- Processed Food

- Gluten-free Food Market

Gluten-free Food Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Gluten-free Food Market by Product Type (Bakery & Confectionery, Snacks & RTE Products, Dairy Products, Sauces & Dressings, Meat & Meat Substitutes, Others), Source (Plant, Animal), Distribution Channel (HoReCA, Hypermarkets/Supermarkets, Convenience Store, Specialty Store, Online Retail, Others), and Regional Analysis, 2026 - 2033

Gluten-free Food Market Share and Trends Analysis

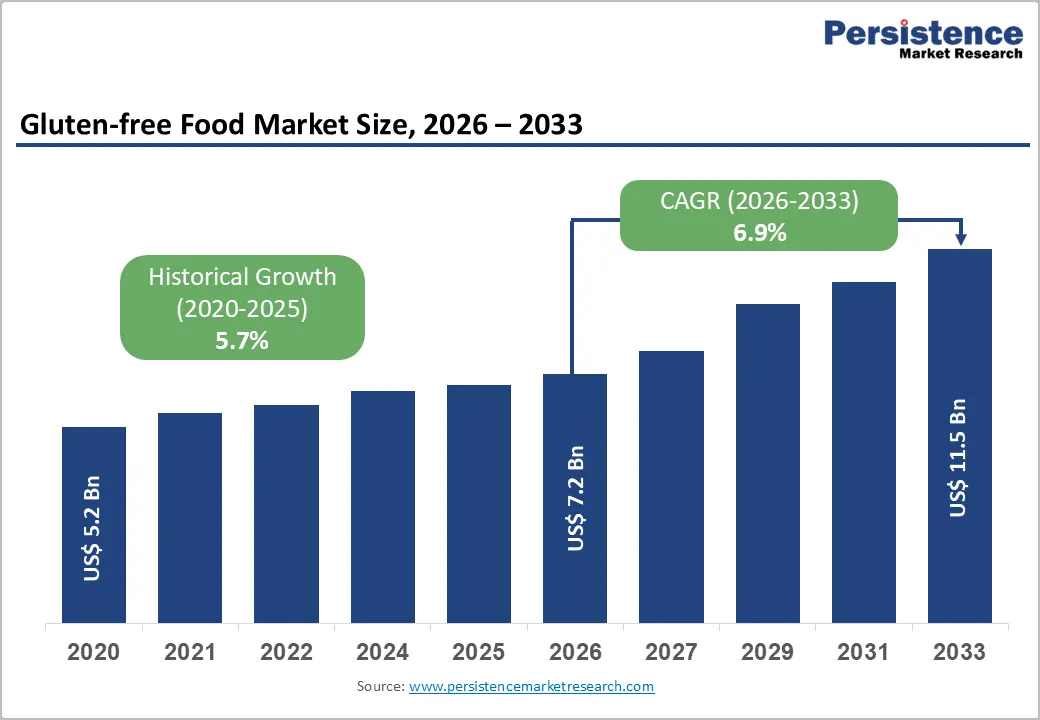

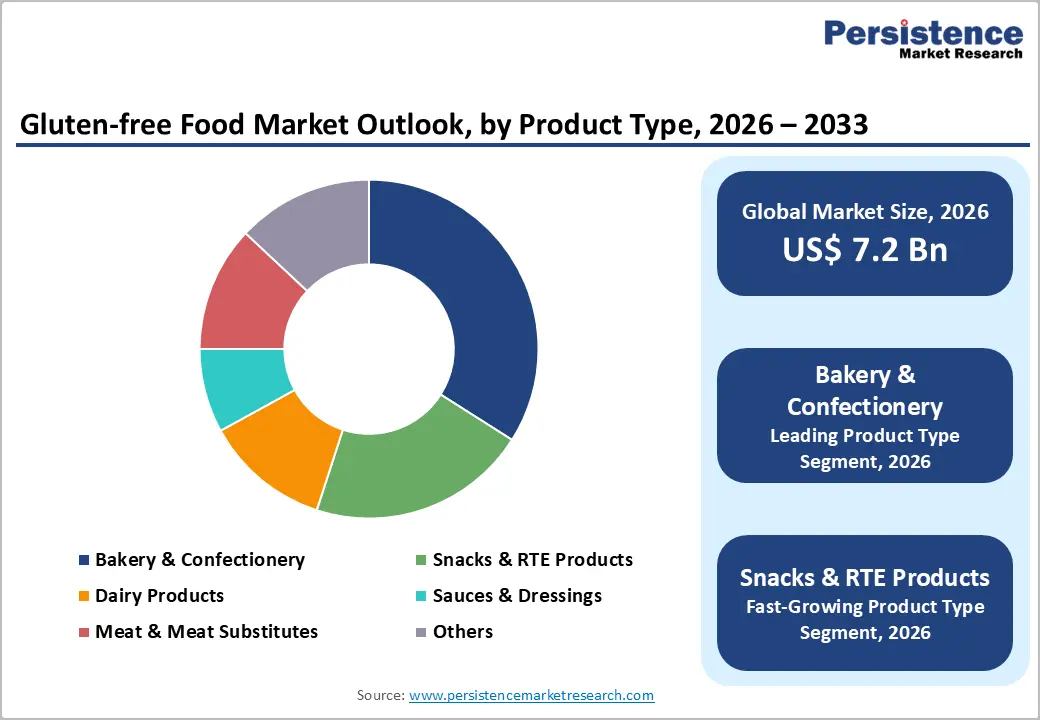

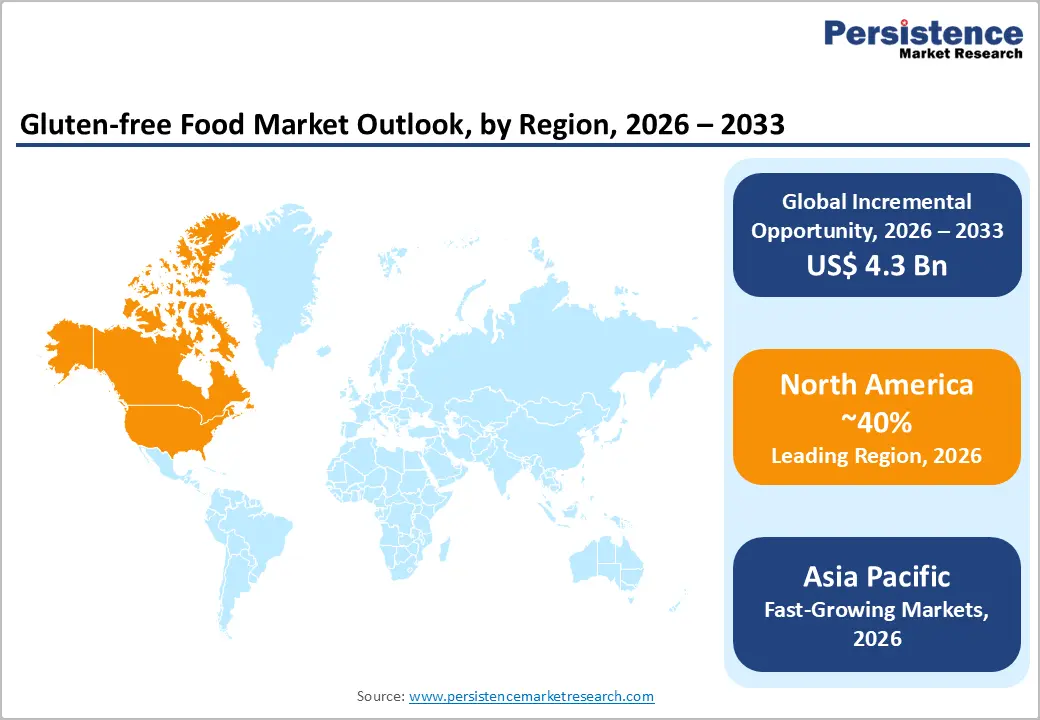

The global gluten-free food market is estimated to grow from US$ 7.2 billion in 2026 to US$ 11.5 billion by 2033. The market is projected to record a CAGR of 6.9% during the forecast period from 2026 to 2033.

The Gluten-free Food Market is rapidly transitioning from a niche dietary segment to a mainstream wellness category, fueled by rising health awareness and lifestyle-driven consumption. Strong innovation across plant-based ingredients and convenient formats is reshaping product development and consumer adoption globally.

Key Industry Highlights

- Leading Region: North America dominates with 40% share (2025), driven by strong regulatory frameworks, high diagnosis rates of gluten intolerance, and advanced product innovation.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, supported by urbanization, dietary shifts, and expanding access to Gluten free products through e-commerce platforms.

- Leading Source: Plant-based segment leads with 74% share (2025), owing to natural Gluten free properties, cost efficiency, and strong alignment with clean-label and vegan trends.

- Fastest Growing Segment (By Product Type): Snacks and RTE products are witnessing the highest growth, driven by rising demand for convenient, portable, and functional Gluten free options.

- Key Market Driver: Increasing prevalence of celiac disease and gluten intolerance is expanding the core consumer base, supported by improved diagnostics and rising health awareness.

- Key Market Opportunity: Expansion into wellness-focused and snacking categories is creating strong growth potential, with brands leveraging digestive health, weight management, and convenience-driven positioning.

Market Dynamics

Driver: Increasing Prevalence of Celiac Disease and Gluten Intolerance

The rise in global incidence of celiac disease and gluten intolerance is fundamental for Gluten-free Food Market growth. According to the Celiac Disease Foundation, the condition affects nearly 1 in 100 people worldwide, though a significant portion remains undiagnosed. As diagnostic capabilities improve and routine screenings become more widespread, particularly in developed regions, a growing number of individuals are required to adopt strict gluten free diets. Health authorities such as the National Institutes of Health emphasize that lifelong gluten avoidance remains the only effective treatment, ensuring a sustained and expanding consumer base.

Beyond clinical diagnosis, increasing awareness of gluten sensitivity and digestive health is influencing broader dietary behavior. A notable share of consumers, especially in the United States, are voluntarily reducing gluten intake as part of wellness-focused lifestyles. This shift is driving demand across mainstream retail and foodservice channels, encouraging manufacturers to expand Gluten free portfolios with clean-label, allergen-free, and functional offerings.

Restraint: High Costs and Supply Constraints Limit Adoption

The Gluten-free Food Market faces challenges due to limited availability and high costs of essential raw materials. Key ingredients such as sorghum, millet, quinoa, amaranth, and certified Gluten free oats are subject to seasonal variability, restricted cultivation, and stringent sourcing standards to avoid cross-contamination. These constraints create supply inconsistencies and elevate procurement costs, particularly impacting small and mid-sized manufacturers. In addition, climate-related risks and global supply chain disruptions further affect price stability and availability, limiting scalability and slowing product innovation in emerging markets.

Production complexities add another layer of restraint. Gluten free formulations rely on premium alternative flours and functional additives such as xanthan gum to replicate gluten’s texture, increasing manufacturing costs. Compliance with standards set by organizations such as the Gluten free Certification Organization requires dedicated facilities or rigorous cleaning protocols, further raising operational expenses. As a result, Gluten free products often carry a significant price premium, restricting accessibility for price-sensitive consumers and limiting widespread adoption, particularly in developing economies.

OPPORTUNITY: Expanding into Wellness and Snacking Categories

The Gluten-free Food Market is unlocking new growth avenues as brands increasingly position products around weight management and digestive health benefits. Beyond medical necessity, Gluten free offerings are being marketed as lighter, gut-friendly, and aligned with overall wellness goals, attracting a broader consumer base. Ingredients such as quinoa, buckwheat, and chia enhance nutritional value with added fiber and micronutrients, reinforcing digestive health claims. Brands like KIND Snacks exemplify this strategy by promoting portion-controlled, Gluten free snacks focused on balanced nutrition and satiety, strengthening consumer engagement in the better-for-you segment.

Simultaneously, the rapid expansion of snacks and ready-to-eat (RTE) categories presents a high-growth opportunity. Evolving lifestyles and increased snacking frequency are driving demand for convenient, portable Gluten free options. Companies such as PepsiCo, Inc. highlight rising consumer preference for functional, savory snacks. Advances in processing technologies are enabling improved taste and texture, allowing Gluten free chips, crackers, and bars to compete directly with conventional products, while new retail channels further accelerate market penetration.

Category-wise Analysis

By Source Insights

Plant-based Gluten free foods account for a dominant share of approximately 74% in 2025, driven by their natural compatibility with Gluten free formulations and growing consumer preference for health-focused diets. Ingredients such as rice, corn, pulses, and ancient grains like millet and buckwheat are inherently Gluten free, making them widely adopted across large-scale food processing. Their cost efficiency, availability, and versatility further strengthen their position, particularly in staple categories such as bakery, snacks, and ready-to-eat meals. As awareness of gluten intolerance rises, consumers increasingly favor plant-derived alternatives that offer both safety and nutritional value.

The segment is also benefiting from the strong convergence of Gluten free and plant-based dietary trends, especially among younger consumers prioritizing sustainability and clean-label consumption. Plant-based ingredients are rich in fiber, vitamins, and antioxidants, supporting digestive health and overall wellness. Leading companies such as Bob’s Red Mill Natural Foods are leveraging this trend by expanding portfolios centered on whole grain flours and plant-based formulations, reinforcing the segment’s long-term growth trajectory.

By Product Type Insights

Snacks and ready-to-eat (RTE) products are projected to register strong growth in the global Gluten-free Food Market, driven by shifting consumption patterns and the increasing need for convenience. Modern consumers are moving toward frequent snacking, favoring portable, nutritious options that align with dietary sensitivities and fast-paced lifestyles. Gluten free snacks are benefiting from rapid innovation, with manufacturers incorporating clean-label ingredients, plant-based formulations, and functional benefits such as added protein and fiber. Insights from Mondelez International highlight that a majority of consumers’ snack for both emotional and functional reasons, reinforcing the category’s everyday relevance.

At the same time, Gluten free RTE offerings are becoming integral to daily diets, providing safe and accessible meal solutions for health-conscious and intolerant consumers alike. While bakery and confectionery remain dominant due to staple consumption, snacks and RTE categories are gaining momentum through product diversification and improved taste profiles. This evolution is positioning the segment as a key growth engine within the broader Gluten free market.

Regional Insights

North America Gluten-free Food Market Trends

North America leads the global Gluten-free Food Market, accounting for 40% share, supported by strong awareness of gluten intolerance and advanced regulatory frameworks. Standards set by the U.S. Food and Drug Administration have enhanced product labeling transparency, strengthening consumer trust. The region benefits from a mature retail ecosystem, high product innovation, and growing demand for clean-label, allergen-free foods. Expansion across bakery, snacks, and ready-to-eat segments continues to reinforce market leadership.

- U.S. Gluten-free Food Market Trends

The U.S. remains the largest contributor, driven by high diagnosis rates and strong lifestyle adoption of Gluten free diets. Advocacy from organizations like the Celiac Disease Foundation has improved awareness, while continuous product innovation across snacks, bakery, and beverages sustains growth. Consumers increasingly prioritize premium, organic, and functional Gluten free options.

- Canada Gluten-free Food Market Trends

Canada is witnessing rapid growth, supported by rising health awareness and evolving food processing capabilities. Increasing demand for clean-label and non-GMO Gluten free products, along with expanding retail and e-commerce availability, is driving adoption. Consumers are also showing a preference for convenient, ready-to-eat Gluten free meal solutions.

Asia Pacific Gluten-free Food Market Trends

Asia Pacific is the fastest-growing Gluten free market, driven by dietary shifts, urbanization, and rising awareness of digestive health. Westernized eating habits are increasing gluten consumption, indirectly boosting demand for Gluten free alternatives. The region benefits from strong raw material availability such as rice and pulses, supporting cost-effective production. Additionally, rapid expansion of e-commerce platforms like Alibaba and JD.com is improving accessibility of specialty Gluten free products across urban and semi-urban markets.

- China Gluten-free Food Market Trends

China’s market is gaining traction among affluent urban consumers seeking premium, health-oriented diets. Rising awareness of autoimmune and digestive conditions is driving demand for imported Gluten free snacks and flours. Growth is heavily supported by online retail channels and the increasing availability of international brands targeting wellness-conscious consumers.

- India Gluten-free Food Market Trends

India’s market is expanding steadily, supported by traditional consumption of naturally Gluten free staples such as rice and millets. Rising health awareness, fitness trends, and increasing diagnosis of gluten intolerance are driving demand for packaged Gluten free foods, particularly in snacks and health-focused categories.

- Australia and New Zealand Gluten-free Food Market Trends

Australia and New Zealand represent a mature market with stringent labeling regulations ensuring high product quality. Strong consumer awareness and demand for clean-label products support steady growth, while innovation in bakery and ready-to-eat Gluten free foods continues to drive premiumization.

Competitive Landscape

The global Gluten-free Food Market is moderately fragmented, characterized by the presence of multinational corporations alongside specialized niche players. Large companies such as Nestlé, General Mills, Inc., and The Kraft Heinz Company are leveraging their extensive distribution networks to expand gluten free portfolios, either through product innovation or acquisition of smaller brands. At the same time, dedicated players like Dr. Schar USA Inc maintain a strong position through specialized expertise in formulation and product quality.

Competitive strategies are centered on diversification into new categories such as frozen meals and ethnic cuisines, along with continuous investment in R&D to enhance taste, texture, and nutritional value. Companies are increasingly incorporating functional ingredients like ancient grains, pulse proteins, and probiotics to strengthen product appeal. Additionally, the rise of e-commerce and direct-to-consumer models is enabling broader reach, while personalized nutrition and clean-label positioning continue to shape differentiation in an increasingly competitive market.

Key Industry Developments:

- In April 2026, Gerber upgraded its Puffs and Teether Wheels with a new recipe incorporating sorghum, a nutrient-dense Gluten free grain. The move aligns with clean-label trends and rising demand for allergen-friendly infant snacks.

- In February 2026, Bob's Red Mill expanded its oat portfolio with Chocolate Chip Instant Oatmeal Packets and Chocolate Hazelnut Overnight Protein Oats. The launch strengthens its Gluten free and Non-GMO instant oatmeal range while tapping into indulgent, protein-rich breakfast trends.

- In January 2026, General Mills launched a wide range of new cereals and granola snacks, focusing on protein-enriched and flavor-innovative offerings. The company also reintroduced two previously popular flavors, leveraging nostalgia alongside health-focused innovation.

Gluten-free Food Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.1 Bn |

| Projected Market Value (2026) | US$ 7.2 Bn |

| Projected Market Value (2033) | US$ 11.5 Bn |

| CAGR (2026 - 2033) | 6.9% |

| Leading Region | North America, 40% share |

| Dominant Source | Plant-based, 74% share |

| Top-ranking Product Type | Bakery & Confectionery, 34% share |

| Incremental Opportunity | US$ 4.3 Bn |

Companies Covered in Gluten-free Food Market

- The Hain Celestial Group Inc

- General Mills, Inc.

- The Kraft Heinz Company

- ConAgra Brands Inc

- Kellanova

- Mondelez International, Inc.

- Dr. Schar USA Inc

- Raisio Oyj

- Bob’s Red Mill Natural Foods

- Nestlé

- PepsiCo, Inc.

- Barilla G.E.R Fratelli S.P.A

- Kameda Seika Co., Ltd.

- Others

Frequently Asked Questions

The global Gluten-free Food Market is projected to be valued at US$ 7.2 Bn in 2026.

The increasing prevalence of Celiac Disease and Gluten Intolerance is driving the global Gluten-free Food Market.

The global Gluten-free Food Market is poised to witness a CAGR of 6.9% between 2026 and 2033.

Expanding into Wellness and Snacking Categories supplements is a key opportunity in the global Gluten-free Food Market.

The Hain Celestial Group Inc, General Mills, Inc., The Kraft Heinz Company, ConAgra Brands Inc, Kellanova, and Mondelez International, Inc.