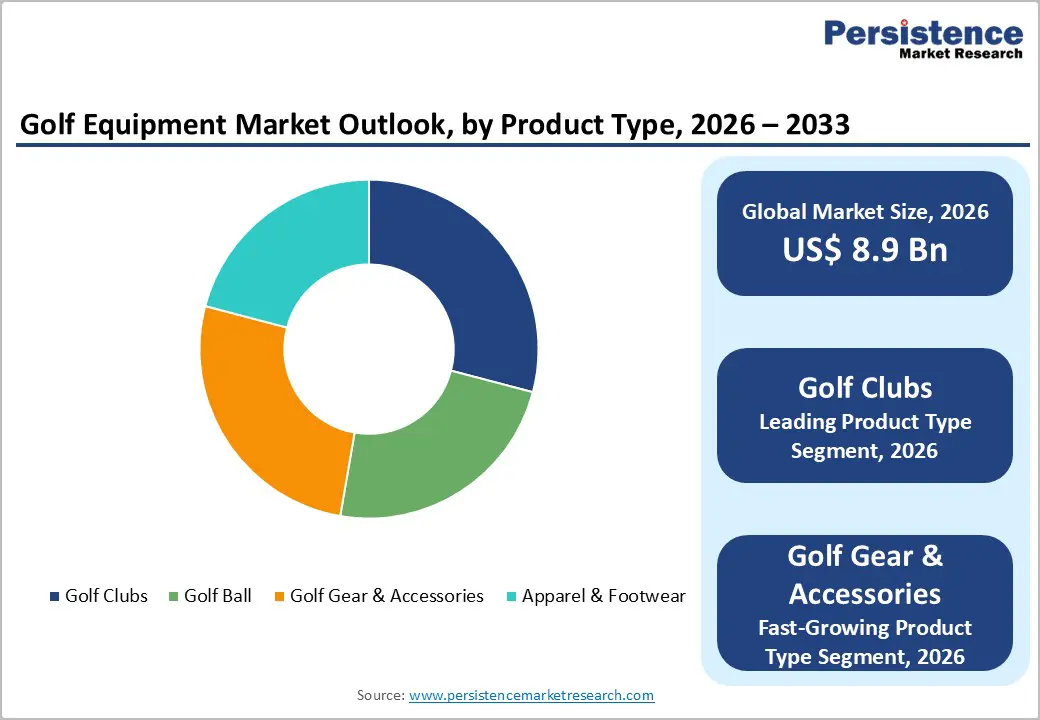

The global golf equipment market size is expected to be valued at US$ 8.9 billion in 2026 and projected to reach US$ 12.9 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. This growth trajectory is underpinned by a sustained post-pandemic resurgence in golf participation globally, rapid adoption of technologically advanced equipment, and expanding golf infrastructure across emerging economies.

The Golf Equipment Manufacturers Association (GEMA) and leading industry bodies have noted a consistent uptick in beginner and recreational golfer registrations since 2020, driving demand across all product categories. Premium club technologies such as adjustable drivers, multi-material irons, and smart-sensor embedded balls are further accelerating average selling prices and overall market revenues.

Key Market Highlights

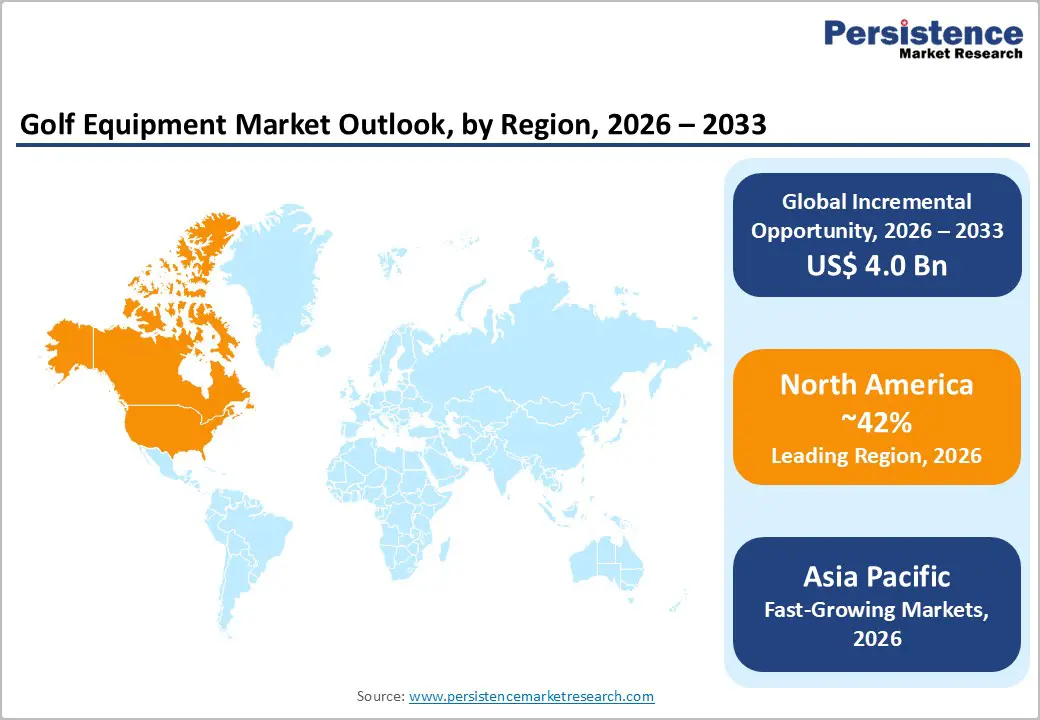

- Leading Region: North America: North America leads the global golf equipment market with 42% share in 2025, supported by the U.S.’s 41+ million golfers, high disposable income, and strong retail and golf course infrastructure.

- Fastest Growing Region: Asia Pacific: Asia Pacific is the fastest-growing region, driven by rapid golf infrastructure expansion in China, South Korea, and Southeast Asia, along with rising middle-class spending on premium sports equipment.

- Dominant Segment: Golf Clubs: Golf clubs dominate with 45% share in 2025, supported by high-value pricing, frequent upgrades, AI-driven innovation, and strong demand for custom-fitted performance equipment.

- Fastest Growing Segment: Online Distribution: Online channels are growing the fastest due to rising e-commerce adoption, direct-to-consumer strategies, and increasing preference among younger, tech-savvy golfers.

- Key Opportunity: Women & Junior Golf: Women and junior golfers represent a major growth opportunity, with rising female participation and over 3.4 million junior players driving long-term equipment demand expansion.

Market Dynamics

Drivers - Rising Global Golf Participation and Institutional Infrastructure Expansion Driving Demand

Rising global participation in golf is a key growth driver for the golf equipment market, supported by increasing engagement among younger and recreational players. The National Golf Foundation reported over 41.1 million golfers in the United States in 2023, while the R&A estimated 66.6 million players across 208 countries globally. This reflects a strong post-pandemic recovery and sustained long-term adoption of the sport across regions.

Government-led infrastructure development in the Asia Pacific and Europe is further accelerating market expansion. Countries such as China, Japan, and South Korea are investing heavily in golf courses and membership programs. This expanding player base is directly driving demand for clubs, balls, apparel, and accessories across all price segments, supporting both first-time and repeat equipment purchases.

Technological Innovation and Premiumization Transforming Golf Equipment Demand Dynamics

Technological innovation is transforming the golf equipment market by driving premium product adoption and performance-focused purchasing behavior. Companies such as Callaway, TaylorMade, and Acushnet are integrating AI-based design, advanced composite materials, and aerodynamic engineering into clubs and balls. Innovations like AI-optimized clubfaces and high-speed ball technologies are enhancing accuracy, distance, and consistency for players.

Custom-fitting solutions powered by TrackMan and Foresight Sports are further accelerating premiumization trends. Golfers increasingly prefer personalized equipment for performance gains, boosting demand for high-end products. Additionally, the global sports technology sector growing at over 17% CAGR, is reinforcing adoption of smart and connected golf equipment, creating new revenue opportunities for manufacturers worldwide.

Restraints - High Cost of Participation and Premium Equipment Restricting Mass Market Adoption

High cost of participation remains a major restraint for the golf equipment market despite rising global interest in the sport. A complete entry-level golf club set from established brands typically ranges between USD 300 and USD 700, while premium sets can exceed USD 3,000. When combined with additional expenses such as course fees, apparel, footwear, and accessories, golf remains one of the most expensive recreational sports globally.

A 2023 Sports & Fitness Industry Association survey identified cost as the primary barrier preventing new participants from entering the sport. This affordability challenge is particularly severe in price-sensitive emerging economies across Latin America, South Asia, and Africa. As a result, high equipment costs significantly restrict broader adoption and limit overall addressable market expansion, especially in developing regions.

Limited Golf Infrastructure in Developing Regions Constricts Market Expansion

Limited accessibility to golf infrastructure continues to restrain the global golf equipment market, as course availability remains heavily concentrated in developed economies. According to the R&A Golf Around the World report, over 75% of the world’s 38,864 golf facilities are located in just 10 countries, primarily in North America and Europe. This uneven distribution creates a structural imbalance in global participation levels.

Emerging regions such as Africa, South Asia, and parts of Latin America face challenges including land constraints, high development costs, and limited maintenance expertise. Regulatory barriers further slow course development. Without sufficient golf course access, equipment demand in these regions remains suppressed, restricting geographic diversification and preventing the market from achieving balanced global penetration and long-term growth potential.

Opportunities - Expansion of Golf Simulators and Indoor Golf Venues Unlocking New Equipment Demand Channels

The rapid expansion of indoor golf simulators and entertainment-driven golf venues is creating a strong growth opportunity for the golf equipment market. Concepts such as Topgolf, Drive Shack, and PopStroke have made golf more accessible to urban populations by removing the need for traditional course access. Topgolf alone reported over 30 million annual visitors across its global venues in 2023, significantly increasing exposure to the sport.

This exposure is directly converting casual participants into equipment buyers. According to the National Golf Foundation, individuals who first experience golf through off-course facilities are more likely to purchase equipment within 12 months. Additionally, rising adoption of home golf simulators from brands like SkyTrak and Full Swing is creating demand for simulator-optimized clubs and balls, opening a new high-value product segment.

Women’s and Junior Golf Segments Emerging as High-Growth Untapped Markets

The women’s and junior golf segments are emerging as significant untapped growth opportunities for the golf equipment market. According to the National Golf Foundation, women represented approximately 25% of all U.S. golfers in 2023, marking a record high. Meanwhile, junior golfers exceeded 3.4 million on-course participants, reflecting strong long-term participation potential and pipeline development for the sport.

Leading manufacturers such as Callaway, PING, and Cobra Golf are introducing dedicated women-specific product lines featuring lighter shafts, ergonomic designs, and improved performance customization. Institutional programs from the LPGA, USGA, and other bodies are further promoting inclusivity and participation. In addition, apparel and footwear brands targeting female golfers are expanding cross-category opportunities, positioning these segments as key drivers of future equipment demand growth.

Category-wise Analysis

Product Type Insights

Golf clubs dominate the product type segment, accounting for approximately 45% of the total golf equipment market share in 2025. Their dominance is driven by their essential role in gameplay, higher average selling prices, and frequent replacement cycles. Continuous innovation in materials such as titanium faces, carbon composite structures, and adjustable hosel systems is encouraging regular upgrades across all player categories.

Driver and iron sets remain the highest revenue-generating categories in retail sales, supported by strong demand from both amateur and professional golfers. Custom fitting has further strengthened club sales, with a large portion of purchases involving personalized specifications. Premium club sets priced above USD 1,500 are also gaining traction, reinforcing the segment’s strong revenue leadership in the global market.

Price Range Insights

The premium price segment holds the largest share of the golf equipment market at approximately 42% in 2025. This dominance is supported by strong brand loyalty toward manufacturers such as Titleist, TaylorMade, and PING, along with a consumer base that prioritizes performance, precision, and product prestige over cost considerations. High-end golf balls and club sets continue to perform strongly across major developed markets.

The fastest-growing momentum is emerging in the mid-to-premium upgrade transition, where golfers increasingly shift toward higher-value equipment driven by customization and performance optimization. Influenced by digital marketing and professional player endorsements, younger golfers are also adopting premium equipment earlier in their playing journey. This behavioral shift is steadily strengthening value-based growth across the overall pricing structure of the market.

Distribution Channel Insights

The offline distribution channel dominates the golf equipment market with approximately 62% share in 2025. This leadership is driven by the experiential nature of golf purchases, where consumers prefer in-store fittings, physical testing, and expert guidance before buying high-value equipment. Specialty retailers, pro shops, and sporting goods chains remain critical touchpoints for consumer decision-making.

The fastest-growing shift is occurring in online distribution, supported by rising e-commerce adoption and direct-to-consumer brand strategies. Digital platforms are increasingly offering virtual fittings, product customization tools, and AI-based recommendations, improving buyer confidence. Convenience, wider product availability, and promotional pricing are further encouraging online purchases, gradually reshaping the traditional retail structure of the golf equipment industry while complementing offline channels.

Regional Insights

North America Golf Equipment Market Trends and Insights

North America dominates the global golf equipment market, holding approximately 42% of total market share in 2025, underpinned by the world's largest and most mature golf participation base, extensive course infrastructure exceeding 16,000 facilities, high disposable income among core golfers, and the presence of headquarters of global equipment leaders including Acushnet, Callaway, TaylorMade, and PING. The region is witnessing a resurgence in younger and diverse golfer participation, further propelling equipment replacement cycles.

- U.S. Golf Equipment Market Size

The United States is by far the largest individual country market, accounting for approximately 85% of North America's golf equipment revenues. With over 41 million golfers including off-course participants, the U.S. market is estimated at approximately USD 3.3 billion in 2026. Robust retail infrastructure, premium brand penetration, and technology-led product launches sustain strong demand annually.

Europe Golf Equipment Market Trends and Insights

Europe accounts for approximately 24% of global golf equipment revenues in 2025, driven by established golf cultures in the United Kingdom, Germany, Sweden, and France. The region benefits from a growing recreational golfer segment, rising investments in sustainable golf course management, and increasing women's participation driven by campaigns supported by the European Golf Association (EGA). Premium and mid-range equipment categories are particularly strong in this market.

- Germany Golf Equipment Market Size

Germany is among Europe's top golf equipment markets, with an estimated market share of approximately 14% within the European region in 2025. The German Golf Association (DGV) reported over 640,000 registered golfers as of 2023, with continued growth in new entrants. Rising golf club memberships, supported by domestic retail expansion and premium brand availability, position Germany as a steady-growth market.

- U.K. Golf Equipment Market Size

The United Kingdom remains Europe's single largest golf equipment market, holding approximately 28% of regional revenues in 2025. England Golf reported approximately 870,000 affiliated golfers, while total participation, including non-affiliated players, is significantly higher. The U.K. benefits from a deeply embedded golf culture, a large base of premium consumers, and a strong retail presence from national chains and on-course shops.

- France Golf Equipment Market Size

France represents a growing golf equipment market in Europe, with an estimated 9% regional share in 2025. The French Golf Federation (FFG) reported approximately 420,000 licensed golfers in 2023. Government initiatives to promote golf as part of the national sports development agenda, combined with the country's hosting of the 2024 Paris Olympics, where golf featured as a competition sport, have catalyzed fresh consumer interest and equipment uptake.

Asia Pacific Golf Equipment Market Trends and Insights

Asia Pacific is the fastest-growing regional market for golf equipment, projected to expand at a CAGR of approximately 7.2% through 2033, and holds an estimated 22% global market share in 2025. China, Japan, South Korea, and Australia are core contributors, with China emerging as a pivotal growth engine. The China Golf Association projected golf participation in China to surpass 5 million registered players by 2025. Rapid urbanization, rising middle-class incomes, and government support for sports infrastructure are powering regional growth.

- India Golf Equipment Market Size

India is an emerging market within the Asia Pacific, estimated to account for approximately 4% of the regional market in 2025. The Professional Golf Tour of India (PGTI) and corporate golf culture in cities like Bangalore, Mumbai, and Delhi are key demand drivers. Rising affluent consumer spending and the expansion of premium golf facilities are gradually building a more robust equipment demand base.

- Japan Golf Equipment Market Size

Japan is one of the Asia Pacific's most mature and largest golf markets, contributing approximately 30% of regional equipment revenues in 2025. With over 7 million golfers and a highly sophisticated consumer base, Japan has a robust demand for premium and technologically advanced equipment. Domestic brands such as Honma Golf and XXIO (Sumitomo Rubber) coexist competitively with global brands, reflecting the market's depth.

- Southeast Asia Golf Equipment Market Size

Southeast Asia is an exciting high-growth sub-region, estimated to hold approximately 10% of the Asia Pacific regional market in 2025. Markets such as Thailand, Malaysia, Indonesia, and Vietnam are witnessing rapid golf infrastructure expansion, with Thailand alone hosting over 250 golf courses. Golf tourism, affluent consumer growth, and a young, aspiring middle-income population is fueling consistent equipment demand across the sub-region.

Competitive Landscape

The global golf equipment market is moderately consolidated, with a small group of leading manufacturers dominating overall revenue through strong brand positioning and continuous product innovation. Competition is primarily driven by technological differentiation, product performance, and endorsement visibility across professional tournaments. Companies compete by investing heavily in advanced materials, precision engineering, and design enhancements that improve distance, accuracy, and player experience across all skill levels.

Mid-tier and emerging players focus on value-driven offerings and niche positioning to capture price-sensitive and developing market segments. The competitive environment is also evolving with growing emphasis on direct-to-consumer sales, digital retail channels, and customization-based offerings. Sustainability initiatives, including the use of recycled materials and eco-friendly manufacturing processes, are increasingly becoming key differentiators across the industry.

Key Developments:

- In January 2025, Topgolf Callaway Brands announced the strategic spin-off of the Topgolf entertainment business to unlock shareholder value and allow the core golf equipment division to focus on product innovation and global expansion.

- In March 2024, TaylorMade Golf launched its Qi10 driver series, integrating next-generation Qi-Weighted technology for maximum forgiveness, becoming the #1 played driver on the PGA TOUR within weeks of its commercial release.

- In August 2024, Acushnet Holdings reported record net sales of USD 648.3 million in its Q2 2024 earnings, driven by strong demand for Titleist golf balls and clubs, underscoring the continued premiumization of the category.

Golf Equipment Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 6.9 Billion |

| Current Market Value (2026) | US$ 8.9 Billion |

| Projected Market Value (2033) | US$ 12.9 Billion |

| CAGR (2026 - 2033) | 5.4% |

| Leading Region | North America, 42% market share (2025) |

| Dominant Category - Product Type | Golf Clubs, 45% market share (2025) |

| Top-ranking Category - Price Range | Premium Segment, 42% market share (2025) |

| Incremental Opportunity (2026-2033) | US$ 4.0 Billion |

Companies Covered in Golf Equipment Market

- Callaway Golf Company

- TaylorMade Golf Company

- Acushnet Holdings Corp.

- PING

- Cobra Golf

- Mizuno Corporation

- Bridgestone Golf

- Sumitomo Rubber Industries

- Wilson Sporting Goods

- Parsons Xtreme Golf (PXG)

- Yonex Co., Ltd.

- Honma Golf Co., Ltd.

- Tour Edge Golf Manufacturing

- Volvik Co., Ltd.

- Globeride, Inc.

Frequently Asked Questions

The global golf equipment market is estimated to be valued at US$ 8.9 billion in 2026. This valuation reflects a historical CAGR of 4.3% between 2020 and 2025, driven by post-pandemic resurgence in golf participation.

The primary demand drivers include the global expansion of golf participation with the R&A reporting 66.6 million golfers across 208 countries in 2023 and continuous technological innovation.

North America is the leading region, accounting for approximately 42% of global golf equipment market share in 2025. The United States is the primary driver, with over 41 million golfers, over 16,000 golf facilities.

The most significant growth opportunity lies in the expansion of the women's and junior golf segments. The NGF reported record women's participation at 25% of U.S. golfers in 2023, while junior participation exceeded 3.4 million.

The global golf equipment market is led by Acushnet Holdings Corp., Topgolf, Callaway Brands Corp., and TaylorMade Golf Company.