Comprehensive Snapshot for Clostridium Difficile Infection Treatment Including Regional and Country Analysis in Brief.

Industry: Healthcare

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 170

Report ID: PMRREP15775

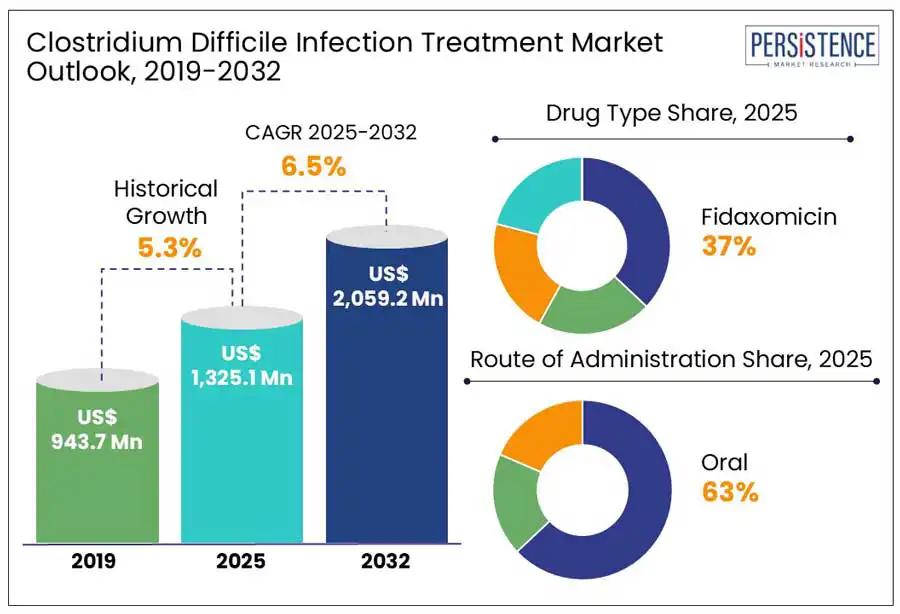

The global clostridium difficile infection treatment market size is anticipated to reach a value of US$ 1,325.1 Mn in 2025 and likely attain a value of US$ 2,059.2 Mn to witness a CAGR of 6.5% by 2032.

Steady expansions, rising incidence of CDI (Clostridium difficile Infection), increasing antibiotic resistance, and growing awareness of hospital-acquired infections drives the need for treatment. The demand for novel therapeutics, microbiome-based treatments, and targeted antibiotics is increasing as healthcare providers seek more effective and less resistance-prone treatment options. Advancements in microbiome research, fecal microbiota transplantation (FMT), and monoclonal antibody therapies are enhancing treatment outcomes.

North America and Europe lead the market due to strong healthcare infrastructure and high CDI prevalence, while Asia Pacific is emerging as a key growth region, supported by improved diagnostic capabilities and expanding access to advanced infection management solutions.

Key Industry Highlights:

|

Global Market Attribute |

Key Insights |

|

Clostridium difficile Infection Treatment Market Size (2025E) |

US$ 1,325.1 Mn |

|

Market Value Forecast (2032F) |

US$ 2,059.2 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

The increased use of antibiotics is a major driver of growth in the CDI Treatment Market. Antibiotics such as cephalosporins, clindamycin, and fluoroquinolones disrupt the gut microbiome, reducing beneficial bacteria and enabling C. difficile overgrowth, leading to severe diarrhea and colitis. According to CDC (Centers for Disease Control and Prevention), CDI affects nearly 500,000 people annually in the U.S., with 29,000 deaths within 30 days of diagnosis and According to WHO up to 25% of antibiotic-treated patients in hospitals develop CDI. This rising CDI incidence is driving demand for advanced treatments such as fidaxomicin, vancomycin, fecal microbiota transplantation (FMT), and monoclonal antibodies to prevent recurrence and improve patient outcomes.

Developing novel CDI treatments requires substantial financial investment, posing a significant barrier to market growth. On average, bringing a new drug to market costs approximately $2.6 billion, with only 12% of drugs entering clinical trials successfully reaching regulatory approval. The drug development process spans 10–15 years, demanding extensive resources for preclinical research, clinical trials, and regulatory compliance. These high costs and long timelines make it challenging for companies, especially smaller biotech, to introduce innovative non-antibiotic CDI treatments, potentially slowing market expansion.

Microbiome-based therapies offer a promising opportunity in the Clostridium difficile infection (CDI) treatment market, especially for recurrent cases. Unlike traditional antibiotics that disrupt gut flora, treatments like fecal microbiota transplantation (FMT) restore microbial balance. A key example is Rebyota, developed by Ferring Pharmaceuticals, the first FDA-approved fecal microbiota product, authorized in November 2022 to prevent recurrent CDI in adults. These therapies reduce relapse risk and support long-term gut health. With growing clinical evidence and regulatory backing, microbiome-based solutions are emerging as a transformative and sustainable approach in the evolving CDI treatment landscape.

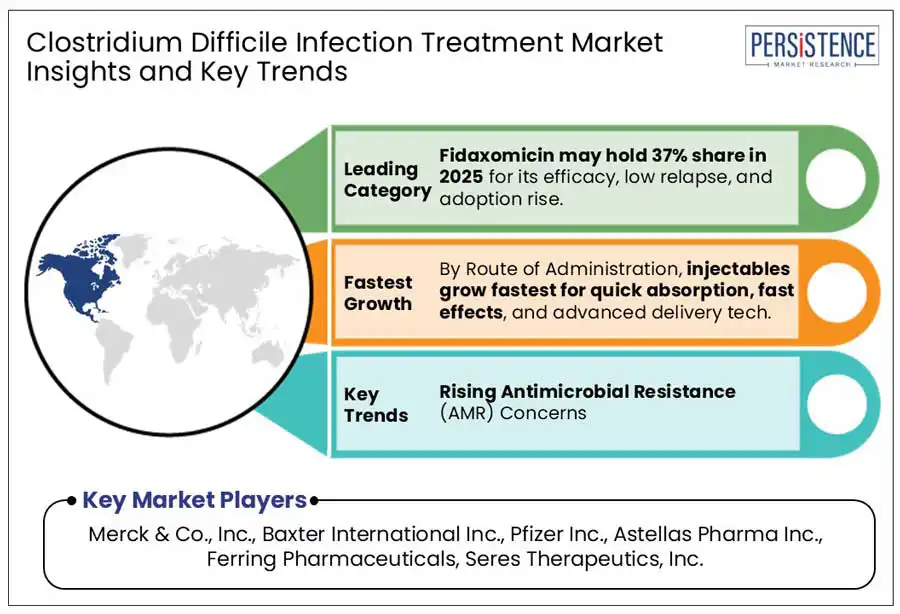

Fidaxomicin is a leading treatment for CDI due to its high efficacy and lower recurrence rates compared to traditional antibiotics such as vancomycin. Clinical studies show that fidaxomicin achieves a clinical cure rate of 92.1%, similar to vancomycin's 89.8%, but significantly reduces the recurrence rate to 13.3%, compared to 24% with vancomycin. Additionally, fidaxomicin’s targeted action helps preserve beneficial gut microbiota, minimizing disruption to the intestinal microbiome. These advantages enhance its effectiveness and reinforce its dominant role in the CDI treatment market.

The oral route of administration is the preferred method for treating clostridium difficile infections (CDI) due to their convenience, effectiveness, and patient compliance. In 2024, the oral administration segment is projected to hold highest share in the market. This preference stems from the ability of oral antibiotics to deliver targeted therapy directly to the gastrointestinal tract, the primary site of infection, facilitating prompt treatment initiation and reducing the need for hospitalization. Additionally, oral medications are generally more cost-effective and easier to administer than injectables, enhancing patient adherence to treatment regimens. These factors contribute to the dominance of oral administration in the CDI treatment market.

U.S. Clostridium difficile infection treatment market is attributed to several factors, including a high prevalence of CDI cases, advanced healthcare infrastructure, and significant economic impact. In the U.S., Clostridium difficile infection (CDI) poses a significant health burden, contributing to high rates of hospitalizations and complications. For instance, from 2000 to 2014, the number of hospitalizations with CDI as a primary diagnosis surged from 31,782 to 107,760, and associated hospital charges escalated from $0.51 billion to $3.87 billion annually.

The economic burden is further highlighted by the fact that CDI adds an average of 3–20 extra hospital days per patient, contributing to an additional cost of over $1 billion per year in the U.S. These statistics underscore the significant impact of CDI in North America and the imperative for effective treatment solutions.

Europe plays a key role largely due to the notable prevalence of CDI cases across the region. In the U.K., between 2022 and 2023, the 30-day all-cause mortality rate for hospital-onset healthcare-associated CDI cases reached 4.0 deaths per 100,000 bed days the highest recorded since current healthcare exposure definitions were introduced. These rising infection rates across major European countries highlight the urgent need for effective treatment options and reinforce the region’s significance in the global CDI treatment landscape.

Asia Pacific is experiencing a significant growth in the clostridium difficile infection treatment market due to several factors. Enhanced healthcare infrastructure and increased awareness have led to better diagnostic capabilities resulting in more reported cases. Additionally, the widespread use of antibiotics, sometimes unregulated, has contributed to a higher incidence of CDI, as antibiotic exposure is a primary risk factor. An aging population further amplifies this trend; as senior adults are more susceptible to CDI infections.

China has reported notable CDI prevalence rates in 2024. A meta-analysis covering 14 provinces in China found a pooled prevalence rate of 11.4% among patients with diarrhea, with Zhejiang province reporting rates as high as 23.6%. These figures underscore the growing recognition and diagnosis of CDI in China, highlighting the need for effective treatment strategies in the region.

The global clostridium difficile infection market is moderately competitive due to the presence of small and large market players who offer a range of clostridium difficile infection treatment. The players are actively involved in enhancing their offerings to increase their market share.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Drug Type

By Route of Administration

By Distribution Channel

By Region

To know more about delivery timeline for this report Contact Sales

The global market is estimated to increase from US$ 1,325.1 Mn in 2025 to US$ 2,059.2 Mn in 2032.

The market grows due to Rising antibiotic use, aging population, non-antibiotic therapies, improved diagnostics, and increased healthcare spending are driving CDI treatment market growth.

The market is projected to record a CAGR of 6.5% during the forecast period from 2025 to 2032.

Major players include Merck & Co., Inc., Baxter International Inc., Pfizer Inc., Astellas Pharma Inc., Ferring Pharmaceuticals, Seres Therapeutics, Inc. and Others.

Opportunities include developing non-antibiotic therapies, expanding fecal microbiota transplantation, improving diagnostics, increasing R&D investments, and growing CDI awareness programs.