- Chipsets & Processors

- General Purpose Analog IC Market

General Purpose Analog IC Market Size, Share, and Growth Forecast for 2026-2033

General Purpose Analog IC Market by Product Type (Power Management ICs, Linear ICs, Data Converters, Interface ICs, Timing ICs), End-Use Industry (Automotive, Consumer Electronics, Telecommunications, Healthcare), Technology (Analog-Only, Mixed-Signal, Ultra-Low-Power, High-Voltage), and Regional Analysis for 2026-2033

General Purpose Analog IC Market Share and Trends Analysis

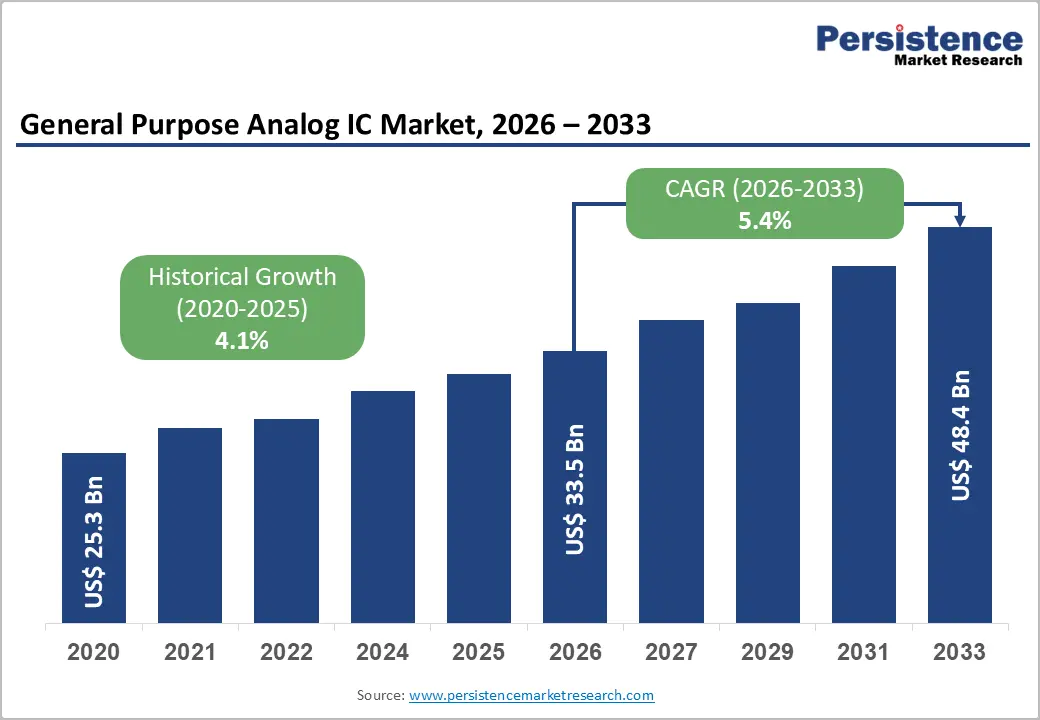

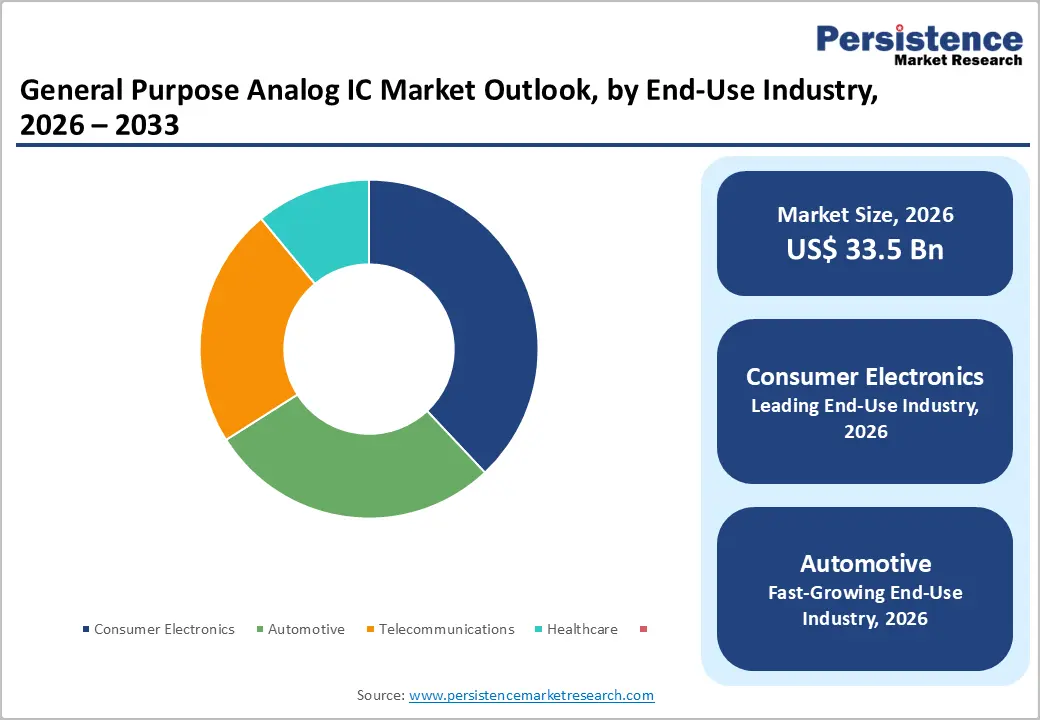

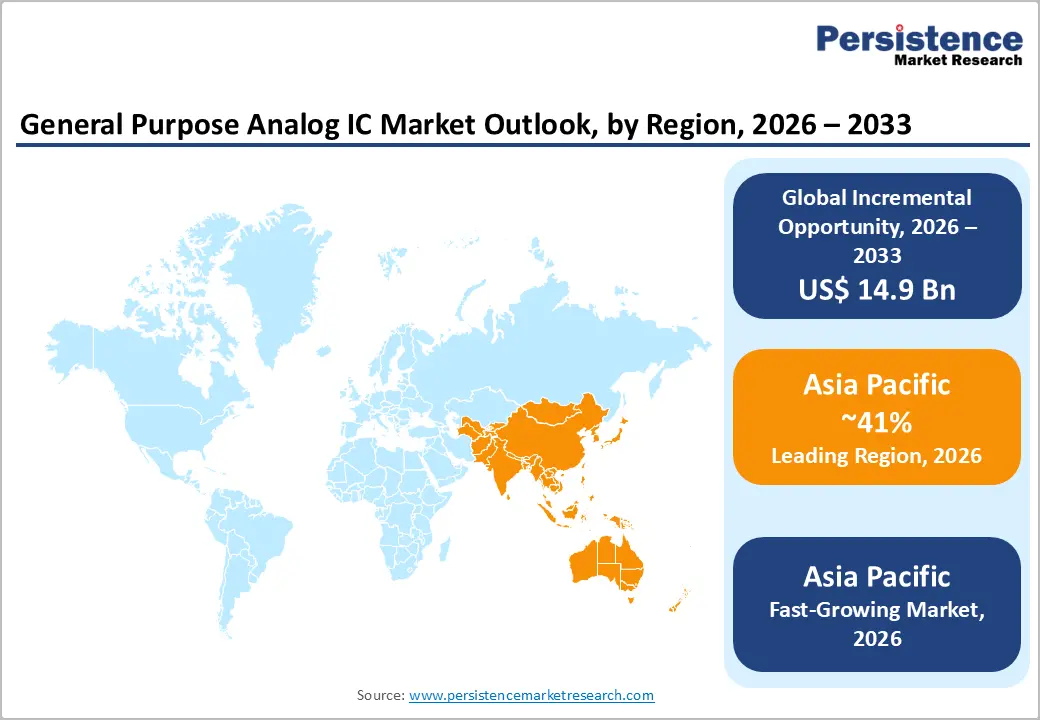

The global general purpose analog IC market size is likely to be valued at US$ 33.5 billion in 2026, and is projected to reach US$ 48.4 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026–2033.

The market demonstrates steady expansion, driven by rising demand across automotive, industrial automation, telecommunications, and consumer electronics sectors. Manufacturers continue to increase semiconductor content per device, particularly in electrified vehicles, smart factory systems, and connected consumer products. The acceleration of automotive electrification, 5G infrastructure rollout, and edge computing deployment strengthens long-term demand for analog semiconductor components. Growing integration of sensors, battery management systems, and real-time monitoring solutions further reinforces adoption of power management integrated circuits (ICs) and signal conditioning technologies. Sustained capital investment in high-reliability electronic systems positions the market for resilient, innovation-led growth across critical infrastructure and advanced electronics applications.

Key Industry Highlights

- Dominant Product Type: Power management ICs are set to command around 35% of the revenue share in 2026, while data converters are likely to grow the fastest through 2033, driven by heightening precision data acquisition needs.

- Leading End-Use Industry: Consumer electronics is projected to hold approximately 38% share in 2026, while automotive is expected to expand at the fastest pace with around 7.4% CAGR through 2033, supported by escalating vehicle electrification.

- Technology Leadership: Analog-only ICs are expected to account for approximately 39% of the revenue share in 2026, reflecting their broad deployment in core signal and power functions.

- Regional Leadership: Asia Pacific is poised to capture about 41% market share in 2026 and register the highest 2026-2033 CAGR of roughly 6.3%, led by electronics manufacturing scale and electric vehicle (EV) production growth.

- Competitive Environment: Major players are focusing on EV-oriented power management IC expansion and 300mm wafer capacity scaling to enhance cost efficiency, supply resilience, and long-term competitiveness.

| Key Insights | Details |

|---|---|

|

General Purpose Analog IC Market Size (2026E) |

US$ 33.5 Bn |

|

Market Value Forecast (2033F) |

US$ 48.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating Automotive Electrification and Strategic Semiconductor Capacity Expansion

Automotive electrification is a primary growth catalyst for the general purpose analog IC market. According to the International Energy Agency (IEA), global electric car sales surpassed 17 million units in 2024, with EVs accounting for nearly 20% of total car sales. Each battery electric vehicle contains significantly higher analog semiconductor content compared to internal combustion vehicles, particularly in power management ICs, battery monitoring systems, and motor control units. Original equipment manufacturers (OEMs) continue to scale EV production capacity to meet emission targets and consumer demand, structurally increasing semiconductor content per vehicle.

Analog ICs perform mission-critical functions including voltage regulation, current sensing, thermal monitoring, and data conversion within EV powertrains. These components ensure battery efficiency, safety compliance, and drivetrain reliability under dynamic operating conditions. In 2025, the Government of India confirmed that three additional semiconductor plants are scheduled to begin commercial operations in 2026, reinforcing domestic chip manufacturing capacity for automotive and electronics applications. Such policy-backed capacity expansion strengthens supply resilience for analog semiconductors and aligns production ecosystems with rising EV-driven demand worldwide.

Industrial Automation Growth and 5G Infrastructure Deployment

The acceleration of Industry 4.0 initiatives is boosting demand for analog IC solutions across industrial and automation sectors. According to the International Federation of Robotics (IFR), global industrial robot installations exceeded 550,000 units annually, reflecting sustained automation investment. Industrial control systems rely heavily on signal conditioning, data converters, and timing ICs for precision measurement and process control. Smart factories increasingly deploy connected sensors, programmable controllers, and motor drives, all of which depend on stable analog front-end architectures.

Simultaneously, 5G infrastructure deployment is increasing demand for high-performance interface ICs and timing ICs. The International Telecommunication Union (ITU) reports rapid expansion of global 5G subscriptions, particularly across Asia Pacific and North America. 5G base stations require precise timing synchronization, efficient power regulation, and strong signal integrity management. Edge computing nodes and telecom equipment integrate advanced analog circuits for signal conditioning and power conversion. As operators continue network densification and governments support digital connectivity expansion, infrastructure-driven demand for analog ICs remains structurally robust.

Semiconductor Supply Chain Volatility, Mature-Node Constraints, and Geopolitical Risks

The analog IC industry remains exposed to supply chain disruptions, particularly in wafer fabrication and specialty analog foundries. Capacity constraints in mature nodes (90nm–180nm), commonly used for analog manufacturing, can limit output. Industry data from global semiconductor associations indicates periodic lead-time extensions during peak demand cycles. These mature nodes are critical because analog devices prioritize long-term stability and electrical performance over extreme miniaturization. As demand fluctuates across automotive, telecom, and industrial markets, production imbalances can quickly emerge, tightening supply availability.

Given that analog ICs often use older process nodes, capacity expansion requires targeted capital investment rather than rapid scaling on advanced digital lines. Foundries must dedicate specialized production capacity, creating structural rigidity during demand surges. In 2025–2026, government discussions in the United States and Europe highlighted vulnerabilities in semiconductor supply chains linked to export controls and critical material sourcing, reinforcing systemic risk awareness. Supply bottlenecks can delay OEM production schedules in automotive and industrial sectors, directly affecting short-term revenue realization and increasing procurement complexity across the value chain.

Pricing Pressure, Cost Inflation, and Competitive Fragmentation

The general purpose analog IC market is moderately fragmented, with several global and regional suppliers competing on cost and reliability. Standardized product categories such as linear ICs and timing ICs face price erosion due to commoditization. Buyers frequently compare functionally equivalent components across multiple vendors, intensifying price-based competition and limiting differentiation in lower-complexity segments. High-volume applications, particularly in consumer electronics, amplify margin sensitivity because procurement teams prioritize cost optimization at scale.

OEMs often pursue multi-sourcing strategies to reduce procurement risks, further increasing pricing pressure on suppliers. While premium automotive-grade analog ICs maintain higher margins due to strict qualification standards, commoditized segments face structural margin compression. Multiple semiconductor manufacturers announced selective price increases in 2025 and early 2026 in response to rising input costs, supply constraints, and inflationary pressures. Major analog IC producers, including Texas Instruments and Infineon, publicly initiated price adjustments on legacy and power related product lines, often ranging from 10% to 30% depending on stock keeping units (SKUs) and applications. These pricing actions reflect broader cost inflation in fabrication and raw materials, while competing firms adjust their strategies to maintain margin performance. This dynamic underscores ongoing profitability challenges and intensifies competitive differentiation pressures in a cost sensitive market environment.

Expansion of EV charging infrastructure and high power analog IC demand

Global investments in EV charging networks are creating substantial growth potential for analog IC vendors. According to the IEA, both public and private sectors are steadily increasing funding for EV charging infrastructure to support rising adoption of electric vehicles. Charging stations rely on robust power management ICs, voltage controllers, and isolation amplifiers to ensure safe, efficient, and reliable high-voltage energy conversion. As governments and corporations expand charging networks across North America, Europe, China, and India, demand for analog front-end components escalates significantly.

In early 2026, the U.S. Department of Energy (DOE) announced a US$ 2.5 billion investment in EV charging infrastructure to accelerate deployment in under-served regions. The initiative includes thousands of new DC fast-charging stations, which require high-reliability analog ICs for power regulation, grid interface, and monitoring. Expansion of high-power, fast-charging infrastructure increases IC content per installation and offers recurring demand for suppliers. Geographic diversification of charging networks further strengthens long-term revenue potential for analog semiconductor providers, supporting sustained market growth.

Modernization of Healthcare Equipment and Precision Analog IC Adoption

Healthcare systems worldwide are increasingly integrating advanced diagnostic imaging, portable monitoring devices, and precision instrumentation, driving demand for high-performance analog components. The World Health Organization (WHO) highlights rising healthcare infrastructure investment globally, supporting modernization of medical equipment across developed and emerging markets. Medical devices depend on high-accuracy data converters, low-noise linear ICs, and precision signal conditioning circuits to ensure diagnostic reliability and operational safety. Aging populations in developed countries further boost demand for sophisticated monitoring and treatment systems.

Several national health ministries announced technology enhancement programs for healthcare infrastructure. For example, the Government of Japan approved a major healthcare digitization initiative funding upgrades to imaging equipment and remote patient monitoring in rural hospitals. These programs emphasize adoption of next-generation diagnostic platforms that integrate advanced analog front ends. Procurement of precision analog components is expected to increase, particularly in regulated, high-margin medical applications. Broader healthcare digitization also creates opportunities for analog IC suppliers in connected health ecosystems and telemedical instrumentation.

Category-wise Analysis

Product Type Insights

Power management ICs are projected to hold approximately 35% of the revenue share in 2026, driven by widespread adoption across automotive powertrains, telecom infrastructure, industrial systems, and consumer electronics. They provide essential functions such as voltage regulation, energy conversion, and thermal efficiency, supporting modern electronic designs. Electrification of vehicles and the rapid expansion of data centers and communication networks further boost demand for high-efficiency solutions.

In 2025–2026, onsemi partnered with GlobalFoundries to develop next-generation GaN power devices, including optimized DC-DC converters and onboard chargers for EVs and renewable energy applications. Customer sampling is expected in 2026, expanding analog power device content through advanced packaging and higher efficiency architectures. This collaboration exemplifies the segment’s strategic growth potential and long-term market relevance.

Data converters are expected to grow at a 6.8% CAGR through 2033, driven by increasing demand for high-precision ADCs and DACs in industrial automation, healthcare imaging, IoT devices, and robotics. They enable accurate analog-to-digital and digital-to-analog conversion critical for real-time monitoring, sensor interfacing, and control systems.

Expanding smart factories and connected device networks require low-latency, high-performance data conversion. The advanced driver assistance systems (ADAS) and industrial control platforms integrated more sophisticated sensor arrays dependent on high-accuracy data converters, highlighting their growing strategic importance. This positions the segment as a high-growth, revenue-expanding area for analog IC suppliers.

End-Use Industry Insights

Consumer Electronics

Consumer Electronics is anticipated to hold approximately 38% of the general purpose analog IC market revenue share in 2026, supported by smartphones, tablets, wearables, PCs, and smart home devices. Analog ICs in these products manage power, signal processing, connectivity, and sensor integration, ensuring reliable and energy-efficient operation. Ongoing innovation, miniaturization, and high-volume production sustain structural market leadership. In 2025–2026, regional manufacturing expansions in electronics hubs such as Vietnam, Thailand, and India increased local device output, further boosting analog IC demand and reinforcing consumer electronics as a core volume driver.

Automotive is expected to expand at nearly 7.4% CAGR through 2033, fueled by electrification, ADAS, and increased in-vehicle semiconductor content. Analog ICs are critical for battery management, motor control, power conversion, safety systems, and infotainment. In 2025–2026, Renesas Electronics introduced automotive-grade SoCs for ADAS and cockpit domain control, while Rohm Semiconductor launched SiC MOSFET modules for EV traction inverters, supporting high-efficiency powertrains. These innovations highlight rising analog IC content per vehicle, making automotive the fastest-growing end-use segment with long-term strategic potential.

Regional Insights

North America General Purpose Analog IC Market Trends

North America is a major contributor to the global general purpose analog IC market, led by the United States, which benefits from a robust innovation ecosystem and concentrated semiconductor R&D. The region’s analog IC demand is driven by EV manufacturing, 5G infrastructure deployment, advanced industrial systems, and defense electronics. Federal initiatives to strengthen domestic semiconductor fabrication and supply chain resilience further reinforce North America’s competitive position.

Leading analog IC vendors headquartered in the U.S. maintain technological leadership in automotive-grade, mixed-signal, and power management solutions, contributing to sustained regional relevance. North American OEMs increasingly integrate analog ICs into EV powertrains, industrial automation equipment, and telecom hardware, driving consistent adoption. The region also attracts investment in advanced packaging, wafer fabrication, and analog IC design hubs.

The U.S. Department of Commerce expanded support for semiconductor manufacturing through enhanced grant allocations and tax incentives, accelerating domestic analog IC and power device capacity. These measures support new fabrication facilities and the integration of advanced production lines for high-reliability components, reducing dependence on external suppliers. Combined with increasing adoption of analog ICs in automotive, industrial automation, and telecom applications, North America is positioned for stable growth and innovation-led leadership.

Public-private collaborations, R&D tax credits, and defense-driven electronics projects further strengthen the ecosystem. The region is expected to maintain healthy growth, driven by consistent technology upgrades and strategic investments in mixed-signal and power management technologies.

Europe General Purpose Analog IC Market Trends

Europe is a formidable entity in the automotive, industrial automation, and telecom sectors, with Germany leading the regional demand due to its automotive OEM base and advanced manufacturing ecosystem. The U.K., France, and Spain contribute through investments in industrial robotics, renewable energy integration, and telecom infrastructure upgrades. European Union (EU) regulatory harmonization ensures quality standards, supply chain transparency, and compliance, supporting reliable analog IC deployment across industries.

Electrification policies and emission targets accelerate automotive-related analog IC adoption, particularly for power management ICs and data converters. Industrial automation expansion and renewable energy initiatives also stimulate demand for mixed-signal and high-precision analog devices. European OEMs increasingly adopt energy-efficient analog solutions, enhancing product reliability and performance.

The European Commission (EC) approved additional funding under the EU Chips Act to strengthen semiconductor design and manufacturing, including analog and mixed-signal technologies. This initiative supports supply chain resilience and attracts long-term investment in advanced IC production. Coupled with rising EV adoption, industrial digitalization, and renewable energy deployment, Europe is expected to grow steadily. Specialized European analog IC firms focusing on automotive-grade solutions complement global market leaders, creating a competitive and innovation-driven landscape. Expansion of industrial robotics, smart factories, and energy-efficient consumer electronics ensures ongoing analog IC demand, while regulatory alignment fosters market stability.

Asia Pacific General Purpose Analog IC Market Trends

Asia Pacific is projected to be the largest and fastest-growing market for general purpose analog ICs, accounting for an estimated 41% value share in 2026, with a projected CAGR of 6.3% through 2033. China dominates with large-scale EV production, consumer electronics assembly, and telecom infrastructure deployment, driving substantial analog IC consumption. Japan contributes through high-end automotive, industrial automation, and robotics applications, while South Korea and Taiwan continue to advance semiconductor fabrication and packaging capabilities.

India and ASEAN are rapidly expanding domestic electronics manufacturing, generating incremental demand and reducing reliance on single-country supply chains. Regional cost advantages, government incentives, and integrated supply chains reinforce leadership. Growth in smart factories, EV adoption, and telecom densification continues to propel analog IC requirements.

In 2025, the Government of India expanded its production-linked incentive (PLI) program to attract semiconductor and analog IC manufacturing investments. This policy is already driving interest from global firms evaluating new fabrication and assembly capacities.

Combined with robust EV, industrial, and consumer electronics growth in China, India, and Southeast Asia, the region strengthens its position as a strategic growth hub. Investment in wafer fabrication, IC design, and packaging facilities continues, further supporting market expansion. Suppliers targeting automotive, industrial automation, and high-volume consumer electronics segments benefit from increasing demand, making Asia Pacific a critical region for long-term analog IC growth.

Competitive Landscape

The global general purpose analog IC market structure is moderately consolidated, with leading players including Texas Instruments, Analog Devices, STMicroelectronics, Infineon Technologies, and NXP Semiconductors collectively controlling a significant portion of global revenue. These established companies leverage deep industry relationships, extensive IP portfolios, and integrated design-to-manufacturing capabilities. Heavy investment in R&D enables leadership in high-performance, automotive-grade, and mixed-signal analog ICs, supporting advancements in power management, data conversion, and signal conditioning.

Regional and specialized players such as Rohm Semiconductor, Maxim Integrated, ON Semiconductor, and Renesas Electronics focus on niche segments or geographic strongholds, including EV powertrain solutions, industrial automation, and consumer electronics. Barriers such as high-capital fabrication requirements, process complexity, and stringent automotive and industrial qualification standards limit new entrants. However, software-enabled design tools, simulation platforms, and foundry collaborations allow emerging players to participate via IC design or analog IP licensing. Market consolidation is expected to continue gradually, driven by strategic acquisitions, capacity expansions, and technology partnerships aimed at broadening geographic reach and advancing mixed-signal and ultra-low-power capabilities.

Key Industry Developments

- In February 2026, Texas Instruments announced the acquisition of Silicon Labs, expanding its analog and wireless IC capabilities in industrial and consumer markets. This strategic move strengthens TI’s portfolio in power management, sensor integration, and mixed-signal solutions, positioning the company to capture growing demand across automotive, industrial, and IoT applications.

- In February 2026, Infineon increased its investment to €2.7billion to advance AI, power management, and analog semiconductor solutions. The acquisition of AMS Osram’s non-optical analog and mixed-signal sensor operations enhances Infineon’s product portfolio and supports high-efficiency, automotive-grade, and industrial applications.

- In February 2026, the Government of India launched India Semiconductor Mission 2.0 with a 1.25 lakh crore budget to boost domestic chip design and manufacturing. This initiative promotes local analog and mixed-signal IC development, strengthens supply chain resilience, and attracts global semiconductor investments into the Indian market.

Companies Covered in General Purpose Analog IC Market

- Texas Instruments

- Analog Devices

- Infineon Technologies

- STMicroelectronics

- NXP Semiconductors

- ON Semiconductor

- Renesas Electronics

- Microchip Technology

- Maxim Integrated

- Skyworks Solutions

- ROHM Semiconductor

- Vishay Intertechnology

Frequently Asked Questions

The global general purpose analog IC market is projected to reach US$ 33.5 billion in 2026.

Market growth is fueled by automotive electrification, industrial digitization, and 5G infrastructure deployment.

The market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Expansion of EV charging infrastructure and healthcare equipment modernization are prime market opportunities.

Texas Instruments, Analog Devices, STMicroelectronics, Infineon Technologies, and NXP Semiconductors are some of the leading players in the market.