- Food Ingredients & Additives

- Corn Protein Market

Corn Protein Market Size, Share and Growth Forecast, 2026 - 2033

Corn Protein Market by Grade (Feed Grade, Food Grade, Industrial Grade, Specialty Grade), Application (Animal Feed, Food and Beverage, Industrial Applications, Agriculture Inputs), Product Type (Corn Gluten Meal, Zein Protein, Corn Protein Isolates and Concentrates, Hydrolyzed Corn Protein), and Regional Analysis for 2026 - 2033

Corn Protein Market Share and Trends Analysis

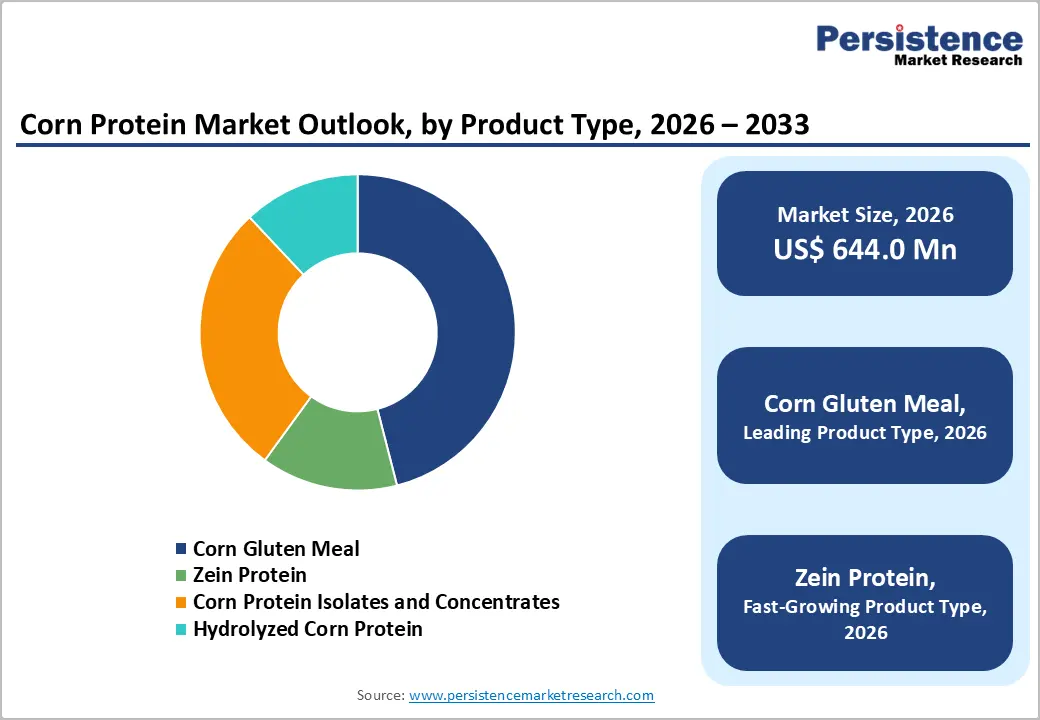

The global corn protein market size is likely to be valued at US$ 644.0 million in 2026 and is projected to reach US$ 1,055.0 million by 2033, growing at a CAGR of 7.3% during the forecast period 2026 - 2033.

The corn protein market is growing steadily as consumers shift toward plant-based, clean-label, and gluten-free protein ingredients, with over 65% of consumers globally increasing their plant protein intake. Its functional advantages, including high digestibility, emulsification, and film-forming properties, support widespread use in food, nutraceuticals, and biodegradable materials.

Simultaneously, expansion in the animal feed industry, driven by rising global meat production and protein demand, continues to anchor volume growth. Rapid urbanization and income growth in emerging markets further boost consumption of processed foods and livestock products, accelerating demand across both food and feed applications.

Key Industry Highlights

- Dominant Application Segments: Animal feed is set to command approximately 42% share in 2026, while food & beverage is projected to be the fastest-growing segment, driven by plant-based demand.

- Leading Product Types: Corn gluten meal is expected to lead with around 45% share in 2026, while zein protein is likely to grow the fastest, supported by specialty and biodegradable applications.

- Dominant Grade Segment: Feed grade is anticipated to dominate with nearly 48% share in 2026, while specialty grade is projected to grow the fastest through 2033, driven by high-value end uses.

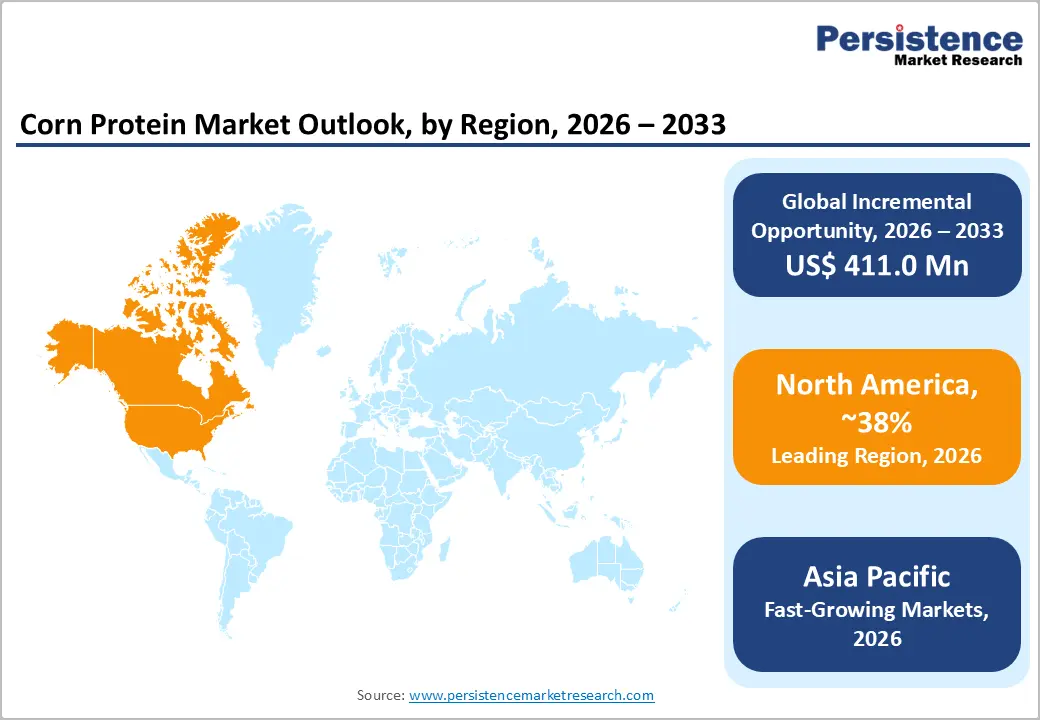

- Regional Leadership: North America is expected to lead with a 38% share in 2026, while Asia Pacific is projected to be the fastest-growing region at a 8.1% CAGR through 2033, supported by livestock expansion and rising protein demand.

- Technology and Innovation Trends: Advancements in corn processing technologies are improving efficiency and enabling sustainable applications, with industrial use expected to grow steadily through 2033 as demand for bio-based materials increases.

| Key Insights | Details |

|---|---|

| Corn Protein Market Size (2026E) | US$ 644.0 Mn |

| Market Value Forecast (2033F) | US$ 1,055.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

DRO Analysis

Driver - Rising Demand for Plant-Based Protein Ingredients

The global shift toward plant-based diets is driving strong growth in the corn protein market. The FAO reports that global plant protein consumption has risen by over 15% since 2018, reflecting growing consumer awareness of health, sustainability, and dietary balance. Corn-derived proteins, including zein and protein isolates, are increasingly favored for their functional versatility and non-allergenic profile compared to soy or wheat. This trend is particularly pronounced in developed markets, where manufacturers are reformulating products to align with clean-label and vegan preferences, expanding both market reach and product innovation. Corn protein’s adaptability in snacks, beverages, and bakery items further supports its adoption across multiple categories.

In 2025, Cargill’s Protein Profile study highlighted a notable rise in consumer demand for alternative plant proteins in North America and Europe, specifically corn-based ingredients. Concurrently, FDA clean-label initiatives have encouraged manufacturers to replace allergenic proteins with versatile, compliant alternatives, reinforcing corn protein’s relevance. Partnerships between ingredient suppliers and food manufacturers are accelerating the development of functional formulations, from improved texture and emulsification to innovative encapsulation solutions. Together, these factors are positioning corn protein as a scalable, mainstream option for both health-focused and sustainable product lines.

Expansion of the Livestock Industry and Advancements in Corn Processing

The animal feed sector remains a cornerstone of corn protein demand. According to the OECD-FAO Agricultural Outlook, global meat production is projected to grow by 1.3% annually through 2030, creating steady demand for high-protein feed ingredients. Corn gluten meal, a by-product of wet milling, is widely used due to its digestibility and cost efficiency. Rapid growth in livestock production across China and India is driving increased feed-grade protein consumption, while investments in large-scale feed mills and integrated supply chains are improving product accessibility and reducing costs for end users.

Simultaneously, EU initiatives to reduce single-use plastics are driving the adoption of bio-based alternatives, including zein-derived coatings and films, while U.S. Department of Energy-supported biorefining programs have improved protein extraction efficiency by up to 20%. These technological advancements allow manufacturers to diversify into high-value industrial applications, including bioplastics, coatings, and pharmaceutical excipients. By combining sustainable policy incentives with improved processing methods, corn protein is increasingly positioned to serve both feed and industrial markets, creating robust opportunities for growth and long-term market resilience.

Restraint - Volatility in Corn Prices and Supply Chain Risks

Corn prices remain highly sensitive to climatic conditions, trade policies, and supply shifts. The USDA National Agricultural Statistics Service reported that U.S. farmers plan to plant 3% fewer corn acres in 2026, redirecting some land to soybeans due to cost and profitability pressures. This reduction may tighten future supply and contribute to price swings for corn-based inputs. Meanwhile, USDA Grain Stocks data showed U.S. corn ending stocks down 13% in 2025 compared with the prior year, signaling tighter inventories and heightening uncertainty around raw material costs. Such fluctuations complicate procurement planning and can compress margins for corn protein manufacturers, particularly when demand remains strong.

Supply chain challenges further amplify risk. Transportation bottlenecks and freight volatility have disrupted on-time deliveries, while ocean freight delays and inventory distortions are forcing buyers to move away from just-in-time models toward buffer stocking. These logistical challenges increase operational costs and create short-term pricing unpredictability for downstream industries. Collectively, price swings and supply chain instability underscore the structural risks facing the corn protein market, requiring companies to adopt hedging strategies and diversified sourcing to maintain production continuity and protect profitability.

Competition from Alternative Plant Proteins

Corn protein faces strong competition from established plant proteins such as soy, pea, and wheat, which benefit from mature supply chains and broader consumer acceptance. European Commission agricultural data shows that soy protein accounts for over 60% of plant protein consumption in Europe, highlighting its dominant position in food applications. This limits the penetration of corn protein, particularly in higher-value segments where cost efficiency and functionality are critical. As a result, manufacturers need to differentiate corn protein through enhanced functional properties or sustainable sourcing. Consumer familiarity with alternative proteins also reinforces their market preference, making the adoption of corn protein slower in some regions.

In addition, global feed markets are adjusting formulation strategies in response to price volatility and import policies. For example, China is promoting alternative feed ingredients and fermentation-based protein options to reduce reliance on imported soybeans. These measures intensify competition for corn protein in both feed and food applications, as alternative proteins may offer cost advantages or better supply security. Manufacturers must therefore innovate continuously in processing, functionality, and pricing to remain competitive. This dual challenge of market penetration against established proteins and maintaining cost-effectiveness remains a key structural restraint for the corn protein industry.

Opportunities - Expansion in Functional and Specialty Food Ingredients

The growing global demand for functional foods and nutraceuticals presents a major opportunity for corn protein. Corn-derived ingredients, particularly zein protein, offer unique functional properties, including film-forming, emulsification, and encapsulation. According to the World Health Organization (WHO), the global functional food market is projected to exceed US$ 500 Bn by 2030, creating strong demand for value-added protein ingredients. Food manufacturers are increasingly reformulating products to meet health-conscious and clean-label trends, expanding the range of protein inclusions in beverages, snacks, and fortified foods. Regulatory compliance and allergen-free properties further enhance the adoption of corn protein. These factors together position corn protein as a preferred ingredient for innovation in high-value food applications.

In 2026, government agricultural policy shifts in major markets are supporting diversified protein sources, encouraging ingredient innovation to improve nutrition and food security. These measures are accelerating the adoption of corn protein in specialty foods as manufacturers seek compliant, high-functioning alternatives to traditional proteins. Demand is particularly strong in North America and Europe, where clean-label, plant-based, and functional formulations are growing rapidly. The convergence of consumer health trends and regulatory support provides an actionable growth pathway. Corn protein’s functional versatility and compatibility with multiple applications strengthen its market positioning. Overall, it is becoming a mainstream ingredient for health-driven product innovation.

Emerging Markets and Industrial Applications

Rapid growth in emerging economies, particularly in the Asia Pacific and Latin America, is expanding demand for corn protein across food, feed, and industrial applications. The World Bank projects agricultural output in developing countries to grow by 2-3% annually, driving increased consumption of protein-rich ingredients. Investments in local processing infrastructure and favorable government policies further enhance market penetration. The rise in livestock production and food processing industries creates steady demand for feed-grade and functional corn proteins. These developments make emerging markets a key avenue for revenue growth and industrial adoption.

Policy emphasis on sustainability and bio-based materials is creating additional industrial opportunities. China’s 2026 “No. 1 document” highlights support for agricultural innovation, diversification, and bio-industrial applications, including value-added protein products. Meanwhile, Asia’s expanding feed corn imports reflect growing demand for alternative proteins in the livestock and poultry sectors. Regulatory targets for reducing single-use plastics in Europe and North America encourage the adoption of corn-based biodegradable materials and coatings. These developments provide strategic avenues for corn protein to capture both food and industrial applications. The combination of favorable policies, growing demand, and sustainable innovation reinforces long-term market potential.

Category-wise Analysis

Application Insights

The animal feed segment is expected to be the leading application, holding around 42% of the global corn protein market in 2026, driven by expanding livestock production and demand for high-quality feed ingredients. Corn gluten meal remains a staple due to its high protein content, digestibility, and cost efficiency. In Q4 2025, it was reported as a preferred sustainable protein for poultry and livestock, reflecting its critical role in feed strategies. Procurement adjustments in early 2026 show buyers managing supply variability while retaining corn gluten meal in formulations. The broader compound feed market is expanding as livestock and aquaculture adopt precision-nutrition approaches. These trends confirm animal feed as a strategically indispensable application for corn protein.

The food & beverage segment is anticipated to be the fastest-growing application, supported by rising demand for plant-based proteins and clean-label products. Corn protein enhances texture, emulsification, and nutritional value in beverages, snacks, and fortified foods. Regulatory trends in past years have encouraged diversification beyond animal proteins, boosting its adoption. Functional foods, allergen-free formulations, and R&D investments support growth, particularly in North America and Europe. Consumer preference for health-conscious, sustainable ingredients reinforces expansion. These factors make food & beverage a key growth frontier for corn protein.

Product Type Insights

Corn gluten meal is poised to be the leading product type, accounting for about 45% of global production in 2026, and is widely used in feed formulations due to its high protein content, digestibility, and cost efficiency. In 2025, it remained a critical sustainable protein in poultry and livestock feed, with a reliable supply supporting market stability. Wet-milling by-products offer cost advantages, while compound feed expansion and livestock growth drive consistent demand. Procurement strategies in early 2026 further reinforce its indispensability. Corn gluten meal remains a revenue cornerstone for manufacturers across global feed markets.

Zein protein is projected to be the fastest-growing product type, driven by its functional versatility and industrial adoption. Its hydrophobicity, film-forming, and biodegradable properties support applications in food coatings, pharmaceuticals, and sustainable packaging. Developments in 2025-2026, including protein-based biodegradable films and thermoplastic blends, underscore growing commercial viability. Rising demand for clean-label, plant-based solutions and regulatory support for bio-materials accelerate adoption. Zein protein is transitioning from niche use to a high-value innovation driver across food and industrial sectors.

Regional Analysis

North America Corn Protein Market Trends

North America is expected to be the leading corn protein market, accounting for approximately 38% of the global share in 2026, anchored by the U.S. as a dominant producer of corn and related proteins. Regulatory frameworks such as those from the FDA support ingredient safety while enabling innovation in food and feed applications. North America’s advanced wet-milling capacity ensures a consistent supply of corn protein ingredients and by-products such as corn gluten meal. Feed millers continue to integrate corn protein into high-quality animal nutrition strategies, adapting formulations to suit precision-nutrition goals. In early 2026, some industry sources reported that corn gluten meal remained a cornerstone ingredient in livestock and poultry feed portfolios.

The evolving feedstock economics influenced sourcing approaches, as corn processing facilities increasingly balanced protein by-product allocation with starch and biofuel priorities. These shifts prompted North American feed buyers to reassess corn protein sourcing strategies to maintain supply continuity and cost stability amid pricing pressures. Integration of corn protein in functional food formulations continues in tandem, supported by consumer trends toward high-protein, allergen-free products. The region’s strong feed and food value chains, combined with mature logistics and innovation ecosystems, reinforce North America’s leadership while sustaining robust market dynamics.

Europe Corn Protein Market Trends

Europe represents a mature and strategically significant market, led by Germany, the U.K., France, and Spain. Stringent sustainability regulations and circular economy policies encourage the adoption of corn protein in both industrial and food applications. The European Commission’s initiatives promoting sustainable agriculture and eco-friendly packaging have strengthened the market for corn-derived proteins such as zein. In 2025, European feed and food companies actively incorporated corn protein into eco-friendly formulations and biodegradable material projects to meet environmental mandates.

Policy-driven investments in alternative protein research and industrial processing are enhancing innovation in functional foods and sustainable applications. Despite reliance on imported raw corn and competition from soy protein, corn protein is increasingly recognized for its versatility and environmental alignment. Adoption in both feed and industrial applications continues to expand, supported by regulatory compliance and evolving consumer preferences, ensuring steady market relevance and resilience across the region.

Asia Pacific Corn Protein Market Trends

Asia Pacific is projected to be the fastest-growing regional market, to expand at a CAGR of about 8.1% from 2026 to 2033, supported by rapid urbanization, rising incomes, and expanding livestock and aquaculture sectors. Feed manufacturers in Asia are increasingly relying on corn gluten meal as a strategic protein and energy source due to rising meat consumption and feed production growth. Industry insights show that by 2026, Asia’s animal feed sector is integrating corn gluten meal as a core ingredient to support intensive poultry, swine, and aquaculture diets, reflecting robust regional demand patterns.

Government emphasis on food security and regional feed self-sufficiency is shaping market adoption patterns. The cost competitiveness of corn-derived protein and the escalating cost of compound feed production are influencing procurement strategies across China, India, Indonesia, and Vietnam. These countries are expanding wet-milling facilities and enhancing processing capacities to support local demand. Increasing feed formulations that balance cost, performance, and sustainability bolster corn protein uptake. Combined with macro trends in animal protein consumption and supportive policy directions, Asia Pacific’s role as the fastest-growing regional market is well supported in 2025-2026, with ongoing expansion in both feed and emerging industrial applications.

Competitive Landscape

The global corn protein market is moderately consolidated, with leading players such as Cargill, ADM, Ingredion, and Tate & Lyle controlling a substantial portion of the revenue share. These companies leverage extensive supply chains, large-scale processing facilities, and established relationships with feed and food manufacturers. Heavy investments in R&D, innovation in protein extraction and isolation technologies, and development of functional and specialty protein applications maintain their competitive edge.

Regional and niche players, including Farbest Brands and Shandong Dabeinong Feed Co., focus on specialty segments such as zein protein, industrial applications, or regional feed markets. Entry barriers such as high capital requirements, regulatory compliance, and complex supply chain management limit new competitors. Market consolidation is expected to continue through strategic M&A, capacity expansions, and technology partnerships in protein processing, while innovation in sustainable and biodegradable applications drives collaboration between established and emerging companies.

Key Developments:

- In March 2024, ADM introduced a new line of hydrolyzed corn protein powders and liquid concentrates to enhance solubility, texture, and taste in plant-based beverages, supporting its strategy to capture growth in the allergen-free and sustainable protein market.

Companies Covered in Corn Protein Market

- Cargill, Incorporated

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Roquette Frères

- Ingredion Incorporated

- Bunge Limited

- DuPont Nutrition & Biosciences

- Kerry Group

- Tereos Group

- Agrana Beteiligungs-AG

- Gulshan Polyols Ltd.

- HL Agro Products Pvt. Ltd.

- Grain Processing Corporation

Frequently Asked Questions

The global corn protein market is projected to reach US$ 644.0 million in 2026.

Rising plant-based diets, livestock feed demand, and industrial adoption of sustainable proteins drive growth.

The market is expected to grow at a CAGR of 7.3% from 2026 to 2033.

Emerging functional food applications, biodegradable materials, and expanding feed demand in Asia Pacific are key opportunities.

Cargill, ADM, Ingredion, and Tate & Lyle are leading corn protein market players.