- Healthcare Services

- Fill-finish Pharmaceutical Contract Manufacturing Market

Fill-finish Pharmaceutical Contract Manufacturing Market Size, Share, and Growth Forecast 2026-2033

Fill-finish Pharmaceutical Contract Manufacturing Market by Service Type (Aseptic Fill-Finish, Terminal Sterilization, Lyophilization [Freeze-Drying], Blow-Fill-Seal [BFS], Visual Inspection and Quality Control, and Labeling and Secondary Packaging), Packaging Format (Vials, Prefilled Syringes, Cartridges, Ampoules, and Others), End-user, and Regional Analysis, 2026–2033

Fill-finish Pharmaceutical Contract Manufacturing Market Size and Trend Analysis

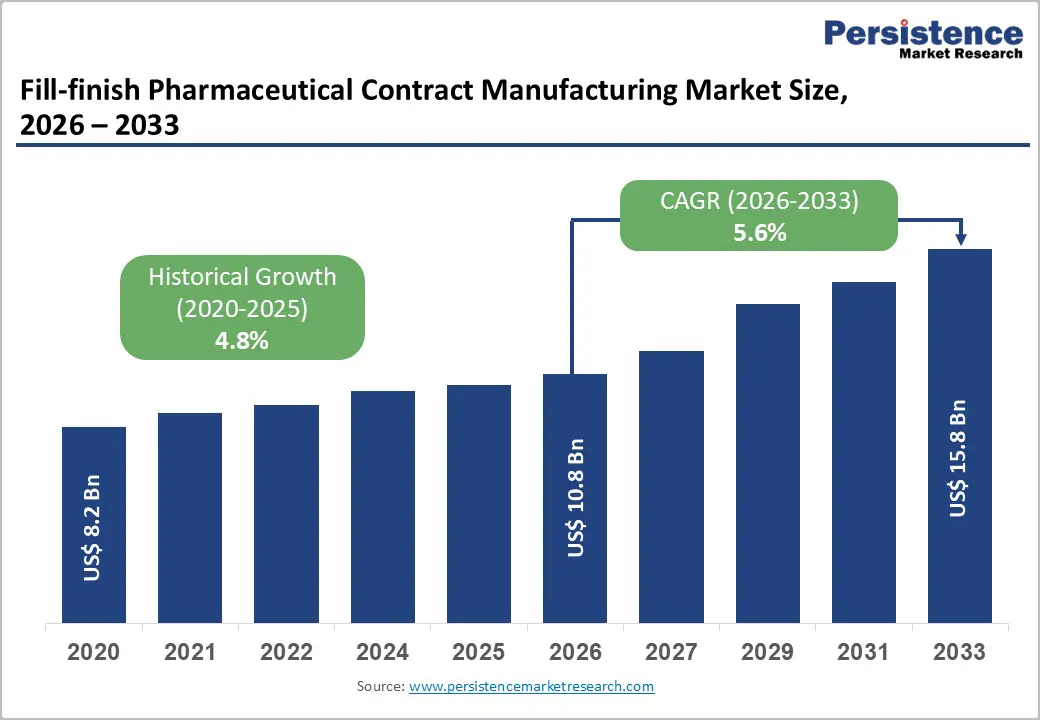

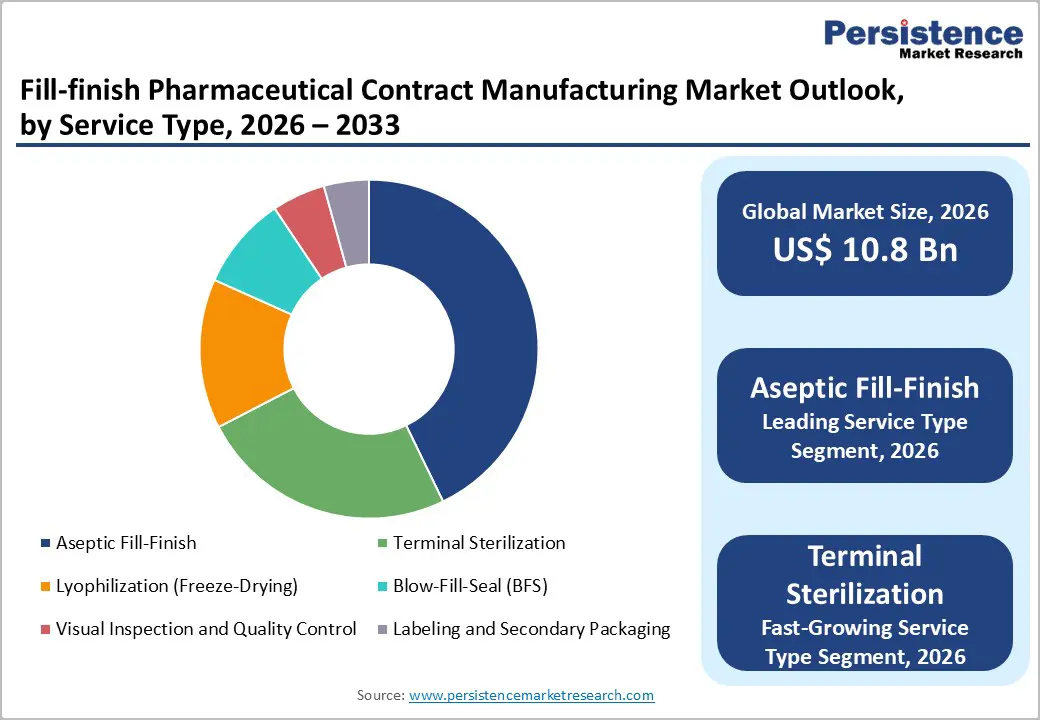

The global fill-finish pharmaceutical contract manufacturing market size is expected to be valued at US$ 10.8 billion in 2026 and projected to reach US$ 15.8 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

This steady and supported growth is primarily driven by the pharmaceutical and biopharmaceutical industry's accelerating shift toward outsourced manufacturing, rising demand for injectable drug formats, and the rapid proliferation of biologics, biosimilars, and advanced therapy medicinal products (ATMPs) all of which require specialized fill-finish capabilities that many sponsor companies choose to contract out rather than build in-house.

The Pharmaceutical Research and Manufacturers of America (PhRMA) reported that biopharmaceutical companies invested over US$ 102 billion in R&D in 2022, continuously expanding the pipeline of injectable drugs requiring fill-finish services. Capacity expansions by leading CDMOs, including Catalent, Lonza, and Vetter and tightening regulatory standards governing sterile manufacturing globally are further reinforcing the market's durable growth trajectory through 2033.

Key Industry Highlights

- Leading Region: North America: North America is likely to command approximately 47% of global share in 2026, anchored by the U.S.'s world-leading FDA-regulated sterile drug manufacturing ecosystem and dominant CDMOs including Catalent, Thermo Fisher Scientific, and Baxter BioPharma Solutions.

- Fast-Growing Market: Asia Pacific: Asia Pacific is the fast-growing regional market driven by Samsung Biologics' and WuXi Biologics' global capacity expansion, India's PLI Scheme pharmaceutical infrastructure investment, and Singapore's EDB-supported world-class fill-finish manufacturing cluster.

- Dominant Service Segment: Aseptic Fill-Finish: Aseptic fill-finish leads the service type category with approximately 43% share in 2026, driven by the biologic drug pipeline's mandatory requirement for ISO Class 5 Grade A sterile processing and persistent global capacity constraints sustaining premium CDMO pricing.

- Fast-Growing Segment: Terminal Sterilization: Terminal sterilization is the fast-growing service type benefiting from rising demand for cost-effective sterile small-molecule injectable manufacturing and expanding biosimilar pipelines where terminal sterilization is scientifically viable, reducing per-unit fill-finish costs.

- Key Opportunity: Prefilled syringe fill-finish capacity represents a high-value growth opportunity driven by self-administration biologic therapies (GLP-1 agonists, monoclonal antibodies) and FDA/EMA approvals of drug-device combination products commanding premium CDMO pricing and attracting major capacity investment from global leaders including Vetter and Simtra BioPharma Solutions.

Market Dynamics

Driver - Accelerating Biologics Pipeline and Increasing Preference for Injectable Drug Delivery

The global pharmaceutical pipeline has undergone a structural shift toward biologics, biosimilars, and gene therapies product categories that inherently require sterile injectable fill-finish manufacturing. According to the FDA's Center for Drug Evaluation and Research (CDER), novel biological drug approvals have consistently represented 30–40% of all new drug approvals annually in recent years.

The European Medicines Agency (EMA) has similarly seen biologics dominate its approval pipeline. Biologics require highly specialized aseptic fill-finish environments ISO Class 5 Grade A cleanrooms with validated contamination control systems capabilities that represent enormous capital investment, driving even large pharmaceutical manufacturers to contract fill-finish services to established CDMOs. The global biosimilars market is also generating substantial incremental fill-finish demand, as over 100 biosimilar products have been approved by the FDA since the pathway was established under the Biologics Price Competition and Innovation Act (BPCIA).

Pharmaceutical Outsourcing Trend Deepening as Drug Sponsors Optimize Capital Allocation

A well-established and deepening trend of pharmaceutical outsourcing is a primary structural driver of the fill-finish contract manufacturing market. Drug sponsor companies from large multinationals to emerging biotech firms are strategically choosing to outsource fill-finish operations to specialized CDMOs rather than invest in proprietary sterile manufacturing assets that require hundreds of millions of dollars in capital expenditure, continuous regulatory maintenance, and specialized workforce management.

According to online studies, the fill-finish pharmaceutical contract manufacturing services consistently rank among the top outsourced pharmaceutical manufacturing activities. This preference is particularly strong among small and mid-size biotech companies. The Biotechnology Innovation Organization (BIO) estimates there are over 5,000 biotech companies globally the vast majority of which lack dedicated fill-finish infrastructure and rely entirely on CDMO partners to commercialize injectable drug products.

Restraints - Significant Capital Investment and Long Lead Times for Capacity Expansion

Building or expanding fill-finish manufacturing capacity, particularly for sterile aseptic processing, requires capital investments ranging from US$ 100 million to over US$ 500 million per facility, depending on scale and technology sophistication. Facility construction, cleanroom qualification, equipment validation, and regulatory approval processes typically require three to five years from investment decision to commercial readiness.

This capital intensity creates cyclical supply-demand mismatches, as demonstrated during the COVID-19 pandemic when global fill-finish capacity was severely constrained. CDMOs face prolonged return on investment timelines that can constrain capacity expansion decision-making, limiting the industry's ability to rapidly respond to surges in outsourced fill-finish demand and creating temporary market access bottlenecks.

Regulatory Complexity and Evolving Compliance Standards Increasing Operational Burden

Fill-finish pharmaceutical manufacturing is subject to among the most stringent regulatory requirements in the entire pharmaceutical value chain. The FDA's 21 CFR Part 211 for Current Good Manufacturing Practice (cGMP), the EU GMP Annex 1 (substantially revised in 2023 with expanded contamination control strategy requirements), and ICH Q10 pharmaceutical quality system guidelines collectively impose extensive validation, documentation, and quality assurance obligations.

Regulatory inspections and the risk of FDA Warning Letters or EU GMP non-compliance findings impose significant compliance management costs. Any facility shutdown following a major regulatory action can disrupt client drug supply chains severely, adding operational risk that makes prospective CDMO partners subject to extremely rigorous qualification processes, extending sales cycles, and constraining market growth velocity.

Opportunities - Prefilled Syringe Format Growth Driven by Self-Administration and Biologic Drug Delivery Trends

Prefilled syringes represent the fastest-growing packaging format segment within the fill-finish pharmaceutical contract manufacturing market and constitute a compelling strategic growth opportunity. Patient preference for self-administration enabled by auto-injector device integration with prefilled syringes is driving sustained volume growth, particularly for subcutaneous biologic therapies including monoclonal antibodies, insulin analogs, and GLP-1 receptor agonists.

The FDA and EMA have approved a growing number of biologic therapies in prefilled syringe formats specifically to enable patient self-injection outside clinical settings. Major CDMOs, including Vetter Pharma-Fertigung GmbH, Catalent, and Simtra BioPharma Solutions, have made substantial investments in dedicated prefilled syringe fill-finish lines. With the global auto-injector device market growing in parallel and drug-device combination products representing an increasingly large share of injectable biologic submissions, prefilled syringe fill-finish capacity is among the most strategically sought-after CDMO capabilities by 2033.

Asia Pacific CDMO Capacity Expansion Unlocking Cost-Competitive Fill-Finish Manufacturing

Asia Pacific and particularly India, China, and South Korea presents exceptional growth opportunities for fill-finish pharmaceutical CDMO market participants, as the region scales world-class sterile manufacturing capacity at competitive cost structures. Samsung Biologics (South Korea) has become one of the world's largest biologics CDMOs, and WuXi Biologics (China) has aggressively expanded global fill-finish capacity.

In India, the government's Production Linked Incentive (PLI) Scheme for Pharmaceuticals has allocated INR 15,000 crore (approximately US$ 1.56 billion) to incentivize pharmaceutical manufacturing infrastructure, including sterile injectable facilities. India's Pharmaceuticals Export Promotion Council (Pharmexcil) reports that injectable exports have grown substantially, reflecting the country's rising fill-finish competency. As global drug sponsors seek to diversify supply chains beyond traditional Western CDMO networks, Asia Pacific CDMOs are increasingly positioned as high-quality, cost-competitive alternatives, creating substantial market growth opportunities.

Category-wise Analysis

Service Type Insights

Aseptic Fill-Finish is the dominant service type in the Fill-finish pharmaceutical contract manufacturing market, commanding approximately 43% of the total share in 2026. This leadership reflects the fundamental reality of the modern pharmaceutical pipeline: the majority of new molecular entities, particularly biologics, monoclonal antibodies, vaccines, and gene therapy vectors, are terminally heat-labile and cannot withstand terminal sterilization, making aseptic fill-finish the only viable manufacturing pathway.

Aseptic processing requires ISO Class 5 (Grade A) unidirectional airflow conditions and validated environmental monitoring programs, creating high barriers to entry that concentrate market share among established, capital-intensive CDMOs. According to the International Society for Pharmaceutical Engineering (ISPE), aseptic manufacturing capacity globally remains supply-constrained relative to the demand generated by the exploding biologic drug pipeline, sustaining premium pricing and high utilization rates for this service category.

Packaging Format Insights

Vials represent the leading packaging format segment in the Fill-finish Pharmaceutical Contract Manufacturing market, accounting for approximately 44% of total packaging format revenue in 2026. Vials' market leadership is rooted in their universal applicability across biologics, small molecules, vaccines, and lyophilized products, offering compatibility with both liquid and freeze-dried formats, broad material options (borosilicate glass, polymer), and a well-established global supply chain for components.

The COVID-19 pandemic dramatically reinforced vial dominance, as virtually all early-generation mRNA and adenoviral vector vaccines were filled into multi-dose glass vials by CDMOs including Catalent, Baxter BioPharma Solutions, and Thermo Fisher Scientific. Ongoing vial format innovation, including polymer vials with reduced breakage and extractables profiles and ready-to-use pre-sterilized vial systems is further strengthening the segment's position as the default primary packaging choice for injectable drug products globally.

End-user Insights

Biopharmaceutical companies are the leading end-user segment in the Fill-finish Pharmaceutical Contract Manufacturing market, accounting for approximately 46% of the total share in 2026. This dominance is structurally anchored in the biopharmaceutical sector's exceptional reliance on external fill-finish manufacturing. Biologic drugs require sterile aseptic processing capabilities that are highly capital-intensive, and many biopharmaceutical companies, from emerging clinical-stage biotechs to established mid-size innovators, lack proprietary fill-finish infrastructure.

The FDA approved a record 21 new biologic license applications (BLAs) in 2022 per CDER data, each requiring validated fill-finish manufacturing arrangements before commercial supply can begin. Large biopharmaceutical companies, including Amgen, Genentech (Roche), and AstraZeneca, actively use CDMO fill-finish services for capacity overflow, geographic supply chain diversification, and specialized format requirements, sustaining the segment's dominant revenue contribution.

Regional Insights

North America Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

North America is likely to account for approximately 47% of the global fill-finish pharmaceutical contract manufacturing market in 2026, driven by the United States and supported by Canada’s growing sterile injectable ecosystem. The region benefits from a high concentration of biologics and vaccine developers, robust venture capital funding, and advanced aseptic manufacturing infrastructure. Stringent oversight from the U.S. Food and Drug Administration and continued investments in prefilled syringes, cartridges, and lyophilization capabilities reinforce North America’s position as the largest outsourcing hub for commercial and clinical-stage fill-finish services.

U.S. Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

The U.S. represented nearly 41.8% of the global market in 2026 and remains the dominant contributor to regional revenue. The country hosts leading CDMOs such as Catalent, Thermo Fisher Scientific, and PCI Pharma Services. Strong biotech formation, BARDA-backed surge capacity agreements, and FDA requirements for contamination control strategies are accelerating investments in high-speed aseptic filling, isolators, and ready-to-use sterile packaging technologies.

Canada Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

Canada accounted for approximately 3.2% of the global market in 2026 and continues to strengthen its position through public and private investments in domestic biomanufacturing. GMP-certified facilities in Ontario and Québec are expanding vial and syringe filling capacity to support biologics, vaccines, and specialty injectables. Regulatory alignment with both the FDA and Health Canada makes Canada an increasingly attractive nearshore outsourcing destination for North American pharmaceutical and biotechnology companies.

Europe Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

Europe held an estimated 29.4% share of the global market in 2025, supported by world-class specialty CDMOs and the implementation of revised EU GMP Annex 1. The region is a global leader in prefilled syringes, cartridges, and lyophilized injectable manufacturing. Harmonized regulation through the European Medicines Agency and ongoing investments in advanced isolator-based facilities sustain Europe’s strong position in high-value outsourced fill-finish services.

Germany Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

Germany captured approximately 9.6% of the global share in 2026 and serves as Europe’s principal hub for high-precision aseptic manufacturing. The country is home to Vetter Pharma-Fertigung GmbH & Co. KG and Boehringer Ingelheim, both of which operate globally recognized sterile production campuses. Continued investment in isolator systems, robotics, and ready-to-use components supports Germany’s leadership in complex biologic and specialty injectable fill-finish.

Sweden Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

Sweden represented about 2.8% of the global share in 2025 and plays a strategic role in the European outsourced manufacturing landscape. Recipharm AB provides commercial-scale vial, syringe, and lyophilized product filling for multinational pharmaceutical companies. Sweden’s strong engineering capabilities, regulatory compliance culture, and focus on high-potency and niche injectable products continue to support steady market expansion.

Asia Pacific Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

Asia Pacific is likely to account for roughly 18.9% of the global share in 2026 and is projected to register the fastest CAGR of 11.8% in the coming years. Its growth is fueled by rapid capacity expansion in South Korea, China, and India, along with increasing regulatory harmonization with ICH standards. Competitive manufacturing economics and large-scale biologics investments are transforming the region into a preferred outsourcing destination for global pharmaceutical and biotechnology companies.

South Korea Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

South Korea is likely to register approximately 4.6% of the global market in 2026 and has emerged as one of the most technologically advanced fill-finish hubs in Asia. Samsung Biologics continues to expand integrated biologics and aseptic filling capacity, offering large-scale vial and prefilled syringe production. Strong government support and international regulatory compliance enhance the country’s appeal to multinational drug developers.

China Fill-finish Pharmaceutical Contract Manufacturing Market Trends and Insights

China accounted for nearly 5.4% of the global share in 2026 and is rapidly gaining share as domestic CDMOs scale globally compliant sterile manufacturing operations. WuXi Biologics has established advanced fill-finish facilities supporting global clinical and commercial supply. Alignment of the National Medical Products Administration with ICH guidelines has significantly increased international confidence in Chinese outsourcing capabilities.

Competitive Landscape

The global fill-finish pharmaceutical contract manufacturing market is moderately consolidated, with global leaders Catalent Inc., Lonza Group Ltd., Vetter Pharma-Fertigung GmbH & Co. KG, Recipharm AB, and Thermo Fisher Scientific collectively commanding substantial market share through world-class aseptic processing capabilities, multi-format fill-finish platforms, and established global regulatory agency relationships.

Key competitive differentiators include technology breadth (aseptic + lyophilization + BFS), geographic manufacturing network, regulatory track record, and integrated drug product development services. Emerging business trends include technology platform investments in isolator-based aseptic processing, continuous manufacturing integration, digital quality management systems, and strategic acquisitions of specialized fill-finish boutiques to expand service capabilities and geographic reach.

Key Developments:

- In November 2024, Lonza reported the successful completion of its inaugural GMP batch at the Portsmouth facility, thereby augmenting its capacity for small- to mid-scale mammalian biologics and improving support for diverse molecule types.

- In February 2024, Societal CDMO announced its acquisition by CoreRx for roughly USD 30 million, resulting in a strengthened CDMO with augmented capabilities in formulation development, production, and packaging services.

Contract Manufacturing Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 8.2 Bn |

|

Current Market Value (2026) |

US$ 10.8 Bn |

|

Projected Market Value (2033) |

US$ 15.8 Bn |

|

CAGR (2026-2033) |

5.6% |

|

Leading Region |

North America, 46% share |

|

Dominant Packaging Format |

Vials, 51.7% share |

|

Top-ranking Aseptic Fill-Finish |

Aseptic Fill-Finish, 42.8% |

|

Incremental Opportunity |

US$ 5.0 Bn |

Companies Covered in Fill-finish Pharmaceutical Contract Manufacturing Market

- Lonza Group Ltd

- Baxter BioPharma Solutions

- Recipharm AB

- Catalent, Inc.

- Societal CDMO, Inc.

- Symbiosis Pharmaceutical Services Ltd

- MabPlex International Co., Ltd.

- Fresenius Kabi USA, LLC

- Thermo Fisher Scientific Inc.

- Boehringer Ingelheim International GmbH

- Vetter Pharma-Fertigung GmbH & Co. KG

- Samsung Biologics Co., Ltd.

- Simtra BioPharma Solutions

- PCI Pharma Services

- Rentschler Biopharma SE

- Others

Frequently Asked Questions

The global fill-finish pharmaceutical contract manufacturing market is projected to be valued at US$ 10.8 billion in 2026, and is forecast to reach US$ 15.8 billion by 2033, expanding at a CAGR of 5.6% through the forecast period.

Rapid growth in biologics, biosimilars, and injectable therapies is increasing outsourcing demand for specialized aseptic fill-finish manufacturing capacity.

North America leads the global market with approximately 47% of total market share in 2025. The region's dominance is driven by the U.S.'s world-leading concentration of FDA-regulated sterile injectable manufacturing facilities, the presence of global CDMO leaders including Catalent, Thermo Fisher Scientific, and Baxter BioPharma Solutions, and BARDA-supported strategic fill-finish capacity investments for pandemic preparedness.

Expansion of high-value formats such as prefilled syringes, cartridges, and ready-to-use sterile systems presents significant growth opportunities for fill-finish contract manufacturers.

Leading market players include Catalent Inc., Lonza Group Ltd., Vetter Pharma-Fertigung GmbH & Co. KG, Recipharm AB, Thermo Fisher Scientific Inc., Baxter BioPharma Solutions, Boehringer Ingelheim International GmbH, Samsung Biologics Co. Ltd., Simtra BioPharma Solutions, Fresenius Kabi USA LLC, WuXi Biologics, Rentschler Biopharma SE, and PCI Pharma Services, competing on aseptic technology breadth, regulatory track record, and global manufacturing network.