- Sporting Goods & Equipment

- Cricket Equipment Market

Cricket Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Cricket Equipment Market by Product Type (Bat, Ball, Protective Gear, Others), by End-User (Men, Women, Kids), by Distribution Channel (Offline, Online), and Regional Analysis for 2026 - 2033

Cricket Equipment Market Size and Trend Analysis

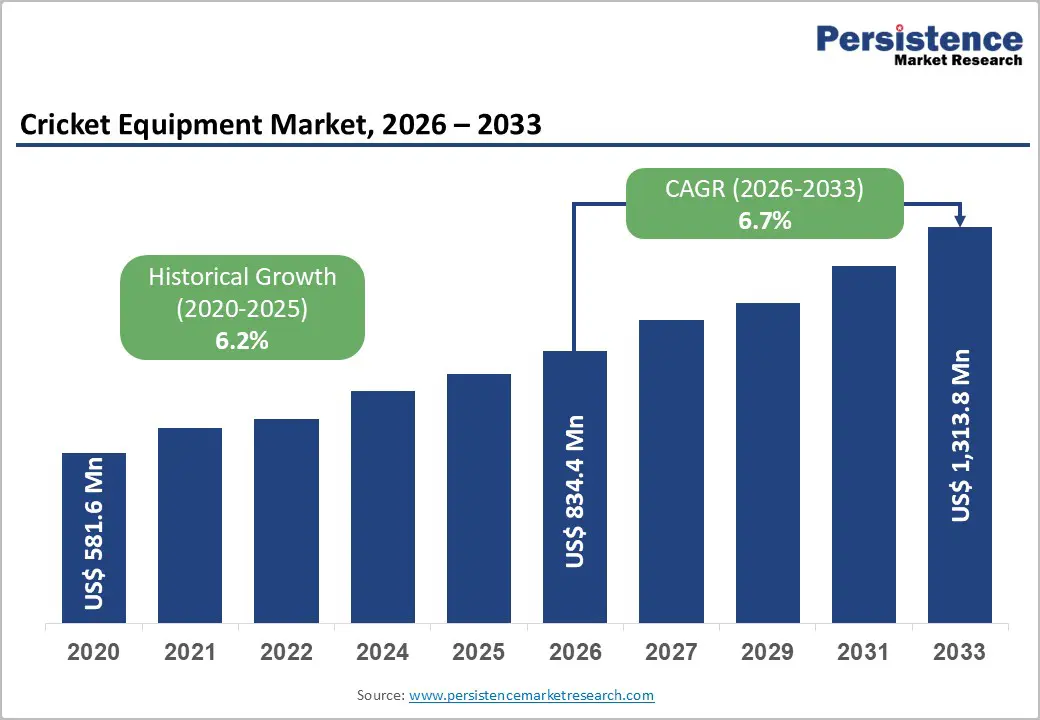

The global Cricket Equipment market size is valued at US$ 839.2 million in 2026 and is projected to reach US$ 1,313.8 million by 2033, growing at a CAGR of 6.7% between 2026 and 2033.

The cricket equipment market is on a structurally sound growth trajectory, driven by the sport's rapid globalization through franchise leagues, expanding women's cricket participation, and the accelerating shift to organized online retail. The International Cricket Council (ICC)'s active expansion into new territories, including the USA, Canada, UAE, and across Africa, is broadening the sport's participant base well beyond traditional strongholds of India, Australia, England, and the West Indies.

Key Industry Highlights:

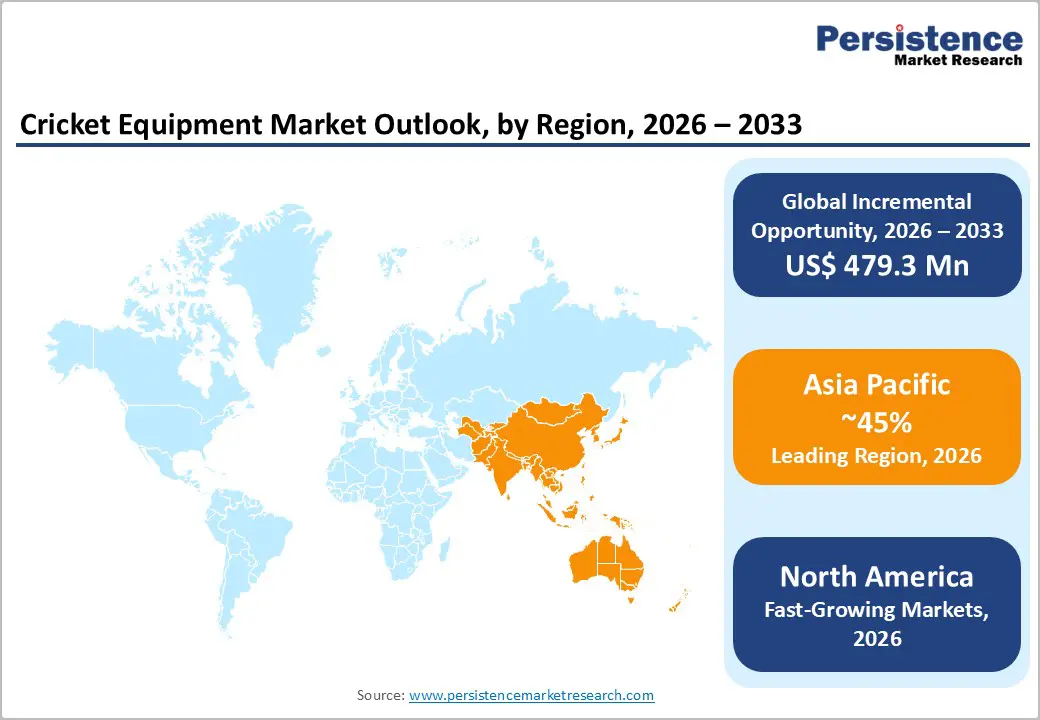

- Leading Region: Asia Pacific dominates the global Cricket Equipment market with approximately 45% revenue share in 2025, driven by India's unparalleled cricket economy, IPL's US$ 16.4 billion franchise valuation, and the BCCI's governance of over 200,000 registered players across 30 state associations.

- Fastest Growing Region: North America is the fastest-growing region through 2033, catalysed by the ICC Men's T20 World Cup 2024 co-hosted in the USA, the launch of Major League Cricket, and a 30-million-strong South Asian diaspora creating institutionalized equipment demand in a frontier cricket market.

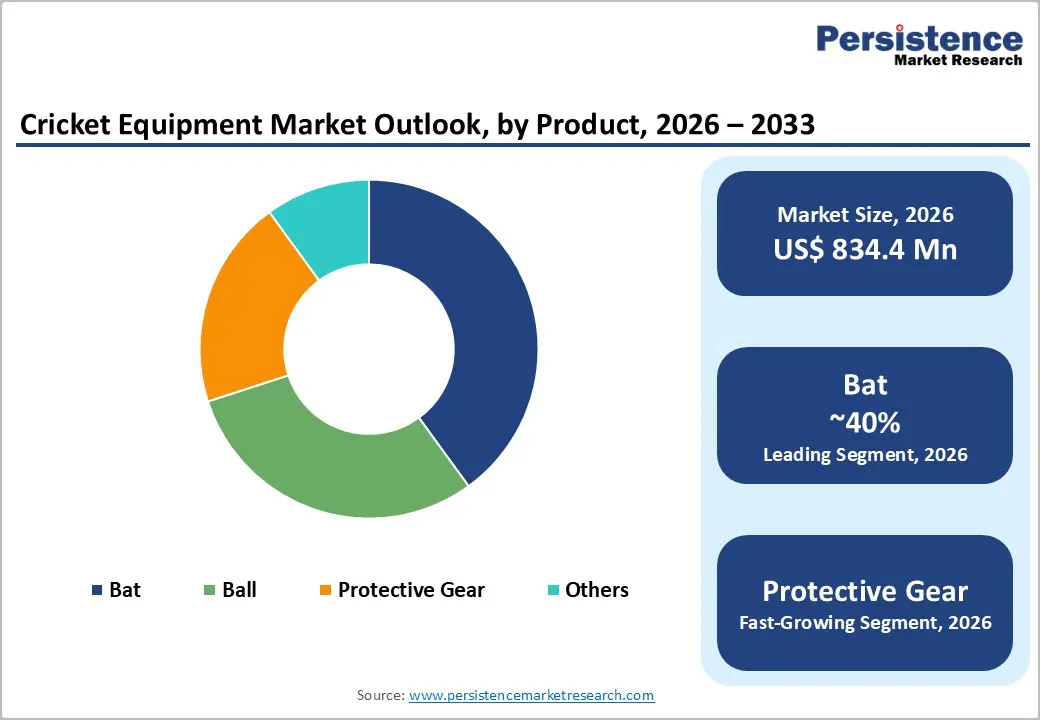

- Leading Product Segment: The bat segment leads the product type category with approximately 34% market share in 2026, driven by high average selling prices, strong aspirational purchasing behaviour, and the powerful brand visibility generated by professional player endorsements across IPL, The Hundred, and BBL broadcast platforms.

- Fast-Growing Distribution Channel: The online distribution channel is the fast-growing segment, accelerated by expanding e-commerce infrastructure across India and diaspora markets, D2C brand investments by SG and BDM, and the growing digital purchasing confidence of under-35 cricket consumers in Tier-2 and Tier-3 cities.

- Opportunity: The most compelling market opportunity lies in youth development programs with ECB's Chance to Shine reaching 5 million+ children and ICC's Cricket for Good spanning 45 countries creating structured pipelines for entry-level equipment procurement and long-term premium brand loyalty conversion.

Market Dynamics

Drivers - Global Franchise Cricket Leagues Fuelling Equipment Demand and Brand Aspirations

The proliferation of franchise-based Twenty20 cricket leagues across multiple continents has transformed cricket from a Commonwealth sport into a global entertainment and commercial phenomenon, directly stimulating equipment demand at both elite and grassroots levels. The Indian Premier League (IPL), valued at approximately US$ 16.4 billion according to Duff & Phelps analysis, sets global benchmarks for player endorsements and equipment visibility.

The Big Bash League (BBL) in Australia, SA20 in South Africa, The Hundred in England, the Caribbean Premier League (CPL), and the International League T20 (ILT20) in the UAE collectively expose millions of viewers to professional equipment brands, driving aspirational consumer purchasing. The ICC reported that cricket now has over 1 billion fans globally, with the sport's official associate member base having expanded to 108 countries as of 2024, directly widening the addressable participant and equipment buyer base.

Women's Cricket Expansion: Creating a New Equipment Demand Pool

Women's cricket has undergone a transformational decade of growth, with international governing bodies and franchise league organizers investing substantially in professional women's competitions that are generating their own equipment demand ecosystems. The ICC Women's T20 World Cup 2024 in the UAE attracted record viewership, while the Women's Premier League (WPL) in India, launched in 2023, has emerged as a landmark franchise competition with elite players commanding significant endorsement contracts that drive equipment brand visibility.

According to ICC participation data, women's cricket participation has grown at a double-digit pace across India, Australia, England, and South Africa over the past five years. This structural shift is compelling manufacturers, including Gray-Nicolls, Kookaburra, and MRF, to develop gender-specific product lines in bats, protective gear, and apparel, opening a previously underserved market segment.

Restraints - Geographic Concentration of Demand in a Limited Number of Core Cricket Markets

Despite ICC's expansion efforts, cricket equipment demand remains heavily concentrated in India, Australia, England, Pakistan, Sri Lanka, and the West Indies, creating structural vulnerability to economic cycles and participation trends in these core geographies. India alone accounts for an estimated 40% of global cricket equipment revenue, making the market disproportionately sensitive to domestic economic conditions, consumer sentiment, and the competitive intensity of the IPL season.

In contrast, emerging cricket markets in USA, Canada, and across Africa have large diaspora-driven fan bases but nascent organized participation infrastructure, limiting near-term equipment sales volume generation despite growing ICC investment.

Raw Material Cost Volatility Affecting Manufacturing Economics for Premium Equipment

Cricket bat manufacturing is critically dependent on English willow, specifically Grade 1 and Grade 2 English willow from the species *Salix alba var. caerulea* a specialty agricultural commodity with limited cultivation geography concentrated in Essex and Suffolk in England. Climate variability, including irregular rainfall patterns affecting willow growth cycles, combined with increasing premium bat demand from the global market, has contributed to significant raw material cost inflation.

Premium English willow bats retailing at £300–£600+ are subject to supply constraints that manufacturers cannot easily resolve through substitution, as Kashmir willow, while more affordable, is widely perceived as inferior for professional play. These material dynamics constrain margin management and price accessibility for manufacturers catering to mid-tier market segments.

Opportunities - Online Retail Channel Transformation and D2C Brand Building

The rapid shift toward online retail procurement of cricket equipment represents one of the most significant growth opportunity vectors, particularly for brand-direct and specialist digital-native players. E-commerce penetration in sporting goods has accelerated post-pandemic, with platforms such as Amazon, Flipkart (India), and specialist cricket retailers enabling reach into Tier-2 and Tier-3 cities in India and diaspora-dominated communities in the USA, Canada, UK, and Australia that were previously inaccessible to organized retail.

According to the Confederation of Indian Industry (CII), India's sports goods industry, of which cricket equipment forms the largest segment, has identified e-commerce as the primary growth channel for domestic distribution expansion. Direct-to-consumer (D2C) models are enabling brands, including SS Ton, SG, and BDM, to bypass traditional multi-tier distribution, improving margins while building direct customer relationships through customization services, interactive fitting tools, and player endorsement content.

Youth Cricket Development Programs and School-Level Participation Initiatives

Youth cricket development programs funded by national cricket boards and the ICC's global development programs represent a highly promising demand catalyst for entry-to-mid-tier equipment manufacturers. The Board of Control for Cricket in India (BCCI) has operationalized cricket academies and grassroots participation programs across all 30 state associations, while Cricket Australia's national development pathway and the England and Wales Cricket Board (ECB)'s Chance to Shine program which has introduced cricket to over 5 million children since its inception, are systematically building the next generation of equipment buyers.

The ICC's Cricket for Good social impact program spans 45 countries and specifically targets youth inclusion. Equipment manufacturers that invest in school-level kit partnerships, affordable starter pack product lines, and coach endorsement programs are positioned to capture early-stage brand loyalty that converts into lifetime premium equipment purchasing relationships.

Category-wise Analysis

Product Type Insights

The bat segment dominates the global Cricket Equipment market by product type, accounting for approximately 34% of the total market share in 2026. This leadership reflects the bat's central role as the primary individual playing implement in cricket, its high average selling price relative to other equipment categories, and the strong aspirational purchasing behaviour it generates across skill levels.

Premium bats from heritage brands such as Gray-Nicolls, Kookaburra, Gunn & Moore, and SS Ton command retail prices of £200–£600+, while mid-range and entry-level options from SG and BDM serve the mass market. Player endorsement culture, particularly the visibility of signature bats used by Virat Kohli (MRF), Rohit Sharma (CEAT), and Steve Smith (Bat by Bell), directly drives aspirational consumer purchasing. The Protective Gear segment is the fast- growing product type, driven by increasing safety awareness and mandatory protective equipment requirements in youth cricket programs globally.

End-user Insights

The men's segment constitute the dominant end-user category, representing approximately 62% of global cricket equipment share in 2025, reflecting men's cricket's longer commercial history, higher participation volumes, and greater professional league infrastructure globally. Men's cricket has the deepest equipment procurement ecosystem, spanning international professionals, domestic first-class players, club cricketers, and recreational participants across all age groups.

The BCCI reported over 200,000 registered male cricketers in India's organized domestic structure as of 2024, while Cricket Australia and the ECB each maintain extensive male participation databases spanning junior through senior age groups. However, the Women's and Kids segments are the fast- growing end-user categories, with women's cricket participation growing at double-digit rates across India, Australia, and England, and structured youth programs driving consistent demand for appropriately sized starter equipment.

Distribution Channel Insights

The Offline distribution channel retains market leadership, accounting for approximately 61% of the total cricket equipment market share in 2025, reflecting the established role of specialist cricket retailers, sports goods stores, and pro shops at cricket grounds in the purchasing journey for high-value items such as bats and protective gear.

Consumers purchasing premium equipment, particularly bats valued above £150, overwhelmingly prefer physical inspection, weight assessment, and expert fitting guidance, creating a durable structural advantage for offline channels. Established specialist retailers, including Morrant Sports (UK), All Rounder Cricket (UK/Australia), and regional sports chains across India, serve as both retail and fitting specialists.

Regional Analysis

North America Cricket Equipment Market Trends & Analysis

North America represents an emerging and rapidly evolving market for cricket equipment, driven predominantly by the substantial South Asian diaspora population in the USA and Canada and the ICC's strategic investment in the region as a frontier cricket market. The ICC Men's T20 World Cup 2024, co-hosted by the USA and the West Indies, marked a landmark moment for cricket's North American profile, exposing the sport to new audiences through high-profile matches at Nassau County International Cricket Stadium in New York. The USA Cricket national governing body is actively expanding participation through school programs and community leagues, while the Major League Cricket (MLC) franchise competition launched in 2023 has further institutionalized professional cricket infrastructure in the region, stimulating organized equipment retail demand.

U.S. Cricket Equipment Market Size

The U.S. Cricket Equipment market is valued at approximately US$ 68 Mn in 2026, underpinned by the estimated 30 million South Asian diaspora in the United States, one of the world's largest cricket fan and participant communities. The co-hosting of the ICC Men's T20 World Cup 2024 delivered a measurable boost to equipment retail and participation infrastructure, while Major League Cricket's six-franchise model is generating sustained demand from professional and amateur players.

Europe Cricket Equipment Market Trends, Drivers & Insights

Europe's cricket equipment market is anchored by England has one of the highest per-capita participation alongside diaspora-driven demand in Germany, France, and the Netherlands. The England and Wales Cricket Board (ECB)'s active domestic development programs, including Chance to Shine (reaching over 5 million children) and the Hundred franchise competition, sustain strong grassroots and elite equipment demand across the region.

Germany Cricket Equipment Market Size

Germany's cricket equipment market was valued at approximately US$ 18 million in 2025, driven primarily by a growing South Asian diaspora community and the Deutsche Cricket Verband (DCV)'s expansion programs that have increased registered clubs and players steadily over the past decade. Germany Cricket is an ICC associate member actively developing youth and women's participation pathways, creating structured demand for entry-level and mid-tier equipment across expanding club networks in Berlin, Frankfurt, and Hamburg.

U.K. Cricket Equipment Market Size

The U.K. Cricket Equipment market is likely to be valued at US$ 142 million in 2026, reflecting England's position as the global centre of cricket heritage and one of the sport's most commercially mature equipment markets. The ECB reported approximately 280,000 registered recreational cricketers in England and Wales, supported by over 5,700 cricket clubs. Premium bat brands including Gray-Nicolls, Gunn & Moore, and Hunts County are headquartered in the UK, supporting a sophisticated domestic market with strong brand equity and established specialist retail infrastructure.

France Cricket Equipment Market Size

France's Cricket Equipment market remains nascent but steadily developing, valued at approximately US$ 9 Mn in 2026, sustained by a growing South Asian diaspora concentrated in the Île-de-France region and the Fédération Française de Cricket (FFC)'s ICC-supported development programs. The Paris 2024 Olympics increased overall sports participation awareness in France, while the FFC's school cricket introduction programs are creating an early-stage participant pipeline that will drive entry-level equipment demand over the forecast period.

Asia Pacific Cricket Equipment Market Drivers & Analysis

Asia Pacific dominates the global cricket equipment market, commanding approximately 45% of global revenue in 2026, anchored by India's unparalleled market scale and complemented by significant and growing contributions from Australia, Pakistan, Sri Lanka, and Bangladesh. India's cricket economy fueled by the IPL, BCCI's US$ 6.2 billion media rights cycle, and the countries over one billion cricket followers creates a consumption environment with no parallel globally. China and Southeast Asian markets remain peripheral but are beginning to attract ICC investment as part of the sport's Asian expansion strategy.

China Cricket Equipment Market Size

China's Cricket Equipment market remains in its infancy, estimated at approximately US$ 12 Mn in 2025, with demand concentrated among expatriate communities and a small but growing domestic enthusiast base in cities including Beijing, Shanghai, and Guangzhou. The ICC has invested in targeted cricket development programs in China, and several Chinese sports goods manufacturers including those operating under OEM contracts for global cricket brands represent the primary domestic market link to the broader global cricket equipment supply chain.

India Cricket Equipment Market Size

India's Cricket Equipment market is the largest single-country market globally, valued at approximately US$ 395 Mn in 2025, driven by the world's largest cricket participation base, the commercial behemoth of the IPL, and a deeply entrenched culture of cricket as the dominant national sport. The BCCI governs over 200,000 registered players across 30 state associations, while the unregistered recreational cricket ecosystem spanning gully cricket, club cricket, and corporate tournaments encompasses tens of millions of additional equipment consumers.

Japan Cricket Equipment Market Size

Japan's Cricket Equipment market is a niche but growing segment, estimated at approximately US$ 8 Mn in 2025, primarily sustained by a dedicated expatriate community and the Japan Cricket Association (JCA)'s systematic development efforts that have expanded registered club membership across major cities. The JCA an ICC associate member has developed school cricket programs and national league infrastructure that are gradually building a domestic participant base, supporting entry-level equipment demand through organized retail and online channels.

Competitive Landscape

The global cricket equipment market exhibits a moderately fragmented competitive structure, with established heritage brands maintaining dominant positions in premium segments while regional mass-market manufacturers command high volume in price-sensitive markets.

Kookaburra, Gray-Nicolls, Gunn & Moore, and Salix lead the premium bat and ball segment globally, while Indian manufacturers SG, MRF, and BDM dominate the high-volume mid-tier. Key differentiators include player endorsement portfolios, willow grade sourcing capabilities, and innovation in protective gear materials such as carbon fibre and advanced foam composites.

Key Market Developments

- In April 2025, Kookaburra launched its next-generation Ghost Pro bat series featuring an updated scoop profile and extended edge thickness optimized for T20 power hitting, reinforcing its position as the preferred bat brand for professional fast-scoring formats.

- In June 2024, FanCode Shop, the merchandising division of FanCode, has renewed its exclusive licensing and merchandising partnership with the International Cricket Council (ICC) in India. This partnership allows FanCode Shop to create official fan merchandise and accessories for the ICC Men's T20 World Cup 2024 and ICC Women’s T20 World Cup 2024.

Global Cricket Equipment Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 581.6 Mn |

|

Current Market Value (2026) |

US$ 834.4 Mn |

|

Projected Market Value (2033) |

US$ 1,313.8 Mn |

|

CAGR (2026-2033) |

6.7% |

|

Leading Region |

Asia Pacific, 45% share |

|

Dominant Application |

Bat, 35% share |

|

Top-ranking Product |

Men, 55% |

|

Incremental Opportunity |

US$ 479.3 Mn |

Companies Covered in Cricket Equipment Market

- Kookaburra Sport Pty Ltd

- Gray-Nicolls (Spartan Sports)

- Gunn & Moore Ltd

- SG – Sanspareils Greenlands

- MRF Limited

- BDM Cricket

- SS Ton

- Salix Cricket

- Hunts County Bats

- Masuri Cricket Helmets

- Ayrtek Cricket

- New Balance Cricket

- Puma SE

- Adidas AG

- CA Sports

- Slazenger

Frequently Asked Questions

The global Cricket Equipment market is valued at US$ 839.2 Mn in 2026 and is projected to reach US$ 1,313.8 Mn by 2033, expanding at a CAGR of 6.7% between 2026 and 2033.

The primary demand drivers are the global proliferation of franchise T20 cricket leagues including the IPL (valued at US$ 16.4 billion), Big Bash League, The Hundred, and Major League Cricket which generate aspirational equipment demand, combined with ICC's expansion of cricket into 108 associate member nations and the structural growth of women's cricket participation across India, Australia, England, and South Africa.

The Bat segment dominates with approximately 34% market share in 2025, reflecting its high average selling price, the aspirational purchasing behaviour it generates across skill levels, and the powerful brand visibility created by professional player endorsement contracts with global icons including Virat Kohli (MRF), Rohit Sharma (CEAT), and Steve Smith across IPL, The Hundred, and international platforms.

Asia Pacific leads the global Cricket Equipment market with approximately 45% revenue share in 2025, with India being the single largest national market valued at approximately US$ 395 Mn. India's dominance is driven by the BCCI's commercial scale, the IPL's media rights cycle, over 200,000 registered domestic players, and an unregistered recreational participant base spanning ten of millions of equipment consumers.

The market is led by Kookaburra Sport (official ICC ball supplier), Gray-Nicolls (premium English willow heritage brand), SG – Sanspareils Greenland’s (India's largest volume manufacturer and BCCI official ball supplier), Gunn & Moore, MRF Limited, and SS Ton.