- Energy Storage Solutions

- Energy Storage Systems Market

Energy Storage Systems Market Size, Share, and Growth Forecast 2026 - 2033

Energy Storage Systems Market by Technology (Electrochemical/BESS, Mechanical, Thermal Energy Storage, Chemical, Electrical), Application (Grid-Scale Storage, Commercial & Industrial (C&I) Storage, Residential Storage, Renewable Energy Integration, Microgrids & Off-Grid Storage, Other Applications), and Regional Analysis, 2026 - 2033

Energy Storage Systems Market Size and Trend Analysis

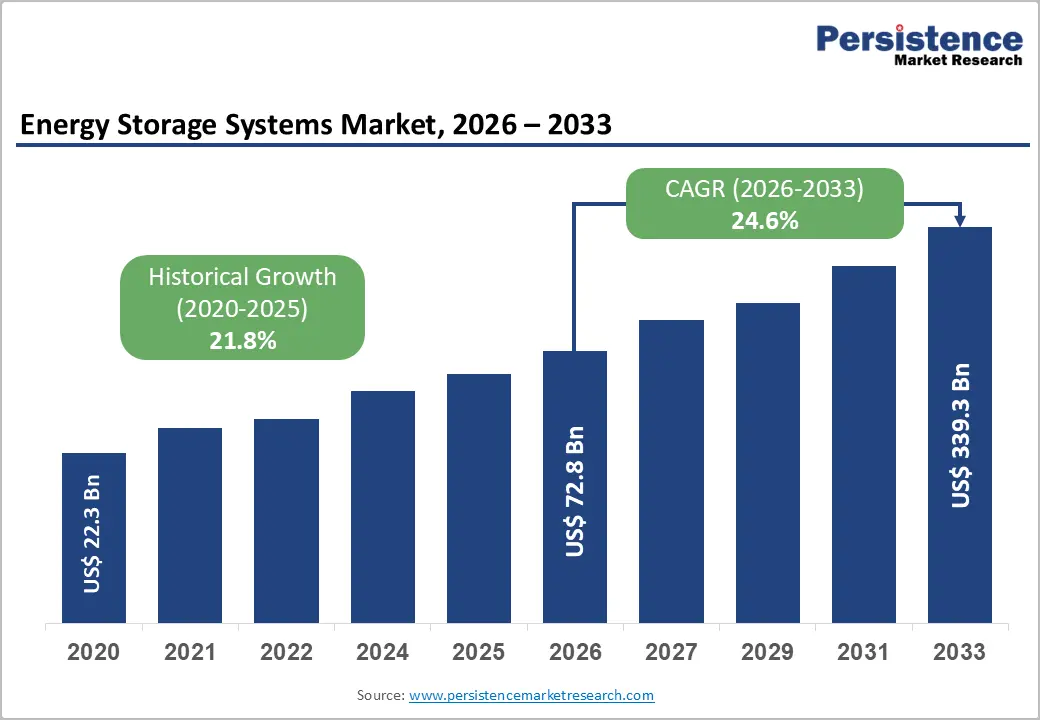

The global energy storage systems market size is expected to be valued at US$ 72.8 billion in 2026 and projected to reach US$ 330.1 billion by 2033, growing at a CAGR of 24.6% between 2026 and 2033.This trajectory is supported by the accelerating global energy transition, in which nations must balance intermittent renewable energy generation with grid reliability requirements.

The rapid deployment of utility-scale battery storage, evidenced by a 66% expansion in U.S. utility-scale battery capacity in 2024, surpassing 26 GW alongside landmark international commitments at COP28 to triple renewable capacity by 2030, is fundamentally reshaping power infrastructure investment priorities worldwide. Simultaneously, the sustained decline in lithium-ion battery pack costs, falling nearly 84% since 2013, continues to lower deployment barriers, unlocking new applications across grid, commercial, industrial, and residential segments.

Key Industry Highlights:

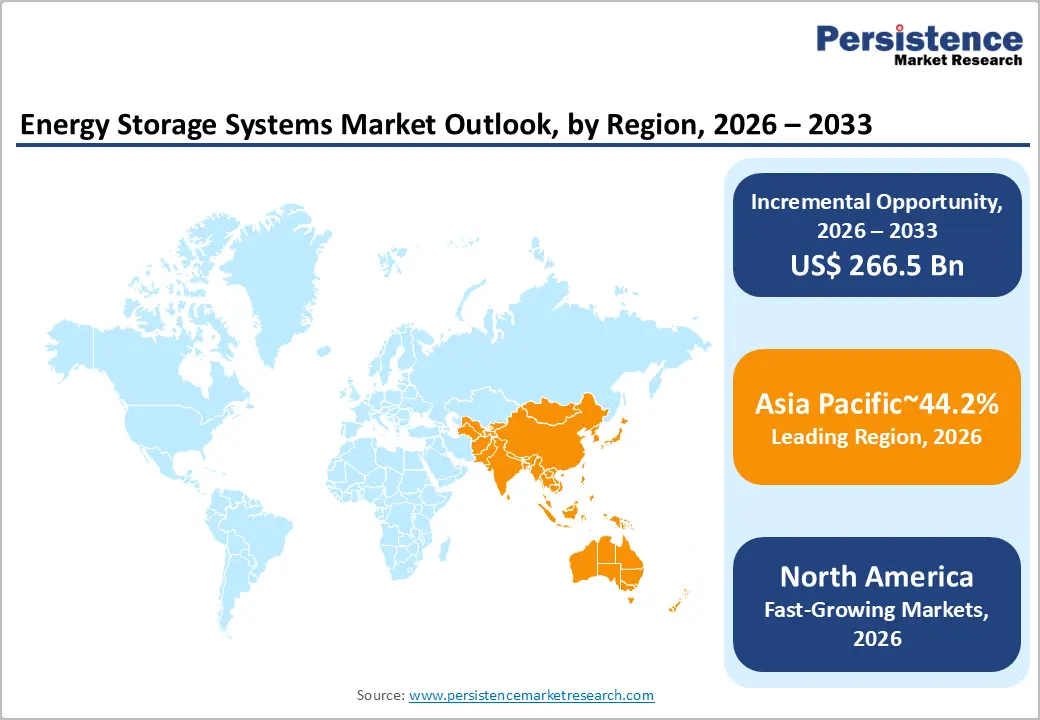

- Leading Region Asia: Asia Pacific dominates the global Energy Storage Systems market with a 44.2% share in 2026, led by China's 39.5 GW of cumulative user-side BESS installations through November 2025 and India's rapidly scaling policy-mandated storage market.

- Fast-Growing Market: Asia Pacific (India Driving Growth): India is the fastest growing major country market within Asia Pacific, propelled by CEA's projected 411 GWh storage requirement by FY2031-32 and its Energy Storage Obligation (ESO) mandate scaling to 4% by FY2030.

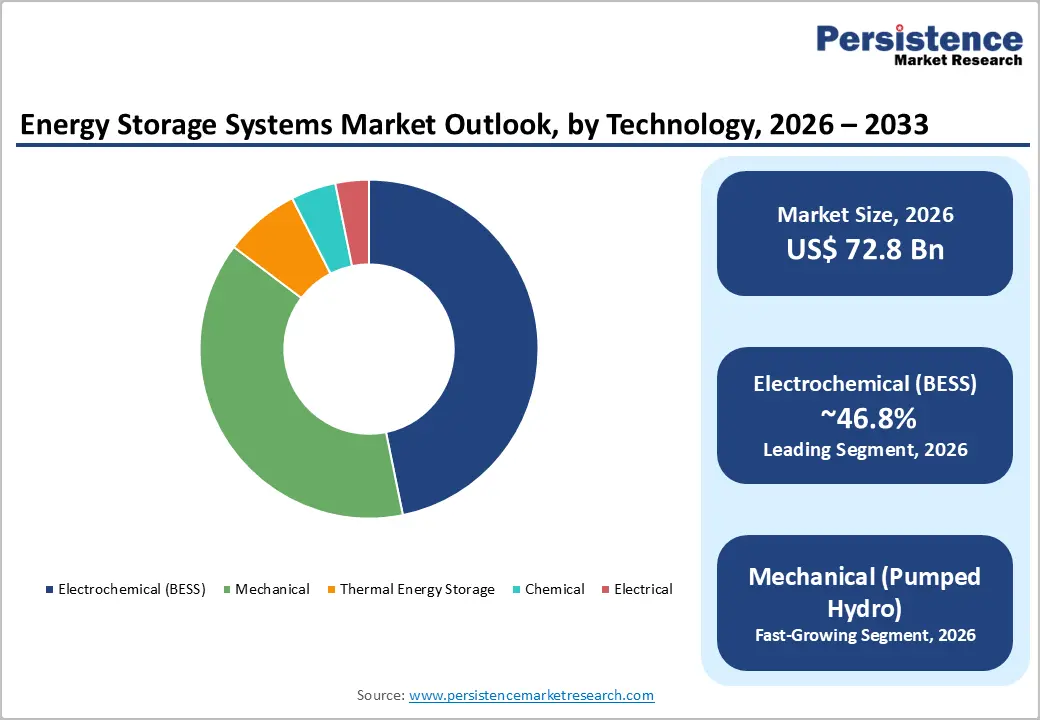

- Dominant Segment: Electrochemical storage holds approximately 47% technology market share in 2025, anchored by LFP battery dominance in both utility-scale and C&I applications globally, with continued cost reduction trajectories confirmed by U.S. DOE ATB 2024 data.

- Fast-Growing Segment: Dedicated storage for wind and solar integration is forecast at a 29.5% CAGR (2026 - 2033), the highest among all application segments, driven by global commitments to triple renewable capacity by 2030 per COP28 pledges and accelerating offshore wind pipelines.

- Key Opportunity: Long-duration storage (4-12+ hours) and service-based business models represent the most transformative near-term opportunity, with Mechanical storage (pumped hydro) forecast at 29% CAGR and innovative structures like ABB's BESS-as-a-Service unlocking large C&I addressable markets.

DRO Analysis

Drivers - Surge in Utility-Scale Battery Deployments Driven by Renewable Integration Mandates

Government mandates and power sector decarbonization goals are compelling utilities to invest heavily in grid-scale energy storage. In the United States alone, utility-scale battery storage capacity expanded by 66% in 2024, adding 10.4 GW of new installations. Forecasts from the U.S. Energy Information Administration (EIA) suggest another record-setting 19.6 GW of additions in 2025.

According to the International Energy Agency (IEA), more than 560 GW of renewable capacity was added globally in 2023, attracting USD 623 billion in new investments. As solar and wind penetration deepens, storage systems are indispensable for absorbing excess generation, managing grid frequency, and enabling 24/7 clean power delivery, creating substantial, durable demand across grid infrastructure globally.

Policy Frameworks and Economic Incentives Catalysing Private Investment

Policy-driven financial incentives are a primary catalyst for energy storage deployment. The U.S. Inflation Reduction Act (IRA), through the Investment Tax Credit (ITC) preserved under the One Big Beautiful Bill Act (OBBBA), offers meaningful CapEx reductions that unlock near-term project pipelines.

In Europe, the EU Net-Zero Industry Act and evolving state aid frameworks for storage flexibility are reshaping project economics across member states. India's Energy Storage Obligation (ESO) set to reach 4% by FY2030, is mandating storage procurement at scale. Collectively, these regulatory instruments are de-risking investment, attracting private capital, and accelerating the commercialisation of advanced storage technologies across diverse geographies and project typologies.

Restraints - Supply Chain Concentration and Critical Mineral Dependency

The energy storage supply chain remains heavily concentrated in China, which accounted for 60% of new global renewable capacity in 2023 and dominates lithium-ion battery cell manufacturing and critical mineral processing.

The IEA has documented nearly 200 restrictive trade measures introduced globally since 2020, while Foreign Entity of Concern (FEOC) regulations in the U.S. risk constraining future battery cell sourcing. This concentration creates systemic vulnerabilities, cost volatility, logistics disruptions, and geopolitical exposure that could impede project timelines and inflate system costs, particularly for markets seeking supply chain diversification.

High Upfront Capital Costs and Project Financing Barriers

Despite declining battery pack costs, the total installed cost of energy storage systems remains a substantial barrier, particularly for commercial & industrial (C&I) and residential segments. Long-duration storage technologies such as flow batteries and compressed air systems carry significantly higher capital expenditures than short-duration lithium-ion systems.

In developing economies, limited access to concessional financing, rising interest rates, and currency risk further constrain deployment, a challenge the IEA describes as a growing "climate debt trap". Permitting delays, land acquisition complexities, and grid interconnection queues add additional cost and schedule risk, collectively dampening the pace of commercial rollout across emerging market economies.

Opportunities - Long-Duration Energy Storage: The Next Frontier for Grid Decarbonization

The transition toward deeper renewable penetration is generating urgent demand for storage systems capable of discharging energy over 4 to 12 plus hours, well beyond the capabilities of conventional short-duration lithium-ion systems.

Technologies such as pumped hydro, flow batteries, and zinc-based systems, exemplified by Eos Energy's Z3 BESS and its partnership with Talen Energy to support AI data center infrastructure, are capturing this emerging segment. India's Central Electricity Authority (CEA) projects storage requirements of 411 GWh by FY2031-32 and 2,380 GWh by 2047 to achieve net-zero, creating a structurally large addressable market. As Mechanical storage (particularly pumped hydro) is forecast to record a 29% CAGR from 2026 to 2033, early movers in long-duration storage infrastructure stand to capture significant and durable project pipelines.

Service-Based Business Models Lowering Deployment Barriers for C&I Users

Innovative financing and service structures are transforming market access, particularly for commercial and industrial (C&I) users who face CapEx constraints. ABB's launch of its Battery Energy Storage Systems-as-a-Service (BESS-as-a-Service) model in May 2025 expanded through a strategic partnership with GridBeyond to integrate AI-driven energy optimisation and price forecasting, enabling zero-upfront-CapEx deployments with performance guarantees.

This "storage-as-a-service" paradigm, combining hardware, software, lifecycle management, and energy trading, fundamentally lowers adoption barriers. As Renewable Energy Integration applications are projected to record a 29.5% CAGR from 2026 to 2033 the fastest among all application segments, service-based models will be critical in channelling capital toward distributed, behind-the-meter deployments in commercial buildings, industrial facilities, and data centres globally.

Category-wise Analysis

Technology Insights

Electrochemical energy storage, primarily battery energy storage systems (BESS) commands the dominant position likely to register approximately 47% share in 2026. This leadership is anchored in the unmatched versatility of lithium-ion chemistry, particularly Lithium Iron Phosphate (LFP), which accounted for over 99% of installed power capacity in China's user-side market as of 2025.

Cost trajectories from the U.S. Department of Energy's Annual Technology Baseline (ATB) 2024 confirm continued $/kWh cost reductions across all innovation scenarios through 2050. BESS systems are now deployable across durations from 2 to 10 hours, enabling applications from residential behind-the-meter installations to utility-scale frequency regulation, cementing their technological primacy.

Application Insights

Grid-scale storage represents the largest application segment, capturing approximately 49% market share in 2026. The primacy of this segment reflects utilities' strategic prioritisation of large-capacity storage for frequency regulation, peak shaving, and renewable curtailment reduction. In the United States, utility-scale battery storage reached 26 GW in 2024, representing a 66% year-on-year expansion.

In Europe, 12 GW of energy storage was installed in 2024, with front-of-the-meter (FTM) grid-scale systems driving the majority of new capacity additions. India's National Electricity Plan (2023) by the Central Electricity Authority (CEA) projects storage capacity requirements rising to 82 GWh by 2026-27, providing a strong demand base for grid-scale deployments across emerging markets.

Regional Insights

North America Energy Storage Systems Market Trends and Insights

North America holds a 28.4% share of the global Energy Storage Systems market in 2025, anchored by aggressive U.S. federal policy support, record utility-scale procurement cycles, and a maturing residential storage segment.

The region's growth is propelled by the IRA's Investment Tax Credit, state-level procurement mandates across California, Texas, and New York, and surging data center power demand positioning North America as both a technology innovation hub and a high-volume deployment market through 2033.

U.S. Energy Storage Systems Market Size

The U.S. energy storage systems market is likely to be valued at approximately US$ 14.8 billion in 2026, driven by a 66% surge in utility-scale battery capacity to over 26 GW and a 132% year-on-year jump in residential storage installations.

The Q2 2025 quarterly record of 5.6 GW of new installations, with Texas, California, and Arizona each adding over 1 GW, underscores the U.S. market's structural momentum, supported by near-term certainty from the ITC preservation under the OBBBA and capacity expansion forecasts of 87.8 GW by 2029.

Europe Energy Storage Systems Market Trends and Insights

Europe holds a 19.6% share of the global Energy Storage Systems market in 2025, recording a landmark 12 GW of new storage installations in 2024 and reaching 89 GW of cumulative capacity. Growth is driven by EU decarbonization mandates, evolving state aid frameworks that require member states to create revenue-accessible markets for storage, and major project pipelines across the UK, Germany, and Italy. Deployment momentum is expected to accelerate sharply from 2027, supported by falling CapEx and EU-backed funding streams targeting high double-digit GW annual additions through 2030.

Germany Energy Storage Systems Market Size

Germany energy storage systems market is likely to be valued at approximately US$ 2.8 billion in 2025, underpinned by the Energiewende policy framework, a mature behind-the-meter residential solar-plus-storage segment, and industrial flexibility requirements driven by the phase-out of nuclear baseload.

Germany's advanced manufacturing sector creates sustained demand for C&I storage to manage peak tariffs and ensure operational resilience, with project-scale BESS deployments expanding as grid flexibility markets mature under evolving EU state aid rules.

U.K. Energy Storage Systems Market Size

The U.K. energy storage systems market size is likely to be valued at approximately US$ 2.1 billion in 2025, bolstered by the Capacity Market and Balancing Mechanism frameworks that provide material revenue streams for grid-scale BESS operators. The UK's ambition to achieve 100% clean power by 2030 under its Clean Power Action Plan is generating a robust pipeline of long-duration storage and frequency regulation projects, with the UK identified as one of Europe's leading markets for accelerated storage deployment post-2027.

France Energy Storage Systems Market Size

France energy storage systems market is supported by the French Multi-Year Energy Plan (PPE), which targets a 40% share of renewables in electricity generation, driving demand for grid balancing storage. France's high nuclear baseload historically limited storage adoption, but the accelerating deployment of offshore wind and solar is creating new ancillary services opportunities. The French market is estimated to account for approximately 16-18% of European energy storage capacity additions by 2033, supported by regulated flexibility tenders.

Asia Pacific Energy Storage Systems Market Trends and Insights

Asia Pacific holds the dominant position with a 44.2% share of the global Energy Storage Systems market in 2025. China is the single largest national market globally, with its LFP-dominated user-side new energy storage installations reaching a cumulative 39.5 GW in the first eleven months of 2025 a 28% increase year-on-year. India is emerging as the region's fastest-growing market, supported by government storage mandates, while Japan, South Korea, and Southeast Asian economies are building out grid modernisation and renewable integration storage capacity at scale.

China Energy Storage Systems Market Size

The China Energy Storage Systems market was valued at approximately US$ 14.5 billion in 2025, with Lithium Iron Phosphate (LFP) technology accounting for over 99% of installed power capacity. China accounted for 60% of new global renewable capacity in 2023, per the IEA, and its solar PV generation is projected to exceed total U.S. electricity demand by the early 2030s.

The country's strategic push toward long-duration storage technologies, including all-vanadium redox flow batteries for 8-hour commercial and industrial applications, signals a deliberate transition toward higher-value, extended-duration energy storage solutions across industrial and grid-scale segments.

India Energy Storage Systems Market Size

The India Energy Storage Systems market was valued at approximately US$ 3.0 billion in 2025, reflecting accelerating investment driven by the country's 2030 target of 50% non-fossil electricity capacity and a 45% reduction in emissions intensity.

The CEA's National Electricity Plan (2023) projects total storage needs rising from 82 GWh in FY2026-27 to 411 GWh by FY2031-32. India's first regulatory-approved grid-scale BESS, a 20 MW/40 MWh system commissioned by AmpereHour Energy for Indigrid and BRPL in Delhi, signals the market's transition from pilot to commercial-scale deployment.

Competitive Landscape

The global Energy Storage Systems market exhibits a moderately consolidated structure at the system integration and technology platform tier yet remains fragmented at the component and regional deployment level. Market leaders such as ABB, Tesla Energy, LG Energy Solution, BYD, CATL, and Fluence compete through vertical integration, proprietary software platforms (BMS, EMS, SCADA), and financing innovation.

Key differentiators include AI-driven energy optimisation, long-duration storage capabilities, safety certifications, and service-based deployment models. Emerging business models, particularly storage-as-a-service and virtual power plant (VPP) integrations, are reshaping competitive dynamics, enabling non-utility players to participate in ancillary services markets and accelerating behind-the-meter adoption in C&I and residential segments.

Key Developments:

- In May, 2025, ABB launched its Battery Energy Storage Systems-as-a-Service (BESS-as-a-Service) model, enabling commercial and industrial users to deploy advanced battery storage with zero upfront CapEx. This service-based offering supports clean energy adoption, provides performance guarantees, and integrates with energy trading to lower deployment barriers and accelerate intelligent ESS adoption across sectors.

- In May 2025, AmpereHour Energy commissioned India’s first regulatory-approved grid-scale Battery Energy Storage System (20 MW / 40 MWh) for Indigrid and BRPL in Delhi, marking a significant advancement in urban grid modernisation and intelligent clean energy storage. The turnkey BESS project integrates AI-driven energy management for peak shaving, backup power, and renewable integration, strengthening grid resilience and reducing fossil-fuel reliance in high-demand urban zones.

Companies Covered in Energy Storage Systems Market

- CATL

- BYD Co. Ltd.

- LG Energy Solution Ltd.

- Samsung SDI Co., Ltd.

- Fluence Energy Inc.

- Sungrow Power Supply Co.

- Panasonic Holdings Corp.

- LG Chem

- Toshiba Corporation

- Hitachi Energy India Ltd.

- Saft

- Siemens Energy India

- Tata Power Renewable Energy Ltd.

- GE Vernova / GENERAL ELECTRIC

- Showa Denko Materials Co., Ltd.

Frequently Asked Questions

The global energy storage systems market is estimated at US$ 72.8 billion in 2026.

The primary demand drivers are the global energy transition toward renewable power requiring grid balancing infrastructure, government policy mandates such as the U.S. IRA and India's Energy Storage Obligation (ESO), and dramatic cost reductions in lithium-ion battery technology, falling nearly 84% since 2013, which have made BESS economically viable across utility, commercial, and residential applications.

Asia Pacific leads the global Energy Storage Systems market with a 44.2% share in 2025. China is the dominant national market, with cumulative user-side BESS installations reaching 39.5 GW through November 2025, while India is the region's fastest-growing market, driven by CEA-mandated storage targets and the Energy Storage Obligation framework.

The most significant opportunities include long-duration energy storage systems (4-12+ hours), which address deep renewable integration requirements with Mechanical storage forecast at a 29% CAGR from 2026 to 2033 and service-based business models such as BESS-as-a-Service, pioneered by ABB and GridBeyond, that enable zero-CapEx deployments for commercial and industrial users.

Key market participants include ABB Ltd., Tesla Energy, LG Energy Solution, BYD Co. Ltd., CATL, Fluence Energy, Siemens Energy, GE Vernova, Hitachi Energy, and Others.