- Technology

- Embedded Intelligent Systems Market

Embedded Intelligent Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Embedded Intelligent Systems Market by Intelligence Capability (Rule-Based, AI-Enabled, Self-Learning Systems), Compute Location (Edge, Gateway, Cloud-Connected), Application (Automotive & Mobility, Others), and Regional Analysis for 2026 - 2033

Embedded Intelligent Systems Market Share and Trends Analysis

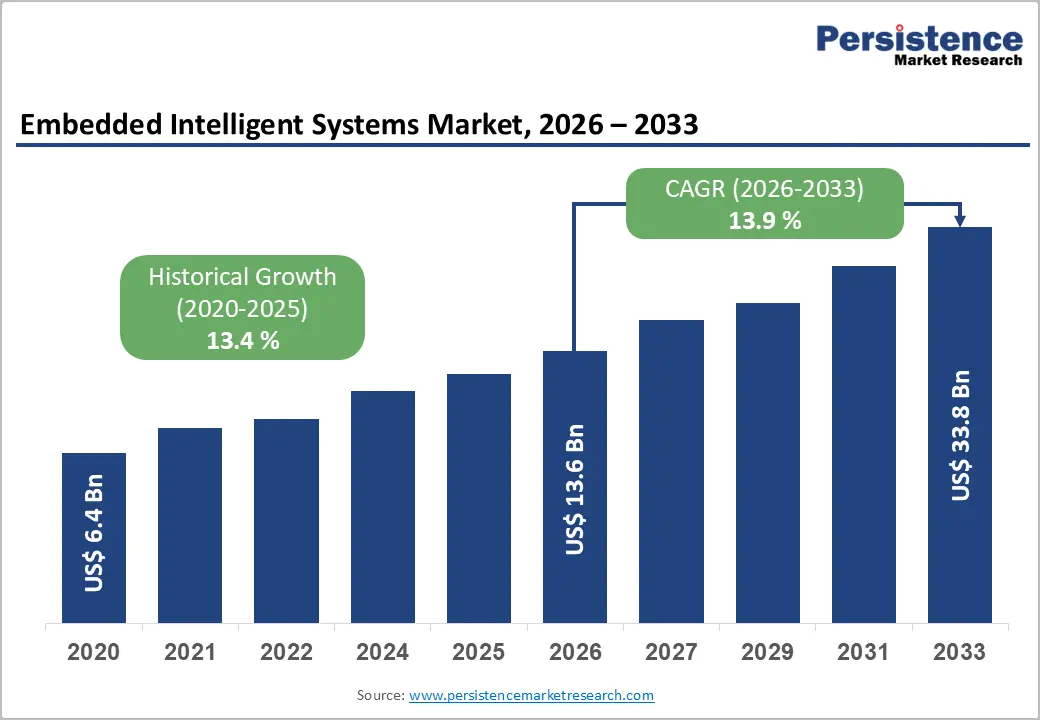

The global embedded intelligent systems market size is likely to be valued at US$13.6 billion in 2026 and is projected to reach US$33.8 billion by 2033, growing at a CAGR of 13.9% during the forecast period 2026 - 2033, driven by the rapid integration of AI-enabled embedded systems across automotive, industrial automation, and healthcare applications, alongside rising demand for edge computing capabilities.

Increasing adoption of real-time data processing, expansion of IoT ecosystems, and advancements in semiconductor technologies are accelerating deployment. Regulatory support for smart infrastructure and digital transformation initiatives further reinforces long-term market expansion.

Key Industry Highlights:

- Dominant Intelligence Capability: AI-enabled embedded systems are set to command around 50% of the revenue share in 2026, while self-learning systems are likely to grow the fastest at 14.1% CAGR through 2033, driven by rising demand for predictive and autonomous capabilities.

- Leading Compute Location: Edge embedded systems are expected to lead with an estimated 44% share in 2026, while cloud-connected systems are projected to be the fastest-growing at 14% CAGR during 2026 - 2033, supported by hybrid edge-cloud adoption.

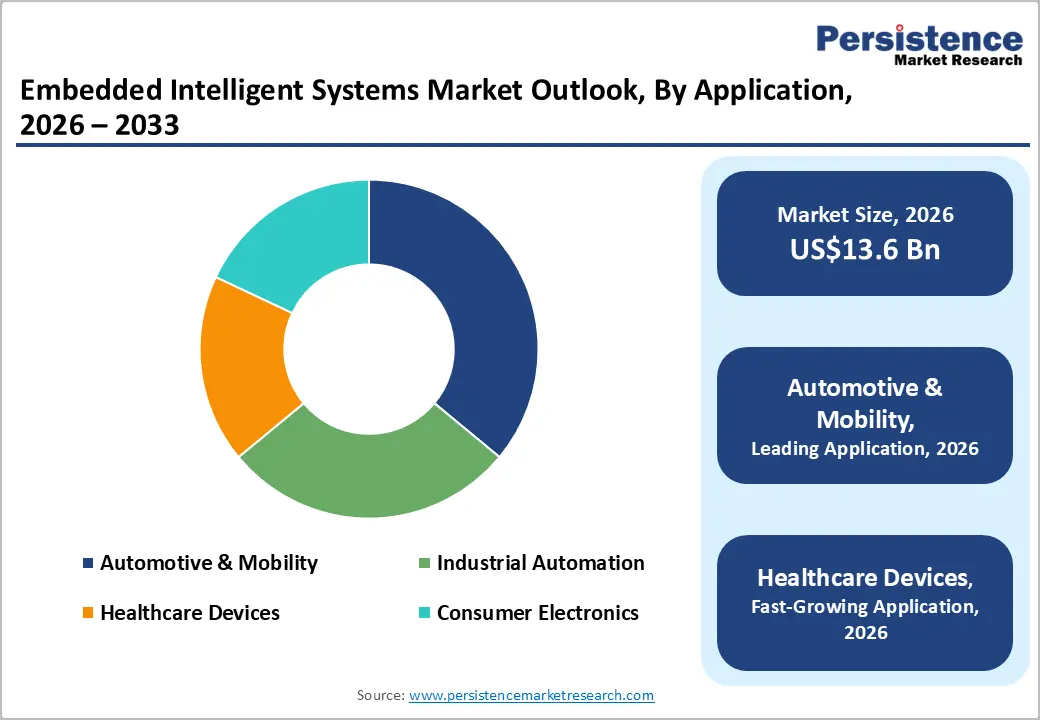

- Dominant Application Segment: Automotive & mobility is anticipated to hold about 36% share in 2026, while healthcare devices are likely to register the fastest growth at 14.3% CAGR through 2033, fueled by remote monitoring and AI diagnostics.

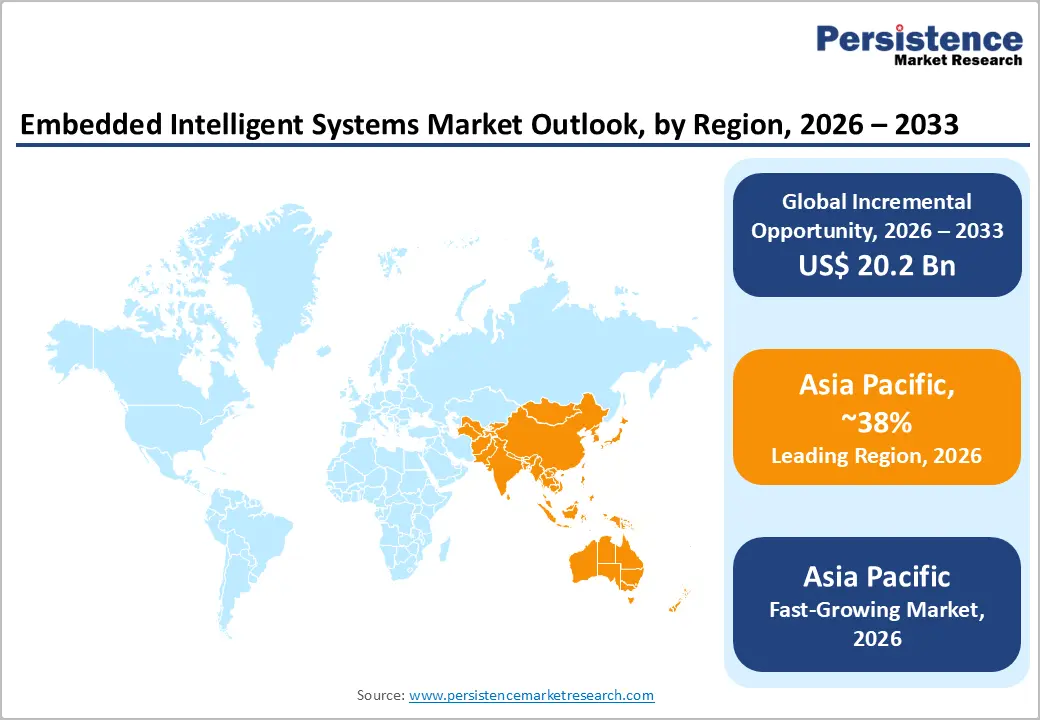

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 38% share in 2026 and grow at 14.5% CAGR through 2033, led by strong manufacturing and digital infrastructure investments.

- Competitive Environment: Competitive dynamics include AI-led innovation, edge computing expansion, and strategic partnerships, with players focusing on vertical integration and global market expansion.

DRO Analysis

Driver - Rising Adoption of AI-Enabled Edge Computing in Industrial and Automotive Systems

The proliferation of AI-enabled embedded systems at the edge is a key growth driver. According to data from OECD digital economy reports, over 50% of enterprise-generated data is expected to be processed at the edge by 2026, up from less than 20% in 2020.

In automotive, regulatory mandates such as advanced driver-assistance systems (ADAS) requirements across the U.S. and Europe have accelerated integration of embedded intelligence. Additionally, the International Energy Agency (IEA) highlights that connected and electric vehicles exceeded 40 million units globally in 2024, significantly increasing demand for embedded AI processors.

From a market impact perspective, the shift toward low-latency, real-time decision-making systems is transforming system architectures. Enterprises are prioritizing decentralized processing to reduce bandwidth costs and improve system responsiveness. This directly boosts demand for edge embedded systems, enabling scalable deployment across industrial automation and mobility ecosystems.

Restraint - High Development Costs and System Complexity Limiting Scalable Adoption

Rising demand for intelligent, real-time systems is pushing manufacturers to deliver advanced capabilities at scale. However, the transition toward self-learning embedded systems has significantly increased design complexity, requiring advanced chipsets, specialized software frameworks, and highly skilled engineering resources. Chip design costs have surged by over 30-40% in recent years due to process node advancements and R&D intensity, further amplified by semiconductor price increases linked to AI-driven demand and supply constraints.

This cost pressure is compounded by interoperability challenges across heterogeneous systems, which extend deployment timelines and elevate integration costs. Small and mid-sized enterprises face limited access to capital and technical expertise, restricting market entry. The need for customized hardware-software integration further reduces scalability, particularly in fragmented environments. As a result, adoption slows in cost-sensitive sectors such as consumer electronics and emerging markets, directly impacting speed-to-market and overall return on investment.

Opportunity - Expansion of Smart Healthcare and Remote Monitoring Systems Creating High-Value Growth Avenues

The healthcare industry is undergoing a structural shift toward digital-first and decentralized care delivery, accelerating demand for embedded intelligent systems in wearables, diagnostics, and remote monitoring. This transition is reinforced by accelerating digital health adoption post-pandemic, with remote patient monitoring projected to grow at over 20% annually through 2030. Large-scale deployments of AI-enabled telehealth platforms and hospital digitization initiatives across major economies are reinforcing real-time, data-driven care models.

The implementations of AI-enabled e-ICU command centers and government-backed digital health programs highlight how embedded intelligence is improving critical care response and early diagnosis capabilities. These advancements are extending into imaging systems, robotic surgery, and predictive diagnostics, enabling more precise and proactive treatment pathways. As healthcare infrastructure investments expand across Asia Pacific and North America, embedded intelligent systems are positioned for scalable adoption, unlocking sustained revenue opportunities and long-term value creation for solution providers.

Category-wise Analysis

Intelligence Capability Insights

AI-enabled embedded systems are estimated to dominate the market, accounting for approximately 50% share in 2026, driven by their ability to process complex datasets and support real-time decision-making across mission-critical environments. These systems are widely embedded in automotive safety stacks, industrial robotics, and smart consumer devices, where deterministic performance is critical. In 2025, BMW Group is estimated to have expanded AI-enabled embedded controller integration within its Neue Klasse EV platform, strengthening real-time perception and predictive driving functions across next-generation vehicle architectures.

Self-learning systems are estimated to be the fastest-growing segment, projected at a 14.1% CAGR through 2033, supported by adaptive learning algorithms and continuous feedback-loop optimization. Their adoption is expanding in industrial automation and predictive maintenance environments. Siemens is estimated to have scaled autonomous optimization capabilities at its Amberg facility in Germany, enabling embedded production systems to self-adjust machine parameters based on defect detection patterns and throughput variation, improving operational efficiency and reducing downtime.

Compute Location Insights

Edge embedded systems are estimated to lead the market with approximately 44% share in 2026, driven by demand for real-time processing and localized intelligence. They are widely deployed in automotive ADAS, robotics, and industrial control systems where latency-sensitive decision-making is critical. In 2025, Barcelona City Council is estimated to have expanded its smart mobility infrastructure under its urban digitalization program, deploying edge-based roadside sensors and adaptive traffic systems to optimize congestion management and emergency routing efficiency.

Cloud-connected embedded systems are estimated to be the fastest-growing segment at a projected 14% CAGR through 2033, driven by centralized analytics, OTA updates, and AI model training requirements. In 2026, Amazon is estimated to have expanded cloud-integrated robotics orchestration across its fulfillment network, enabling real-time coordination between embedded robotic fleets and centralized cloud intelligence systems for inventory routing and dynamic task allocation optimization.

Application Insights

The automotive & mobility segment is estimated to lead the market with approximately 36% share in 2026, supported by EV adoption, ADAS integration, and connected vehicle platforms. Embedded intelligence is central to perception, control, and autonomous navigation functions. In 2025, Hyundai Motor Group is estimated to have advanced its E-GMP platform architecture with centralized domain controllers, integrating safety, infotainment, and driving assistance functions into a unified embedded computing system across its Ioniq EV lineup.

Healthcare devices are estimated to be the fastest-growing segment, projected at a 14.3% CAGR through 2033, driven by wearable diagnostics and remote patient monitoring systems. The UK National Health Service is estimated to have expanded its remote cardiac monitoring program across selected NHS Trust hospitals in London and Manchester, deploying wearable ECG patch devices integrated with embedded analytics for continuous arrhythmia detection and early intervention alerts, improving outpatient monitoring efficiency.

Regional Insights

North America Embedded Intelligent Systems Market Trends

North America is estimated to account for approximately 32% share of the global embedded intelligent systems market in 2026, driven by early AI adoption, strong semiconductor capability, and large-scale deployment of edge computing infrastructure. The region is characterized by high penetration of embedded intelligence in mobility systems, industrial automation, and defense-grade applications. The expansion of federal smart infrastructure modernization programs in the U.S. has accelerated deployment of AI-enabled embedded sensing systems across transportation corridors and public safety networks, strengthening demand for real-time edge intelligence.

U.S. Embedded Intelligent Systems Market Trends

The U.S. holding an estimated 45% share of North America, continues to lead due to rapid commercialization of AI-integrated embedded platforms. In 2025, Tesla expanded its Full Self-Driving (FSD) embedded compute stack across upgraded vehicle models, improving onboard real-time decision-making through enhanced neural processing units. Industrial automation upgrades across semiconductor fabrication facilities in Arizona have also increased adoption of embedded AI for predictive equipment maintenance and yield optimization.

Canada Embedded Intelligent Systems Market Trends

Canada, contributing an estimated 12% share within the region, is steadily advancing embedded intelligence adoption in healthcare and smart infrastructure. In 2025, Ontario expanded its smart grid modernization initiative, integrating embedded IoT controllers for real-time energy balancing and outage prediction across urban distribution networks. This reflects Canada’s increasing focus on embedding intelligence into public infrastructure and energy systems to improve operational resilience.

Europe Embedded Intelligent Systems Market Trends

Europe is estimated to hold approximately 27% share of the global embedded intelligent systems market in 2026, supported by strong industrial automation, regulatory-driven AI adoption, and sustainability-focused digital transformation. The region emphasizes energy-efficient embedded systems, ethical AI deployment, and standardized industrial interoperability. In 2025-2026, the European Union expanded funding under its digital infrastructure acceleration programs, promoting large-scale deployment of edge-based embedded systems in manufacturing and mobility ecosystems.

Germany Embedded Intelligent Systems Market Trends

Germany, accounting for approximately 30% share within Europe, leads the region through advanced industrial automation and automotive innovation. In 2025, Bosch and Continental integrated next-generation embedded AI control units into electric vehicle platforms to enhance real-time sensor fusion and driving assistance systems. German industrial firms also expanded deployment of embedded predictive maintenance systems in smart factories across Bavaria, improving production uptime and equipment efficiency.

U.K. Embedded Intelligent Systems Market Trends

The U.K., with an estimated 16% share within Europe, is witnessing strong momentum in healthcare and financial technology applications. In 2025-2026, the U.K. government expanded NHS digital transformation initiatives by deploying embedded remote patient monitoring systems across hospital networks in Scotland and Northern England, improving early detection of chronic conditions. Parallel investments in AI research hubs in Cambridge and London have further strengthened embedded system innovation in healthcare diagnostics and edge analytics.

Asia Pacific Embedded Intelligent Systems Market Trends

Asia Pacific is estimated to dominate the global market with approximately 38% share in 2026, making it the fastest-expanding regional hub for embedded intelligent systems. The region benefits from large-scale electronics manufacturing, rapid urban digitalization, and strong government-backed AI and semiconductor investment programs. The national-level smart city expansions and industrial automation upgrades across key economies have significantly accelerated embedded intelligence deployment.

China Embedded Intelligent Systems Market Trends

China, accounting for an estimated 45% share within Asia Pacific in 2026, leads large-scale implementation of embedded AI systems across mobility, surveillance, and industrial automation. In 2025, Shanghai expanded its AI-enabled urban mobility network by deploying embedded edge controllers across traffic junctions to optimize congestion flow and emergency routing. Additionally, Chinese semiconductor manufacturers increased production of AI-focused embedded chips to support domestic industrial automation demand.

India Embedded Intelligent Systems Market Trends

India, contributing an estimated 12% share within Asia Pacific, is emerging as a fast-growing hub for embedded systems development and deployment. India expanded its national smart manufacturing program, integrating embedded IoT controllers across automotive component plants in Tamil Nadu and Maharashtra to improve production efficiency and quality control. The growing investments in electronics manufacturing clusters and AI-driven startups are further strengthening India’s embedded intelligence ecosystem.

Competitive Landscape

The global embedded intelligent systems market is moderately consolidated, with key players such as NVIDIA, Intel, Qualcomm, Texas Instruments, and STMicroelectronics accounting for an estimated 50% share in 2026. These companies lead through strong semiconductor portfolios and advanced AI-enabled embedded platforms across automotive, industrial, and edge computing applications. Their dominance is supported by continuous R&D in edge AI processors, high-performance computing, and long-term OEM integration. Strong ecosystem control and hardware-software convergence further reinforce their leadership position.

Specialized firms such as NXP Semiconductors, Renesas Electronics, Infineon Technologies, and Microchip Technology maintain strong positions in automotive and industrial embedded systems. The increasing partnerships between chipmakers and cloud/AI ecosystem providers are enabling hybrid edge-cloud architectures. However, high R&D costs, fabrication complexity, and ecosystem lock-in continue to limit new entrants. The market is expected to consolidate further through acquisitions and strategic collaborations focused on AI and edge computing expansion.

Key Industry Developments:

- In October 2025, Arm extended its Flexible Access program to include Armv9 edge AI IP, including Ethos-U85 NPU and Cortex-A320 CPU, enabling startups to access advanced embedded AI tools with low upfront cost and pay-at-tape-out licensing. This is estimated to accelerate edge AI and embedded system innovation by reducing design entry barriers for startups.

- In October 2025, Qualcomm partnered with HUMAIN to deploy 200MW AI infrastructure starting 2026 using AI200/AI250 systems to build a hybrid edge-to-cloud AI ecosystem. This is expected to scale embedded AI inference and edge computing capacity, strengthening large-scale real-time AI deployment infrastructure.

Companies Covered in Embedded Intelligent Systems Market

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Technologies, Inc.

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Infineon Technologies AG

- Analog Devices, Inc.

- Microchip Technology Inc.

- Broadcom Inc.

- Arm Holdings plc

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

Frequently Asked Questions

The global embedded intelligent systems market is projected to reach US$13.6 billion in 2026.

The embedded intelligent systems market grows due to rising adoption of AI-enabled embedded systems, expansion of edge computing, and increasing demand for real-time automation.

The embedded intelligent systems market is expected to grow at a 13.9% CAGR from 2026 to 2033.

Key opportunities include expansion of autonomous mobility systems, smart healthcare devices, and cloud-edge hybrid architectures.

Key players include NVIDIA, Intel, Qualcomm, Texas Instruments, STMicroelectronics, NXP Semiconductors, and Renesas Electronics.