- Medical Devices

- Dermatology Imaging Market

Dermatology Imaging Market Size, Share, and Growth Forecast, 2026 - 2033

Dermatology Imaging Market by Modality (Dermatoscopes, Optical Coherence Tomography (OCT), High-frequency ultrasound, Others), Application (Inflammatory Dermatoses, Skin Cancer, Psoriasis, Others), End-User (Hospitals, Others), and Regional Analysis for 2026 - 2033

Dermatology Imaging Market Share and Trends Analysis

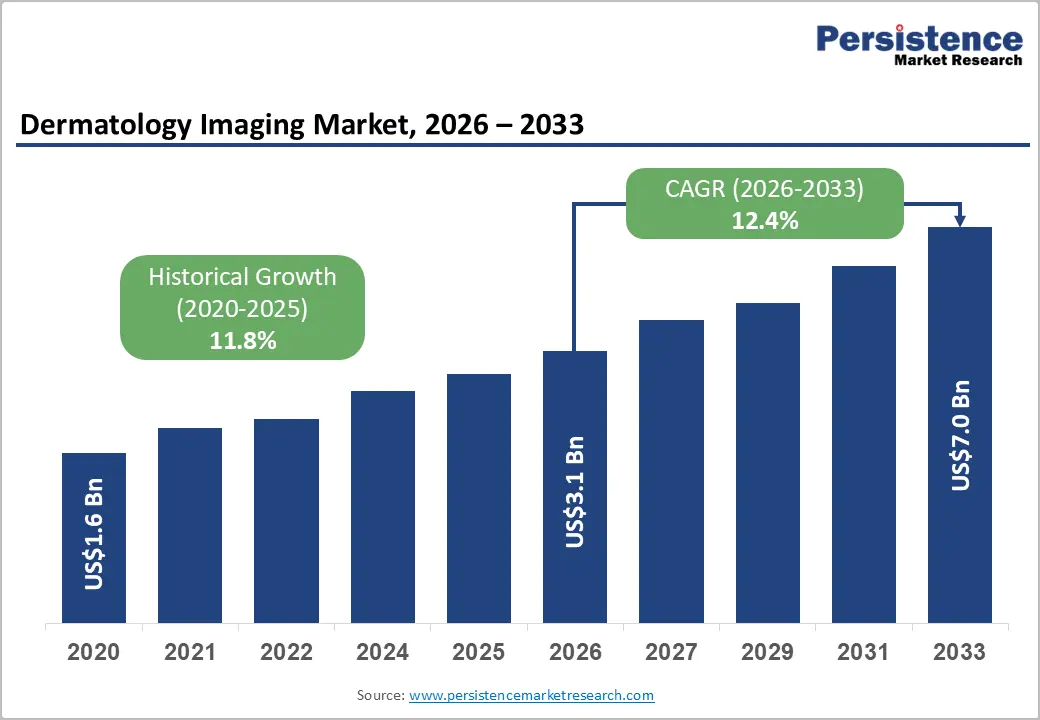

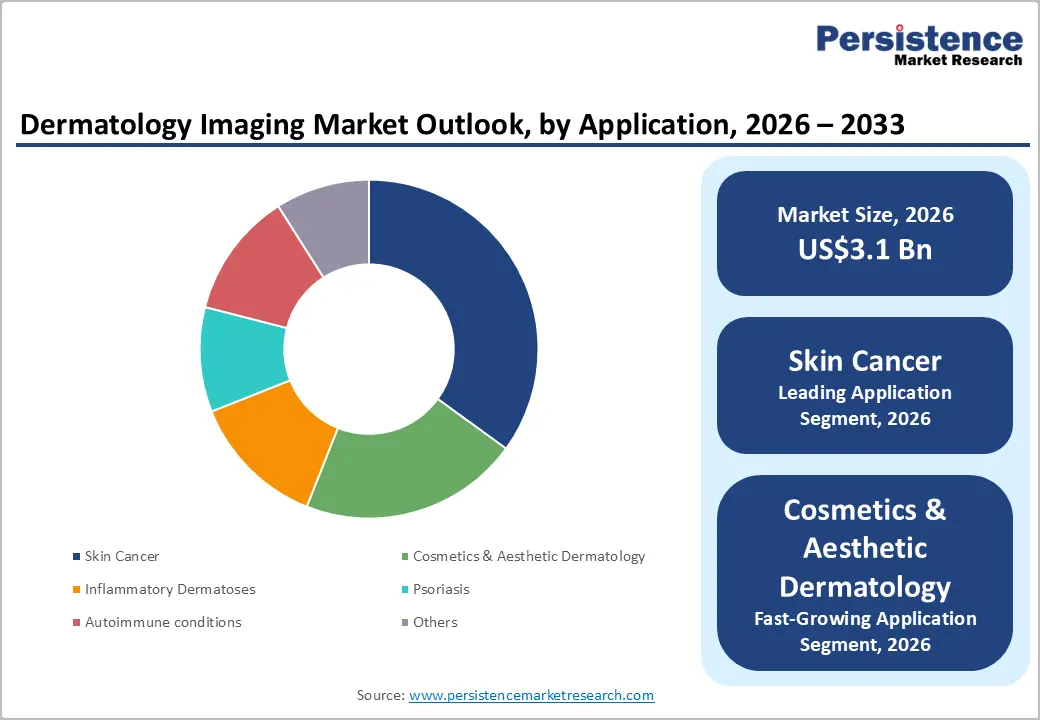

The global dermatology imaging market size is likely to be valued at US$3.1 billion in 2026 and is estimated to reach US$7.0 billion by 2033, growing at a CAGR of 12.4% during the forecast period from 2026 to 2033, driven by aging population expansion, rising skin cancer incidence, expansion of dermatology screening programs, and increasing integration of digital imaging systems across clinical workflows.

Growth is reinforced by demographic pressure from higher ultraviolet exposure and longer life expectancy patterns, increasing dermatological disorder prevalence. Regulatory frameworks supporting early cancer detection and reimbursement expansion for non-invasive diagnostic imaging accelerate adoption. Technology adoption across optical coherence systems, dermatoscopic platforms, and artificial intelligence-assisted imaging improves diagnostic accuracy.

Key Industry Highlights:

- Leading Modality: Dermatoscopes are set to hold around 38% revenue share in 2026, driven by widespread deployment in outpatient dermatology and primary care screening settings.

- Fastest-Growing Modality: Optical coherence tomography (OCT) is projected as the fastest-growing modality, supported by clinical validation of non-invasive cross-sectional tissue imaging as a biopsy alternative in oncology workflows.

- Leading Application: Skin cancer is estimated to hold roughly a 35% revenue share in 2026, due to structured national melanoma screening mandates and AI-assisted diagnostic platform adoption across oncology departments.

- Fastest-Growing Application: Cosmetics and aesthetic dermatology are forecast to record the fastest application growth, driven by rising demand for precision skin analysis in medical aesthetic clinics across urban markets.

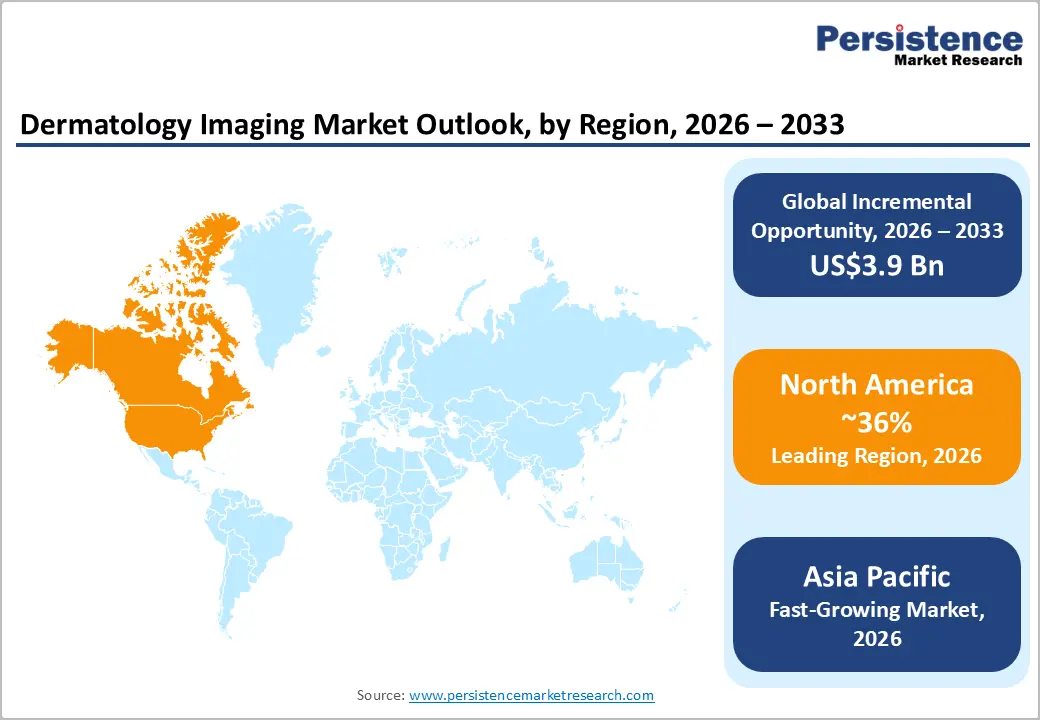

- Regional Leadership: North America is projected to capture roughly 36% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to expanding healthcare infrastructure.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as Canfield Scientific and FotoFinder Systems leveraging AI integration, clinical evidence portfolios, and distribution scale to maintain competitive positioning.

- Innovation Trends: Advances in AI-assisted dermoscopy, cloud-enabled teledermatology platforms, and subscription-based software licensing models are shaping long-term market evolution and directing capital allocation toward interoperable diagnostic ecosystems.

DRO Analysis

Driver - Rising Burden of Skin Cancer and Chronic Dermatological Disorders

Rising incidence of melanoma and non-melanoma skin cancer strengthens demand for advanced imaging systems that support early detection and lesion characterization. Increasing ultraviolet radiation exposure and aging population profiles contribute to higher screening volumes across clinical settings. Imaging adoption improves diagnostic accuracy and reduces dependency on invasive biopsy procedures.

According to the United States Centers for Disease Control and Prevention 2025 surveillance update, more than 5.4 million cases of non-melanoma skin cancer treatment episodes were recorded across outpatient dermatology settings. This clinical load increases utilization of dermatoscopic and digital imaging platforms. Hospitals integrate imaging systems into dermatology workflows to improve early intervention outcomes.

Restraint - High Capital Cost of Advanced Imaging Systems

Advanced dermatology imaging systems, such as optical coherence tomography and high-frequency ultrasound, require high initial investment and maintenance expenditure. Small clinics face procurement limitations that restrict adoption rates. Cost barriers slow penetration in price-sensitive healthcare environments.

Limited reimbursement frameworks in several healthcare systems reduce financial viability for smaller diagnostic providers. Maintenance costs and software upgrade cycles increase operational burden. This constraint impacts the scalability of imaging deployment across decentralized outpatient facilities.

Opportunity - Deployment of AI-Driven Diagnostic Support Systems for Automated Triaging

The integration of machine learning algorithms into digital diagnostic software creates an actionable pathway to transform standard clinical workflows. Traditional skin examinations create massive volumes of high-resolution image data that require meticulous, time-consuming manual review by scarce specialist dermatologists. AI-driven triaging systems address this operational challenge by automatically scanning image datasets, flagging micro-structural anomalies, and prioritizing high-risk cases for immediate clinical review.

This automated filtering system drastically reduces diagnostic latency, allowing healthcare networks to scale screening programs without adding expensive specialized staff. Clear software development guidelines established by regulatory bodies like the FDA provide developers with structured pathways for clinical validation. As validated software plugins become standard additions to existing hardware, imaging device manufacturers can capture steady recurring revenue through software-as-a-service (SaaS) licensing models.

Category-wise Analysis

Modality Insights

Dermatoscopes are anticipated to secure around 38% of the dermatology imaging market share in 2026, reflecting widespread integration across outpatient clinics and primary care settings due to their non-invasive nature and cost accessibility. Companies such as Dermlite deploy polarized light systems that enhance visualization accuracy. Cost-effectiveness and portability sustain high adoption rates relative to capital-intensive modalities in budget-constrained settings.

Optical coherence tomography (OCT) is expected to be the fastest-growing segment, propelled by its cross-sectional imaging capability that eliminates the need for invasive biopsy in a significant share of diagnostic workflows. Caliber Imaging and Diagnostics has commercially deployed confocal-OCT hybrid systems in academic dermatology centers. Demand is accelerating as clinical evidence supporting OCT-guided surgical margin assessment accumulates in peer-reviewed dermatological oncology literature.

Application Insights

Skin cancer applications are poised to dominate with a forecast market share of over 35% in 2026, powered by escalating melanoma incidence, structured national screening protocols, and reimbursement support for imaging-guided biopsy decisions. Siemens Healthineers has integrated AI melanoma risk stratification modules into imaging platforms deployed in European hospital networks. The clinical urgency of early detection sustains consistent imaging utilization across all care settings.

Cosmetics and aesthetic dermatology are estimated to be the fastest-growing segment, fueled by rising consumer demand for non-invasive skin analysis and personalized treatment planning in aesthetic clinics. Canfield Scientific deploys multi-spectral facial imaging systems widely adopted by aesthetic practitioners. Growing disposable income in urban markets and the proliferation of medical-grade aesthetic clinics are compounding demand for precision imaging tools beyond traditional clinical diagnostics.

End-user Insights

Hospitals are likely to be the leading segment with a projected 42% of the dermatology imaging market share in 2026. Due to concentrated patient volumes, multidisciplinary care requirements, and the availability of capital budgets for advanced imaging acquisitions. Academic medical centers such as Mayo Clinic and Johns Hopkins have deployed comprehensive imaging suites integrating dermoscopy, OCT, and whole-body photography systems. Institutional procurement frameworks support regular equipment refresh cycles.

Dermatology centers are anticipated to be the fastest-growing segment, fueled by the proliferation of dedicated outpatient dermatology networks in North America and Europe that prioritize subspecialty imaging capabilities as a competitive differentiator. Chain dermatology providers such as U.S. Dermatology Partners are standardizing AI-integrated imaging platforms across multi-site networks. Favorable reimbursement structures for outpatient dermatological procedures are supporting capital deployment in this setting.

Regional Insights

North America Dermatology Imaging Market Trends

North America is expected to lead with an estimated 36% of the dermatology imaging market share in 2026, supported by advanced healthcare infrastructure, high dermatology screening penetration, and strong integration of AI-enabled imaging systems across hospital networks. Increased adoption of digital dermatoscopy and optical imaging platforms strengthens early detection workflows. Large-scale reimbursement coverage and structured screening programs support sustained diagnostic imaging utilization across clinical settings.

U.S. Dermatology Imaging Market Insights

The U.S is projected to hold around 80% of the market share in 2026, driven by high skin cancer prevalence and advanced diagnostic infrastructure. Hospital dermatology departments expand integration of AI-based dermatoscopy and digital imaging systems into early detection programs. Medicare-supported screening frameworks increase patient access to imaging-enabled diagnostic services.

Canada Dermatology Imaging Market Insights

Canada is forecast to account for approximately 20% of the market share in 2026, supported by universal healthcare coverage and structured dermatology referral pathways. Public healthcare institutions adopt portable imaging systems to improve access in remote regions. Tele-dermatology expansion enhances diagnostic continuity across provincial healthcare systems.

Europe Dermatology Imaging Market Trends

Europe holds an estimated 28% share of the market in 2026, driven by structured public health screening programs and strict clinical guidelines regarding early oncological intervention. Strong collaboration between academic research institutions and medical device manufacturers speeds up the translation of new optical technologies into commercial diagnostic tools.

Germany Dermatology Imaging Market Insights

Germany is projected to capture around 29% of the market share in 2026, driven by advanced hospital infrastructure and strong dermatology specialization centers. University hospitals expand adoption of high-resolution imaging systems for diagnostic precision. Clinical research programs support integration of AI-enabled dermatology imaging workflows.

U.K. Dermatology Imaging Market Insights

The U.K. is forecast to hold approximately 18% of the market share in 2026, supported by national skin cancer screening initiatives and dermatology referral systems. National Health Service facilities expand digital imaging adoption across dermatology departments. Telehealth integration improves access to dermatology diagnostics in regional care settings.

Asia Pacific Dermatology Imaging Market Trends

Asia Pacific is forecast to be the fastest-growing market for dermatology imaging, stimulated by rapid healthcare infrastructure expansion and a growing clinical focus on objective diagnostic methods across expanding urban hospital networks. Rising disposable incomes across developing nations increase consumer demand for precise aesthetic and clinical skin assessments, prompting private medical groups to invest in advanced imaging platforms.

China Dermatology Imaging Market Insights

China is projected to account for approximately 28% of the market share in 2026, driven by the expansion of tertiary hospitals and dermatology specialty centers. Urban healthcare facilities increase the deployment of advanced dermatoscopy and optical imaging systems. National healthcare modernization programs strengthen diagnostic technology integration across public hospitals.

India Dermatology Imaging Market Insights

India is expected to hold around 15% of the market share in 2026, supported by rising dermatology clinic networks and increasing prevalence of skin disorders. Private hospital investments expand access to digital imaging systems in urban centers. Tele-dermatology adoption improves diagnostic reach across semi-urban and rural regions.

Competitive Landscape

The global dermatology imaging market is moderately fragmented, with a mix of large multinational medical device corporations and specialized imaging technology firms competing across distinct modality and application segments. Key participants include Canfield Scientific, FotoFinder Systems, Dermlite, Heine Optotechnik, and Caliber Imaging and Diagnostics, each maintaining differentiated positioning through proprietary imaging algorithms, clinical evidence libraries, and established distribution networks.

Competition is intensifying as AI software companies without hardware manufacturing capabilities enter through platform licensing agreements with established device manufacturers. Scale advantages in clinical data acquisition, regulatory approval track records, and service infrastructure are sustaining the competitive positioning of incumbents, while start-up entrants focus on software-layer differentiation and specialty niche applications to establish market footholds.

Key Industry Developments:

- In April 2026, SquareMind raised US$18 million to advance its AI-powered robotic dermatology imaging platform, accelerating development of full-body automated skin examination systems designed to improve early skin cancer detection and standardize clinical imaging workflows across dermatology practices in the U.S. and Europe.

- In September 2025, QuantifiCare and LegitHealth launched the first AI-powered dermatology imaging platform for clinical trials, integrating advanced imaging systems with artificial intelligence to enable automated lesion assessment, improve scoring consistency, and accelerate dermatology drug development workflows.

Companies Covered in Dermatology Imaging Market

- Canfield Scientific

- FotoFinder Systems

- 3Gen

- Heine Optotechnik

- Caliber Imaging & Diagnostics

- Siemens Healthineers

- Cortex Technology

- DermTech

- STRATA Skin Sciences

- Heidelberg Engineering

- Longport

- Sony Group Corporation

- MELA Sciences

- Miiskin

- Carl Zeiss Meditec

Frequently Asked Questions

The global dermatology imaging market is projected to reach US$3.1 billion in 2026.

Rising skin cancer incidence, increasing adoption of AI-enabled non-invasive imaging, and expansion of dermatology screening infrastructure drive the dermatology imaging market.

The dermatology imaging market is poised to witness a CAGR of 12.4% from 2026 to 2033.

Key market opportunities include the expansion of AI-powered diagnostic and decision-support software, growing adoption of teledermatology platforms, development of home-based and portable skin imaging solutions, increasing investments in skin cancer screening programs across emerging markets, and the emergence of subscription-based software and cloud-enabled imaging platforms that generate recurring revenue streams.

Some of the key market players include Canfield Scientific, FotoFinder Systems, Dermlite, Heine Optotechnik, and Caliber Imaging and Diagnostics.