- Technology

- Flashlight Market

Flashlight Market Size, Share, and Growth Forecast 2026 - 2033

Flashlight Market by Product Type (LED Flashlights, Incandescent Flashlights, HID Flashlights, Solar Powered Flashlights, Others), Power Source (Non-Rechargeable, Rechargeable), Material (Aluminum, Plastic, Stainless Steel, Others), End-user (Commercial, Residential, Industrial, Outdoor Activities, Others), and Regional Analysis for 2026 - 2033

Flashlight Market Size and Trend Analysis

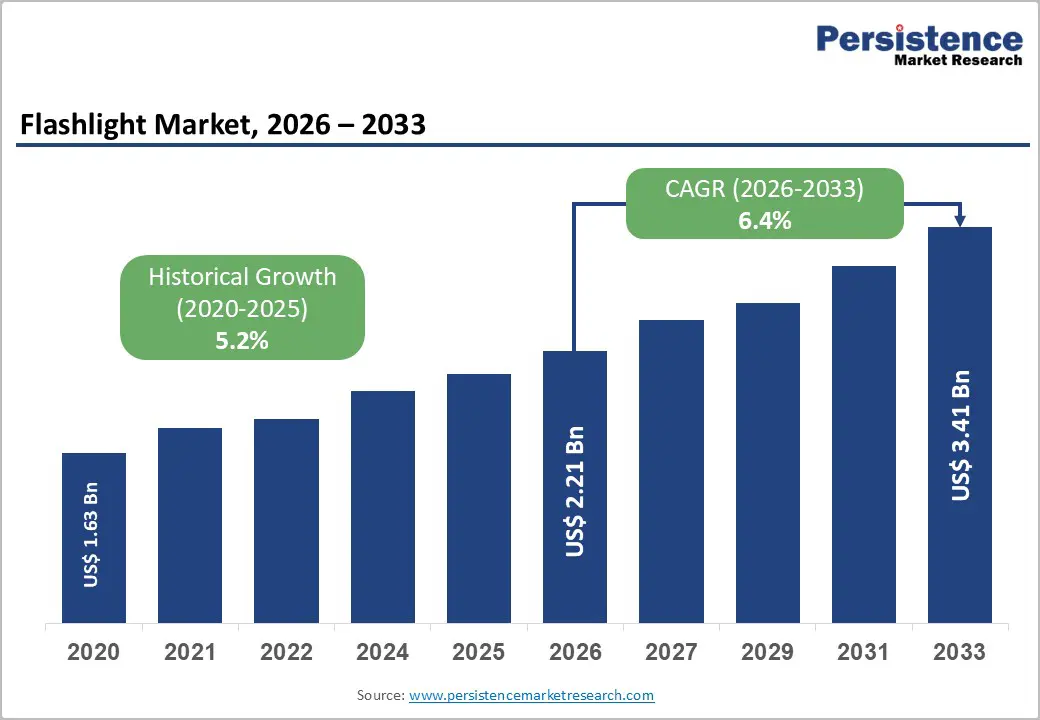

The global flashlight market size is likely to be valued at US$ 2.21 billion in 2026 and is projected to reach US$ 3.41 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033. This sustained expansion is driven primarily by rising demand for energy-efficient portable lighting across emergency preparedness, law enforcement, and outdoor recreation sectors.

The market has witnessed a significant transformation with the rapid adoption of LED beam technology, which has substantially reduced energy consumption while improving lumen output, efficiency, and product lifespan compared to conventional incandescent flashlights. In addition, rising infrastructure development across the Asia Pacific and the Middle East, along with growing consumer awareness regarding disaster preparedness amid increasing natural calamities, is driving steady demand across residential, commercial, and industrial end-use sectors.

Key Industry Highlights:

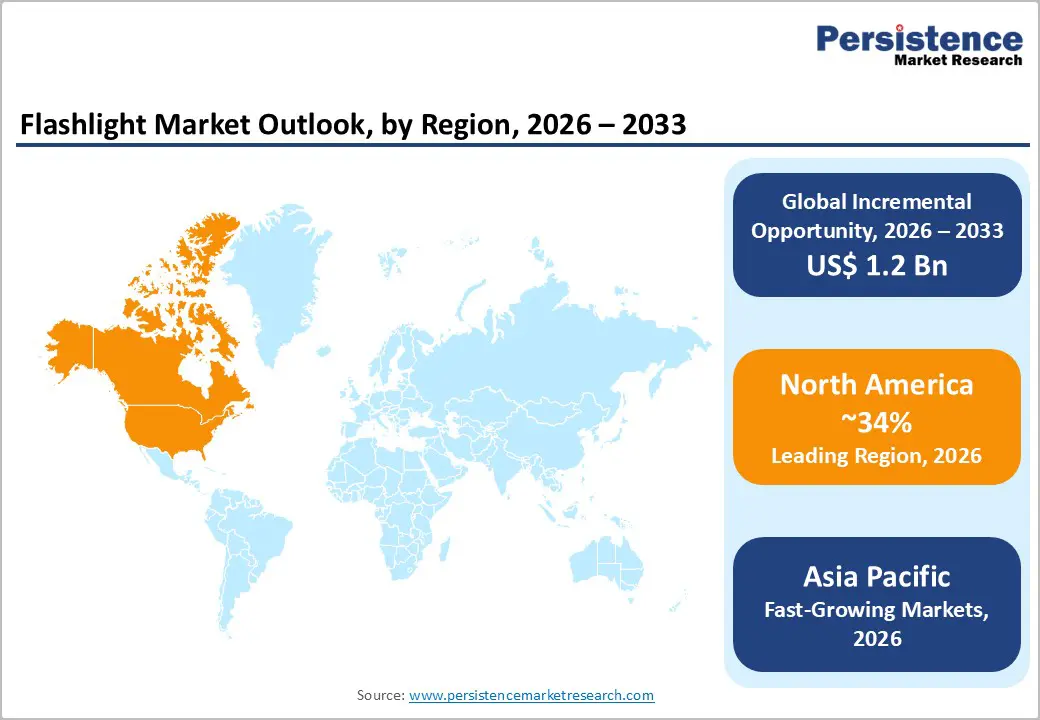

- Leading Region: North America leads the global flashlight market with approximately 34% revenue share in 2026, driven by robust emergency preparedness culture, defense and law enforcement procurement, and a mature outdoor recreation economy sustaining consistent high-value demand.

- Fast-Growing Market: Asia Pacific is the fast-growing regional market with a projected CAGR of 8.1% by 2033, fueled by rapid industrialization, rural electrification programs, infrastructure investment, and surging outdoor recreation adoption across China, India, and Southeast Asia.

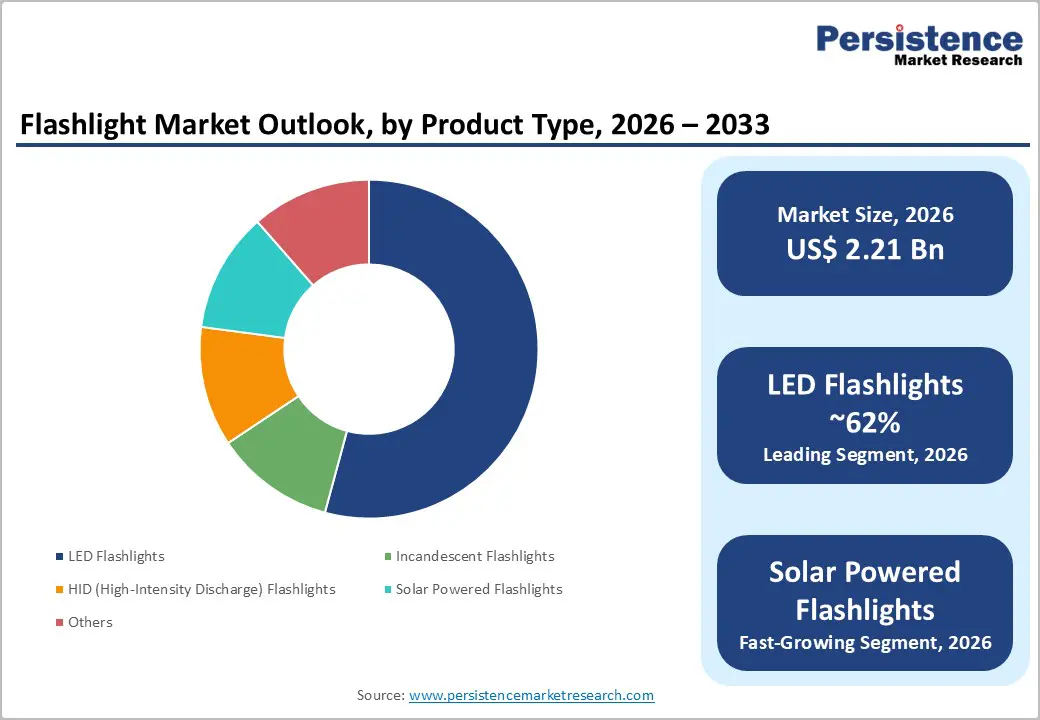

- Dominant Product: LED flashlights dominate the product type category with approximately 62% share in 2026, supported by superior energy efficiency, declining component costs, regulatory mandates phasing out incandescent lighting, and compatibility with modern rechargeable battery systems.

- Fast-Growing Product: Solar-powered flashlights are the fast-growing product type segment with a leading CAGR driven by off-grid demand in Sub-Saharan Africa and South Asia, rural electrification initiatives, and falling solar component costs.

- Key Opportunity: Emerging markets in the Asia Pacific and Africa present a compelling opportunity for manufacturers offering rechargeable and solar-powered flashlights tailored to off-grid communities, with an estimated 675 million people globally still lacking reliable electricity access per IEA.

Market Dynamics

Drivers - Rising Emergency Preparedness Spending and Tactical Lighting Demand

Global governmental and institutional investments in emergency preparedness have surged significantly over the past decade. According to the U.S. Federal Emergency Management Agency (FEMA), emergency preparedness expenditures in the U.S. exceeded US$ 33 Bn in fiscal year 2023, with portable lighting cited as a critical household and first-responder requirement. The demand for Tactical Emergency Lighting solutions, particularly among military, law enforcement, and search-and-rescue personnel, has accelerated the adoption of ruggedized, high-performance flashlights.

The U.S. Department of Defense (DoD) regularly procures tactical lighting gear meeting MIL-STD-810 environmental standards. Globally, the increasing frequency of extreme weather events, with the World Meteorological Organization (WMO) reporting a 5x increase in weather-related disasters over the past 50 years, directly correlates with heightened consumer demand for reliable portable lighting products, sustaining long-term market growth.

Proliferation of LED Technology and Energy Efficiency Standards

The widespread transition from incandescent to LED Beam Technology has been a pivotal driver of flashlight market expansion. LED flashlights now account for the majority of unit sales globally, owing to their superior energy efficiency, extended battery life, and enhanced High Lumen Output per watt. The U.S. Department of Energy (DOE) reports that LED lighting is approximately 75% more energy efficient than incandescent lighting and lasts up to 25 times longer.

This transition has been further accelerated by regulatory mandates phasing out incandescent bulbs across the European Union (Regulation EU 2019/2020) and multiple U.S. states. Consumer preference for products delivering robust performance at lower operational costs, combined with declining LED component prices falling over 90% in the last decade, per the International Energy Agency (IEA) has propelled LED flashlight adoption across all end-use segments.

Restraints - Commoditization and Price Compression from Low-cost Manufacturers

One of the most significant restraints facing the flashlight market is intense price competition driven by the proliferation of low-cost manufacturers, particularly from China and Southeast Asia. According to data from the World Trade Organization (WTO), China accounted for over 65% of global portable lighting exports by volume in 2023. This has created severe margin pressure on established brands, limiting their ability to invest in premium product development and innovation.

The commoditization of standard LED flashlights has compressed average selling prices in mass-market channels, making it challenging for mid-tier players to differentiate solely on performance parameters without significant marketing investment.

Environmental and Regulatory Challenges Around Battery Disposal

Increasing regulatory scrutiny surrounding battery disposal and e-waste management for flashlight products. The EU Battery Regulation (EU 2023/1542), effective from 2024, mandates extended producer responsibility and enforces stricter recycling targets for portable battery products. Compliance costs for manufacturers shipping into the EU have increased, particularly for non-rechargeable battery-dependent products. The Basel Convention further restricts the cross-border movement of hazardous battery waste, complicating supply chains. These regulatory pressures are disproportionately challenging for smaller manufacturers who lack the infrastructure and capital to establish compliant take-back programs.

Opportunities - Expanding the Outdoor Recreation Economy and Waterproof Portable Design Demand

The global outdoor recreation industry presents a compelling growth opportunity for flashlight manufacturers. The Outdoor Industry Association (OIA) estimated the U.S. outdoor recreation economy alone at US$ 862 Bn in 2022, with camping, hiking, and adventure sports registering year-on-year growth. Consumers in this segment actively seek Waterproof Portable Design flashlights that are compact, durable, and capable of operating in extreme environmental conditions.

The growing popularity of outdoor activities post-COVID, with the National Park Service (NPS) reporting 325.5 million recreation visits in 2022, directly expands the addressable consumer base. Manufacturers investing in IPX8-rated waterproofing, impact-resistant casing, and lightweight aluminum or titanium constructions are well-positioned to capture premium pricing and brand loyalty in this high-growth outdoor segment.

Rapid Urbanization and Smart Infrastructure Development in Emerging Economies

Emerging economies across the Asia Pacific, Latin America, and Africa represent a significant untapped opportunity for flashlight market participants. According to the United Nations (UN), the global urban population is expected to increase by 2.5 billion by 2050, with the majority of growth concentrated in Asia and Africa. The World Bank reports ongoing infrastructure development investments exceeding US$4 trillion annually across developing economies, driving industrial and construction sector demand for reliable portable lighting.

Furthermore, power outage frequency remains high in many developing regions. The International Energy Agency (IEA) estimates that approximately 675 million people globally still lack reliable electricity access, making rechargeable battery systems in solar-powered and USB-rechargeable flashlights a critical product category with immense demand potential in off-grid and semi-urban communities.

Category-wise Analysis

Product Type Insights

LED Flashlights dominate the global flashlight market, commanding approximately 62% of total market share in 2026. This dominance is deeply rooted in the superior technological profile of LED-based solutions, exceptional energy efficiency, extended operational lifespan averaging 50,000 hours or more, and versatile High Lumen Output configurations ranging from compact everyday-carry models to professional-grade 1,000+ lumen tactical units.

According to the U.S. Department of Energy, LED lighting accounts for over 50% of all lighting product sales in the U.S. as of 2022, a trend mirrored in the portable lighting segment. The declining cost of LED components, with prices for standard LED chips falling over 40% between 2018 and 2023, has further democratized access, driving volume across both premium and mass-market product lines. LED flashlights are also preferred for their compatibility with modern Rechargeable Battery Systems and smart features such as adjustable beam modes and SOS signaling, reinforcing their market leadership across commercial, industrial, and outdoor end-use segments.

Solar-powered flashlights represent the fastest-growing segment within the product type category, projected to expand at a CAGR of 9.2% between 2026 and 2033. The accelerating push toward renewable energy and growing demand in off-grid and rural areas across Sub-Saharan Africa, South Asia, and Southeast Asia are primary growth catalysts. Government-backed rural electrification programs and falling solar panel costs continue to bolster the adoption of solar-integrated portable lighting solutions globally.

Power Source Insights

The rechargeable segment holds the leading position in the power source category, accounting for approximately 58% of the flashlight market in 2026. The shift toward rechargeable flashlights is driven by long-term cost advantages, environmental sustainability considerations, and the rapid proliferation of USB-C and wireless charging standards that have simplified the recharging process. According to the International Energy Agency (IEA), global lithium-ion battery demand grew by over 65% between 2020 and 2023, reflecting broader consumer acceptance of rechargeable products.

Rechargeable Battery Systems in modern flashlights are increasingly lithium-ion or lithium-polymer based, offering superior energy density compared to alkaline or NiMH alternatives. Professional-grade rechargeable flashlights used in law enforcement, firefighting, and industrial inspection applications further reinforce the segment's dominance. The growing availability of power bank-compatible designs and the integration of USB-C ports into flashlight housings have significantly broadened the appeal of rechargeable models across all consumer demographics.

Non-Rechargeable flashlights continue to exhibit steady, if slower, demand growth with an estimated CAGR of 3.8% in the forecast period. This segment remains relevant for emergency preparedness kits, remote applications, and regions with limited electricity infrastructure, where alkaline battery availability serves as a practical advantage over rechargeable alternatives requiring consistent power access.

Material Insights

Aluminum leads the material category with a share of approximately 48% in 2026. Aluminum's dominance is attributable to its exceptional strength-to-weight ratio, natural heat dissipation properties, and corrosion resistance, making it the material of choice for mid-range to premium flashlight housings. Aerospace-grade 6061-T6 aluminum alloy is widely used in tactical and professional flashlights, offering mil-spec durability while maintaining a lightweight profile. According to the Aluminum Association, global demand for aluminum in consumer electronics and portable devices continued to grow at a steady pace in 2022 - 2023, driven by its favorable mechanical properties.

The premium positioning of aluminum-bodied flashlights also commands higher average selling prices compared to plastic counterparts, contributing disproportionately to revenue share. Leading manufacturers including Streamlight and SureFire, extensively deploy machined aluminum in their professional product lines to meet rigorous durability and thermal management requirements.

Stainless Steel emerges as the fast-growing material segment with a leading CAGR. Its premium aesthetic appeal, combined with superior corrosion resistance in marine and high-humidity environments, is attracting demand from luxury EDC (Every Day Carry) flashlight buyers and professional users in coastal and offshore industrial applications, representing a niche but high-value growth avenue.

End-user Insights

The outdoor activities segment leads the end-user category with an estimated market share of approximately 31% in 2026. The outdoor recreation economy has been one of the most resilient consumer spending categories post-pandemic. Consumers engaged in camping, hiking, trail running, mountaineering, and water sports require reliable, Waterproof Portable Design lighting that performs across extreme conditions. According to the Outdoor Industry Association (OIA), approximately 164.2 million Americans, or 55% of the U.S. population aged six and above, participated in outdoor recreation in 2022.

Globally, the outdoor tourism sector continues to expand, with the World Tourism Organization (UNWTO) highlighting adventure tourism as among the fastest-growing travel segments. Flashlight products catering to this segment, such as headlamps, compact LED torches, and multi-mode lanterns benefit from consistent seasonal demand, strong brand loyalty, and higher willingness-to-pay compared to residential or commercial buyers.

The Industrial end-use segment is projected to be the fast-growing category with an estimated CAGR of 7.8% between 2026 and 2033. Rising investments in oil and gas infrastructure, mining expansion in developing economies, and increased ATEX-certified lighting requirements in hazardous work environments are driving the procurement of specialized industrial-grade flashlights. The International Labour Organization (ILO) has reported increased global employment in extractive industries, amplifying demand for certified portable lighting solutions.

Regional Insights

North America Flashlight Market Trends

North America remains the dominant regional market for flashlights, accounting for approximately 34% of global revenue in 2026. The region's leadership is anchored by high consumer spending on emergency preparedness, a mature outdoor recreation ecosystem, and robust procurement by government and defense agencies. FEMA's National Preparedness Goal consistently emphasizes portable lighting as a household emergency essential, spurring consumer purchasing particularly ahead of hurricane and wildfire seasons.

The presence of globally recognized flashlight manufacturers and a well-established retail distribution network spanning big-box retailers, e-commerce platforms, and specialty outdoor stores further supports market maturity.

Regulatory and institutional demand dynamics are particularly favorable. The U.S. Department of Defense and Department of Homeland Security represent significant institutional buyers of tactical and high-performance lighting. The commercial construction boom, with U.S. Census Bureau data showing residential construction spending exceeding US$ 900 Bn in 2023, also drives industrial and contractor flashlight demand. Canada contributes through its mining and oil sands sectors, which mandate certified portable lighting in underground and hazardous environments per Transport Canada and provincial occupational safety regulations.

- U.S. Leads North America with Tactical and Consumer Flashlight Demand

The United States represents approximately 78-80% of the North American flashlight market, reflecting its scale and depth across consumer, commercial, and government procurement channels. With a CAGR of approximately 5.9% projected for the forecast period, the U.S. market benefits from unique drivers: widespread homeowner emergency preparedness culture, law enforcement and military procurement, and a thriving outdoor retail industry. The American Hiking Society estimates over 47 million Americans hike annually, directly sustaining demand for high-performance portable lighting. Government and institutional procurement further stabilizes market revenues, making the U.S. the single most important national market globally for flashlight sales.

Europe Flashlight Market Trends

Europe constitutes the second-largest regional market for flashlights, with a collective share of approximately 27% in 2026. The region is characterized by strong regulatory compliance environments, particularly the EU RoHS Directive and EU Battery Regulation 2023/1542, which drive demand for energy-efficient, environmentally compliant LED and rechargeable flashlight products. Outdoor recreation has a deep cultural rooting across Germany, the Nordic countries, and France, where hiking, cycling, and mountaineering traditions sustain consistent consumer demand.

The European Outdoor Group reported that the European outdoor equipment market grew steadily through 2022-2023, reinforcing the addressable consumer base.

Industrial and construction end-use is particularly significant in Europe. The EU's Green Deal and infrastructure investment programs under REPowerEU are driving energy sector development and construction activity, indirectly supporting professional lighting procurement. Additionally, growing emergency preparedness awareness amid geopolitical uncertainties has prompted households and civil defense agencies across Eastern and Central Europe to increase stocks of portable lighting and emergency supplies, providing a meaningful demand uplift.

- Germany: Engineering-Driven LED Flashlight Innovation Hub in Europe

Germany represents the largest single national market within Europe for flashlights, accounting for approximately 22-24% of the regional share. Germany's manufacturing and engineering culture drives demand for high-quality, precision-engineered LED flashlights in both professional and consumer segments. The country's robust industrial base, spanning automotive, machinery, and construction, generates sustained procurement of certified portable lighting.

- U.K.: Outdoor Heritage and Emergency Preparedness Driving Flashlight Sales

The United Kingdom accounts for approximately 17-19% of the European flashlight market. The U.K.'s market is shaped by its strong outdoor recreation tradition, with organisations such as the British Mountaineering Council (BMC) reporting millions of active members and participants in hill walking and climbing. Post-Brexit, the U.K. has maintained regulatory alignment with many EU CE marking requirements for portable lighting products. The market is forecast to reach a CAGR of 5.3% between 2026 and 2033, supported by consistent demand from emergency services, the construction sector, and growing household emergency preparedness awareness.

- France: Outdoor Tourism and Public Safety Fueling Portable Lighting Adoption

France holds approximately 14-16% of the European flashlight market. As the world's most visited tourist destination, welcoming over 100 million international visitors annually, according to the UNWTO France's outdoor and adventure tourism economy creates sustained demand for portable lighting products. French consumer electronics regulations align with EU RoHS and Ecodesign standards, favorably positioning LED and rechargeable flashlight brands.

- Italy: Industrial Safety Regulations Driving Certified Flashlight Procurement

Italy represents approximately 11-13% of the European flashlight market, with its market dynamics strongly influenced by industrial safety standards under Legislative Decree 81/2008 (the Italian Consolidated Act on Safety at Work). The country's significant manufacturing, construction, and agricultural sectors generate consistent demand for ATEX-certified and high-performance professional flashlights. Italy's market is projected to register a CAGR of 4.8% between 2026 and 2033, anchored by industrial procurement cycles, growing consumer outdoor culture, and alignment with EU battery and product safety regulations requiring compliant portable lighting.

Asia Pacific Flashlight Market Trends

Asia Pacific is the fast-growing regional market for flashlights, expected to register a CAGR of 8.1% between 2026 and 2033. The region benefits from a powerful combination of large and growing populations, rapid industrialization, significant infrastructure investment, and manufacturing cost advantages. China dominates both flashlight production and consumption, while India and Southeast Asian markets are emerging as high-growth demand centers driven by urbanization, industrial expansion, and rising disposable incomes.

The region also accounts for the majority of global flashlight manufacturing output, with supply chain ecosystems for LED components, batteries, and precision machining concentrated in China, Taiwan, and South Korea.

Outdoor recreation adoption is accelerating across the Asia Pacific, with camping and hiking growing rapidly in China, Japan, South Korea, and Australia. According to the China Tourism Academy, domestic camping and outdoor tourism participation in China surpassed 350 million trips in 2022, creating enormous consumer demand for portable lighting. The region's exposure to natural disasters, typhoons, earthquakes, and monsoon flooding also drives emergency preparedness procurement of Rechargeable Battery Systems in flashlights and solar-powered portable lighting solutions across residential and civil defense applications.

- China: Global Flashlight Manufacturing Powerhouse and Mass-Market Consumer Base

China dominates the Asia Pacific flashlight market with an estimated 45-48% regional share, driven simultaneously by its status as the world's leading flashlight manufacturer and its vast domestic consumer base. Chinese manufacturers produce the majority of global LED components and finished flashlight products exported worldwide. Domestically, demand is driven by infrastructure construction US$ 1.4 Tn in infrastructure investment planned under China's 14th Five-Year Plan, industrial applications, and rapidly growing outdoor recreation. The Chinese flashlight market is forecast to grow at a CAGR of 7.8% with premium domestic brands such as NITECORE and Fenix successfully competing on performance and quality against international peers.

- India: Infrastructure Surge and Rural Electrification Expanding Flashlight Demand

India represents one of the most compelling growth stories in the Asia Pacific flashlight market, accounting for approximately 12-14% of regional revenue and projected to grow at a CAGR of 9.5% between 2026 and 2033. The government's PM Gati Shakti National Master Plan and massive infrastructure investments under the National Infrastructure Pipeline (NIP) targeting US$ 1.4 Tn in investment through FY2025 are generating substantial industrial and construction sector demand for professional flashlights. Additionally, the Saubhagya Scheme's rural electrification mission, despite significant progress, still leaves approximately 30-40 million households reliant on portable off-grid lighting solutions, creating sustained rural demand, particularly for solar-powered and Rechargeable Battery Systems-based flashlights.

- South Korea: Advanced LED R&D and Defense Procurement Elevating Flashlight Standards

South Korea accounts for approximately 7-9% of the Asia Pacific flashlight market, occupying a strategically important position as a technology innovator and defense-grade flashlight consumer. South Korean companies, including global leaders in LED chip manufacturing such as Samsung LED and LG Innotek, supply advanced LED components that underpin performance improvements across the global flashlight industry. Domestically, the Republic of Korea Armed Forces and civil defense authorities represent significant institutional buyers of tactical flashlights.

Competitive Landscape

The global flashlight market exhibits a moderately fragmented competitive structure, with a mix of established multinational brands, specialized professional lighting manufacturers, and a large base of Asian OEM producers. Leading players pursue differentiation through LED Beam Technology innovation, ATEX and mil-spec certifications, and premium materials such as aerospace aluminum. Strategic partnerships with e-commerce platforms, notably Amazon, have become critical for DTC market penetration.

R&D investment is increasingly focused on smart flashlight features, including USB-C rechargeable systems, Bluetooth connectivity, and adaptive lumen output technology, while sustainability-driven product lines (rechargeable, solar) are emerging as key competitive differentiators among environmentally conscious consumer segments.

Key Developments:

- In January 2026, Streamlight launched the PolyTac® 1X, a compact multi-fuel tactical flashlight designed for professional-grade performance across diverse operational environments.

- In August 2025, Olight unveiled its flagship ArkPro Series EDC flashlights in New York and showcased the lineup at IFA Berlin 2025, marking the company’s first participation in Europe’s largest consumer electronics exhibition.

- In March 2025, Fenix introduced the PD45R ACE multi-mode tactical flashlight featuring customizable controls, military-grade durability, and advanced operational modes for professional and tactical applications.

- In late 2025, Olight officially opened orders for its ArkPro EDC flashlight series following earlier production delays, after demonstrating multiple units at IFA Berlin 2025.

- February 2024: Streamlight, Inc. launched the ProTac HL-X USB series, incorporating dual-fuel capability and USB-C direct charge, targeting law enforcement and military procurement channels in North America and Europe.

- September 2024: NITECORE introduced the P series of compact tactical flashlights with AI-adaptive brightness control, achieving over 3,000 lumens in a pocket-sized format, reflecting the intensifying arms race in High Lumen Output performance.

- March 2023: Fenix Lighting announced expanded production capacity at its Shenzhen facility to meet surging global demand for rechargeable outdoor flashlights, with exports to over 150 countries reported in its 2023 product catalog.

Companies Covered in Flashlight Market

- Streamlight, Inc.

- SureFire, LLC

- Fenix Lighting Co., Ltd.

- NITECORE (Sysmax Innovations Co., Ltd.)

- Pelican Products, Inc.

- Coast Products

- Black Diamond Equipment Ltd.

- Princeton Tec

- Energizer Holdings, Inc.

- Panasonic Corporation

- Duracell (Berkshire Hathaway)

- Milwaukee Tool (Techtronic Industries)

- MAGLITE (Mag Instrument, Inc.)

- Ledlenser GmbH & Co. KG

- Petzl Company

- Olight Technology Co., Ltd.

- ThruNite Co., Ltd.

- Armytek Optoelectronics Inc.

- Nextorch Technology Co., Ltd.

- Klarus Lighting Technology Co., Ltd.

Frequently Asked Questions

The global flashlight market is valued at US$ 2.21 billion in 2026 and is projected to reach US$ 3.41 billion by 2033, registering a CAGR of 6.4% during the forecast period 2026 - 2033.

The key growth drivers include widespread adoption of LED Beam Technology delivering superior energy efficiency and High Lumen Output, rising emergency preparedness spending, regulatory phase-out of incandescent products, and expanding outdoor recreation participation globally.

LED Flashlights dominate the product type category, accounting for approximately 62% of the global flashlight market in 2026, driven by their energy efficiency, extended lifespan, compatibility with rechargeable battery systems, and declining component costs.

North America is the leading region, representing approximately 34% of global flashlight market revenue in 2026, supported by strong demand from emergency preparedness, law enforcement, outdoor recreation, and defense procurement channels, with the U.S. being the dominant country.

The opportunity lies in developing markets across Asia Pacific and Sub-Saharan Africa, where an estimated 675 million people lack reliable electricity access per the IEA, creating immense demand for solar-powered and Rechargeable Battery Systems-based flashlights tailored to off-grid communities.

The leading companies in the global flashlight market include Streamlight, Inc., SureFire, LLC, Fenix Lighting Co., Ltd., NITECORE, Pelican Products, Inc., Black Diamond Equipment, Ledlenser GmbH & Co. KG, Olight Technology Co., Ltd., MAGLITE, and Milwaukee Tool, among others.