- Food Ingredients & Additives

- Fermented Sweeteners Market

Fermented Sweeteners Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Fermented Sweeteners Market by Product Type (Fermented Honey, Fermented Maple Syrup, Fermented Agave Syrup, Fermented Coconut Sugar, and Others), Form (Liquid, Powder, and Granular), Application (Food & Beverages, Nutraceuticals, Cosmetics & Personal Care, Pharmaceuticals, and Others) Distribution Channel (Supermarkets, Convenience Stores, Specialty Stores, and Online Retail), and Regional Analysis from 2026 - 2033

Fermented Sweeteners Market Share and Trend Analysis

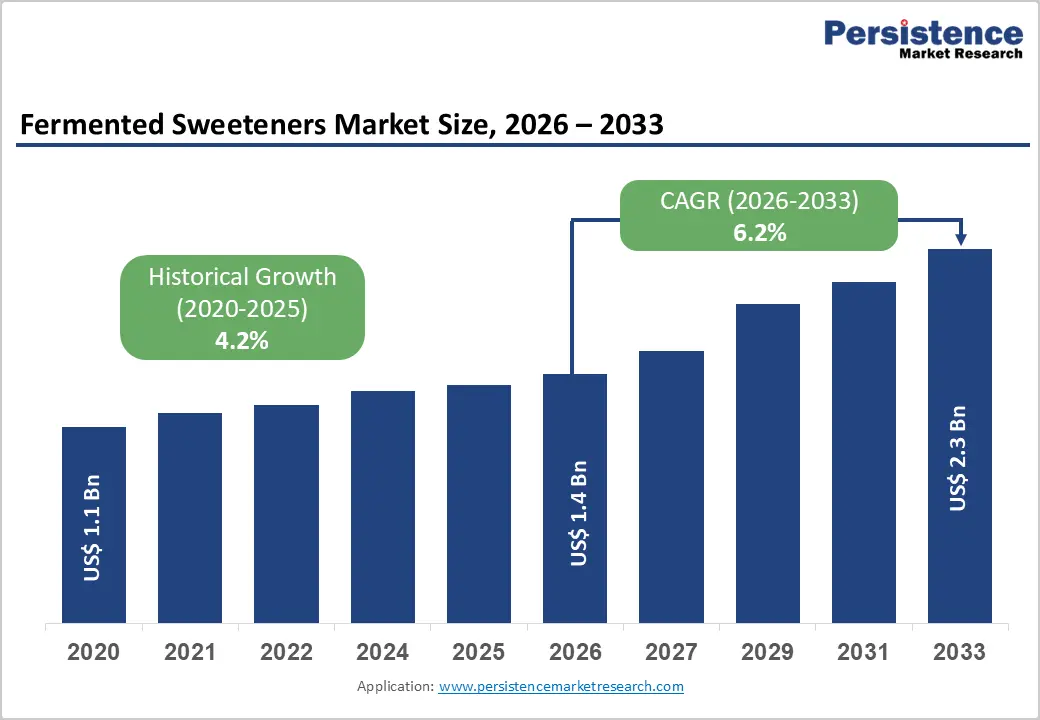

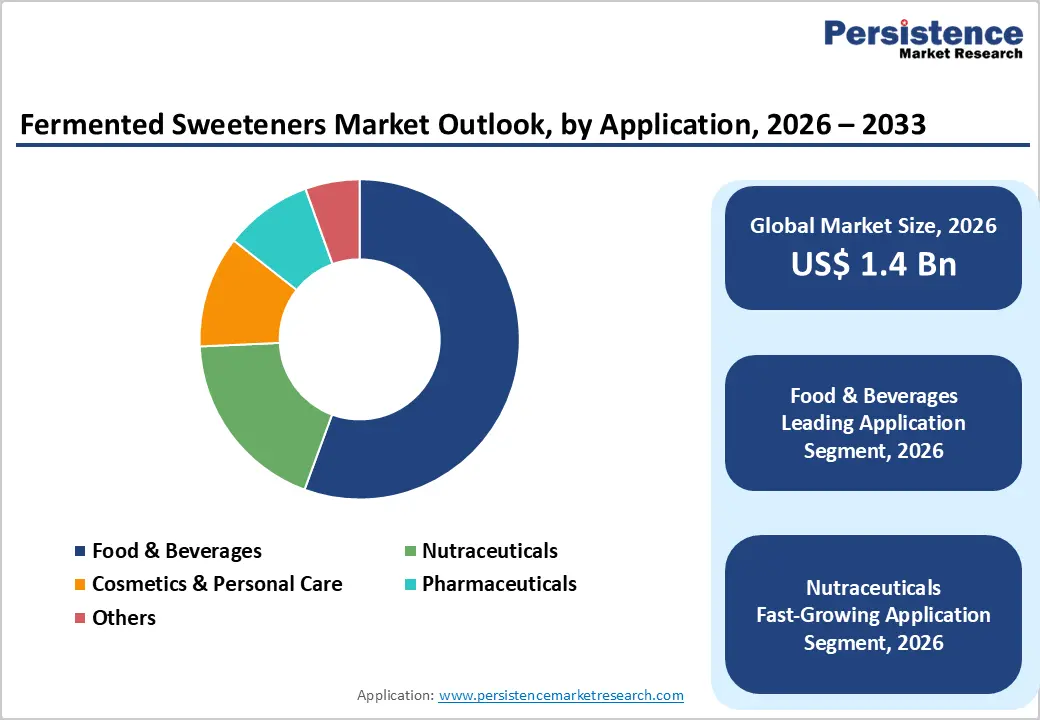

The global fermented sweeteners market size is estimated to grow from US$ 1.4 billion in 2026 to US$ 2.3 billion by 2033. It is projected to record a CAGR of 6.2% during the forecast period from 2026 to 2033.

Growing inclination toward naturally sourced and fermentation-derived sweetening solutions is significantly accelerating adoption across modern food systems. Consumers are increasingly moving away from refined sugar and synthetic additives, prompting manufacturers to integrate alternatives that align with clean-label expectations and perceived health benefits.

Key Industry Highlights:

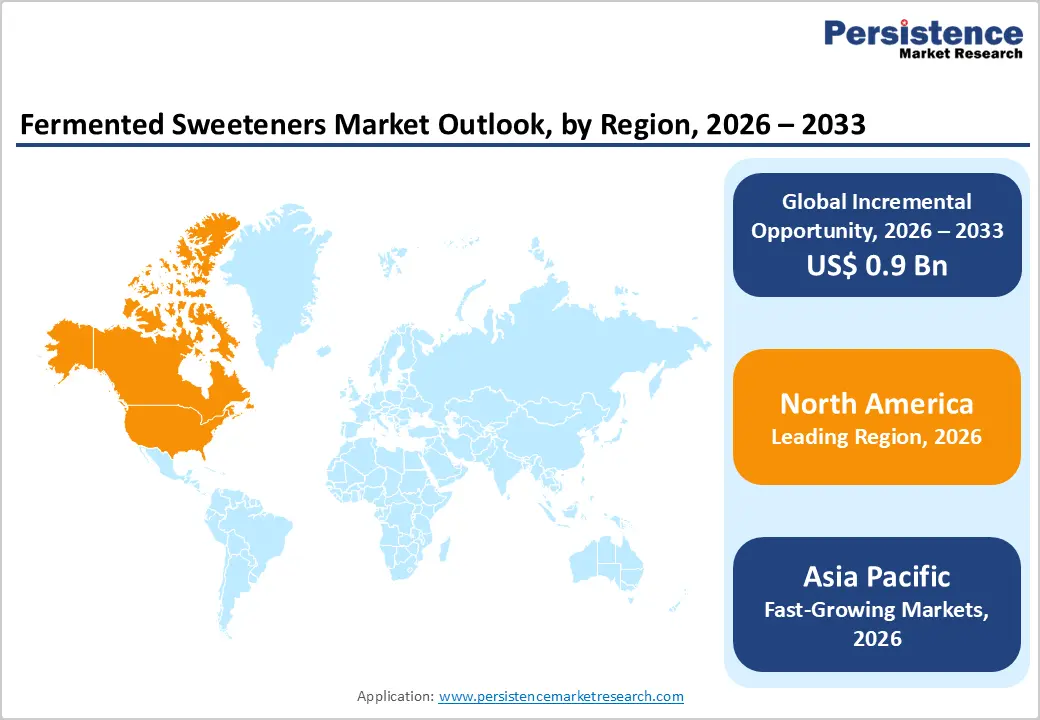

- Leading Region: North America holds 46.7% of the market, driven by strong demand for natural sweeteners, active product reformulation, and a mature food processing industry.

- Fastest-Growing Region: Asia Pacific is witnessing rapid expansion, supported by urbanization, rising disposable incomes, and increasing preference for healthier packaged foods.

- Leading Product Type Segment: Fermented honey dominates due to its wide availability, cost-effectiveness, and compatibility with large-scale food manufacturing.

- Fastest-Growing Product Type Segment: Fermented agave syrup is gaining traction as demand rises for plant-based, low-calorie, and premium sweetening solutions.

- Leading Application Segment: Food & beverages lead the market, supported by extensive use as a natural sugar substitute across diverse product categories.

- Fastest-Growing Application Segment: Nutraceuticals are expanding rapidly, driven by rising demand for functional ingredients with health benefits and clean-label appeal.

| Key Insights | Details |

|---|---|

|

Fermented Sweeteners Market Size (2026E) |

US$ 1.4 Bn |

|

Market Value Forecast (2033F) |

US$ 2.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Dynamics

Driver - Increasing Preference for Fermentation-Derived, Low-Calorie Sweeteners with Clean-Label Positioning

A major growth catalyst is the accelerating consumer shift toward naturally derived sweetening solutions that align with clean-label expectations and reduced sugar intake. Fermented sweeteners are gaining traction as they offer lower caloric content, improved digestibility, and in some cases, functional health benefits such as gut-friendly properties. This makes them particularly attractive across food and beverage applications where manufacturers aim to balance sweetness with nutritional value. The transition is strongly visible in segments such as functional beverages, dairy alternatives, and health-focused snacks, where ingredient transparency has become a decisive purchasing factor.

The regulatory pressures in developed markets are increasingly emphasizing sugar reduction and clearer labeling practices, indirectly encouraging the adoption of fermentation-based alternatives over synthetic sweeteners. These products often benefit from simpler ingredient declarations and a perception of being less processed.

Technological advancements in microbial fermentation are also improving yield efficiency, taste profiles, and scalability, allowing manufacturers to integrate these sweeteners without compromising product quality. Emerging economies are witnessing parallel trends, driven by rising health awareness and urban consumption patterns. Collectively, these factors are reinforcing the role of fermented sweeteners as a viable and scalable substitute for traditional sugar across global markets.

Restraints - Cost Pressures and Performance Variability in Complex Food Formulations

Despite growing adoption, several constraints continue to challenge widespread penetration, particularly in cost-sensitive markets. Fermented sweeteners generally involve more sophisticated production processes, including controlled microbial fermentation and downstream purification, which can elevate production costs compared to conventional sugar or corn-based syrups. For large-scale food manufacturers operating on tight margins, this cost differential can limit integration, especially in high-volume, low-cost product categories.

From a technical aspect, performance consistency remains another concern. Variability in sweetness intensity, aftertaste, and stability under different processing conditions can complicate formulation, particularly in applications requiring precise control over texture, moisture, and shelf life. Some fermented sweeteners may exhibit sensitivity to high temperatures or pH variations, impacting their usability in baked or processed products.

Achieving uniform quality across batches can be challenging due to differences in fermentation conditions and raw material inputs. Incorporating these ingredients often necessitates reformulation, additional testing, and process optimization, increasing both time and operational costs. Limited standardization across suppliers further adds complexity, making it difficult for manufacturers to ensure consistent product performance. These factors collectively act as barriers, particularly in highly standardized and price-driven segments of the food industry.

Opportunity - Expansion Potential Across Functional Nutrition, Premium Products, and High-Growth Emerging Markets

A significant opportunity lies in the rapid expansion of functional and health-oriented food categories, where fermented sweeteners are increasingly positioned as value-added ingredients. Their ability to provide sweetness alongside potential metabolic and digestive benefits makes them suitable for applications such as protein bars, dietary supplements, low-calorie beverages, and specialized nutrition products. As consumers actively seek alternatives that align with wellness goals, these ingredients are gaining prominence in product innovation pipelines.

Premiumization trends are further amplifying demand, particularly in organic, artisanal, and clean-label product segments. Brands are leveraging fermented sweeteners to differentiate offerings through improved ingredient quality, traceability, and sustainability credentials. In parallel, emerging markets present strong growth potential due to rising disposable incomes, urbanization, and evolving dietary preferences. Countries across Asia Pacific and Latin America are witnessing increased consumption of packaged and health-oriented foods, creating favorable conditions for adoption.

Advancements in fermentation technology, including precision fermentation and improved strain development, are enabling higher efficiency and cost optimization, supporting scalability. Moreover, sustainability considerations such as reduced dependence on traditional sugar crops and lower environmental impact are opening new avenues for innovation. These combined factors position fermented sweeteners as a high-potential segment with expanding applications across diverse global industries.

Category-wise Analysis

By Product Type, Fermented Honey Leads Owing to High Availability and Cost-Effective Large-Scale Utilization

Fermented honey is projected to remain the leading product segment in the global fermented sweeteners market in 2026, accounting for 34.8% of total revenue. Its dominance is supported by widespread raw material availability, relatively lower processing complexity, and strong compatibility with large-scale food production systems.

The ingredient is extensively utilized across bakery, beverages, and confectionery due to its balanced sweetness, natural positioning, and formulation stability. Compared to niche fermented sweeteners, it offers greater pricing flexibility, making it suitable for both premium and mass-market applications.

Additionally, its longer shelf stability and well-established supply chain infrastructure enhance its appeal among manufacturers. While plant-based alternatives such as agave are gaining momentum, fermented honey continues to dominate due to its scalability, consistent quality, and ability to meet high-volume global demand efficiently.

By Application, the Food & Beverages Segment Leads Based on High Preference as a Natural Sugar Substitute

The food & beverages segment is expected to hold 58.6% of the total market share in 2026, making it the primary application area. This dominance is driven by the increasing use of fermented sweeteners as natural substitutes for refined sugar across a wide range of products including bakery goods, dairy items, functional drinks, and processed foods. These sweeteners not only provide sweetness but also contribute to improved flavor complexity, texture, and product stability.

Growing consumer preference for clean-label and minimally processed ingredients has accelerated their adoption in reformulated food products. In comparison to pharmaceutical or cosmetic applications, the food industry demonstrates significantly higher consumption volumes. Additionally, manufacturers are leveraging fermented sweeteners to align with evolving nutritional trends such as low glycemic index and reduced-calorie diets, further reinforcing the segment’s leading position.

By Distribution Channel, Supermarkets & Hypermarkets Lead Supported by Strong Retail Presence and Accessibility

Supermarkets & hypermarkets are anticipated to account for 41.7% of the global market share in 2026, establishing them as the dominant distribution channel. Their leadership is attributed to strong retail infrastructure, high product visibility, and the ability to cater to diverse consumer segments. These outlets offer a wide assortment of fermented sweeteners, enabling direct comparison based on pricing, formulation, and certifications such as organic or non-GMO.

In-store promotions and strategic shelf placement further enhance product accessibility and consumer awareness. Moreover, established procurement systems and bulk purchasing capabilities strengthen supply chain efficiency. Although online retail is gaining traction due to convenience and expanding digital penetration, physical retail formats continue to generate higher sales volumes. Consumer trust, immediate product availability, and the growing presence of health-focused product sections within supermarkets collectively sustain their dominance.

Regional Insights

North America Fermented Sweeteners Market Trends

North America is projected to capture 46.7% of the global fermented sweeteners market in 2026, with the United States serving as the primary growth engine. The region’s leading position is driven by a highly developed food and beverage sector that is actively transitioning toward reduced-sugar formulations.

Manufacturers are increasingly incorporating fermented sweeteners to meet regulatory expectations and shifting consumer preferences toward natural and functional ingredients. Rising awareness regarding metabolic health, obesity, and clean eating habits has significantly influenced purchasing behavior, encouraging the adoption of alternatives perceived as healthier than conventional sugar.

Furthermore, the presence of well-established retail chains and efficient distribution networks ensures widespread product availability across both urban and semi-urban markets. Innovation remains a key differentiator, with companies introducing fortified, blended, and application-specific sweetener solutions to enhance product appeal.

The rapid expansion of plant-based and functional food categories further supports market penetration. Additionally, transparent labeling regulations and strong emphasis on ingredient traceability continue to encourage manufacturers to adopt fermented sweeteners, reinforcing sustained demand across the region.

Europe Fermented Sweeteners Market Trends

Europe represents a stable and mature market for fermented sweeteners, characterized by strong regulatory frameworks and high consumer awareness regarding food quality. Countries such as Germany, France, the United Kingdom, Spain, and the Netherlands are key contributors to regional demand. Strict regulations limiting artificial additives have accelerated the shift toward natural and fermentation-derived sweeteners, positioning them as viable alternatives in multiple food applications.

Consumers across the region exhibit a clear inclination toward organic, non-GMO, and ethically sourced products, compelling manufacturers to enhance transparency and adhere to stringent certification standards. Sustainability considerations, including environmentally responsible sourcing and packaging, are increasingly influencing purchasing decisions.

The food industry continues to integrate fermented sweeteners into premium and specialty product lines, particularly within bakery, confectionery, and health-focused segments. In addition, collaborations between ingredient suppliers and food manufacturers are fostering innovation and enabling the development of differentiated offerings. These factors collectively support consistent market expansion despite the region’s relatively mature status.

Asia Pacific Fermented Sweeteners Market Trends

Asia Pacific is expected to register the fastest growth, with a CAGR of approximately 8.4% during 2026–2033. The region’s rapid expansion is fueled by increasing urbanization, rising disposable incomes, and evolving dietary patterns favoring packaged and convenience foods. Major economies such as China and India are at the forefront of this growth, supported by a growing middle-class population and heightened awareness of healthier food alternatives.

The adoption of fermented sweeteners is increasing across both household consumption and industrial applications, particularly as consumers shift away from traditional high-calorie sweeteners. Expanding food processing industries and investments in domestic manufacturing capabilities are improving product accessibility and cost efficiency. In addition, the global food companies are strengthening their regional presence to capitalize on rising demand for natural and functional ingredients.

Government initiatives aimed at enhancing food quality standards and supporting local production further contribute to market development. The influence of Western dietary habits, combined with growing health consciousness, continues to drive long-term demand across diverse consumer groups in the region.

Competitive Landscape

The global fermented sweeteners market is highly competitive, with strong participation from Cargill, Incorporated, Archer Daniels Midland Company, Tereos, Ajinomoto Co., Inc., Ingredion Incorporated, and Jungbunzlauer Suisse AG. These companies leverage advanced fermentation technologies, clean-label formulation capabilities, and integrated sourcing networks to strengthen market positioning while enhancing sweetness profile, stability, and functionality across food and beverage applications.

Rising demand for natural, low-calorie sweeteners is accelerating innovation, with manufacturers expanding production capacity, improving traceability, ensuring regulatory compliance, and investing in R&D to develop functional fermented sweetener solutions.

Key Developments:

- In November 2025, Oobli introduced a novel natural sweetener derived from proteins rather than carbohydrates, marking a significant innovation in sugar alternatives. The product, designed to replicate the taste of sugar, is the first of its kind to achieve GRAS certification for commercial use, offering a promising solution to concerns around excessive sugar intake and related health issues such as obesity, diabetes, and cardiovascular diseases.

- In February 2025, Oobli, a pioneer in sweet protein platforms, announced a strategic partnership with Ingredion Incorporated to expand access to innovative and healthier sweetening solutions. Through this collaboration, the companies aim to combine natural sweeteners such as stevia with Oobli’s protein-based sweeteners to deliver cost-effective, great-tasting alternatives to sugar.

- In October 2024, NutraEx Food, Inc. introduced Bi-Sugar, a novel sweetening solution developed using its proprietary dry-embedding technology, which combines L-arabinose with conventional sugar and an additional natural sweetener, as stated by the company.

Companies Covered in Fermented Sweeteners Market

- Cargill, Incorporated

- Archer Daniels Midland Company

- Tereos

- Ajinomoto Co., Inc.

- Ingredion Incorporated

- Jungbunzlauer Suisse AG

- Gulshan Polyols Limited

- NOW Foods

- Wilmar Sugar Pty Ltd.

- Nantong Changhai Food Additive Co., Ltd.

- Vitasweet Co., Ltd.

- EvoNext Holdings SA

- Kerry Group plc

- Koninklijke DSM N.V.

- Roquette Frères

- Others

Frequently Asked Questions

The global fermented sweeteners market is projected to be valued at US$ 1.4 Bn in 2026.

Rising demand for clean-label, low-calorie, and plant-based sweeteners is driving the global fermented sweeteners market.

The global fermented sweeteners market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Expanding applications in nutraceuticals and functional foods, along with growing online retail penetration, present key market opportunities.