- Animal Feed & Additives

- Corn Gluten Meal Market

Corn Gluten Meal Market Size, Share, and Growth Forecast, 2026 - 2033

Corn Gluten Meal Market by Product Type (Feed Grade Corn Gluten Meal, Food Grade Corn Gluten Meal, Industrial Grade Corn Gluten Meal), Livestock Type (Poultry, Ruminants, Swine, Aquaculture, Others), Application (Animal Feed, Pet Food, Food Products, Herbicides, Industrial Uses), and Regional Analysis for 2026 - 2033

Corn Gluten Meal Market Share and Trends Analysis

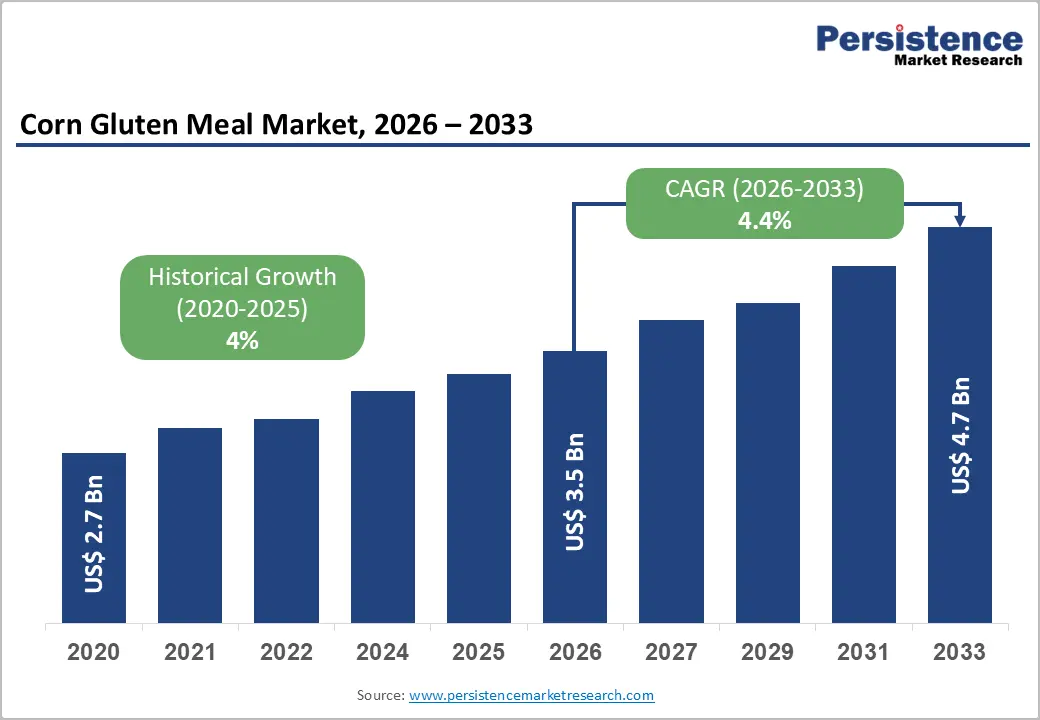

The global corn gluten meal market size is likely to be valued at US$ 3.5 billion in 2026 and is estimated to reach US$ 4.7 billion by 2033, growing at a CAGR of 4.4% during the forecast period 2026−2033. Stable demand expansion is driven by rising protein requirements in livestock nutrition alongside increasing meat consumption in emerging economies. Growth in poultry and aquaculture production sustains demand for high-protein feed ingredients, with corn gluten meal offering strong nutritional efficiency.

Urbanization and income growth shift diets toward protein-rich consumption, accelerating feed utilization. Advancements in feed formulation enable precise nutrient balancing, increasing inclusion rates. Biotechnology integration enhances yield and protein extraction quality, improving supply reliability. Expansion of organized livestock farming supports standardized procurement, while rising awareness of animal health drives preference for digestible, plant-based protein sources aligned with sustainability frameworks.

Key Industry Highlights:

- Leading Product Type: Feed-grade corn gluten meal is set to hold around 68% revenue share in 2026, driven by large-scale adoption in poultry.

- Fastest-Growing Product Type: Food-grade corn gluten meal is projected as the fastest-growing segment, supported by expansion in plant-based food applications.

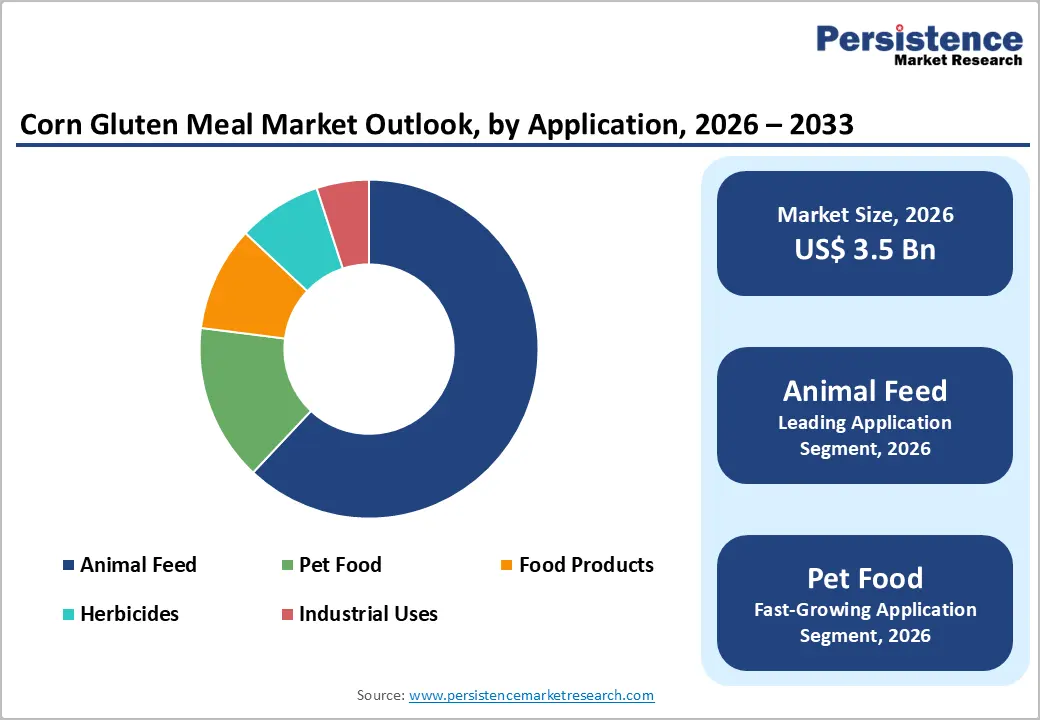

- Leading Application: Animal feed is estimated to hold roughly 62% revenue share in 2026, due to strong integration within commercial livestock production systems and consistent protein demand.

- Fastest-Growing Application: Pet food is forecasted to record the fastest growth between 2026 and 2033, driven by rising pet ownership and premium nutrition trends across urban markets.

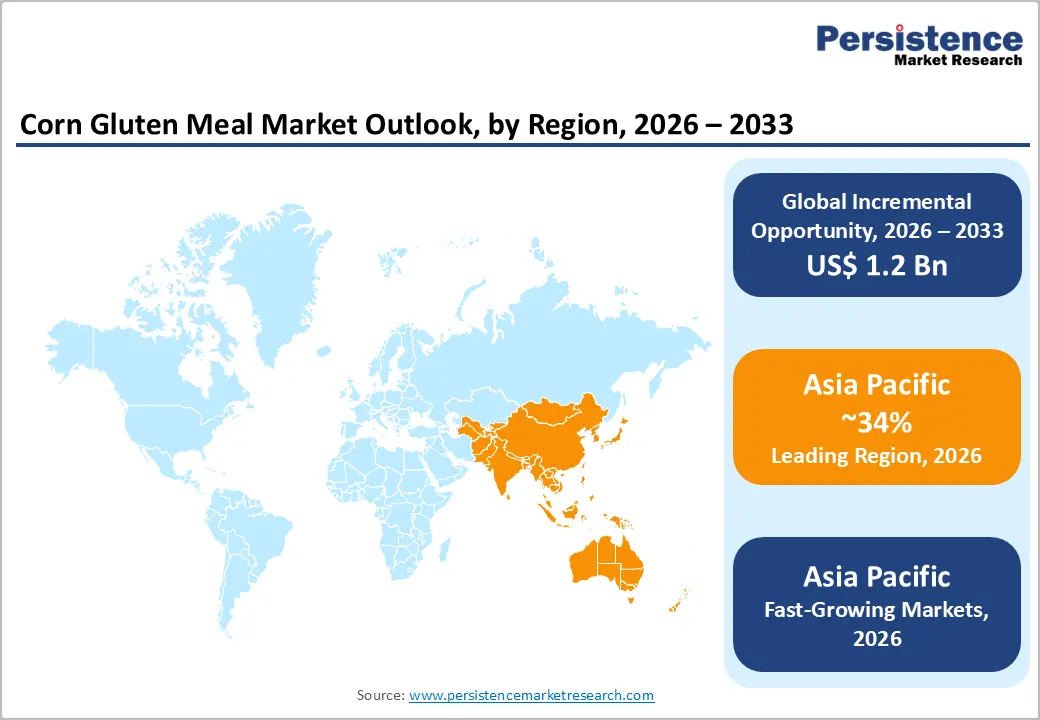

- Regional Leadership: Asia Pacific is projected to capture roughly 34% of the market share by 2026, while Asia Pacific is also forecasted to record the fastest growth between 2026 and 2033 due to expanding livestock production.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as Archer Daniels Midland and Cargill leveraging scale, supply chain integration, and processing efficiency to maintain competitive positioning.

- Innovation Trends: Technological advancements in corn wet milling, product diversification into specialty applications, and sustainability-focused feed solutions are shaping long-term market evolution and investment direction.

| Key Insights | Details |

|---|---|

|

Corn Gluten Meal Market Size (2026E) |

US$ 3.5 Bn |

|

Market Value Forecast (2033F) |

US$ 4.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4% |

DRO Analysis

Driver - Rising Global Demand for High-Protein Animal Feed

Escalating protein consumption trends across developing and developed economies drive sustained pressure on livestock production systems to deliver higher output efficiency. This dynamic elevates reliance on concentrated feed ingredients with superior protein density and digestibility. Corn gluten meal gains strategic importance within feed formulations due to consistent amino acid profile and cost-effective nutrient delivery. Poultry and aquaculture segments demonstrate accelerated scaling, reinforcing bulk procurement patterns. According to the United States Department of Agriculture (USDA), global poultry meat production reached approximately 107.55 million metric tons in 2025, reflecting strong demand intensity for protein-enriched feed inputs across industrial farming operations.

Feed manufacturers prioritize formulation precision to optimize feed conversion ratios and minimize input waste under cost-sensitive production environments. High-protein ingredients support metabolic efficiency, enabling faster growth cycles and improved yield outcomes. Corn processing advancements enhance protein concentration levels, strengthening its competitiveness against alternative plant-based sources. Large-scale livestock operations require standardized feed components that align with nutritional consistency and supply stability. Rising integration of commercial farming practices increases dependence on scientifically balanced diets, reinforcing demand for protein-rich inputs. Regulatory emphasis on sustainable feed sourcing further supports adoption of plant-derived protein concentrates within structured feed supply chains.

Technological Advancements in Corn Processing and Biorefining

Advanced processing systems and integrated biorefining frameworks elevate protein extraction efficiency from corn streams, strengthening output consistency for corn gluten meal. High-precision milling, enzymatic hydrolysis, and membrane separation technologies improve protein concentration levels while reducing residual waste. The United States Department of Agriculture reported US corn production at 17 billion bushels in 2025, reinforcing raw material availability for large-scale processing optimization. Enhanced throughput capacity lowers per-unit production cost, supporting competitive pricing across feed applications. Process automation enables uniform quality standards, which strengthens buyer confidence and supports long-term supply contracts within industrial livestock systems globally.

Biorefining integration converts corn into multiple high-value outputs, increasing economic viability of processing operations and stabilizing revenue streams. Co-product valorization, including ethanol, starch derivatives, and feed proteins, improves resource utilization efficiency and reduces operational waste intensity. This multi-output model supports scalability while maintaining consistent protein supply for feed manufacturers. Precision fermentation and enzyme optimization improve digestibility profiles, strengthening functional value in animal nutrition. Energy-efficient processing systems reduce production costs and align with sustainability targets, encouraging industry-wide adoption. Strong alignment between cost efficiency, output diversification, and quality enhancement drives sustained demand growth across commercial feed production networks globally.

Restraint - Volatility in Corn Supply and Pricing Structures

Fluctuations in raw material availability create cost uncertainty across the corn gluten meal market value chain. Weather variability, acreage shifts, and competing corn applications such as ethanol and food processing tighten supply visibility. Price swings in corn directly influence production input costs, limiting margin stability for processors and feed manufacturers. Procurement planning becomes complex, with short-term contracts replacing long-term sourcing strategies. Feed producers respond by adjusting formulations toward alternative protein ingredients, reducing dependency on corn-derived inputs. This substitution effect weakens volume consistency and constrains demand predictability across key livestock and aquaculture segments.

Unstable pricing structures reduce investment confidence across processing and distribution networks. Capital allocation decisions face delays as cost forecasting remains uncertain, affecting capacity expansion and technology upgrades. Variability in input pricing disrupts inventory management, leading to either excess stock or supply shortages. Smaller producers encounter higher exposure to price shocks, creating uneven competitive conditions. Downstream buyers such as feed mills face difficulty in maintaining consistent pricing for end users, impacting purchasing behavior. Regulatory pressure on cost transparency further intensifies operational complexity, limiting pricing flexibility and reducing overall efficiency within the supply chain.

Regulatory Constraints and Environmental Compliance Pressures

Stringent regulatory frameworks across feed safety, emissions, and agricultural processing create cost-intensive compliance requirements for the corn gluten meal market. Environmental standards targeting water usage, effluent discharge, and carbon emissions impose operational adjustments within corn processing facilities. Capital allocation toward pollution control systems and waste management infrastructure reduces margin flexibility. Regulatory approvals for feed ingredient usage vary across regions, limiting cross-border trade efficiency. Compliance verification processes increase administrative burden and extend product certification timelines. Smaller processors face entry barriers due to limited financial capacity, restricting competitive diversity and slowing capacity expansion across developing production clusters.

Environmental compliance pressures influence sourcing, processing efficiency, and supply chain stability. Corn cultivation faces scrutiny related to fertilizer use, soil degradation, and water intensity, affecting raw material availability and pricing stability. Processing plants encounter restrictions on energy consumption and emissions intensity, leading to higher operating expenditure. Shifts toward sustainable feed inputs encourage alternative protein sources, reducing demand concentration. Export-oriented suppliers navigate complex environmental labeling and traceability requirements, which elevate logistics and documentation costs.

Opportunity - Expansion of Aquaculture and Alternative Protein Supply Chains

Rising global fish consumption drives structural expansion in aquaculture systems, creating sustained demand for high-efficiency protein inputs. Intensive farming models require nutritionally consistent feed to optimize growth cycles and feed conversion ratios. Corn gluten meal supports this requirement through concentrated protein content and digestibility advantages. Production intensity elevates dependence on reliable feed ingredients with stable amino acid profiles. Supply chain alignment with aquaculture integrators strengthens procurement consistency, while cost efficiency supports margin control across large-scale farming operations, reinforcing steady uptake within commercial feed frameworks.

Parallel development of alternative protein supply chains increases focus on plant-based feed inputs within livestock and aquaculture nutrition systems. Regulatory frameworks emphasize reduced reliance on fishmeal, encouraging transition toward sustainable protein substitutes. Corn gluten meal benefits from this shift through established processing infrastructure and predictable availability. Feed manufacturers prioritize ingredients with scalable sourcing and formulation compatibility, improving inclusion across compound feed blends. Vertical integration across processing and feed production enhances operational efficiency and reduces supply volatility, while ongoing feed technology innovation expands functional application within high-performance nutrition programs.

Diversification into Industrial and Specialty Applications

Expansion into industrial and specialty applications creates a strong opportunity for the corn gluten meal market through value chain diversification and margin enhancement. Utilization in pet food, aquafeed additives, and organic fertilizers increases revenue streams beyond traditional livestock feed demand. Functional properties such as high protein concentration, pigment content, and binding capability support adoption in niche formulations. The Food and Agriculture Organization indicated in 2025 that global maize production surpassed 1.2 billion metric tons, ensuring consistent raw material availability for downstream processing. This scale supports cost-efficient allocation toward specialty segments with higher pricing realization and stable demand patterns.

Industrial demand is shifting toward sustainable and bio-based inputs, strengthening long-term growth potential. Application in biodegradable materials, natural herbicides, and fermentation substrates aligns with regulatory frameworks focused on environmental compliance and reduced chemical dependency. Specialty pet nutrition trends emphasize digestible plant proteins, creating premium positioning opportunities. Processing facilities enable flexible output allocation toward higher-margin industrial channels during feed demand fluctuations. Increasing investments in bio-refining technologies improve extraction precision and product customization, enabling targeted application development. Growing adoption across chemical, agriculture, and specialty nutrition sectors expands utilization scope and strengthens demand stability across diversified end-use industries.

Category-wise Analysis

Product Type Insights

Feed grade corn gluten meal is likely to be the leading segment with a revenue share of approximately 68% in 2026, due to strong integration within commercial livestock feed systems and consistent demand from poultry and aquaculture sectors. Feed-grade variants deliver high protein concentration and digestibility, supporting efficient feed conversion. Commercial manufacturers prioritize uniform nutrient profiles and reliable supply. Industrial livestock expansion drives bulk procurement through structured contracts. Cost-efficient protein sourcing strengthens adoption, especially in poultry operations. For example, integrated poultry producers utilize corn gluten meal to optimize feed efficiency and maintain consistent production output.

Food grade corn gluten meal is expected to witness the fastest growth between 2026 and 2033, as expanding application in specialty food formulations and plant-based protein products drives adoption. Rising awareness of alternative proteins and ingredient transparency supports use in processed foods. Functional benefits such as binding and protein enrichment enable innovation across snacks and bakery products. Improved refining enhances taste and safety standards. Regulatory clarity supports market entry. Growth in premium and fortified food categories expands commercial scope, supported by rising disposable income and urban consumption patterns.

Application Insights

Animal feed is poised to lead with a forecasted over 62% share in 2026, owing to extensive utilization across poultry, aquaculture, and ruminant nutrition systems. Commercial livestock production depends on balanced feed formulations to improve growth efficiency and disease resistance. Corn gluten meal provides a concentrated, digestible protein source for compound feed manufacturing. Consumer trust in regulated meat and dairy supply chains supports feed standardization. Cultural preference for meat and seafood sustains demand. Expansion of feed mills and integrated farming enhances distribution efficiency and product accessibility across regions.

Pet food is anticipated to be the fastest-growing segment, driven by rising pet ownership and increasing focus on premium nutrition products. Consumer focus on companion animal care increases spending on enriched formulations. Corn gluten meal supports dietary balance in dry and wet products as a digestible protein source. Ingredient quality awareness influences purchasing decisions, encouraging plant-based inclusion. Expansion of e-commerce and specialty retail improves accessibility. Preventive nutrition trends promote functional, protein-enriched diets, accelerating adoption across premium pet food categories.

Regional Insights

North America Corn Gluten Meal Market Trends

North America demonstrates strong market maturity supported by advanced grain processing infrastructure and high adoption of precision livestock nutrition systems. Large-scale wet milling facilities enable efficient extraction of corn-derived proteins, improving yield optimization and cost control. Integration between corn producers, processors, and feed manufacturers strengthens supply chain coordination and reduces procurement volatility. Regulatory oversight under agencies such as the Food and Drug Administration enforces strict safety and quality standards, reinforcing buyer confidence in consistent feed ingredients across commercial livestock and aquaculture operations.

Sustainability initiatives and bioeconomy strategies influence feed ingredient utilization and processing efficiency across value chains. Policy support for renewable energy and ethanol production increases availability of corn co-products, supporting steady raw material flow for protein extraction. Advanced logistics networks enable efficient distribution across large geographic areas. Strong presence of commercial pet food manufacturing drives application diversification. Trade integration under frameworks such as the United States-Mexico-Canada Agreement supports cross-border commodity movement, improving accessibility and operational scalability.

Europe Corn Gluten Meal Market Trends

Europe demonstrates stable growth driven by regulatory emphasis on sustainable agriculture and reduced reliance on synthetic feed inputs. Feed demand patterns reflect strict quality standards and traceability requirements across livestock and aquaculture systems. Regulatory alignment under frameworks such as the European Food Safety Authority drives rigorous evaluation of feed ingredients, influencing formulation strategies and supplier selection. Corn gluten meal supports consistent nutrient delivery and digestibility within compound feed. High penetration of integrated farming structures enables standardized procurement. Reduced antibiotic usage in animal production increases dependence on balanced nutrition, strengthening demand for reliable plant-based protein inputs.

Sustainability objectives under the European Green Deal influence sourcing strategies and processing efficiency across feed value chains. Environmental targets related to emissions, water usage, and waste management shape operational decisions within corn processing facilities. Preference for plant-based protein inputs aligns with circular economy principles, supporting utilization of corn-derived co-products. Advanced formulation technologies emphasize precision nutrition and improved feed conversion. Strong retail and food service standards increase pressure on livestock producers to maintain consistent quality. Unified regulatory systems support cross-border trade efficiency and stable distribution networks.

Asia Pacific Corn Gluten Meal Market Trends

Asia Pacific is expected to lead with an estimated 34% of the corn gluten meal market share, supported by strong alignment between feed demand intensity and localized corn processing capacity. China drives volume consumption through large-scale poultry and aquaculture operations that require consistent protein inputs. India supports demand through rapid expansion of organized dairy and poultry farming systems. Japan and South Korea maintain stable consumption through advanced feed formulation practices and strict quality standards. Vertical integration across feed mills and livestock producers improves procurement efficiency. Cost-competitive corn availability strengthens processing margins. Export-oriented meat production sustains high utilization of protein-rich feed ingredients across industrial farming networks.

Asia Pacific is forecasted to be the fastest-growing market for corn gluten meal between 2026 and 2033, stimulated by structural transformation in livestock production and rising investment in feed optimization technologies. China accelerates growth through modernization of aquaculture systems and expansion of high-efficiency feed usage. India advances through increasing penetration of compound feed within small and mid-scale farming operations. Japan and South Korea promote premium feed formulations with emphasis on digestibility and nutrient precision. Expansion of cold chain infrastructure supports higher meat consumption. Digital supply chain platforms improve ingredient distribution. Policy focus on feed efficiency encourages adoption of concentrated protein sources.

Competitive Landscape

The global corn gluten meal market competitive environment reflects moderate consolidation, with leading participants such as Archer Daniels Midland, Cargill, and Ingredion controlling a substantial share of global production capacity. These companies leverage vertically integrated supply chains and large-scale wet milling infrastructure to secure raw material flow and maintain cost efficiency. Strategic focus remains on high-volume feed-grade output, supported by long-term procurement contracts with commercial livestock producers.

Corn gluten meal market competitive dynamics include key participants such as Tate & Lyle, Roquette, and Grain Processing Corporation strengthening positioning through process optimization and specialized ingredient portfolios. Regional manufacturers operate within fragmented clusters, particularly across developing production hubs, creating localized competition. Competitive differentiation depends on corn sourcing efficiency, processing yield, and distribution reach, influencing pricing strategies and supply reliability across feed and industrial applications.

Key Developments:

- In January 2026, Riddhi Siddhi Gluco Biols strengthened its position in the corn gluten meal market by acquiring Cargill India’s corn wet milling division, enhancing production capacity for corn-derived co-products including corn gluten used in feed applications.

- In November 2025, Tate & Lyle strengthened the corn gluten meal market by expanding its regenerative agriculture program in France, enhancing sustainable corn sourcing and improving supply chain resilience for corn-derived protein ingredients used in feed applications.

- In March 2025, Cargill strengthened the corn gluten meal market by inaugurating a new corn milling plant in Gwalior, enhancing processing capacity for corn-derived products and supporting consistent supply of protein-rich feed ingredients.

Companies Covered in Corn Gluten Meal Market

- Archer Daniels Midland

- Cargill

- Ingredion

- Tate & Lyle

- Roquette

- Grain Processing Corporation

- Tereos

- Global Bio-chem Technology Group

- COFCO Group

- SunOpta

- Gulshan Polyols

- Sukhjit Starch & Chemicals

- Angel Starch & Food

- Agrana Beteiligungs

Frequently Asked Questions

The corn gluten meal market is projected to reach US$ 3.5 billion in 2026.

Rising demand for high-protein animal feed driven by expanding livestock and aquaculture production fuels the corn gluten meal market.

The corn gluten meal market is poised to witness a CAGR of 4.4% from 2026 to 2033.

Expansion of plant-based protein applications and increasing adoption in premium pet food and specialty feed formulations create key growth opportunities in the corn gluten meal market.

Some of the key market players include Archer Daniels Midland, Cargill, Ingredion, Tate & Lyle, Roquette, and Grain Processing Corporation.