Industry: Healthcare

Published Date: February-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 184

Report ID: PMRREP33259

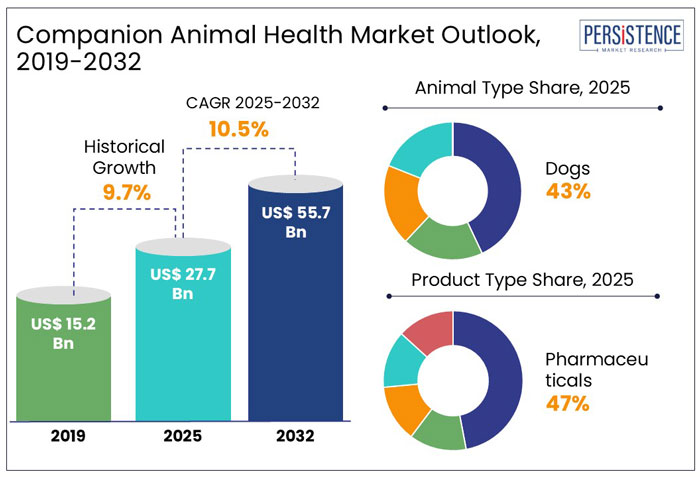

The global companion animal health market size is anticipated to reach US$ 27.7 Bn in 2025. It is predicted to exhibit a CAGR of 10.5% from 2025 to 2032 to attain a size of US$ 55.7 Bn by 2032.

Urban households are witnessing an increased adoption of companion animals. Growing awareness regarding pet health has facilitated higher spending on preventive care, regular check-ups, and wellness products. For example,

The industry is witnessing innovations in technology with the introduction of AI-powered diagnostic tools and wearable health monitoring devices for pets. Enhanced digital health platforms further enable remote consultations.

Key Highlights of the Companion Animal Health Market

|

Global Market Attributes |

Key Insights |

|

Market Size (2025E) |

US$ 27.7 Bn |

|

Market Value Forecast (2032F) |

US$ 55.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

10.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.7% |

Study Reveals Significant Impact of Pandemic on Pet Health and Veterinary Service Accessibility

The global companion animal health market growth was steady at a CAGR of 9.7% in the historical period from 2019 to 2024. This period witnessed a rise in pet ownership, increased focus on preventive healthcare, and innovation in veterinary diagnostics. There was a growth in demand for oral and topical pharmaceuticals to treat infections and chronic diseases among pets.

The COVID-19 pandemic caused initial disruptions in supply chains and veterinary visits, yet the industry rebounded with increased pet adoption during lockdowns. Telehealth services for pets saw significant adoption as social distancing norms limited physical veterinary consultations. For example,

Rising Demand for Personalized Nutrition and Genetic Testing Solutions to Boost Sales through 2032

The companion animal health industry is predicted to showcase a CAGR of 10.5% through 2032. The forecast period is anticipated to witness continued adoption of digital veterinary services and wearable devices.

Rising demand for personalized nutrition and genetic testing solutions for pets is predicted to augment sales. Emerging markets are likely to see growth in veterinary clinics and diagnostic labs, as well as high spending by millennials in pet healthcare. For instance,

Growth Drivers

Predictive AI Models to Enable Early Intervention and Reduce Long-term Healthcare Costs

AI algorithms analyze X-rays, CT scans, and MRIs to detect abnormalities like fractures, tumors, and organ dysfunction. Faster and more accurate diagnostics reduce the time required for veterinary evaluations. For example,

AI models analyze health records, genetic data, and lifestyle factors to predict potential health issues. Early identification of diseases allows preventive interventions, reducing long-term healthcare costs.

AI-driven algorithms customize treatment protocols based on an individual pet’s health history, genetics, and response to previous treatments. This approach optimizes medication dosages and minimizes side effects. Some veterinary platforms use machine learning to recommend tailored nutritional and medical regimens.

Financial Constraints to Compel Pet Owners to Delay or Avoid Vital Medical Treatments

Despite the increasing pet adoption rates and awareness of veterinary advancements, insurance coverage for pets remains underutilized globally. Without insurance, pet owners face significant financial burdens for routine and emergency care. For instance,

Pet owners without insurance are less likely to opt for innovative procedures or preventive care.

Increasing Adoption of Fitness Tracking for Pets to Spur Developments in Wearable Technology

Wearable devices help in tracking key physiological metrics, including heart rate, body temperature, and respiratory rate, for early detection of health issues. They are also useful in managing chronic conditions like heart disease and respiratory disorders. For instance,

Wearable pet health monitoring devices track daily activity levels, steps, and calorie expenditure to promote healthy lifestyles in pets. They also assist in identifying changes in activity patterns that may indicate underlying health problems.

These devices also assist in real-time location tracking to prevent pet loss. Geofencing features alert owners if pets wander beyond a designated area. For instance,

Animal Type Insights

Increasing Emotional Support Role of Dogs Strengthens their Position in the Market

Based on animal type, dogs are predicted to hold a share of 43% in 2025. Dogs are the most common companion animal across all regions, with an estimated around 470 million dogs globally in 2023. In Europe, Germany and France have some of the highest dog ownership rates in the world. For instance,

Dogs are widely seen as emotional support animals as they provide companionship, reduce stress, and offer emotional well-being benefits, making them integral to the family unit in several cultures. Dogs typically require more frequent and specialized veterinary care compared to other companion animals. They are more likely to experience a variety of health issues, such as joint problems, obesity, and cancer, which drive higher spending on health services. For instance,

Product Type Insights

Surging Cases of Canine Cancer and Age-related Illnesses to Propel Pharmaceutical Demand

In terms of product type, pharmaceuticals are anticipated to hold a share of 47% in 2025. Companion animals are susceptible to chronic diseases like arthritis, obesity, diabetes, and cancer along with infectious diseases like leptospirosis and parvovirus. For instance,

Increasing awareness of preventive care has led to the rising administration of vaccines, deworming agents, and parasitic control medications. Routine vaccination for rabies, distemper, and leptospirosis has become a standard practice in developed and emerging markets.

Demand for Innovative Pet Healthcare Solutions Grows in North America as Owners Seek Better Treatment Options

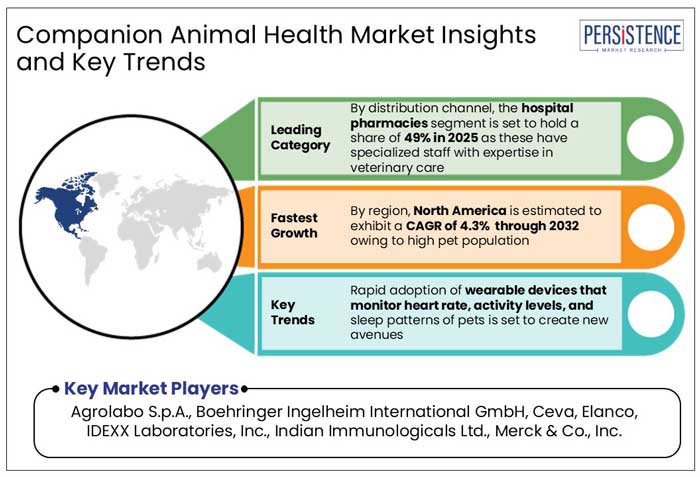

North America companion animal health market is projected to hold a share of 39% in 2025. The region has one of the highest pet ownership rates worldwide. Companion animals are integral parts of households in North America. High pet ownership rate directly drives demand for veterinary care, pharmaceuticals, diagnostics, and wellness products. For example,

The region leads in pet healthcare expenditure, driven by high disposable income and pet owners' willingness to spend on innovative veterinary treatments. Higher spending capabilities enable pet owners to access premium healthcare services and innovative treatments for their pets.

Surging Number of Veterinary Clinics across Europe Enhances Availability of Comprehensive Pet Care

Europe companion animal health market will likely generate a share of 25% in 2025. The region has a culturally established pet-keeping tradition, with millions of households owning dogs, cats, and other companion animals. The large pet population drives demand for veterinary services, pharmaceuticals, and preventive care products. For instance,

Europe has a robust veterinary healthcare network, including specialty hospitals, diagnostic labs, and veterinary clinics. Availability of innovative veterinary services supports the adoption of innovative healthcare solutions for pets.

Increasing Pet Insurance Adoption in Asia Pacific Encourages High Spending on Novel Treatments

Asia Pacific companion animal health market is estimated to account for a share of 23% in 2025. Growing middle-class population and changing societal norms in the region have led to a surge in pet ownership, particularly dogs and cats. The rising pet population directly increases the demand for veterinary care, pharmaceuticals, and wellness products. For instance,

As economies in the region experience rapid growth, disposable incomes have risen, enabling pet owners to spend more on healthcare and wellness for their animals. Higher disposable incomes drive demand for premium veterinary services, pharmaceuticals, and diagnostic products.

Pet insurance adoption is gradually increasing in Asia Pacific as companies enter the market and offer tailored insurance plans for companion animals. Pet insurance helps offset the costs of advanced treatments, encouraging pet owners to seek comprehensive healthcare services.

Companies in the companion animal health industry are investing in research and development activities to develop new and innovative veterinary pharmaceuticals, vaccines, diagnostics, and treatment options. Boehringer Ingelheim launched NexGard COMBO, a broad-spectrum parasiticide for cats, in 2022.

Businesses are diversifying their offerings, including pharmaceuticals, diagnostic kits, wellness products, and speciality diets to capture a broader market. A diverse product portfolio enables companies to cater to different customer needs and capture various market segments. Merck Animal Health extended its product line in 2023 by introducing the Bravecto Plus range for cats, a long-lasting flea and tick treatment.

Mergers and acquisitions enable companies to access new technologies, broaden market reach, and enhance operational efficiencies. They help companies to access innovative solutions and penetrate new geographical markets. Zoetis acquired Basepaws, a pet genetics company, in 2022 to strengthen its position in diagnostics and precision health.

Key Industry Developments

|

Report Attributes |

Details |

|

Historical Data/Actuals |

2019 – 2024 |

|

Forecast Period |

2025 – 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Animal Type

By Product Type

By Distribution Channel

By End Use

By Region

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 27.7 Bn in 2025.

Pharmaceuticals are predicted to lead with a share of 47% in 2025.

Agrolabo S.p.A., Boehringer Ingelheim International GmbH, and Ceva are a few leading players.

The industry is estimated to rise at a CAGR of 10.5% through 2032.

North America is projected to hold the largest share of the industry in 2025.