- Semiconductor Materials & Components

- Frame Grabber Market

Frame Grabber Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Frame Grabber Market by Application (Web Inspection, Transportation Safety & Maintenance, Scientific & Medical Imaging, Factory Automation, Industrial Camera Systems, Security & Surveillance), End-user (OEMs, Manufacturers, System Integrators), and Region Analysis for 2026 to 2033

Frame Grabber Market Trends & Analysis

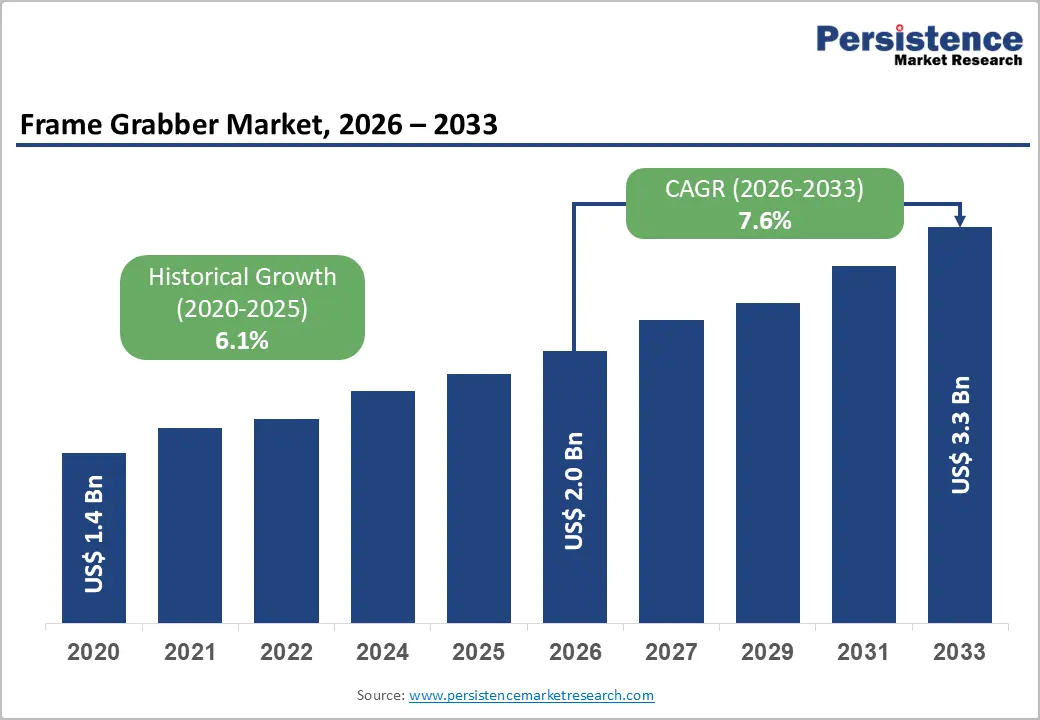

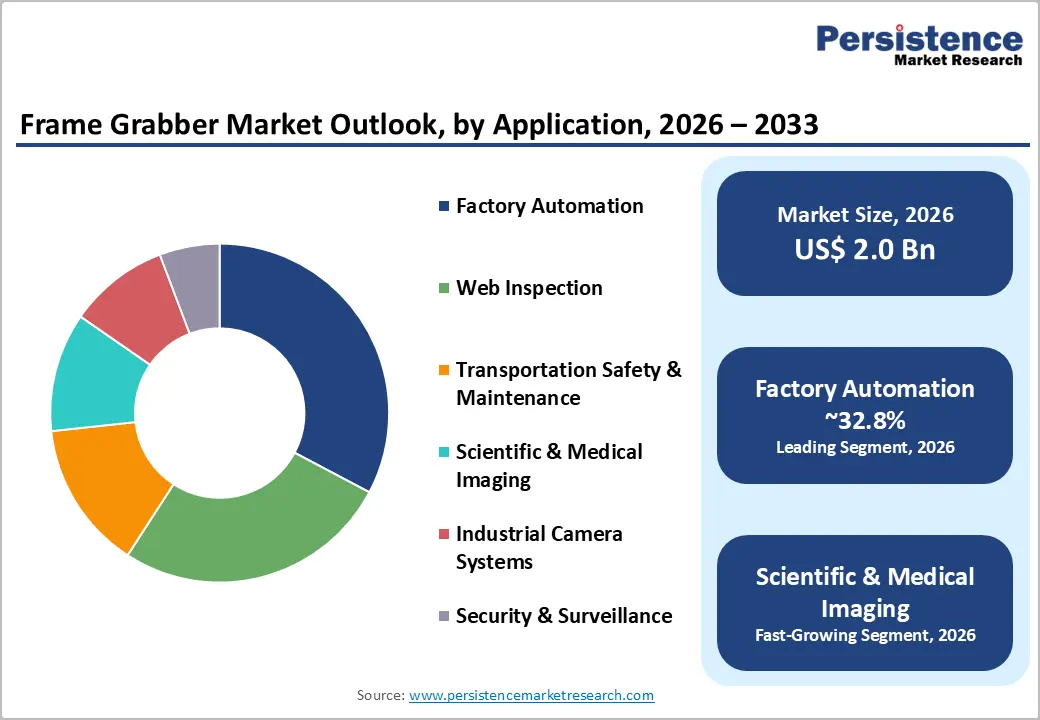

The global frame grabber market size is projected at US$ 2.0 billion in 2026 and is projected to reach US$ 3.3 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

Industrial automation investments surpassed US$ 280 Bn globally in 2024; AI-integrated machine vision deployments grew 34% YoY; CoaXPress 3.0 and Camera Link HS interface adoption expanded factory inspection throughput 2.4x, accelerating high-speed frame grabber procurement across semiconductor, automotive, and pharmaceutical manufacturing programs through 2033.

Factory automation proliferation, AI machine vision integration, and high-bandwidth camera interface standardization across industrial quality inspection programs are primary structural growth drivers. Rising demand for high-speed, high-resolution image acquisition in pharmaceutical, semiconductor, and transportation safety applications, combined with the historical 6.1% CAGR from 2020 to 2026, confirms sustained frame grabber technology adoption momentum globally.

Key Industry Highlights:

- Leading Application: Factory Automation leads and grows fastest at 32.8% share (US$ 646 Mn) and 8.6% CAGR, driven by CHIPS Act semiconductor inspection, EV battery inline quality control, and AI machine vision robot assembly line deployments globally.

- Leading End Use: OEMs lead at 38.2% share (US$ 753 Mn); System Integrators grow fastest at 8.4% CAGR, driven by CoaXPress-integrated custom AI vision inspection, robotic surgery imaging, and ITS transportation camera network system integration programs globally.

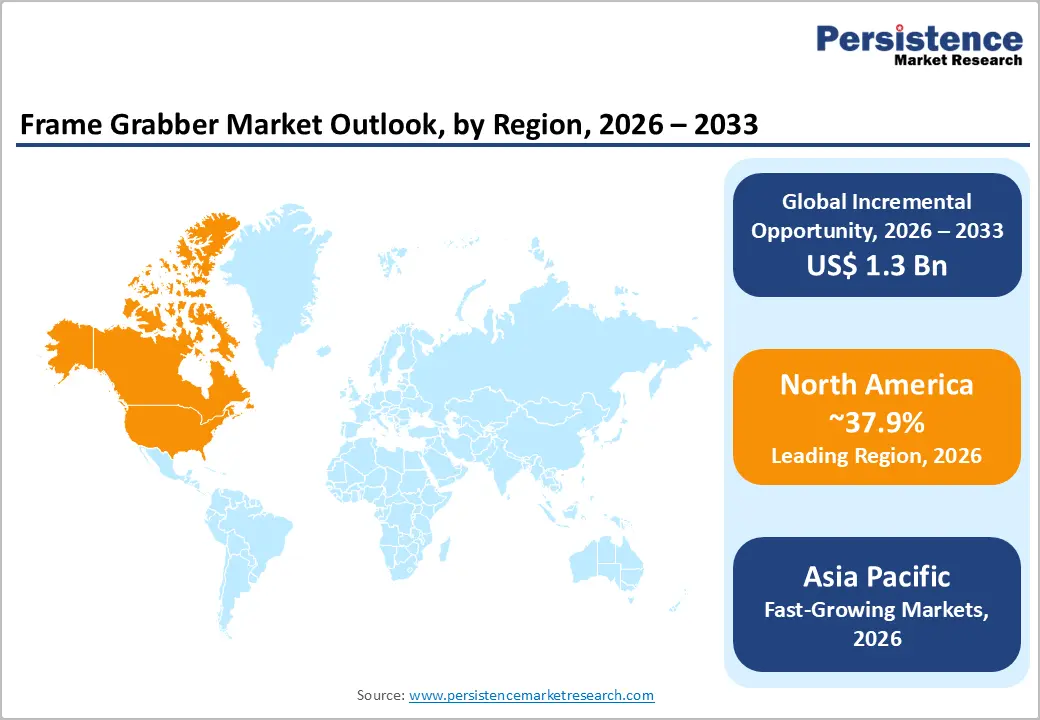

- Regional Leader: North America holds 37.9% share (U.S. US$ 473.1 Mn); Asia Pacific grows fastest at 8.5% CAGR with China at US$ 201.7 Mn and India at US$ 57.7 Mn, anchored by semiconductor fab and EV battery inspection expansion.

- Strategic Milestone: Euresys' Coaxlink Quad CXP-12 Gen2 launch (February 2025) delivering 4×12.5 Gb/s CoaXPress 3.0 channels and Teledyne DALSA's FPGA AI inference frame grabber (September 2024) reducing inspection latency 40% signal embedded AI co-processing as the defining frame grabber technology evolution through 2033.

Market Dynamics Analysis

Drivers - Industrial Automation and AI-Powered Machine Vision Proliferation Driving Frame Grabber Structural Demand

Global industrial automation investment exceeded US$ 280 Bn in 2024 (IFR World Robotics Report), with machine vision system deployments, which universally require frame grabbers for analog/digital camera signal acquisition and real-time image processing pipeline management, growing at 34% YoY in AI-integrated configurations across semiconductor wafer inspection, PCB defect detection, and automotive body panel quality control applications.

IFR data confirms global industrial robot installations reached 541,302 units in 2023, each collaborative robot and vision-guided assembly cell generating dedicated frame grabber procurement requirements for industrial camera interface card acquisition across PCIe, USB 3.0, and CoaXPress hardware platforms.

The global machine vision market, valued at US$ 15.6 Bn in 2024 at 7.4% CAGR (AIA Machine Vision Industry Report), represents the primary structural demand generator for frame grabber hardware and software platform procurement globally. Frame grabbers serve as the hardware bridge between industrial camera sensors generating 10-100 Gb/s pixel data streams and host processing environments, with CoaXPress 3.0 and Camera Link HS-compatible frame grabber cards from Euresys, ADLINK, and Teledyne DALSA enabling the ultra-low-latency acquisition pipelines that 100+ megapixel line-scan camera-based web and PCB inspection systems demand at production throughput speeds.

Transportation Safety Infrastructure Modernization and Intelligent Transportation System Expansion

Global intelligent transportation system (ITS) infrastructure investment reached US$ 36.8 Bn in 2024 (ITS America Annual Market Report), with railway safety inspection systems, traffic management AI cameras, and automated license plate recognition (ALPR) networks each requiring frame grabbers for deterministic multi-camera video acquisition at 25-120 fps with sub-millisecond latency performance guarantees unachievable through software-only USB or Ethernet acquisition frameworks.

U.S. IIJA allocated US$ 108.4 Bn for transportation infrastructure modernization, with ITS digital systems integration specifying frame grabber-equipped multi-channel video acquisition platforms at highway monitoring, tunnel safety inspection, and railway bridge structural monitoring installations.

European Commission TEN-T network digitalization programs, committing €26.7 Bn through 2030 to railway and road infrastructure ITS upgrades, are generating continuous multi-camera frame grabber procurement at transportation safety OEM, system integrator, and national infrastructure authority procurement levels across Germany, France, Netherlands, and Spain transportation networks. Frame grabbers' hardware-triggered multi-camera synchronization capability, achieving ±50 ns inter-camera timing precision across 8-16 simultaneous camera inputs, is technically mandatory for railway bogie underframe inspection, bridge structural monitoring, and highway incident detection systems where frame timing accuracy directly impacts defect detection reliability.

Restraints - Camera Interface Standard Fragmentation Constraining Cross-Platform Frame Grabber Compatibility

The frame grabber hardware market spans seven major camera interface standards, Camera Link, CoaXPress, GigE Vision, USB3 Vision, Camera Link HS, CLHS, and SDI, with each requiring distinct FPGA configuration, driver architecture, and PCIe bandwidth allocation. System integrators deploying multi-vendor camera configurations across machine vision inspection lines face 12-18-week hardware qualification cycles per new camera-frame grabber combination, with incompatibility discovery post-procurement creating system integration delays that constrain frame grabber adoption velocity at smaller OEM and system integrator procurement programs globally.

GPU-Accelerated Frameless Vision Processing Platforms Competing with Dedicated Frame Grabber Hardware

NVIDIA Jetson and Intel OpenVINO GPU-accelerated embedded vision processing platforms, enabling direct USB3 and GigE Vision camera acquisition without dedicated PCIe frame grabber cards, are displacing traditional frame grabber hardware in low-to-medium speed industrial inspection applications below 500 fps camera throughput requirements. Industry estimates indicate GPU-native acquisition platforms captured 22-28% of applications historically served by entry-level frame grabbers between 2021 and 2024, creating structural volume constraint pressure on frame grabber unit growth rates at lower-specification machine vision application tiers globally.

Opportunities - Semiconductor and Electronics Manufacturing Quality Inspection Expansion Driving High-Performance Frame Grabber Demand

Global semiconductor capital expenditure reached US$ 193 Bn in 2024 (SEMI, World Fab Watch), with advanced wafer-level inspection systems for 3nm and below logic chip manufacturing requiring CoaXPress 3.0 and Camera Link HS frame grabbers capable of sustaining 12.5 Gb/s per channel sustained pixel throughput for defect detection at sub-10 nm feature resolution across 300 mm wafer surfaces at production-rate inspection speeds.

Each new semiconductor front-end manufacturing facility of the scale of Intel's Arizona Fab 21 or TSMC's Phoenix campus incorporates 200-500 frame grabber-equipped inspection and metrology stations per production line, generating multi-million-dollar per-facility frame grabber procurement programs at new fab construction and tool installation phases.

The global semiconductor inspection and metrology equipment market, valued at US$ 7.4 Bn in 2024 at 9.8% CAGR, establishes the sustained capital procurement framework for high-performance frame grabber adoption across CHIPS Act-funded U.S. and EU Chips Act-funded European semiconductor manufacturing investments through 2033. Euresys Coaxlink Quad G3 and ADLINK PCIe-FG series targeting semiconductor inspection OEMs represent established commercial design-win pathways for premium-tier CoaXPress frame grabbers in this highest-margin application segment.

Medical and Scientific Imaging Expansion Across Genomics, Pathology, and Surgical Robotic Systems

The global digital pathology market, valued at US$ 1.2 Bn in 2024 at 11.7% CAGR (GBI Research Medical Imaging Tracker), is expanding whole-slide imaging (WSI) scanner deployments that require high-speed line-scan camera frame grabbers capable of sustained 4 Gb/s pixel acquisition across 40x magnification multi-spectral fluorescence microscopy channels. Intuitive Surgical's da Vinci robotic surgical systems and emerging single-port robotic platforms incorporate multiple 4K surgical camera channels requiring latency-deterministic frame grabber acquisition maintaining <5 ms end-to-end imaging pipeline latency for surgically safe real-time stereoscopic visualization at operating theater deployment conditions.

The broader scientific and medical imaging addressable market for frame grabbers, encompassing flow cytometry, high-content screening, digital pathology, and robotic surgery imaging, is estimated at US$ 320-380 Mn by 2030 within the total frame grabber market, representing a structurally premium-priced, specification-driven procurement segment that drives average selling price uplift for medical-grade frame grabber OEM products in the forecast period.

Category-wise Analysis

Application Insights

Factory Automation leads the application segment with a 32.8% market share in 2026, estimated at approximately US$ 646 Mn, anchored by machine vision quality inspection systems at semiconductor, automotive, PCB assembly, pharmaceutical packaging, and food processing manufacturing lines where deterministic, high-throughput frame acquisition is a non-negotiable production system performance specification. The dominance reflects the segment's consistent annual capital investment cycle, with greenfield manufacturing facility construction and brownfield inspection system upgrade programs generating recurring frame grabber procurement demand across all global industrial manufacturing geographies.

Other applications including transportation safety and medical imaging are growing, but factory automation's installed base scale and annual capital reinvestment cycle sustains its application segment leadership through 2033 without displacement risk.

Factory Automation is also the fast-growing application. Semiconductor CHIPS Act-funded fab construction, EV battery cell inspection line deployment, and AI-integrated vision-guided robot assembly line adoption, each requiring ultra-high-speed frame grabbers, collectively sustain factory automation's position as both the leading and fastest-growing application segment through 2033 globally.

End-user Insights

OEMs lead the end-use segment with a 38.2% market share in 2026, estimated at approximately US$ 753 Mn, reflecting the segment's dominant procurement role as machine vision system, industrial camera, and inspection equipment manufacturers integrate frame grabbers as core bill-of-materials components within their turnkey vision system product lines sold to end-user manufacturers globally. OEM procurement's volume advantage, driven by multi-year production contracts with frame grabber suppliers, sustains revenue leadership over manufacturer and system integrator end-use segments.

Manufacturers represent direct end-user procurement, while system integrators build application-specific vision systems, but OEMs' standardized, volume-based procurement model maintains end-use segment dominance through 2033 across all frame grabber interface standards and performance tiers.

System Integrators are the fastest-growing end-use segment at 8.4% CAGR by 2033. Application-specific machine vision system integration demand, driven by AI-powered defect detection, surgical robotic imaging, and smart transportation camera network deployments, is expanding system integrator frame grabber procurement as custom vision solution programs requiring specialized CoaXPress, Camera Link, and embedded frame grabber configurations accelerate globally through 2033.

Regional Market Insights

North America Frame Grabber Market Trends

North America leads with a 37.9% share of the global frame grabber market in 2026, estimated at approximately US$ 747 Mn, anchored by Teledyne DALSA, Matrox Imaging, and Cognex machine vision ecosystem leadership, CHIPS Act-funded semiconductor inspection facility investments, and IIJA transportation safety infrastructure digitalization programs generating structured frame grabber procurement across U.S. and Canadian industrial and transportation application verticals.

U.S. Frame Grabber Market: CHIPS Act Inspection Systems, ITS Infrastructure, and Machine Vision Innovation Leadership

The United States holds approximately US$ 473.1 Mn in 2026, driven by US$ 52.7 Bn in CHIPS Act direct semiconductor manufacturing subsidies, generating new fab inspection station frame grabber procurement at Intel Arizona, TSMC Phoenix, and Samsung Taylor facilities. NI (National Instruments) PCIe frame grabber systems, Teledyne DALSA Xcelera platforms, and Matrox Radient series anchor U.S. machine vision OEM supply. Canada contributes through Matrox Imaging Montreal-based global CoaXPress and Camera Link frame grabber R&D and manufacturing operations.

North America's growth is reinforced by CHIPS Act semiconductor inspection capital investment, IIJA transportation safety ITS multi-camera system deployments, and AI machine vision factory automation upgrade programs across the U.S. semiconductor, automotive, and pharmaceutical manufacturing facility procurement cycles through 2033.

Europe Bubble Diffuser Market Trends

Europe is likely to reach a prominent 7.1% CAGR by 2033, holding approximately 26.4% of global Frame Grabber Market share in 2026, estimated at approximately US$ 521 Mn, driven by German automotive and industrial machinery manufacturing machine vision adoption, EU Chips Act-funded semiconductor inspection investments, and Euresys Belgian-headquartered CoaXPress frame grabber platform global leadership from European industrial vision ecosystem strength.

Germany Frame Grabber Market: Automotive Inspection Leadership and EU Chips Act Investment

Germany holds approximately US$ 262.3 Mn in 2026, anchored by Basler AG camera-Euresys frame grabber integration partnerships across BMW, Mercedes-Benz, and Volkswagen assembly line vision inspection programs. The U.K. sustains Active Silicon and Silicon Software frame grabber deployments in pharmaceutical packaging and railway maintenance inspection systems.

France contributes through Thales ITS transportation surveillance and Airbus aerospace structural inspection vision system procurement. Spain expands through SEAT automotive and ITS traffic management camera system integrations. EU Chips Act €8.1 Bn semiconductor facility investment is expanding European inspection station frame grabber demand.

Europe's EU Chips Act semiconductor inspection investment, German automotive machine vision leadership, and ITS railway and highway safety modernization programs sustain structured premium-tier frame grabber procurement across European industrial and transportation manufacturing supply chains.

Asia Pacific Bubble Diffuser Market Trends

Asia Pacific is the fast-growing market commanding approximately 28.6% of global share in 2025, driven by China's semiconductor and EV battery manufacturing inspection expansion, Japan's precision industrial camera and machine vision OEM leadership, and India's PLI-funded electronics manufacturing capacity generating new frame grabber procurement demand across the region.

China & India Frame Grabber Market: Semiconductor Inspection Scale, EV Battery Quality Control, and Electronics Manufacturing

China holds US$ 201.7 Mn in 2026, driven by SMIC, CXMT, and YMTC semiconductor facility inspection system procurement, CATL and BYD EV battery cell inline inspection line deployments, and domestic industrial camera OEM adoption of ADLINK and KAYA Instruments frame grabber platforms. India at US$ 57.7 Mn expands through PLI electronics manufacturing inspection programs at Tata Electronics and Foxconn India facilities. Japan sustains Sony Semiconductor, Basler-Japan, and Hitachi Kokusai machine vision-integrated frame grabber leadership across precision industrial inspection programs.

Asia Pacific's China semiconductor and EV battery inspection procurement expansion, Japan precision machine vision OEM leadership, and India PLI electronics manufacturing inspection investment collectively sustain the region's accelerating frame grabber market growth trajectory through 2033.

Competitive Landscape

The global frame grabber market is moderately consolidated, with Teledyne DALSA, Euresys, Matrox Imaging, ADLINK Technology, and National Instruments (NI) collectively holding approximately 55-60% of global revenue share, while mid-tier players including IMPERX, Pleora, and BitFlow serve specialized application niches. Proprietary FPGA firmware, multi-standard camera interface support breadth, and SDK software ecosystem depth are the primary competitive moat structures.

CoaXPress 3.0 and Camera Link HS interface innovation leadership, AI vision processing co-design partnerships with OEM machine vision customers, Asia Pacific semiconductor inspection market expansion, and embedded frame grabber platform miniaturization define the dominant competitive strategic themes across all major Frame Grabber market participants through 2033.

Strategic Developments

- In November 2024, Silicon Software GmbH launched the microEnable 5 marathon ACX QP frame grabber, supporting simultaneous four-port CoaXPress 2.0 acquisition with integrated preprocessing FPGA pipeline, targeting automotive body panel paint defect inspection systems requiring real-time multi-camera synchronized acquisition at 2048-pixel line scan resolution at 200 kHz line rates.

- In January 2024, Matrox Imaging expanded its Radient eV-CXP4 frame grabber platform to include Matrox Design Assistant AI vision development environment integration, enabling system integrators to deploy deep-learning-based inspection applications on Matrox frame grabber hardware without separate AI inference accelerator cards, targeting pharmaceutical packaging and food quality inspection OEM design programs.

Frame Grabber Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.4 Bn |

| Current Market Value (2026) | US$ 2.0 Bn |

| Projected Market Value (2033) | US$ 3.3 Bn |

| CAGR (2026 - 2033) | 7.6% |

| Leading Region | North America |

| Dominant Application | Factory Automation - 32.8% |

| Top-ranking End Use | OEMs - 38.2% |

| Incremental Opportunity | US$ 1.3 Bn |

Companies Covered in Frame Grabber Market

- Teledyne DALSA Inc.

- Euresys S.A.

- Matrox Imaging (Matrox Electronic Systems)

- ADLINK Technology Inc.

- National Instruments (NI) / Emerson

- Cognex Corporation

- Silicon Software GmbH

- IMPERX Inc.

- BitFlow Inc.

- Pleora Technologies Inc.

- KAYA Instruments Ltd.

- Active Silicon Ltd.

- Advantech Co., Ltd.

- IDS Imaging Development Systems GmbH

- Basler AG

Frequently Asked Questions

The frame grabber market is valued at US$ 2.0 Bn in 2026, projected to reach US$ 3.3 Bn by 2033, delivering an incremental opportunity of US$ 1.3 Bn through 2033.

AI-integrated machine vision proliferation in semiconductor and EV manufacturing, ITS transportation safety infrastructure digitalization, and CoaXPress 3.0 camera interface adoption enabling ultra-high-speed multi-camera industrial inspection system deployments are the primary growth drivers.

The frame grabber market grows at a CAGR of 7.6% from 2026 to 2033, building on a historical CAGR of 6.1% from 2020 to 2026.

CHIPS Act and EU Chips Act-funded semiconductor fab inspection station deployment and digital pathology whole-slide imaging and surgical robotic 4K multi-channel frame acquisition represent the highest-value addressable growth opportunity pools through 2033.

Teledyne DALSA, Euresys, Matrox Imaging, ADLINK, NI (Emerson), Cognex, Silicon Software, IMPERX, BitFlow, Pleora, KAYA Instruments, Active Silicon, Advantech, IDS Imaging, and Basler AG are the leading global participants.