1. Executive Summary

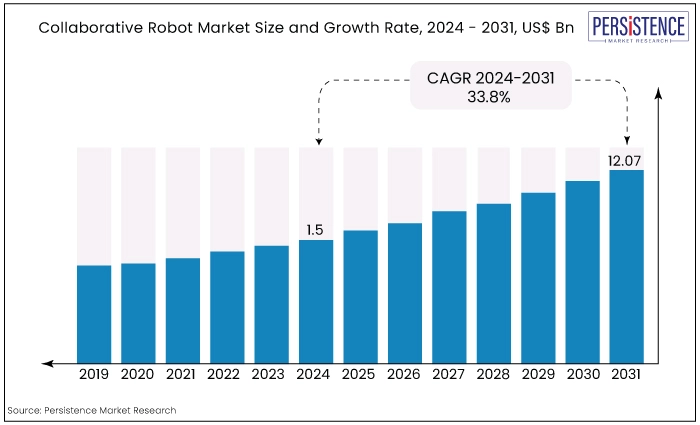

1.1. Global Collaborative Robot Market Snapshot, 2024 and 2031

1.2. Market Opportunity Assessment, 2024 - 2031, US$ Mn

1.3. Key Market Trends

1.4. Future Market Projections

1.5. Premium Market Insights

1.6. Industry Developments and Key Market Events

1.7. PMR Analysis and Recommendations

2. Market Overview

2.1. Market Scope and Definition

2.2. Market Dynamics

2.2.1. Drivers

2.2.2. Restraints

2.2.3. Opportunity

2.2.4. Challenges

2.2.5. Key Trends

2.3. Macro-Economic Factors

2.3.1. Global Sectorial Outlook

2.3.2. Global GDP Growth Outlook

2.3.3. Global IT Spending Outlook

2.3.4. Global Labor Market Outlook

2.3.5. Industrial Growth Outlook

2.4. COVID-19 Impact Analysis

2.5. Forecast Factors - Relevance and Impact

3. Value Added Insights

3.1. Robot Adoption Analysis

3.2. Technology Roadmap Analysis

3.3. Ecosystem Mapping

3.4. Regulatory Landscape

3.5. Value Chain Analysis

3.6. Key Deals and Mergers

3.7. PESTLE Analysis

3.8. Porter’s Five Force Analysis

4. Price Trend Analysis, 2018 - 2031

4.1. Key Highlights

4.2. Key Factors Impacting Collaborative Robot Prices

4.3. Pricing Analysis

4.3.1. Average Monthly Lease Cost for Collaborative Robot

4.3.2. Subscription-based Pricing Analysis

5. Global Collaborative Robot Market Outlook: Historical (2018 - 2023) and Forecast (2024 - 2031)

5.1. Key Highlights

5.1.1. Market Volume (Units) Projections

5.1.2. Market Size (US$ Mn) and Y-o-Y Growth

5.1.3. Absolute $ Opportunity

5.2. Market Size (US$ Mn) Analysis and Forecast

5.2.1. Historical Market Size (US$ Mn) Analysis, 2018-2022

5.2.2. Current Market Size (US$ Mn) Analysis and Forecast, 2023-2031

5.3. Global Collaborative Robot Market Outlook: Payload Capacity

5.3.1. Introduction / Key Findings

5.3.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Payload Capacity, 2018 - 2022

5.3.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Payload Capacity, 2023 - 2031

5.3.3.1. Up to 5 kg

5.3.3.2. 5-10 kg

5.3.3.3. 10-25 kg

5.3.3.4. More than 25 kg

5.4. Market Attractiveness Analysis: Payload Capacity

5.5. Global Collaborative Robot Market Outlook: Application

5.5.1. Introduction / Key Findings

5.5.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Application, 2018 - 2022

5.5.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Application, 2023 - 2031

5.5.3.1. Material Handling

5.5.3.2. Assembling & Dissembling

5.5.3.3. Welding & Soldering

5.5.3.4. Dispensing

5.5.3.5. Packaging

5.5.3.6. Others

5.6. Market Attractiveness Analysis: Application

5.7. Global Collaborative Robot Market Outlook: Industry

5.7.1. Introduction / Key Findings

5.7.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Industry, 2018 - 2022

5.7.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Industry, 2023 - 2031

5.7.3.1. Automotive

5.7.3.2. Electronics and Semiconductor

5.7.3.3. Metal & Machining

5.7.3.4. Plastics & Polymers

5.7.3.5. Healthcare and pharmaceuticals

5.7.3.6. Food and Beverages

5.7.3.7. Others

5.8. Market Attractiveness Analysis: Industry

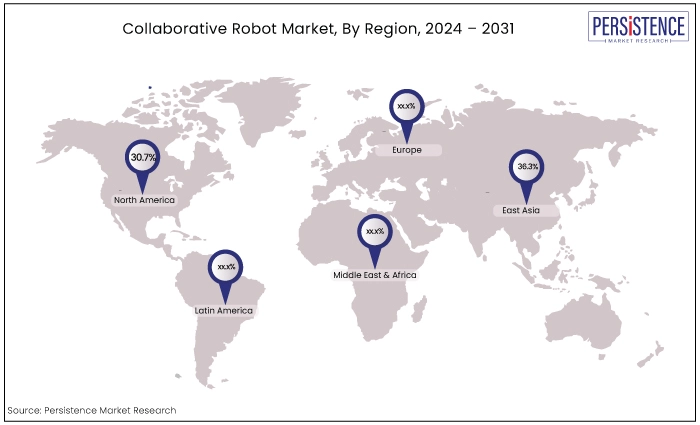

6. Global Collaborative Robot Market Outlook: Region

6.1. Key Highlights

6.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Region, 2018 - 2022

6.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Region, 2023 - 2031

6.3.1. North America

6.3.2. Europe

6.3.3. East Asia

6.3.4. South Asia and Oceania

6.3.5. Latin America

6.3.6. Middle East & Africa

6.4. Market Attractiveness Analysis: Region

7. North America Collaborative Robot Market Outlook: Historical (2018 - 2023) and Forecast (2024 - 2031)

7.1. Key Highlights

7.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Market, 2018 - 2022

7.2.1. By Country

7.2.2. By Payload Capacity

7.2.3. By Application

7.2.4. By Industry

7.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Country, 2023 - 2031

7.3.1. U.S.

7.3.2. Canada

7.4. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Payload Capacity, 2023 - 2031

7.4.1. Up to 5 kg

7.4.2. 5-10 kg

7.4.3. 10-25 kg

7.4.4. More than 25 kg

7.5. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Application, 2023 - 2031

7.5.1. Material Handling

7.5.2. Assembling & Dissembling

7.5.3. Welding & Soldering

7.5.4. Dispensing

7.5.5. Packaging

7.5.6. Others

7.6. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Industry, 2023 - 2031

7.6.1. Automotive

7.6.2. Electronics and Semiconductor

7.6.3. Metal & Machining

7.6.4. Plastics & Polymers

7.6.5. Healthcare and pharmaceuticals

7.6.6. Food and Beverages

7.6.7. Others

7.7. Market Attractiveness Analysis

8. Europe Collaborative Robot Market Outlook: Historical (2018 - 2023) and Forecast (2024 - 2031)

8.1. Key Highlights

8.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Market, 2018 - 2022

8.2.1. By Country

8.2.2. By Payload Capacity

8.2.3. By Application

8.2.4. By Industry

8.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Country, 2023 - 2031

8.3.1. Germany

8.3.2. France

8.3.3. U.K.

8.3.4. Italy

8.3.5. Spain

8.3.6. Russia

8.3.7. Türkiye

8.3.8. Rest of Europe

8.4. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Payload Capacity, 2023 - 2031

8.4.1. Up to 5 kg

8.4.2. 5-10 kg

8.4.3. 10-25 kg

8.4.4. More than 25 kg

8.5. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Application, 2023 - 2031

8.5.1. Material Handling

8.5.2. Assembling & Dissembling

8.5.3. Welding & Soldering

8.5.4. Dispensing

8.5.5. Packaging

8.5.6. Others

8.6. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Industry, 2023 - 2031

8.6.1. Automotive

8.6.2. Electronics and Semiconductor

8.6.3. Metal & Machining

8.6.4. Plastics & Polymers

8.6.5. Healthcare and pharmaceuticals

8.6.6. Food and Beverages

8.6.7. Others

8.7. Market Attractiveness Analysis

9. East Asia Collaborative Robot Market Outlook: Historical (2018 - 2023) and Forecast (2024 - 2031)

9.1. Key Highlights

9.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Market, 2018 - 2022

9.2.1. By Country

9.2.2. By Payload Capacity

9.2.3. By Application

9.2.4. By Industry

9.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Country, 2023 - 2031

9.3.1. China

9.3.2. Japan

9.3.3. South Korea

9.4. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Payload Capacity, 2023 - 2031

9.4.1. Up to 5 kg

9.4.2. 5-10 kg

9.4.3. 10-25 kg

9.4.4. More than 25 kg

9.5. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Application, 2023 - 2031

9.5.1. Material Handling

9.5.2. Assembling & Dissembling

9.5.3. Welding & Soldering

9.5.4. Dispensing

9.5.5. Packaging

9.5.6. Others

9.6. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Industry, 2023 - 2031

9.6.1. Automotive

9.6.2. Electronics and Semiconductor

9.6.3. Metal & Machining

9.6.4. Plastics & Polymers

9.6.5. Healthcare and pharmaceuticals

9.6.6. Food and Beverages

9.6.7. Others

9.7. Market Attractiveness Analysis

10. South Asia & Oceania Collaborative Robot Market Outlook: Historical (2018 - 2023) and Forecast (2024 - 2031)

10.1. Key Highlights

10.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Market, 2018 - 2022

10.2.1. By Country

10.2.2. By Payload Capacity

10.2.3. By Application

10.2.4. By Industry

10.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Country, 2023 - 2031

10.3.1. India

10.3.2. Southeast Asia

10.3.3. ANZ

10.3.4. Rest of South Asia & Oceania

10.4. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Payload Capacity, 2023 - 2031

10.4.1. Up to 5 kg

10.4.2. 5-10 kg

10.4.3. 10-25 kg

10.4.4. More than 25 kg

10.5. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Application, 2023 - 2031

10.5.1. Material Handling

10.5.2. Assembling & Dissembling

10.5.3. Welding & Soldering

10.5.4. Dispensing

10.5.5. Packaging

10.5.6. Others

10.6. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Industry, 2023 - 2031

10.6.1. Automotive

10.6.2. Electronics and Semiconductor

10.6.3. Metal & Machining

10.6.4. Plastics & Polymers

10.6.5. Healthcare and pharmaceuticals

10.6.6. Food and Beverages

10.6.7. Others

10.7. Market Attractiveness Analysis

11. Latin America Collaborative Robot Market Outlook: Historical (2018 - 2023) and Forecast (2024 - 2031)

11.1. Key Highlights

11.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Market, 2018 - 2022

11.2.1. By Country

11.2.2. By Payload Capacity

11.2.3. By Application

11.2.4. By Industry

11.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Payload Capacity, 2023 - 2031

11.3.1. Up to 5 kg

11.3.2. 5-10 kg

11.3.3. 10-25 kg

11.3.4. More than 25 kg

11.4. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Application, 2023 - 2031

11.4.1. Material Handling

11.4.2. Assembling & Dissembling

11.4.3. Welding & Soldering

11.4.4. Dispensing

11.4.5. Packaging

11.4.6. Others

11.5. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Industry, 2023 - 2031

11.5.1. Automotive

11.5.2. Electronics and Semiconductor

11.5.3. Metal & Machining

11.5.4. Plastics & Polymers

11.5.5. Healthcare and pharmaceuticals

11.5.6. Food and Beverages

11.5.7. Others

11.6. Market Attractiveness Analysis

12. Middle East & Africa Collaborative Robot Market Outlook: Historical (2018 - 2023) and Forecast (2024 - 2031)

12.1. Key Highlights

12.2. Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Market, 2018 - 2022

12.2.1. By Country

12.2.2. By Payload Capacity

12.2.3. By Application

12.2.4. By Industry

12.3. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Payload Capacity, 2023 - 2031

12.3.1. Up to 5 kg

12.3.2. 5-10 kg

12.3.3. 10-25 kg

12.3.4. More than 25 kg

12.4. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Application, 2023 - 2031

12.4.1. Material Handling

12.4.2. Assembling & Dissembling

12.4.3. Welding & Soldering

12.4.4. Dispensing

12.4.5. Packaging

12.4.6. Others

12.5. Current Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Industry, 2023 - 2031

12.5.1. Automotive

12.5.2. Electronics and Semiconductor

12.5.3. Metal & Machining

12.5.4. Plastics & Polymers

12.5.5. Healthcare and pharmaceuticals

12.5.6. Food and Beverages

12.5.7. Others

12.6. Market Attractiveness Analysis

13. Competition Landscape

13.1. Market Share Analysis, 2023

13.2. Market Structure

13.2.1. Competition Intensity Mapping By Market

13.2.2. Competition Dashboard

13.3. Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

13.3.1. Doosan Robotics

13.3.1.1. Overview

13.3.1.2. Segments and Payload Capacitys

13.3.1.3. Key Financials

13.3.1.4. Market Developments

13.3.1.5. Market Strategy

13.3.2. AUBO Robotics

13.3.3. ABB

13.3.4. KUKA

13.3.5. Yaskawa Electric Corporation

13.3.6. HAHN Group

13.3.7. Techman Robot

13.3.8. FANUC

13.3.9. Comau

13.3.10. Universal Robots (UR)

14. Appendix

14.1. Research Methodology

14.2. Research Assumptions

14.3. Acronyms and Abbreviations