Industry: Semiconductor Electronics

Published Date: March-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 198

Report ID: PMRREP4720

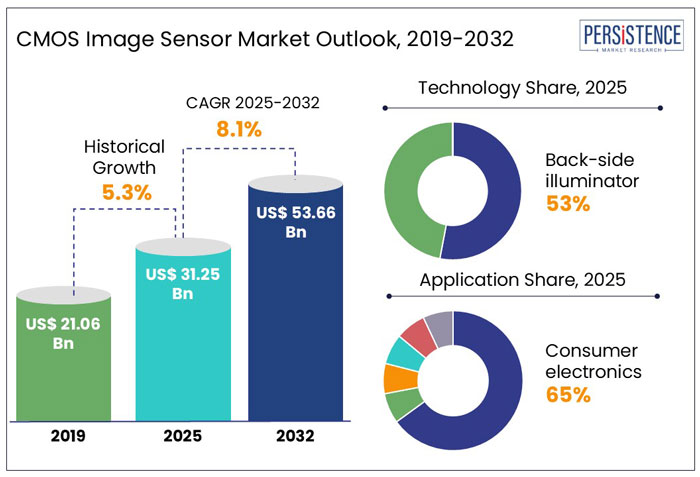

The global CMOS image sensor market size is anticipated to rise from US$ 31.25 Bn in 2025 to US$ 53.66 Bn by 2032. It is projected to witness a CAGR of 8.1% from 2025 to 2032. The increasing use of advanced CMOS image sensors in industrial automation, medical imaging, automotive safety systems, and smartphones is driven by the demand for high-resolution smartphone cameras and ADAS systems.

Sales of ADAS-equipped vehicles are predicted to increase by 14% yearly, with the automotive industry playing a significant role, especially for autonomous driving and LiDAR applications.

In consumer electronics and medical imaging, miniature CMOS sensors are extensively utilized in wearables, IoT devices, smart homes, and endoscopic and robotically assisted procedures. Security and surveillance are advancing as CMOS sensor capabilities improve through AI-driven video analytics, facial recognition, low-light performance, energy efficiency, and computational photography.

Key Highlights of the CMOS Image Sensor Market

|

Global Market Attributes |

Key Insights |

|

CMOS Image Sensor Market Size (2025E) |

US$ 31.25 Bn |

|

Market Value Forecast (2032F) |

US$ 53.66 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Rise in Security Concerns across the Globe Boost Innovation in Surveillance Sensors

As per Persistence Market Research, the global CMOS image sensor industry witnessed a CAGR of 5.3% in the historical period between 2019 and 2024. In the observed period, the focus on security and surveillance has driven demand for cameras with high-performance image sensors. Public safety concerns, smart city efforts, and AI-driven surveillance systems propelled the global video surveillance market to US$ 62 Bn in 2023. Manufacturers in Asia Pacific led the market by catering to the rapid urbanization and smart city projects in the region.

The rising number of burglary incidents has further emphasized the need for advanced surveillance systems. In the U.S., 619,811 burglary incidents were reported in 2021, marking a 31% decline from 2020. However, by 2023, burglary cases rose to 839,563, accounting for 13.1% of all property crimes.

In response to these security concerns, top producers have created picture sensors that are AI-powered, low-light, and have excellent resolution. As security systems advance, machine vision, biometric authentication, and edge AI processing are likely to stimulate innovation in image-sensing technology.

Innovation in Camera Technology Fosters Avenues for Implementation of Sensors

In the estimated timeframe from 2025 to 2032, the global market for CMOS Image Sensor is likely to showcase a CAGR of 8.1%. The demand for image sensor technology is increasing due to advances that enhance low-light performance, reduce power consumption, and improve resolution. High-performance CMOS image sensors are being developed to meet the needs of various industries, including industrial automation, medical imaging, automotive ADAS, security cameras, and smartphones.

Manufacturers such as Sony Semiconductor Solutions, Samsung Electronics, and OmniVision Technologies are innovating with stacked CMOS sensors, backside-illuminated (BSI) structures, and quantum dot technology to enhance dynamic range and low-light sensitivity. For example, Sony's IMX800 series, launched in May 2022, features dual-layer transistor pixels that improve night photography.

As artificial intelligence and edge computing become increasingly integrated into imaging applications, future innovations are expected to focus on 3D sensing, hyperspectral imaging, and neuromorphic vision sensors, advancing the industry further through 2032.

Growth Driver

Trend of Contemporary Photography Promotes the Experimentation with Image Sensors

The rise of computational photography is contributing positively to the quality and versatility of images captured by rofessional and smartphone cameras. Companies such as Apple, Samsung, and Google are utilizing AI-driven image processing techniques to enhance performance in low-light conditions, expand dynamic range, and improve detail.

The trend signifies a robust demand for computational photography, which is expected to extend to applications in smartphones, drones, and AR/VR devices. For example, in January 2024, Sony Semiconductor Solutions unveiled its Lytia image sensor lineup, designed with multi-layer transistor pixels to facilitate enhanced low-light and high dynamic range imaging.

Similarly, Samsung's ISOCELL Zoom Anyplace, announced in October 2023, introduces AI tracking to elevate zoom capabilities for mobile photography. Additionally, Apple's launch of the iPhone 15 Pro in September 2023 showcased a tetraprism 5x periscope zoom lens, further advancing long-range photography.

As advancements in AI and computational photography algorithms continue, the industry can anticipate that next-generation smartphone and automotive cameras will incorporate real-time HDR, AI-enhanced bokeh, and innovative periscope zoom technologies, ultimately reshaping the imaging landscape.

Market Restraining Factor

High Production and Maintenance Expenses of the Image Sensors Limits the Adoption

The persistent demand for innovation in sophisticated image sensors, coupled with exorbitant production costs, is a significant barrier to growth in the industry. The complexities involved in manufacturing, the use of high-end materials, and the constant push for innovation are driving these expenses sky-high. The widespread adoption of market-leading CMOS sensors is severely limited in cost-sensitive applications due to their dependence on expensive machinery and sophisticated production processes.

Sales are further constrained by intense competition and technical limitations. However, advanced packaging techniques and emerging technologies like 3D sensors are proving effective in reducing consumption. To stay relevant in this competitive landscape, companies must make substantial investments in research and development.

The intricate manufacturing process demands cutting-edge equipment and skilled labor, contributing to high production costs. Additionally, in the semiconductor sector, the presence of intangible property rights poses further challenges to market growth.

Key Market Opportunity

Consumer Electronics Sector Paves the Way for Miniature CMOS Sensors

The retail sector for consumer electronics is growing, particularly in wearables and IoT devices, which is driving up demand for miniature CMOS sensors with excellent resolution. The market for wearable technology is expanding globally, propelled by the sales of AR glasses, fitness trackers, and smartwatches. For sophisticated features like biometric verification, gesture recognition, and health monitoring, many gadgets depend on such sensors.

Leading companies like Apple, Samsung, and Huawei are seamlessly integrating CMOS sensors into their smartwatches, enhancing capabilities for ECG, SpO2 monitoring, and comprehensive sleep tracking. Notably, Apple's Vision Pro, released in February 2024, incorporates advanced eye-tracking CMOS sensors that facilitate gesture-based navigation in the dynamic field of mixed reality (MR).

For facial identification, motion detection, and real-time monitoring in smart home appliances and security systems, the IoT industry is utilizing CMOS sensors. The need for compact, high-performance sensors is projected to fuel innovation and market expansion in the future.

Application Insights

Rising Demand from Consumer Electronics Presents Prospects with Novel Features

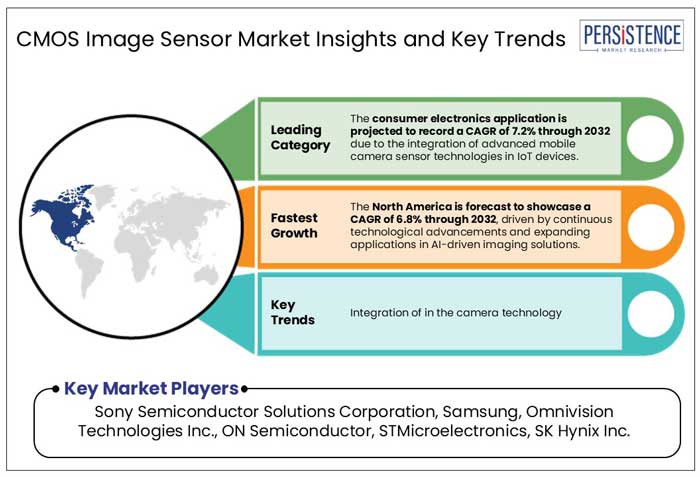

Based on the application, the consumer electronics segment is expected to account for 65% of the market share in 2025. This is due to the integration of advanced mobile camera sensor technologies in smartphones, tablets, and digital cameras. The consumer electronics application is projected to record a CAGR of 7.2% through 2032.

The growth of consumer electronics is influenced by the demand for high-resolution smartphone camera sensor capabilities, mixed reality headsets, action cameras, and social media content creation. Major smartphone manufacturers are focusing on enhancing camera capabilities through advanced CMOS image sensors, particularly in premium devices.

On the other hand, the automobile segment is emerging as the fastest-growing application, accounting for 23% in 2025. The emphasis is attributed to the adoption of ADAS and the development of autonomous vehicles. The emergence of electric vehicles and continuous innovation in automotive camera technologies are creating additional opportunities for CMOS image sensor implementations in the auto sector.

Technology Insights

Back Side Illuminator Technology Presents Opportunities for Advancement in Healthcare

The back-side illuminator (BSI) technology is projected to propel with its enhanced light sensitivity and low-light performance, making it ideal for medical imaging, industrial inspection, and smartphone cameras. The BSI segment is expected to account for 53% of the market share in 2025, with a CAGR of 7.3% from 2025 to 2032. To satisfy the increasing demand in endoscopy, surgical navigation, and high-speed industrial applications, companies such as Sony, OmniVision, and Samsung are spearheading the development of BSI CMOS sensors.

In the meanwhile, front-side illuminator (FSI) technology is expected to hold a 47% market share in 2025 and is still commonly utilized in applications that are cost-sensitive. Improvements in FSI-based CMOS image sensors are being fueled by ongoing research and development, which will increase their performance for consumer electronics, security surveillance, and vehicle ADAS systems.

As both technologies continue to progress, the rivalry between FSI and BSI sensors is anticipated to influence imaging applications in a variety of sectors in the future.

North America CMOS Image Sensor Market

CMOS Image Sensor Production in North America Takes Advantage of Novel Tech Innovations

The CMOS image sensor market in North America is projected to hold a 35% market share in 2025, driven by demand across industries such as automotive, healthcare, industrial automation, and consumer electronics. The North American market is forecast to showcase a CAGR of 6.8% through 2032, driven by continuous technological advancements and expanding applications in AI-driven imaging solutions.

The region benefits from strong investments in research and development, with the U.S. leading the market due to its robust tech ecosystem and government initiatives supporting innovation. The healthcare sector is a major contributor, with increasing demand for high-resolution imaging in diagnostics, endoscopy, and surgical robotics.

In the automotive sector, the push for autonomous vehicles and ADAS fuels the demand for high-performance CMOS sensors. Companies like ON Semiconductor, OmniVision, and Sony are expanding their CMOS sensor portfolios to meet these evolving needs. The region is also witnessing increased adoption of AI-powered surveillance systems, boosting demand for machine vision technology.

Asia Pacific CMOS Image Sensor Market

Rise in Electronics Production in Asia Pacific Presents Avenues in Surveillance Infrastructure

The CMOS image sensor market in Asia Pacific, holding a 26% global revenue share in 2025, is experiencing rapid growth due to production capacities and strong demand from several industries. China and Japan are at the forefront, leveraging their manufacturing expertise and investment in research and development to dominate the sector.

China, as the world’s largest electronics producer, continues to lead the CMOS image sensor market, driven by expanding smartphone manufacturing, smart surveillance adoption, and automotive safety enhancements. Chinese companies like Sony China, GalaxyCore, and OmniVision are heavily investing in high-resolution and AI-powered imaging solutions. Additionally, China’s investment in smart cities and surveillance infrastructure is significantly boosting demand for high-performance CMOS sensors.

Meanwhile, Japan’s CMOS market is projected to record a CAGR of 6.9% through 2032, fueled by the adoption of AI-driven imaging solutions, robotics, and advanced manufacturing. Sony Semiconductor Solutions, the market leader, is continuously innovating with edge AI and low-light imaging technologies.

Europe CMOS Image Sensor Market

Auto Industry in Europe Offers Avenues of Research and Development in Technology

The CMOS image sensor market in Europe is projected to hold a 22% market share in 2025. With increasing investments in research and development in low-light imaging and 3D sensing, the European CMOS image sensor market is expected to record a CAGR of 6% through 2032, reinforcing its position as a leading hub for imaging technology advancements.

Europe’s automotive sector, led by manufacturers like BMW, Mercedes-Benz, and Volkswagen, is investing heavily in ADAS and autonomous vehicle technology, increasing demand for high-performance CMOS sensors.

Industry 4.0 initiatives in Germany, France, and the U.K., are fueling the growth in the machine vision and industrial automation industries. CMOS sensors are widely employed in quality control, robotics, and industrial automation, which improves production precision and productivity. Additionally, the usage of AI-powered security cameras in business areas, urban surveillance, and transit hubs has surged due to the region's strict safety and data protection legislation.

Major players in the global CMOS image sensor industry are actively expanding their product offerings to enhance their competitive edge in the market. Among the novel features being introduced are advanced medical exchange systems that facilitate the sharing of critical imaging data, as well as whole slide imaging systems designed for detailed analysis and diagnosis in medical settings. These developments reflect a commitment to improving technological capabilities and meeting the evolving needs of various sectors.

Key Industry Developments

|

Report Attributes |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Resolution

By Technology

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 31.25 Bn in 2025.

Mobile phone cameras often use CMOS active-pixel image sensors due to their lower power consumption compared to charge-coupled device (CCD) cameras.

Sony Semiconductor Solutions Corporation, Samsung, Omnivision Technologies Inc., ON Semiconductor, and STMicroelectronics are a few leading players.

The industry is estimated to rise at a CAGR of 8.1% through 2032.

North America is projected to hold the largest share of the industry in 2025.