- Beauty & Personal Care

- Fragrance Market

Fragrance Market Size, Share and Growth Forecast, 2026 - 2033

Fragrance Market by Product Type (Fine Fragrances, Deodorants & Antiperspirants, Body Mists, Perfume Oils, Roll-on), Application (Personal Fragrance, Home Fragrance, Car Fragrance, Ambient Scenting), Fragrance Family (Floral, Woody, Amber, Fresh, Gourmand, Fruity, Spicy), and Regional Analysis for 2026 - 2033

Fragrance Market Share and Trends Analysis

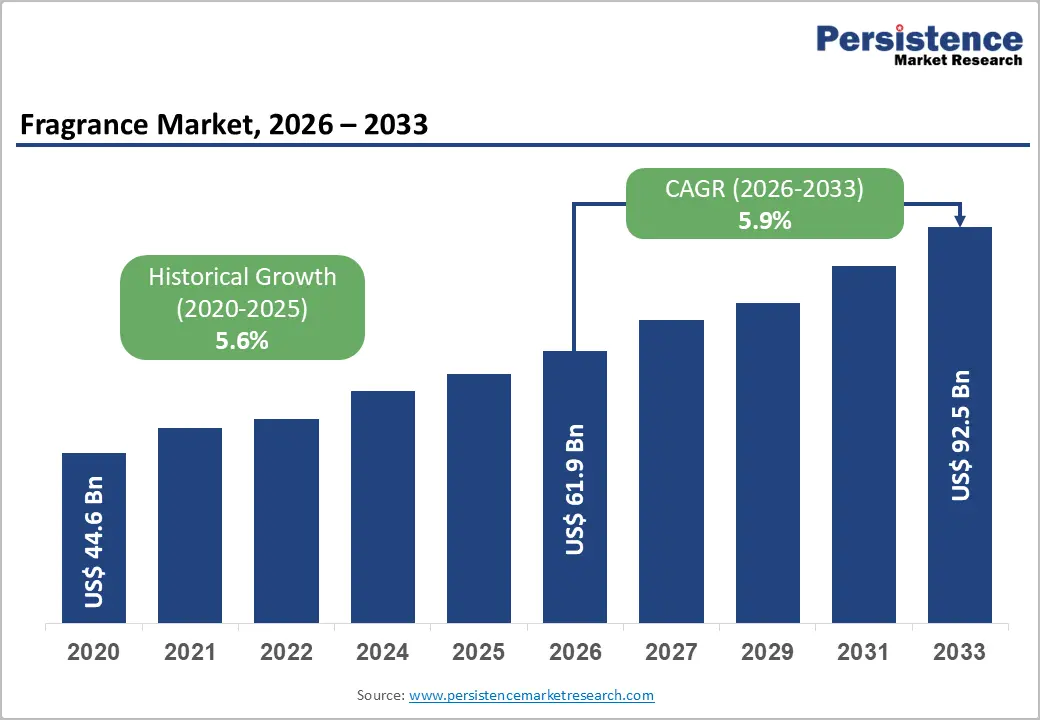

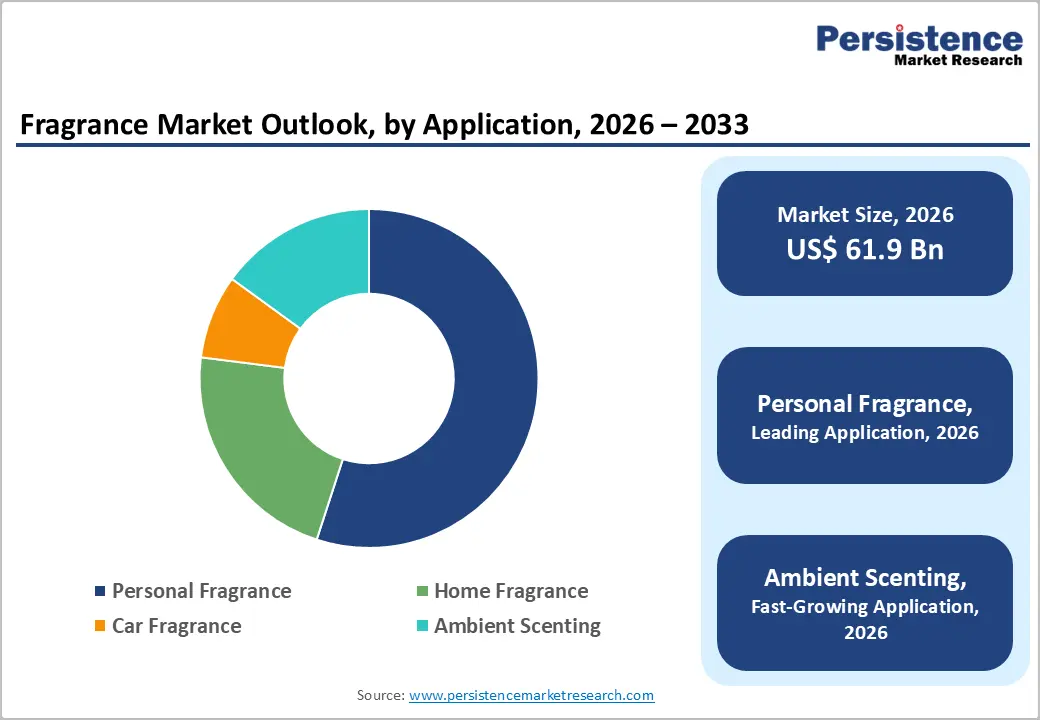

The global fragrance market size is likely to be valued at US$ 61.9 billion in 2026 and is projected to reach US$ 92.5 billion by 2033, growing at a CAGR of 5.9% during the forecast period 2026-2033. The fragrance market growth is driven by evolving consumer preferences toward premium, personalized, and sustainable fragrance products, reflecting a shift from basic hygiene to lifestyle-oriented consumption.

Functional benefits such as long-lasting scent profiles, mood enhancement, and identity expression are increasing product adoption. Expansion of end-use applications, including home fragrance, car fragrance, and ambient scenting, is broadening demand beyond personal use. Additionally, rapid urbanization and rising disposable incomes in emerging markets across Asia-Pacific and Latin America are increasing per capita spending on personal care and grooming products, creating a strong, sustained demand base for fragrance manufacturers.

Key Industry Highlights

- Dominant Product Type: Deodorants & antiperspirants are set to command around 42% of the revenue share in 2026, while fine fragrances are likely to be the fastest-growing segment through 2033, driven by premiumization and increasing demand for luxury scent profiles.

- Leading Application Segment: Personal fragrance is expected to dominate with approximately 55% share in 2026, while ambient scenting is projected to be the fastest-growing segment during 2026–2033, supported by rising adoption in commercial environments.

- Dominant Fragrance Family: Floral fragrances are anticipated to hold nearly 30% share in 2026, while gourmand fragrances are likely to expand at the fastest pace through 2033, fueled by demand for indulgent and unique scent experiences.

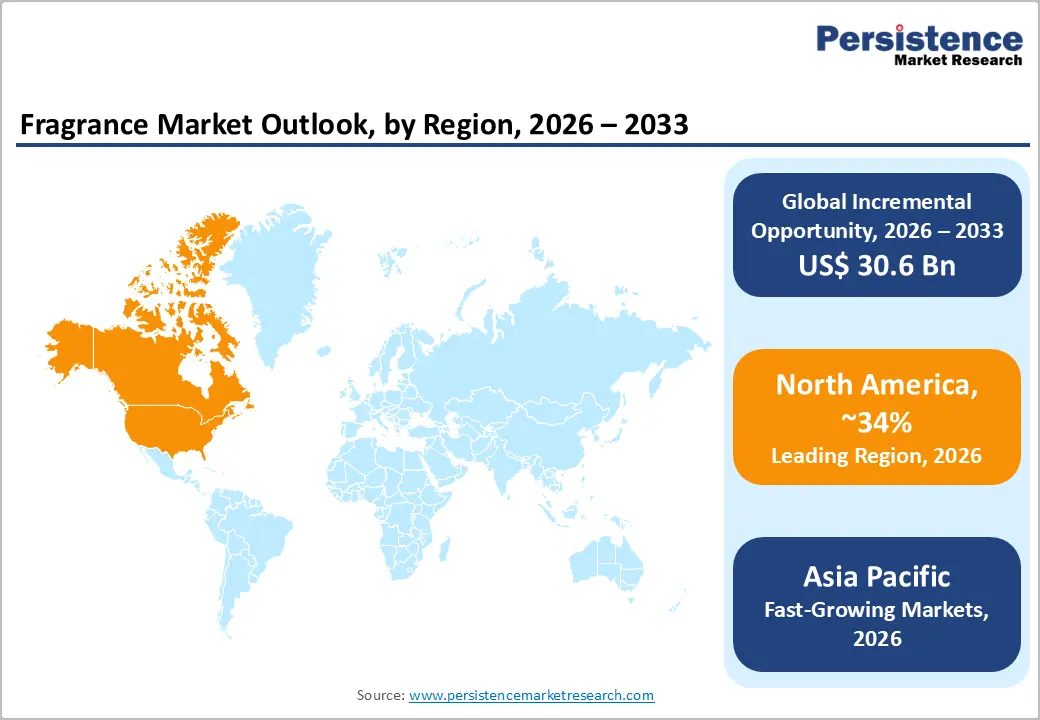

- Regional Leadership: North America is expected to lead the global market with an estimated 34% share in 2026, while Asia Pacific is projected to be the fastest-growing region at a 6.7% CAGR through 2033, supported by rapid urbanization and rising disposable incomes.

- Innovation Trends: Sustainable and personalized fragrances are gaining strong momentum, as clean-label demand and customization technologies reshape product development strategies.

| Key Insights | Details |

|---|---|

|

Fragrance Market Size (2026E) |

US$ 61.9 Bn |

|

Market Value Forecast (2033F) |

US$ 92.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

DRO Analysis

Driver - Rising Disposable Income and Premiumization Trends

Global income growth, particularly in emerging economies, continues to drive the fragrance market growth. According to the World Bank, global middle-class consumption is projected to exceed US$ 64 trillion by 2030, significantly boosting discretionary spending. Premium fragrances, especially fine fragrances, have seen strong growth in markets such as China and India. Consumers increasingly prefer luxury perfumes and artisanal scent profiles, reflecting a shift toward experiential consumption. This trend is further supported by urbanization and aspirational lifestyles, leading to higher per capita fragrance spending. As a result, brands are expanding their premium portfolios to capture this evolving demand.

This premiumization trend is further reinforced by recent industry developments. In 2025–2026, luxury brands accelerated investments in high-end and niche fragrance lines, launching couture collections to target younger, experience-driven consumers. The industry also witnessed a significant surge in innovation, with over 6,000 new perfume launches in 2025, reflecting strong global demand and rapid product diversification. This influx highlights how brands are capitalizing on preferences for exclusivity, storytelling, and personalization. At the same time, companies are advancing sustainable and customized fragrance solutions, strengthening brand differentiation and enabling higher value realization across premium segments.

Expansion of Personal Care and Ambient Fragrance Applications

The expansion of personal care and grooming routines continues to support steady demand for fragrance ingredients. Fragrances play a critical role in products such as deodorants, body mists, and skincare formulations, making them integral to daily usage patterns. Increasing awareness of hygiene, particularly in the post-pandemic period, has led to higher adoption of deodorants and antiperspirants across developing regions. Additionally, male grooming trends are expanding the addressable market, with rising participation from male consumers in fragrance usage. This structural shift ensures consistent demand across multiple product categories and strengthens baseline consumption.

At the same time, the demand for home fragrance products such as scented candles, diffusers, and sprays is growing rapidly. The adoption of ambient scenting systems in commercial spaces, retail stores, hotels, and offices is also expanding. Scent marketing has been shown to enhance customer dwell time and brand recall, with studies indicating up to a 40% increase in consumer engagement. In 2025, fragrance-infused personal care products with added functional benefits gained strong retail traction, particularly among younger consumers. These developments are diversifying application areas beyond personal use and creating new revenue streams for manufacturers.

Restraints - Stringent Regulatory Frameworks and Compliance Complexity

The fragrance industry operates under strict regulations set by authorities such as the European Chemicals Agency (ECHA) and IFRA, particularly concerning allergen disclosure and chemical safety. Over 80 fragrance ingredients are currently subject to restrictions or mandatory labeling requirements in the EU. These regulations significantly increase R&D costs and extend product development timelines. Smaller manufacturers often struggle to meet these evolving standards, limiting their ability to enter or expand in the market. Additionally, differences in regulatory frameworks across regions complicate global product standardization. As a result, companies face ongoing challenges in maintaining compliance while ensuring operational efficiency.

The developments over the years have further underscored the growing regulatory burden. European authorities have intensified requirements around ingredient transparency and safety documentation, increasing scrutiny across the value chain. This has forced companies to reformulate products and invest in compliant alternatives, adding both time and cost pressures.

The rising consumer awareness around ingredient safety, highlighted in leading media coverage, has accelerated demand for clean-label products. While this shift strengthens long-term brand trust, it creates immediate compliance challenges for manufacturers. Consequently, companies must continuously adapt to evolving standards while managing rising operational complexity.

Volatility in Raw Material Supply Chains

Natural fragrance ingredients such as essential oils are highly dependent on agricultural conditions and climate stability. For example, fluctuations in lavender and sandalwood supply have resulted in price volatility exceeding 20% annually in certain years, according to FAO agricultural data. This instability directly impacts production costs and reduces profit margins for manufacturers. In addition, geopolitical tensions and trade restrictions can disrupt access to key raw materials, particularly those sourced from specific regions. These uncertainties make long-term sourcing strategies more complex and increase exposure to unexpected cost variations.

Fragrance companies are increasingly shifting toward sustainable and ethically sourced raw materials to reduce risk and meet consumer expectations. For instance, multiple global brands expanded refillable perfume formats and reduced packaging material usage, as reported by leading outlets such as The Guardian, reflecting efforts to manage resource constraints and environmental impact. However, sourcing certified sustainable inputs often comes with higher costs and limited availability. This adds another layer of complexity to procurement strategies. As a result, companies are prioritizing supply chain diversification and resilience to maintain stability in an increasingly uncertain environment.

Opportunity - Expansion in Emerging Markets and Evolving Consumer Base

Emerging economies in the Asia Pacific, Africa, and Latin America present significant opportunities for fragrance market expansion. According to UN DESA, urban population growth in these regions will exceed 2.5 billion by 2050. Rising disposable incomes, along with greater exposure to global brands, are steadily increasing fragrance adoption among urban consumers.

Buyers are becoming more brand-conscious and are willing to spend more on personal grooming and lifestyle products. This trend is especially strong among younger demographics, who actively explore new fragrance formats and experiences. As a result, demand continues to rise across both mass-market and premium product segments.

A surge in fragrance consumption among Gen Z consumers, particularly in Asia, where social media platforms are accelerating product discovery and influencing purchase behavior. Companies such as Puig have expanded retail partnerships in the Middle East, while Shiseido has strengthened its distribution network across Southeast Asia. Government-led initiatives in countries such as India and Indonesia are improving retail infrastructure and supporting local manufacturing.

Sustainable Innovation and Personalization Technologies

Consumer demand for natural and sustainable fragrances is rising steadily, driven by increasing environmental awareness and more conscious purchasing behavior. OECD data indicates that over 60% of consumers are willing to pay a premium for eco-friendly products. This creates strong opportunities for brands to develop bio-based and biodegradable fragrance formulations. The transparency in sourcing and ethical production practices is becoming a critical factor in purchase decisions. Companies are therefore prioritizing clean-label innovation to strengthen trust and capture premium segments. This shift is reshaping how products are developed and positioned in the market.

Major fragrance brands have introduced refillable perfume formats and reduced packaging materials, as highlighted by The Guardian, aligning with sustainability goals and regulatory pressure on waste reduction. In parallel, digital innovation is transforming personalization. For instance, Symrise has introduced AI-assisted tools for faster custom scent development, while Givaudan has expanded its “Carto” platform to enable tailored fragrance design. Coverage from platforms such as Vogue also points to the growing popularity of scent layering and individualized fragrance routines. These advancements clearly demonstrate how sustainability and personalization are becoming central to competitive differentiation.

Category-wise Analysis

Product Type Insights

Deodorants and antiperspirants are set to command around 42% of the revenue share in 2026 due to their essential role in daily hygiene routines and widespread usage across diverse consumer groups. Their affordability and easy availability, particularly in price-sensitive markets, continue to support strong adoption, while rising urbanization and active lifestyles further drive consistent usage. Increasing awareness of personal hygiene in developing regions is accelerating penetration rates. Product innovations such as long-lasting protection and skin-friendly formulations are enhancing consumer appeal and differentiation.

In 2026, companies such as Unilever expanded portfolios with whole-body and sensitive-skin variants, while Procter & Gamble introduced clinical-strength and aluminum-free options. Additionally, retailers across Asia and Latin America are increasing shelf space, reinforcing accessibility and sustaining segment leadership.

Fine fragrances are set to witness the fastest growth, driven by rising demand for premium and luxury perfumes and a clear shift toward unique, personalized scent experiences. Consumers, especially millennials and Gen Z, are increasingly drawn to exclusivity, niche profiles, and strong brand storytelling.

The expansion of e-commerce has improved access to high-end products, while influencer-led marketing continues to shape buying behavior. Luxury houses such as Chanel and Dior have expanded limited-edition and boutique-exclusive collections to strengthen premium positioning. At the same time, travel retail and department stores are enhancing in-store experiences through personalized consultations. These factors are collectively accelerating growth in the fine fragrance segment.

Application Insights

Personal fragrance is expected to dominate with approximately 55% share in 2026, supported by frequent usage and the strong link between fragrance and self-expression. Products such as perfumes, deodorants, and body mists are now viewed as essential elements of daily grooming routines. Continuous innovation in formulations, packaging, and branding is helping brands attract a wide consumer base.

Rising disposable incomes in emerging markets are further boosting spending on personal care products. Retailers such as Sephora are expanding fragrance assortments and introducing in-store personalization services to enhance engagement. Brands are also promoting travel-sized and layering-friendly formats to encourage experimentation. These developments continue to reinforce the segment’s market leadership.

Ambient scenting is likely to emerge as a key growth area, driven by its increasing use across commercial spaces such as hotels, retail outlets, and offices. Businesses are leveraging scent marketing to enhance customer experience, improve dwell time, and strengthen brand recall. Growing interest in wellness and sensory environments is also supporting demand for advanced scent diffusion systems.

Companies such as Marriott International are expanding signature scent programs across premium properties to deliver consistent brand experiences. Retailers are integrating scent systems into flagship stores to create immersive environments. Additionally, real estate developers are incorporating ambient scenting into modern spaces.

Regional Analysis

North America Fragrance Market Trends

North America is expected to account for approximately 34% of the global fragrance market in 2026, maintaining its leadership due to strong consumer spending on personal care and premium fragrance products. The United States drives regional demand, supported by high purchasing power and lifestyle-oriented consumption. A well-developed retail ecosystem, spanning department stores, specialty beauty chains, and e-commerce, ensures wide accessibility.

Consumers increasingly prefer luxury, niche, and customized fragrances, reflecting evolving tastes. The presence of globally established brands further strengthens market maturity. These factors collectively sustain North America’s dominant position in the global landscape.

Recent developments further reinforce this strength. Companies such as Ulta Beauty have expanded fragrance sections across stores, while Coty Inc. continues to invest in direct-to-consumer platforms and digital personalization tools. Premium and niche brands are increasing their presence through standalone boutiques and shop-in-shop formats in key metropolitan areas. Expansion of fulfillment infrastructure is improving delivery speed and e-commerce efficiency. Retailers are also integrating advanced recommendation tools to enhance engagement.

Europe Fragrance Market Trends

Europe represents a mature yet highly influential market, driven by strong demand for luxury and artisanal fragrances. Key countries such as Germany, France, and the U.K. continue to lead regional performance due to high consumer awareness and established fragrance traditions. France remains a global hub for perfumery, supported by its heritage and expertise. The region benefits from high per capita consumption and a strong preference for premium products. Well-developed distribution networks and luxury retail channels further support market stability. These factors ensure Europe’s continued importance in the global fragrance landscape.

Luxury groups such as LVMH increased their fragrance retail footprint through boutique openings and experiential store formats across Paris, Milan, and London. The niche fragrance brands are expanding through selective distribution partnerships and concept stores to reach premium consumers. European Union policies are also encouraging sustainable production, leading to investments in green chemistry and eco-friendly packaging facilities.

Additionally, cross-border e-commerce within the EU is improving product accessibility. These developments demonstrate how expansion strategies and regulatory alignment are shaping the region’s competitive landscape.

Asia Pacific Fragrance Market Trends

Asia Pacific is projected to be the fastest-growing market at a 6.7% CAGR by 2033, driven by rapid urbanization and rising disposable incomes. Major markets such as China, Japan, and India are witnessing increasing adoption of fragrance products, particularly among younger consumers. Growing exposure to global brands and evolving lifestyle patterns are influencing purchasing behavior. The region also benefits from a large population base, creating significant demand potential. As consumers shift toward premium and lifestyle-oriented products, fragrance usage is expanding across urban and semi-urban areas. These dynamics position the Asia Pacific as a key growth engine for the global market.

Recent regional developments highlight strong expansion activity. Companies such as Reliance Retail are rapidly scaling beauty and fragrance store networks across India, improving offline accessibility. In Southeast Asia, international brands are entering new markets through partnerships with regional distributors and e-commerce platforms.

In China, brands are expanding via flagship digital stores and livestream commerce to capture younger audiences. Governments across the region are also promoting domestic manufacturing through incentives and infrastructure investments. These combined expansion efforts are accelerating market penetration and reinforcing Asia Pacific’s high-growth trajectory.

Competitive Landscape

The global fragrance market is moderately consolidated, with leading players such as L'Oréal, Estée Lauder Companies, Coty Inc., and LVMH holding a significant revenue share. These companies benefit from strong brand portfolios, global distribution networks, and leadership in premium fragrances. High investments in marketing, celebrity endorsements, and product innovation strengthen their competitive positioning. Continuous R&D efforts support advancements in sustainable and personalized fragrance offerings.

Key ingredient suppliers such as Givaudan, International Flavors & Fragrances, and Symrise play a crucial role in enabling product innovation. Niche and regional brands are gaining share through artisanal and clean-label offerings. Entry barriers remain high due to brand loyalty, regulatory requirements, and marketing costs. However, digital-first brands and e-commerce platforms are enabling new entrants, while consolidation continues through acquisitions and partnerships.

Key Industry Developments

- In March 2026, Estée Lauder Companies entered merger discussions with Puig to potentially form a combined entity valued at around US$ 40 billion, aiming to consolidate their fragrance portfolios and enhance market leadership in the global fragrance industry.

- In October 2025, L'Oréal agreed to acquire the beauty division of Kering for approximately €4 billion, including premium fragrance assets such as Creed and securing a long-term Gucci fragrance license valued at €1.5 billion, significantly strengthening its luxury fragrance portfolio and global competitive positioning.

Companies Covered in Fragrance Market

- LVMH

- Estée Lauder Companies Inc.

- Coty Inc.

- L’Oréal Group

- Procter & Gamble

- Unilever

- Givaudan

- Firmenich

- International Flavors & Fragrances Inc.

- Symrise AG

- Shiseido Company

- Chanel

- Puig

- Amorepacific Corporation

Frequently Asked Questions

The global fragrance market is projected to reach US$ 61.9 billion in 2026.

Rising disposable incomes, increasing demand for premium fragrances, and expanding personal care usage drives the market growth.

The fragrance market is expected to reach a CAGR of 5.9% from 2026 to 2033.

Expansion in emerging markets and innovation in sustainable and personalized fragrances are creating major opportunities.

L'Oréal, Estée Lauder Companies, Coty Inc., LVMH, and Givaudan are key players.