- Executive Summary

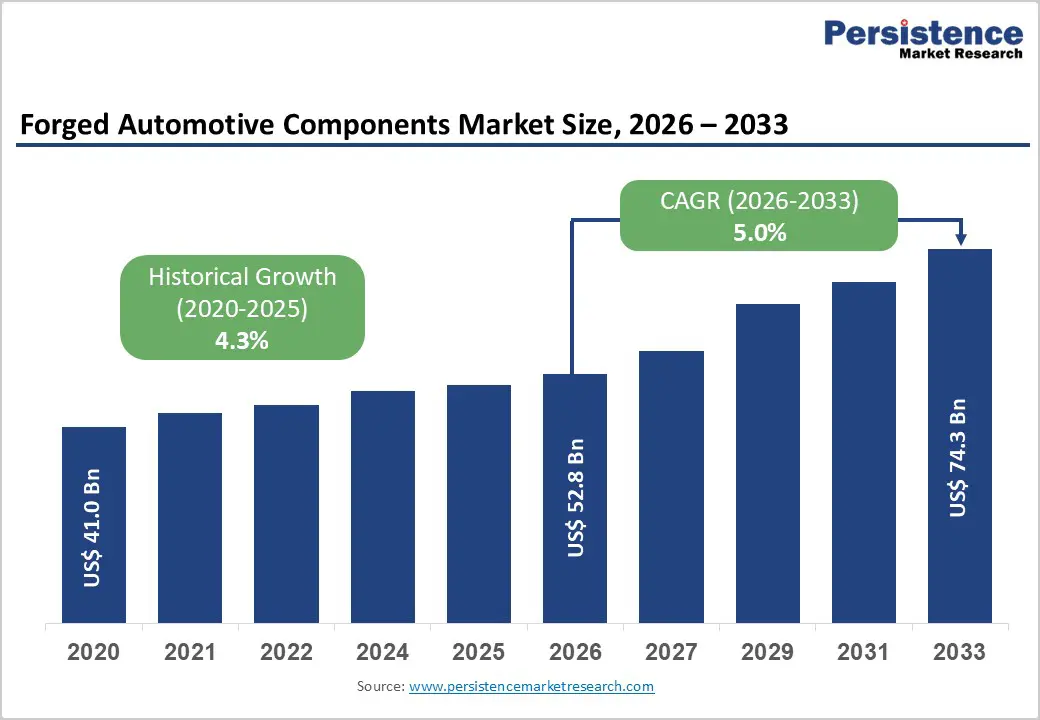

- Global Forged Automotive Components Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Market Dynamics

- Driver

- Restraint

- Opportunities

- Trends

- Macro-Economic Factors

- Global GDP Outlook

- Global Prison Growth Outlook

- Global Crime Rates by Country

- Global Prison Population by Country

- Global Private Prison Market Growth Outlook

- Other Macro-economic Factors

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- Value Added Insights

- Value Chain analysis

- Key Market Players

- Product Adoption Analysis

- Key Promotional Strategies by key players

- PESTLE Analysis

- Porter's Five Forces Analysis

- Regulatory and Technology Landscape

- Price Trend Analysis, 2025

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Forged Automotive Components Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Forged Automotive Components Market Outlook: Vehicle Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Vehicle Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Vehicles

- Market Attractiveness Analysis: Vehicle Type

- Global Forged Automotive Components Market Outlook: Forging Process

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Forging Process, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Forging Process, 2026-2033

- Impression Die Forging

- Hydraulic Presses

- Mechanical Presses

- Hammers

- Cold Forging

- Open Die Forging

- Seamless Rolled Ring Forging

- Impression Die Forging

- Market Attractiveness Analysis: Forging Process

- Global Forged Automotive Components Market Outlook: Material

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Material, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Steel

- Aluminium

- Other

- Market Attractiveness Analysis: Material

- Global Forged Automotive Components Market Outlook: Automotive Component

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Automotive Component, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Automotive Component, 2026-2033

- Connecting rods

- Injectors

- Gears

- Crankshafts

- Axles

- Bearings

- Pistons

- Steering Knuckles

- CV Joints

- Others

- Market Attractiveness Analysis: Automotive Component

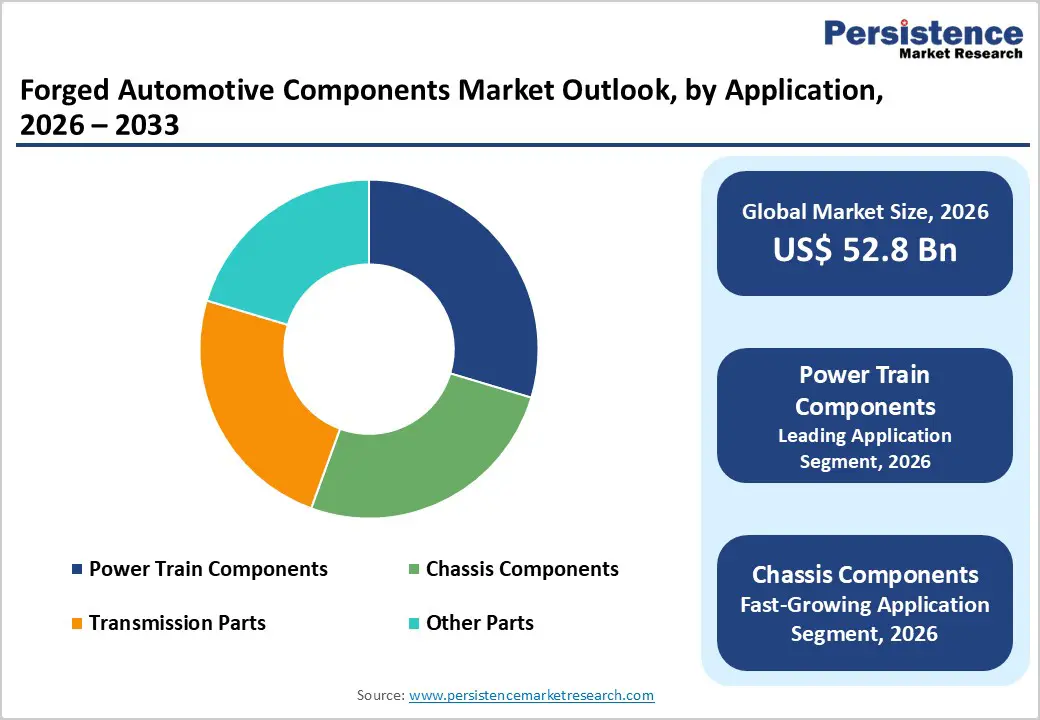

- Global Forged Automotive Components Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Power Train Components

- Chassis Components

- Transmission Parts

- Other Parts

- Market Attractiveness Analysis: Application

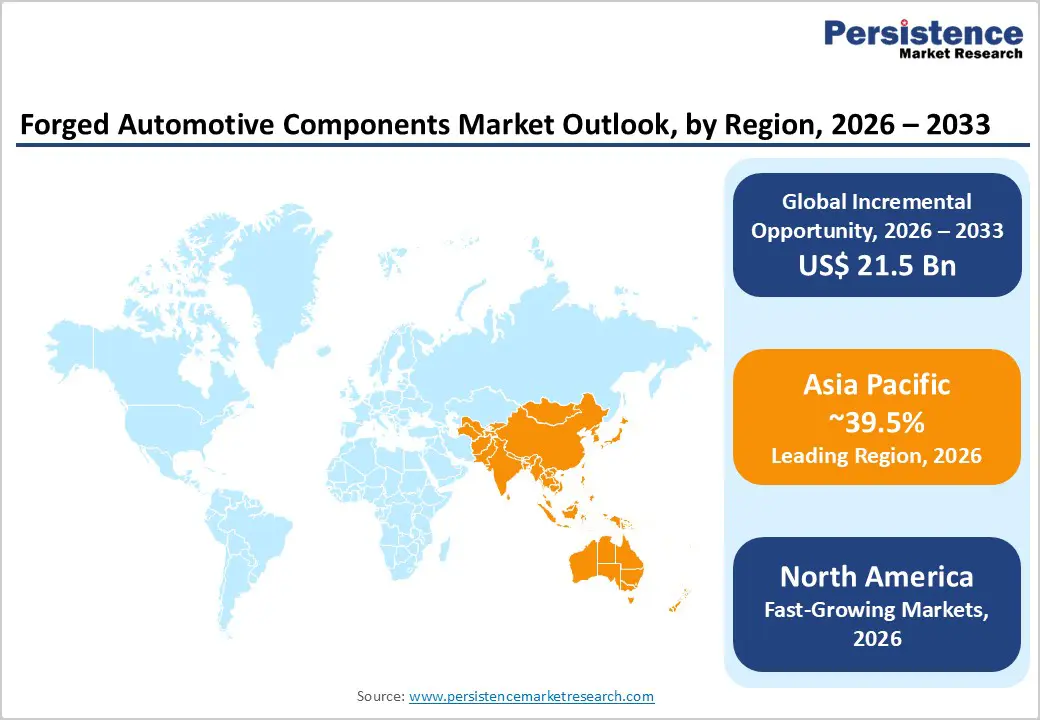

- Global Forged Automotive Components Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Forged Automotive Components Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Vehicles

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Forging Process, 2026-2033

- Impression Die Forging

- Hydraulic Presses

- Mechanical Presses

- Hammers

- Cold Forging

- Open Die Forging

- Seamless Rolled Ring Forging

- Impression Die Forging

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Steel

- Aluminium

- Other

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Automotive Component, 2026-2033

- Connecting rods

- Injectors

- Gears

- Crankshafts

- Axles

- Bearings

- Pistons

- Steering Knuckles

- CV Joints

- Others

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Power Train Components

- Chassis Components

- Transmission Parts

- Other Parts

- Europe Forged Automotive Components Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Vehicles

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Forging Process, 2026-2033

- Impression Die Forging

- Hydraulic Presses

- Mechanical Presses

- Hammers

- Cold Forging

- Open Die Forging

- Seamless Rolled Ring Forging

- Impression Die Forging

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Steel

- Aluminium

- Other

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Automotive Component, 2026-2033

- Connecting rods

- Injectors

- Gears

- Crankshafts

- Axles

- Bearings

- Pistons

- Steering Knuckles

- CV Joints

- Others

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Power Train Components

- Chassis Components

- Transmission Parts

- Other Parts

- East Asia Forged Automotive Components Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Vehicles

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Forging Process, 2026-2033

- Impression Die Forging

- Hydraulic Presses

- Mechanical Presses

- Hammers

- Cold Forging

- Open Die Forging

- Seamless Rolled Ring Forging

- Impression Die Forging

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Steel

- Aluminium

- Other

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Automotive Component, 2026-2033

- Connecting rods

- Injectors

- Gears

- Crankshafts

- Axles

- Bearings

- Pistons

- Steering Knuckles

- CV Joints

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Power Train Components

- Chassis Components

- Transmission Parts

- Other Parts

- South Asia & Oceania Forged Automotive Components Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Vehicles

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Forging Process, 2026-2033

- Impression Die Forging

- Hydraulic Presses

- Mechanical Presses

- Hammers

- Cold Forging

- Open Die Forging

- Seamless Rolled Ring Forging

- Impression Die Forging

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Steel

- Aluminium

- Other

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Automotive Component, 2026-2033

- Connecting rods

- Injectors

- Gears

- Crankshafts

- Axles

- Bearings

- Pistons

- Steering Knuckles

- CV Joints

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Power Train Components

- Chassis Components

- Transmission Parts

- Other Parts

- Latin America Forged Automotive Components Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Vehicles

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Forging Process, 2026-2033

- Impression Die Forging

- Hydraulic Presses

- Mechanical Presses

- Hammers

- Cold Forging

- Open Die Forging

- Seamless Rolled Ring Forging

- Impression Die Forging

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Steel

- Aluminium

- Other

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Automotive Component, 2026-2033

- Connecting rods

- Injectors

- Gears

- Crankshafts

- Axles

- Bearings

- Pistons

- Steering Knuckles

- CV Joints

- Others

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Power Train Components

- Chassis Components

- Transmission Parts

- Other Parts

- Middle East & Africa Forged Automotive Components Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Vehicle Type, 2026-2033

- Heavy Commercial Vehicles

- Light Commercial Vehicles

- Passenger Vehicles

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Forging Process, 2026-2033

- Impression Die Forging

- Hydraulic Presses

- Mechanical Presses

- Hammers

- Cold Forging

- Open Die Forging

- Seamless Rolled Ring Forging

- Impression Die Forging

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Material, 2026-2033

- Steel

- Aluminium

- Other

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Automotive Component, 2026-2033

- Connecting rods

- Injectors

- Gears

- Crankshafts

- Axles

- Bearings

- Pistons

- Steering Knuckles

- CV Joints

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Application, 2026-2033

- Power Train Components

- Chassis Components

- Transmission Parts

- Other Parts

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- ThyssenKrupp AG

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- CIE Automotive

- NTN Corporation

- American Axle and Manufacturing Inc.

- Bharat Forge Limited

- Ramkrishna Forgings

- Dana Limited

- Meritor Inc.

- ZF Friedrichshafen AG

- Kalyani Group

- Om Forge

- Super Auto Forge Private Limited

- GAZ Group

- TBK Co., Ltd.

- EL FORGE LIMITED

- ThyssenKrupp AG

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

Loading page data

Please wait a moment