- Industrial Goods & Service

- Construction and Demolition Waste Management Market

Construction and Demolition Waste Management Market Size, Share, and Growth Forecast 2026 - 2033

Construction and Demolition Waste Management Market by Waste Type (Hazardous, Non-Hazardous), Service Type (Collection & Transportation, Processing & Recycling, Disposal), Material (Soil, Sand & Gravel, Concrete, Bricks & Masonry, Wood, Metal, Other), Source (Residential, Commercial, Industrial, Infrastructure & Public Works), and Regional Analysis, 2026 - 2033

Construction and Demolition Waste Management Market Size and Trend Analysis

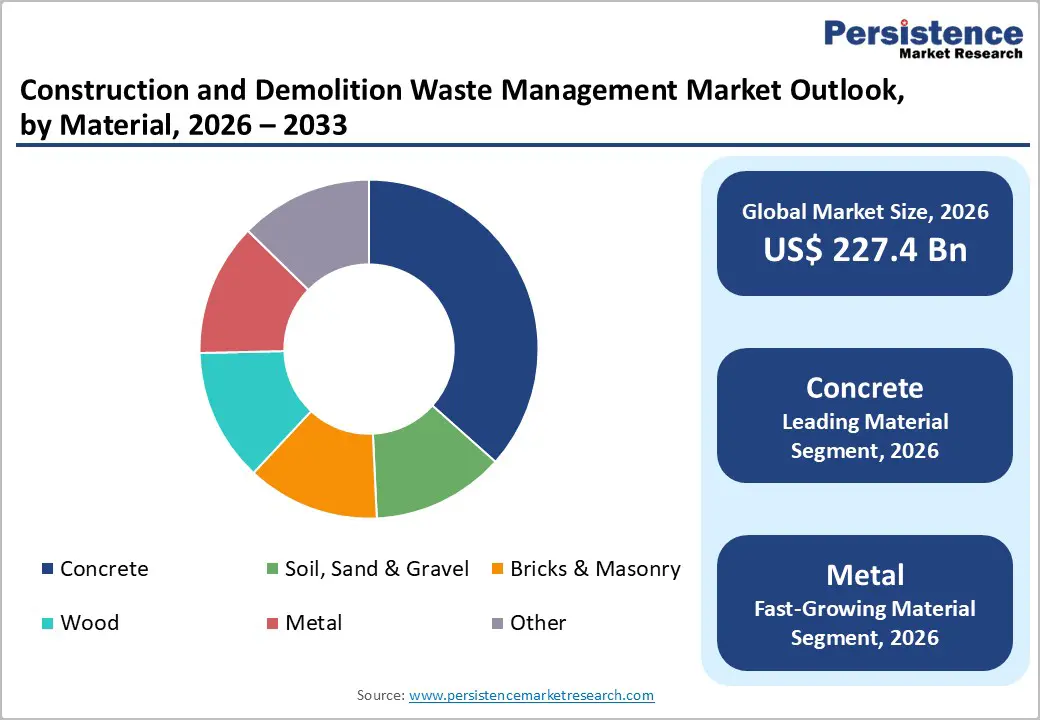

The global construction and demolition (C&D) waste management market size is expected to be valued at US$ 227.4 billion in 2026 and projected to reach US$ 322.1 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033. This sustained growth is fundamentally anchored in accelerating global construction output, tightening landfill diversion mandates across developed markets, and the circular economy's rising priority on secondary materials recovery from demolition streams.

The United Nations Environment Programme (UNEP) estimates that construction and demolition activities generate approximately 40% of global solid waste volumes, creating an enormous and structurally growing management challenge that governments, municipalities, and private operators are compelled to address through invested infrastructure and policy frameworks, each of which directly expands the addressable TIC service base and contracted waste management revenue.

Key Industry Highlights

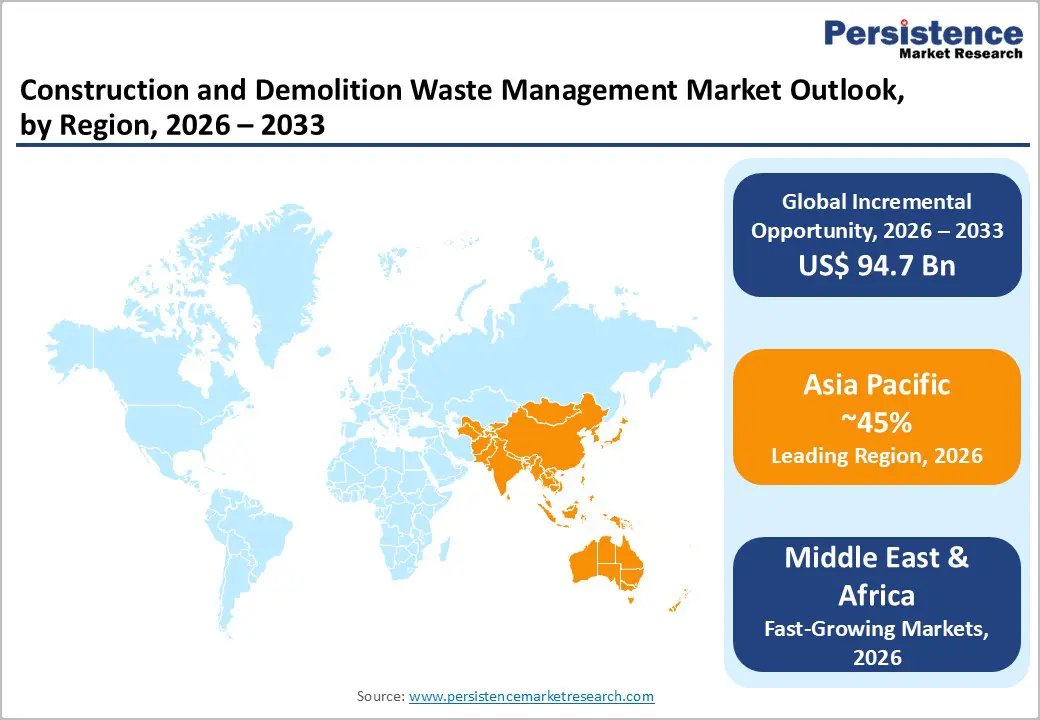

- Leading Region: Asia Pacific commands the largest share of the global C&D waste management market, anchored by China's 2.4 billion tonnes of annual construction waste and India's infrastructure pipeline, making it the world's highest-volume C&D waste generation region.

- Fastest Growing Region: The MEA region is projected to record the highest CAGR through 2033, driven by Saudi Arabia's Vision 2030 100% C&D diversion targets, UAE Green Building Code recycling mandates, and Africa's rapidly expanding urbanization-driven construction activity.

- Dominant Waste Type: Non-hazardous C&D waste leads with approximately 82% market share in 2025, dominated by inert concrete, aggregate, and masonry streams that represent the structural majority of all construction and demolition activities globally.

- Fastest Growing Services: Processing and recycling is the fastest-growing service type, accelerated by EU 70% recovery mandates, circular economy procurement requirements, and recycled concrete aggregate (RCA) commanding certified commercial pricing under EN 12620 and ASTM C33 standards.

- Key Market Opportunity: Saudi Arabia's NWMC and UAE's municipal recycling enforcement are creating large, government-backed C&D processing contracts in an underpenetrated market. Operators who establish licensed MRF capacity and secondary aggregate certification now will secure durable first-mover positions ahead of competitive intensification through 2033.

Market Dynamics

Drivers – Stringent Global Landfill Diversion Targets and Circular Economy Legislation Are Structurally Expanding Recycling and Processing Demand

For C&D waste management operators, the most consequential market signal is the progressive tightening of landfill diversion and material recovery targets by governments across Europe, North America, and Asia Pacific, a shift that is converting what were previously low-margin disposal contracts into higher-value processing and recycling service opportunities. The European Union's Construction Products Regulation and Waste Framework Directive (2008/98/EC) set a binding target for 70% C&D waste recovery by weight across EU member states, and the recast EU Construction Products Regulation (2024) extends material passport requirements that effectively mandate traceability of recovered materials, rewarding operators with certified processing and secondary materials trading capabilities.

The U.S. EPA has identified C&D debris as one of the largest waste streams in the country, generating an estimated 600 million tonnes annually, and growing number of U.S. states are adopting mandatory C&D recycling ordinances modeled on California's CALGreen Building Code requirements. Operators who invest in advanced material recovery facilities (MRFs) targeting concrete, metal, and clean aggregate recovery streams are positioned to capture premium tipping fees and secondary commodity revenue simultaneously.

Accelerating Global Infrastructure Investment Cycles Are Generating Record-Volume C&D Waste Streams That Require Managed Disposal and Recovery

Infrastructure investment programs worldwide are simultaneously producing the raw feedstock of C&D waste management demand, demolition volumes from old stock clearance and construction waste from new build activity, at scales that are stretching the capacity of existing management infrastructure and rewarding operators who can deploy rapidly.

The U.S. Infrastructure Investment and Jobs Act (IIJA) committed USD 1.2 trillion to roads, bridges, transit, and utilities, with significant demolition of aging structures preceding new construction, each generating C&D waste streams requiring permitted management. Across Asia, the Asian Development Bank (ADB) estimates the region requires USD 26 trillion in infrastructure investment through 2030, with demolition of inadequate existing stock in rapidly urbanizing cities generating C&D volumes at a pace that local waste management infrastructure has consistently struggled to absorb.

Restraints - Contamination of Mixed C&D Waste Streams Suppresses Recycling Yields and Undermines Secondary Material Economics

The structural challenge that constrains C&D waste recycling economics most severely is the inherent heterogeneity of demolition waste streams, which intermix concrete rubble, gypsum board, treated timber, asbestos-containing materials, and contaminated soil in proportions that vary dramatically by project type, age of demolished structure, and contractor sorting discipline at source.

The European Environment Agency (EEA) has documented that contamination rates in mixed C&D streams can reduce recyclable material yield by 30–50%, requiring costly sorting, pre-treatment, and in some cases specialized disposal that eliminates the margin advantage of recycling over landfill. For operators without the ability to enforce source-separation at demolition sites, a capability that requires contractual leverage and trained site supervision, mixed stream contamination directly suppresses processing facility throughput and secondary material quality, making it difficult to compete for premium recycled aggregate and metal sales contracts that underpin recycling-led business models.

Regulatory Fragmentation Across Jurisdictions Creates Compliance Complexity That Favors Large Operators and Disadvantages New Entrants

C&D waste management operates under a patchwork of national, regional, and municipal regulations governing permitted disposal sites, material classification, hazardous waste handling, transport manifests, and recycling credit accounting, a complexity that imposes disproportionate compliance costs on smaller operators and new market entrants seeking multi-jurisdictional scale. In the European Union, while the Waste Framework Directive sets the top-level framework, implementation varies materially across 27 member states in areas including end-of-waste criteria for recycled aggregates, treatment standards for hazardous C&D materials, and extended producer responsibility for construction products, each requiring separate permitting, reporting systems, and specialist legal counsel.

The practical consequence for market entrants is that establishing a compliant, multi-site C&D waste processing and disposal operation in a new European country typically requires 12–24 months of regulatory engagement before the first tonne of commercial waste can be accepted, creating a durable competitive moat for established licensed operators.

Opportunities - Processing & Recycling Service Segment Offers the Highest-Margin, Fastest-Growing Revenue Opportunity as Secondary Materials Command Premium Pricing

The processing and recycling segment is the fastest-growing service type in the C&D waste management market, and the most strategically consequential opportunity for operators willing to invest in advanced material recovery capabilities. Recycled concrete aggregate (RCA) now commands consistent commercial pricing in markets with strong circular procurement mandates, the UK Government's Construction Playbook and Dutch SBK Environmental Performance Database both specify recycled content requirements for public infrastructure contracts, and recovered steel from demolition routinely achieves scrap market pricing that partially offsets processing costs.

The Ellen MacArthur Foundation's circular economy analysis estimates that recovering materials from C&D waste streams at the rate technically achievable could save USD 100 billion annually in material input costs globally, providing a compelling economic case that procurement departments at major construction companies are increasingly acting on.

Middle East & Africa's Construction Expansion Is Creating the Fastest-Growing Regional Demand Base, With Greenfield C&D Waste Infrastructure Opportunity

The Middle East & Africa region is poised to be the fastest-growing C&D waste management market globally, and the opportunity is particularly acute because the region is building modern waste management infrastructure largely from a low baseline, meaning first-movers can establish long-term asset positions before competitive density increases. Saudi Arabia's Vision 2030 programme and the National Waste Management Center (NWMC) have explicitly prioritized C&D waste diversion as a national environmental target, committing to 100% diversion of inert C&D waste from landfill in new mega-project contracts for developments including NEOM and the Red Sea Project. The UAE's Ministry of Climate Change and Environment mandates 75% C&D waste recycling on all major construction and demolition projects under its Green Building Codes, backed by municipal inspection and penalty enforcement frameworks in Dubai and Abu Dhabi.

Category-wise Analysis

Waste Type Insights

Non-Hazardous C&D waste leads the waste type segment with approximately 82% market share in 2025, reflecting the reality that the vast majority of construction and demolition activities generate inert or non-hazardous materials, concrete rubble, clean aggregate, timber, and masonry, that do not require the specialized containment, transport manifesting, and disposal infrastructure mandated for hazardous materials.

The dominance of non-hazardous streams is reinforced by modern construction's shift toward newer building stock that contains fewer hazardous legacy materials such as asbestos, lead-based paint, and polychlorinated biphenyls (PCBs) relative to pre-1980 demolition projects. However, the hazardous segment commands significantly higher per-tonne management fees, with asbestos abatement services priced at multiples of standard rubble disposal, and its share is growing in regions undertaking large-scale demolition of post-war commercial and industrial building stock, creating a durable premium-margin niche within the broader non-hazardous volume market.

Service Type Insights

Collection & transportation leads the service type segment with approximately 44% market share in 2025, anchored by its role as the mandatory first step in every C&D waste management value chain, no processing, recycling, or disposal service can be delivered without initial collection from the demolition or construction site. The segment's leadership reflects the sheer volume throughput of C&D waste streams globally, where collection and transport logistics represent the highest-frequency touchpoint between waste generators and service providers.

Processing & recycling is the fastest-growing service segment, expanding at an above-average CAGR through 2033 as regulatory landfill diversion mandates and circular economy procurement requirements by major construction clients are compelling operators to invest in material recovery capabilities that generate both compliance value and secondary commodity revenue, a structural shift that is progressively upgrading the revenue quality of the C&D waste management sector.

Material Insights

Concrete leads the material segment with approximately 35% market share in 2025, a position rooted in concrete's physical dominance of construction and demolition waste streams globally, the European Environment Agency (EEA) attributes concrete and masonry together to over 60% of total EU C&D waste weight, and the mature commercial ecosystem that has developed around recycled concrete aggregate (RCA) as a viable secondary raw material for road sub-base, drainage fill, and lower-grade structural applications. Concrete's high density relative to other C&D materials means it disproportionately dominates weight-based market measurement, and its relative homogeneity when source-separated makes it the most technically tractable C&D material for recycling, with RCA achieving certified quality grades under EN 12620 in Europe and ASTM C33 in North America that unlock commercial secondary market pricing. Metal is the highest-value material by recovered tonne, sustaining premium collection economics, while Wood is the fastest-growing material segment driven by increasing timber construction adoption and biomass recovery markets.

Source Insights

Infrastructure & public works leads the source segment with approximately 38% market share in 2025, driven by the sheer volume of C&D waste generated by large-scale public infrastructure projects, road construction and rehabilitation, bridge demolition and replacement, railway and metro tunneling, and port development, each generating excavation soil and demolition rubble volumes that dwarf residential or commercial project waste per contract.

Government infrastructure programs create predictable, large-volume, long-duration C&D waste management contracts that are particularly attractive to large operators, as they provide revenue visibility and asset utilization stability that smaller, project-by-project residential contracts cannot match. The U.S. Federal Highway Administration (FHWA) documents that highway construction generates an estimated 100–200 million tonnes of reclaimed asphalt pavement (RAP) and aggregate waste annually in the U.S. alone, waste streams that established operators with asphalt recycling and aggregate processing infrastructure can convert from cost liabilities into revenue-generating secondary material supply positions.

Regional Insights

North America Construction and Demolition Waste Management Market Trends and Insights

North America is a mature, scale-driven C&D waste management market where large integrated operators dominate through permitted landfill networks, permitted processing infrastructure, and regulatory relationships across federal, state, and municipal levels. The U.S. EPA's C&D debris management framework and the proliferation of state-level mandatory recycling ordinances modeled on CALGreen are progressively shifting the revenue mix toward higher-margin processing and recycling services. As the IIJA's infrastructure investment wave generates demolition and excavation waste at accelerating volumes, operators with MRF capacity and secondary aggregate sales channels are positioned to benefit disproportionately from the region's evolving contract structure.

U.S. Construction and Demolition Waste Management Market Size

The United States commands approximately 82% of the North American C&D waste management market, generating an estimated 600 million tonnes of C&D debris annually per the U.S. EPA, the world's single largest national C&D waste stream. The IIJA's infrastructure renewal pipeline and growing state recycling mandates are structurally elevating processing demand. Operators like Waste Management (WM), Republic Services, and Clean Harbors are investing in expanded C&D MRF capacity to capture the growing processing and recycling margin premium as landfill diversion requirements tighten at the state level through the forecast period.

Europe Construction and Demolition Waste Management Market Trends and Insights

Europe is the global leader in C&D waste regulatory sophistication, with the EU Waste Framework Directive's 70% recovery target, Construction Products Regulation material passports, and the European Green Deal circular economy action plan collectively driving the region's progressive transition from landfill-dominated to recycling-led C&D waste management. The Netherlands, Belgium, and Denmark consistently achieve C&D waste recovery rates above 90%, benchmarks that are diffusing to Southern and Eastern European markets through EU cohesion fund-supported infrastructure investment.

Germany Construction and Demolition Waste Management Market Size

Germany holds approximately 21% of the European C&D waste management market, underpinned by its large construction and industrial base and the Kreislaufwirtschaftsgesetz (KrWG) circular economy and waste act, which mandates strict separation and recycling of C&D materials. Germany produces an estimated 200 million tonnes of C&D waste annually, with a high proportion processed into recycled aggregates that serve the country's large road construction market. Remondis and Veolia's German operations are major processors, and the country's mature recycled aggregate certification infrastructure sustains premium secondary material economics.

U.K. Construction and Demolition Waste Management Market Size

The United Kingdom accounts for approximately 15% of the European C&D waste management market. The UK's Construction Playbook, which mandates recycled material specification in public sector contracts, and the Environment Agency's Site Waste Management Plan requirements are driving above-average growth in C&D recycling demand. The HS2 rail project and large-scale housing programs are generating substantial C&D waste volumes, and the UK's landfill tax escalator, currently above £100 per tonne, creates a strong financial incentive for recycling that supports premium MRF tipping fees.

France Construction and Demolition Waste Management Market Size

France represents approximately 13% of the European C&D waste management market. The Grand Paris Express, Europe's largest metro expansion project, and France's ambitious housing renovation program are generating large, sustained C&D waste streams in the Île-de-France region. France's Loi anti-gaspillage pour une économie circulaire (AGEC) mandates progressive increases in recycled content in public construction, and Veolia operates the majority of France's permitted C&D processing infrastructure, sustaining high market concentration at the regional processing level.

Asia Pacific Construction and Demolition Waste Management Market Trends and Insights

Asia Pacific is the largest and fastest-growing regional C&D waste management market, propelled by the world's highest construction activity volumes in China, India, and Southeast Asia. China generates an estimated 2.4 billion tonnes of construction waste annually according to the Ministry of Housing and Urban-Rural Development (MOHURD), making it by far the world's largest source of C&D waste, and the Chinese government's 14th Five-Year Plan has set explicit targets for construction waste reduction and resource recycling that are stimulating rapid investment in processing infrastructure. For international operators, Asia Pacific's scale represents the most consequential long-term growth opportunity, though market entry requires local regulatory navigation and partnership strategies that differ markedly by country.

India Construction and Demolition Waste Management Market Size

India holds approximately 16% of the Asia Pacific C&D waste management market, with urban construction activity driving rapidly expanding waste volumes. The Ministry of Environment, Forest and Climate Change (MoEFCC) notified the Construction and Demolition Waste Management Rules, 2016, mandating waste management plans for projects exceeding 20,000 m² and requiring C&D waste processing facility development by municipalities in cities over 1 million population. India's National Infrastructure Pipeline (NIP) and smart city construction programs are amplifying C&D waste volumes, with formal management infrastructure still significantly underpenetrated relative to waste volumes, creating greenfield opportunity for compliant operators.

Japan Construction and Demolition Waste Management Market Size

Japan accounts for approximately 13% of the Asia Pacific C&D waste management market and operates one of the world's most mature C&D recycling systems. The Construction Material Recycling Law (Law No. 104, 2000) mandates source-separation and recycling of concrete, asphalt, wood, and specified metals at construction and demolition sites, achieving C&D recycling rates above 97% for concrete and asphalt. Japan's aging building stock, with significant volume of pre-earthquake-standard buildings requiring demolition and replacement under the Building Standards Act, is sustaining consistent high-value C&D waste volumes through the forecast period.

Australia Construction and Demolition Waste Management Market Size

Australia represents approximately 8% of the Asia Pacific C&D waste management market. The National Waste Policy Action Plan 2019 targets 80% waste diversion from landfill by 2030, with C&D waste identified as a priority stream. Australia's state-level landfill levies, ranging from AUD 75 to AUD 160+ per tonne in key states, create strong financial incentives for C&D recycling, and major operators including Cleanaway Waste Management and international majors, are investing in expanded C&D MRF capacity to serve the country's active infrastructure and urban development pipeline.

Middle East & Africa Construction and Demolition Waste Management Market Trends and Insights

The Middle East & Africa region is the fastest-growing C&D waste management market globally, driven by the Gulf's unprecedented construction boom and progressive formalization of waste management regulations across GCC nations. The UAE and Saudi Arabia lead regional regulatory development, with mandatory C&D recycling targets and green building codes that are creating formal market structures where informal waste disposal previously dominated. Africa's growing urbanization and infrastructure investment, supported by the African Development Bank (AfDB), are creating nascent C&D waste management markets that will expand rapidly as regulatory frameworks formalize.

Saudi Arabia Construction and Demolition Waste Management Market Size

Saudi Arabia holds approximately 32% of the Middle East & Africa C&D waste management market, driven by its position as the region's largest construction economy and the Vision 2030 giga-project pipeline generating demolition and construction waste at unprecedented scales. The National Waste Management Center (NWMC) is actively tendering C&D waste processing facility contracts aligned with the Kingdom's 100% inert C&D diversion target, creating large, government-backed contract opportunities for qualified operators. Saudi Arabia's formal C&D waste management market is in rapid early-growth phase, rewarding first movers with licensed processing capacity and certified secondary aggregate products.

United Arab Emirates Construction and Demolition Waste Management Market Size

The United Arab Emirates represents approximately 22% of the MEA C&D waste market. Dubai's Green Building Regulations and Abu Dhabi's Estidama Pearl Rating System mandate 75% C&D waste recycling on major projects, backed by enforcement through municipality inspection programs. The UAE's active construction pipeline, driven by Expo City Dubai legacy development, infrastructure expansion, and residential construction for a growing expatriate population, sustains large, consistent C&D waste volumes that support economically viable processing operations and secondary aggregate markets for road and infrastructure contractors.

Israel Construction and Demolition Waste Management Market Size

Israel accounts for approximately 6% of the MEA C&D waste management market. Israel's Regulations for Treatment of Construction and Demolition Waste (2011) established mandatory sorting and recycling requirements for construction sites, and the Ministry of Environmental Protection reports C&D recycling rates exceeding 80%, among the highest in the region. Israel's compact geography, high landfill gate fees, and active residential and infrastructure construction create a mature market dynamic where recycled aggregate producers compete directly with quarry-sourced materials on quality and price, sustaining commercial recycling economics without heavy regulatory subsidy.

Competitive Landscape

The global construction and demolition waste management market is structurally driven by scale advantages and control over licensed infrastructure, where ownership of permitted landfills, processing facilities, and transfer stations in high-demand regions creates strong pricing power and significant entry barriers. Established operators dominate by integrating collection, sorting, processing, and material recovery across the full value chain, enabling higher margin capture through secondary aggregates, metals, and recycled materials.

Strategically, leading players are expanding vertically into recycled material trading, enhancing digital waste tracking platforms to support corporate sustainability reporting, and forming partnerships with governments for infrastructure development projects, particularly in emerging markets. At the same time, competition is intensifying in niche areas such as hazardous waste handling and compliance-focused digital solutions, where specialized capabilities allow smaller firms to compete effectively despite the dominance of large integrated waste management networks.

Key Developments

- April 2026: Municipal Corporation of Gurugram announced plans to set up seven construction and demolition waste collection points across the city to improve waste segregation, recycling efficiency, and support compliance with solid waste management regulations.

- December 2025: Holcim expanded its construction and demolition waste recycling business through the acquisition of three recycling firms across the UK, Germany, and France, strengthening its circular construction strategy and increasing annual processing capacity by around 1.3 million tons.

- June 2025: Freehaven Materials, in collaboration with equipment manufacturer CDE, commissioned a 150 tonnes-per-hour construction and demolition waste recycling facility in Brookhaven, driven by landfill closures and rising demand for recycled aggregates in infrastructure and construction projects.

Companies Covered in Construction and Demolition Waste Management Market

- Veolia Environment S.A.

- Waste Connections

- Clean Harbors, Inc.

- Remondis

- Republic Services

- FCC Environment Limited

- WM Intellectual Property Holdings, LLC (Waste Management)

- Kiverco

- Daiseki Co., Ltd.

- Windsor Waste

- Casella Waste Systems, Inc.

- Renewi plc

- GFL Environmental Inc.

- Metso Corporation

- Cleanaway Waste Management Limited

- Biffa plc

- Covanta Holding Corporation

Frequently Asked Questions

The construction & demolition waste management market is valued at US$ 227.4 billion in 2026 and is projected to reach US$ 322.1 billion by 2033.

Demand is driven by stricter landfill regulations, large-scale infrastructure spending, and high waste generation from construction activities globally.

Asia Pacific leads with about 39% market share due to high construction waste volumes from China, India, and Southeast Asia.

The Middle East’s expanding infrastructure and recycling mandates present the strongest near-term growth opportunity.

Key players include Veolia Environment S.A., Waste Management Inc., Republic Services, Remondis, GFL Environmental Inc., and Clean Harbors Inc.