- Retail

- Cigar and Cigarillos Market

Cigar and Cigarillos Market Size, Share, and Growth Forecast 2026 - 2033

Cigar and Cigarillos Market by Product Type (Handmade Cigars, Machine-made Cigars, Cigarillos), Flavor (Unflavored, Flavored, Fruit Flavor, Mint, Coffee, Chocolate, Others), Distribution Channel (Tobacco Specialty Stores, Convenience Stores, Supermarkets/Hypermarkets, Online Retail), by Regional Analysis, 2026 - 2033

Cigar and Cigarillos Market Size and Trend Analysis

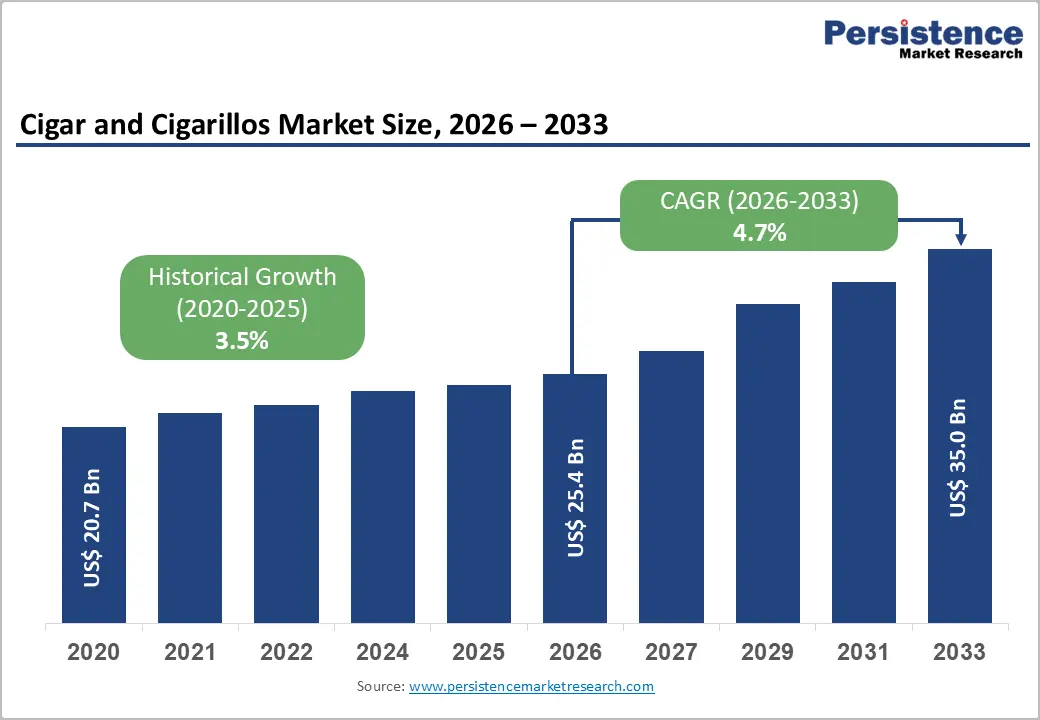

The global cigar and cigarillos market size is expected to be valued at US$ 25.4 billion in 2026 and projected to reach US$ 35.0 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

The market is gaining momentum as cigars have repositioned themselves as premium, lifestyle-driven products rather than mass tobacco items, insulating volumes from the broader cigarette decline. Rising disposable income in Asia, the resurgence of cigar lounges, premiumisation of hand-rolled offerings, and a sharp surge in flavored cigarillo demand among legal-age consumers across the Americas are the principal forces enlarging the addressable base.

Key Industry Highlights:

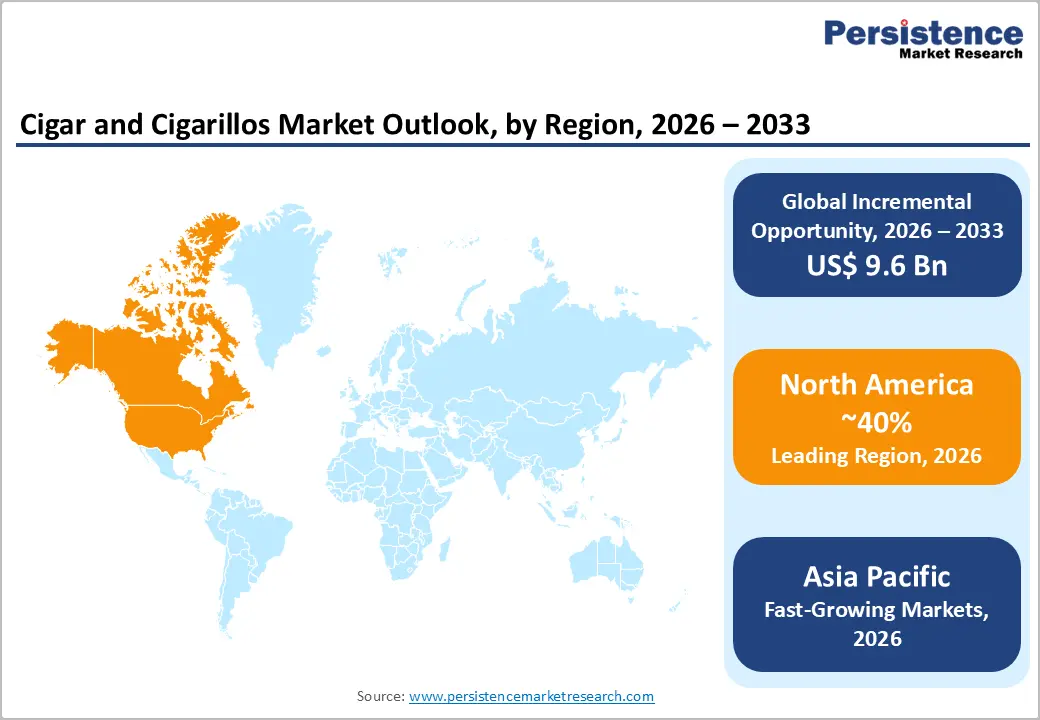

- Leading Region: North America leads with around 40% share in 2025, anchored by U.S. premium imports and dense specialty retail.

- Fastest Growing Region: Asia Pacific is the fastest-growing by 2033, propelled by rising affluence and China-led premium Habanos demand.

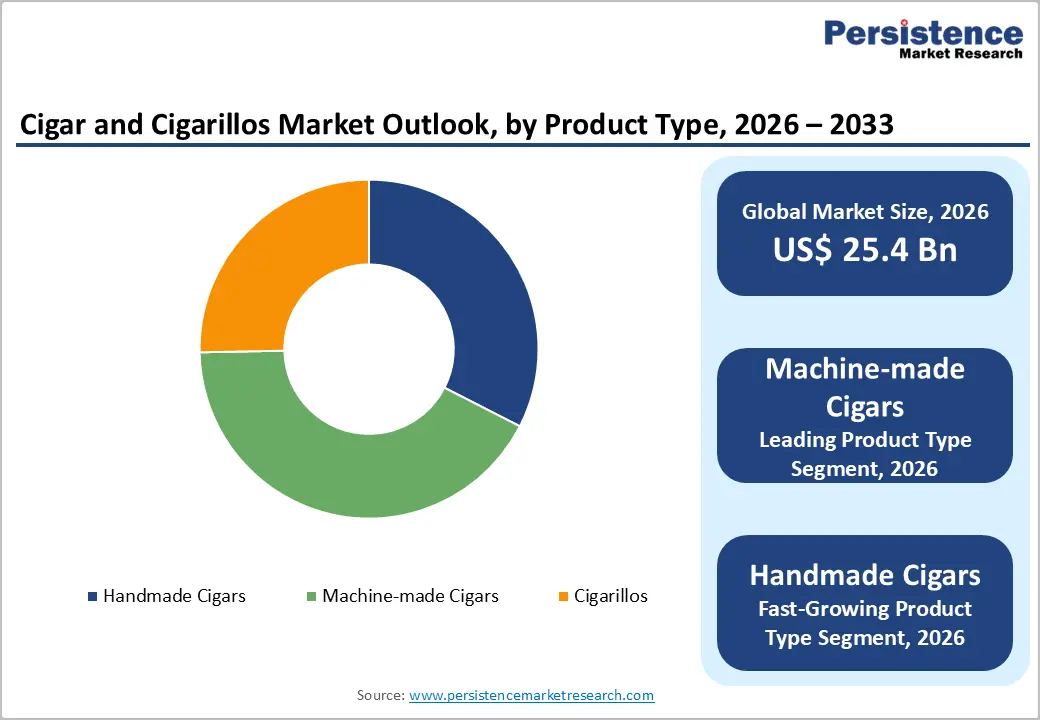

- Dominant Segment: Machine-made cigars lead the product-type category with nearly 52% share in 2025, driven by scale economics and convenience-store ubiquity.

- Fastest Growing Segment: Handmade cigars are the fastest-growing product-type segment, fuelled by premiumisation and surging Nicaraguan and Dominican imports.

- Key Market Opportunity: Boutique handmade cigars sold via digital direct-to-consumer platforms across Asia Pacific represent the highest-value growth opportunity.

Market Dynamics

Drivers - Premiumisation and Affluent Consumer Spending Powering Hand-Rolled Cigar Growth

Premiumisation has emerged as the single biggest engine of value growth across the cigar industry. Data from the Cigar Association of America (CAA) shows that imports of premium hand-made cigars into the United States crossed 555 million sticks in 2022, up from 374 million in 2019, a 48% increase in just three years. This trajectory reflects the post-pandemic embrace of "affordable luxury" rituals among aspirational consumers seeking experiential indulgence.

The entry of millennials into the 21+ consumption cohort has further lifted average retail prices by roughly 9% annually since 2021. Companies such as Davidoff and Arturo Fuente have responded with limited-edition releases priced above US$ 25 per stick. This illustrates how brand equity, terroir storytelling, and craftsmanship are translating directly into pricing power and broader category resilience.

Flavored Cigarillos Capturing Younger Legal-Age Consumer Demand Sharply

Flavored cigarillos have emerged as a high-velocity sub-segment, especially across North America, where they accounted for nearly 59% of total cigarillo unit sales in 2023 per U.S. Centers for Disease Control and Prevention (CDC) surveillance. Brands such as Swisher Sweets, Black & Mild, and Backwoods continue to introduce limited-batch flavor SKUs spanning fruit, honey, wine, and dessert profiles that retail between US$ 0.99 and US$ 2.49 per stick.

The U.S. Food and Drug Administration (FDA) noted in its 2023 deeming report that cigarillos were the second-most-purchased combustible tobacco product among adults aged 21-34. The convergence of affordability, flavor variety, and convenience-store ubiquity is driving steady volume rotation, supporting overall category expansion, and pulling new legal-age consumers into the broader cigar ecosystem.

Restraints - Stringent Regulatory Restrictions and Sweeping Flavor Bans Globally

Regulatory tightening remains the most disruptive headwind facing the cigar and cigarillos market. The U.S. FDA has proposed a federal ban on characterising flavors in cigars, while the European Union Tobacco Products Directive (TPD II) already prohibits flavored cigarillos in most member states as of 2020. Canada, Australia, and parts of the Middle East have followed with similar measures, narrowing the addressable assortment for global manufacturers.

Compliance, reformulation, and the loss of menthol and fruit SKUs threaten to remove an estimated 15-20% of current cigarillo volume in regulated markets. Excise duties have also climbed sharply, with Her Majesty's Revenue and Customs (HMRC) raising UK cigar duty by 10.1% in 2023. These layered fiscal and product restrictions are pressuring price-sensitive consumers and squeezing legacy manufacturer margins.

Rising Health Awareness Eroding Combustible Tobacco Consumer Base

Public-health campaigns are steadily eroding the long-term consumer base for combustible cigars. The WHO Framework Convention on Tobacco Control (WHO FCTC), ratified by 183 parties, mandates plain packaging, graphic warnings, and indoor smoking bans across signatory nations. These measures have shifted consumer perception, particularly among younger demographics increasingly attuned to lifestyle and longevity considerations in mature Western markets.

Cigar smoking prevalence among U.S. adults fell from 3.5% in 2017 to 3.1% in 2022 per the National Health Interview Survey (NHIS). While premium cigar volumes have held up, mass-market machine-made products face structural pressure as health-conscious consumers shift to nicotine pouches and heated-tobacco alternatives, capping upside for legacy combustible manufacturers serving entrenched Western consumer pockets.

Opportunities - Boutique Craft Hand-Made Cigars Surging Across Emerging Asia Pacific

Asia Pacific has crystallised as the fastest-growing opportunity zone for premium cigar manufacturers, driven by an expanding upper-middle class and the cultural prestige attached to imported Cuban and Nicaraguan brands. Habanos S.A. reported that the China-Asia Pacific region contributed roughly 32% of its global turnover in 2023, with mainland China alone surpassing Spain to become the largest single market for premium Habanos products globally.

The opening of more than 60 La Casa del Habano lounges across Shanghai, Singapore, Hanoi, and Mumbai, plus the proliferation of private cigar clubs, is creating a structured retail funnel for boutique brands. Hand-made cigars, projected to be the fastest-growing product-type segment through 2033, are well placed to capture this premium spend as gifting culture and corporate hospitality budgets recover meaningfully.

Digital Direct-to-Consumer Platforms Reshaping Cigar Retail Distribution

Online retail is the next strategic frontier for the cigar industry as legal-age verification technology and digital humidor management tools mature. According to the U.S. Census Bureau, e-commerce sales in the broader "beer, wine, and liquor" tobacco-adjacent category grew at a five-year CAGR above 18% between 2018 and 2023, signalling robust digital migration among adult-beverage and lifestyle consumers.

Platforms such as Cigars International, JR Cigar, and Famous Smoke Shop have invested in subscription-box models, while Scandinavian Tobacco Group acquired Alec Bradley Cigars in 2023 to strengthen its direct-to-consumer pipeline. Online channels deliver a wider assortment, transparent pricing, and personalised recommendations, and are projected to outpace brick-and-mortar growth rates more than twofold during the forecast horizon.

Category-wise Analysis

Product Type Insights

Machine-made cigars lead the global cigar and cigarillos market with approximately 52% share in 2025. Their dominance reflects industrial-scale production economics, broad price ladders starting under US$ 1 per stick, and deep penetration across convenience-store channels. According to the U.S. TTB, machine-made large cigars and cigarillos together accounted for more than 11 billion of the 12 billion total cigar removals in 2023, underscoring the scale advantages of mass manufacturers.

Handmade cigars are emerging as the fastest-growing product-type segment through the forecast horizon, propelled by premiumisation and rising appetite for craft, terroir-led offerings. Imports from the Dominican Republic, Nicaragua, and Honduras continue climbing as boutique makers like Arturo Fuente, Padrón, and Davidoff expand limited-edition portfolios. Lounge culture revival, gifting traditions, and millennial entry into legal-age cohorts are channelling discretionary spend toward hand-rolled premium experiences globally.

Flavor Insights

The flavored segment leads the cigar and cigarillos market with close to 55% value share in 2025, propelled chiefly by fruit-, mint-, and sweet-tip cigarillos. Data from the U.S. CDC National Youth Tobacco Survey shows that roughly 59% of legal-age adult cigar smokers prefer flavored variants, with fruit and wine being the most popular profiles. Flavored SKUs from Swisher International and Altria Group's Black & Mild range dominate convenience-store shelves.

The Flavored segment, particularly the fruit and dessert sub-profiles, is also the fastest-growing flavor category over the forecast horizon. Manufacturers such as Swisher Sweets and Backwoods continue launching limited-batch SKUs spanning honey, wine, blueberry, and tropical profiles to capture flavor-curious legal-age consumers. Despite regulatory scrutiny in selected markets, continued sensory innovation and convenience-store accessibility are sustaining momentum across North America and parts of the emerging Asia Pacific.

Distribution Channel Insights

Convenience stores are likely to lead the distribution channel with around 47% share in 2026, reflecting the channel's alignment with impulse-driven, single-stick cigarillo purchases. According to the National Association of Convenience Stores (NACS), U.S. c-stores generated US$ 859 billion in total in-store sales in 2023, with "other tobacco products"—a category dominated by cigars and cigarillos—contributing roughly 5.8% of merchandise revenue across the network.

Online retail is the fast-growing distribution channel supported by maturing age-verification technology, subscription-box innovation, and digital humidor-management tools. Specialty e-tailers such as Cigars International, JR Cigar, and Famous Smoke Shop are expanding direct-to-consumer reach, while major players such as Scandinavian Tobacco Group continue investing in digital storefronts. Wider assortment, transparent pricing, and personalised recommendations are accelerating consumer migration from brick-and-mortar specialty shops, especially among premium-cigar enthusiasts.

Regional Insights

North America Cigar and Cigarillos Market Trends and Insights

North America commands the global cigar and cigarillos market with 40% share in 2026, supported by mature retail infrastructure, deep brand heritage, and steady premium imports. Key trends include rising hand-made cigar imports from the Dominican Republic and Nicaragua, expansion of cigar lounges across Florida and Texas, and growing online subscription services targeting legal-age aficionados across the region.

- U.S. Cigar and Cigarillos Market Size

The United States is likely to contribute nearly 88% of North American cigar revenue in 2026. U.S. TTB data shows annual cigar removals exceeding 12 billion sticks. Demand drivers include premium hand-made import growth, lounge culture revival in Florida and Texas, and rising flavored cigarillo penetration.

Europe Cigar and Cigarillos Market Trends and Insights

Europe is likely to register approximately 27% of the global cigar and cigarillos market in 2026, anchored by historic consumption in Spain, the United Kingdom, Germany, and France. The market is shaped by the EU TPD II framework, high excise duties, and a clear premium tilt. Specialty tobacconists, duty-free retail, and renewed interest in Habanos underpin regional value growth.

- Germany Cigar and Cigarillos Market Size

Germany is among Europe's largest cigarillo markets, representing roughly 23% of European value and around 5% of global revenue. Per the Federal Statistical Office (Destatis), over 2.6 billion cigarillos were taxed in 2023, supported by strong domestic brands like Dannemann and Villiger alongside imported premium portfolios.

- U.K. Cigar and Cigarillos Market Size

The United Kingdom market contributes about 13% of European cigar revenue and nearly 3% of global value. Per HMRC data, cigar clearances totalled around 1,250 tonnes in 2023. Drivers include premium Habanos demand, London-based lounges such as Davidoff of London, and rising spend among affluent professionals despite duty escalators.

- France Cigar and Cigarillos Market Size

France's cigar and cigarillos market accounts for nearly 10% of European value and around 2% of global revenue. Per Logista France distribution data, cigarillos hold the bulk of unit volume, sold predominantly through state-licensed tobacconists. Premium Habanos imports and a growing female-cigar consumer base support steady, regulation-tempered growth.

Asia Pacific Cigar and Cigarillos Market Trends and Insights

Asia Pacific holds approximately 18% share of the global cigar and cigarillos market in 2025 and is the fastest-growing region through 2033. China leads regional opportunity, having become Habanos S.A.'s largest individual market in 2023. Rising affluence, gifting culture, expanding cigar lounges in tier-1 cities, and cross-border luxury travel collectively drive premium hand-made cigar demand across the region.

- India Cigar and Cigarillos Market Size

India's cigar and cigarillos market contributes nearly 7% of Asia Pacific revenue and around 0.8% of global value. Growth is led by ITC Limited's Armenteros brand and import partnerships, alongside rising premium cigar lounges in Mumbai and Delhi. Affluent millennials and corporate gifting fuel demand despite GST of 28% plus cess.

- Japan Cigar and Cigarillos Market Size

Japan's cigar and cigarillos market holds around 11% of Asia Pacific value and nearly 1.3% of global revenue. Japan Tobacco Inc. dominates domestic distribution while imported Habanos remain prestige products. Drivers include resilient consumer purchasing power and refined connoisseurship in Tokyo's specialty cigar bars, even as broader combustible-tobacco consumption declines.

- Southeast Asia Cigar and Cigarillos Market Size

Southeast Asia's cigar and cigarillos market accounts for about 9% of regional revenue and around 1.1% of global value. Indonesia, Vietnam, and the Philippines lead consumption, supported by indigenous tobacco cultivation. Expansion of La Casa del Habano lounges in Singapore and Ho Chi Minh City, plus a thriving expat customer base, drives premium growth.

Competitive Landscape

The global cigar and cigarillos market is moderately consolidated, with a handful of multinational tobacco majors anchoring value sales alongside a long tail of boutique craft makers. Strategic priorities across leading players include premium portfolio expansion through targeted mergers and acquisitions, vertical integration of leaf sourcing in Nicaragua and the Dominican Republic, sustainability certification of tobacco farms, and investment in direct-to-consumer digital platforms.

Mass-market leaders defend share through aggressive flavor innovation, convenience-store category management, and pan-regional distribution scale. Boutique craft manufacturers, meanwhile, compete via limited-edition releases, terroir-led storytelling, exclusive lounge partnerships, and artisanal positioning targeting affluent connoisseurs globally.

Key Developments:

- In October 2024, Scandinavian Tobacco Group completed the acquisition of premium handmade-cigar maker Alec Bradley Cigars, strengthening its U.S. premium portfolio and direct-to-consumer distribution footprint.

- In March 2024, Habanos S.A. reported record revenues of US$ 721 million for 2023 at its annual Festival in Havana, citing strong demand from the Asia Pacific and ultra-premium Cohiba Behike releases.

- In September 2023, Imperial Brands plc announced an extended five-year strategic capex plan to modernise cigarillo manufacturing in the Netherlands and expand the Backwoods brand internationally.

Companies Covered in Cigar and Cigarillos Market

- Scandinavian Tobacco Group

- Imperial Brands

- Swedish Match

- Altria Group

- British American Tobacco

- Philip Morris International

- J.C. Newman Cigar Company

- Arturo Fuente

- Oliva Cigar Company

- Davidoff

- Gurkha Cigars

- General Cigar Company

- Drew Estate

- Habanos S.A.

- Rocky Patel Premium Cigars

Frequently Asked Questions

The global cigar and cigarillos market is expected to reach US$ 25.4 billion in 2026 and US$ 35.0 billion by 2033, at a 4.7% CAGR.

Premiumisation of hand-made cigars, expanding cigar lounges, and high-velocity flavored cigarillo sales are the principal demand drivers globally.

North America leads with around 40% value share in 2025, anchored by the United States and resilient premium imports.

Premium hand-made cigars distributed across Asia Pacific via cigar lounges and digital direct-to-consumer platforms represent the highest-value opportunity.

Leading companies include Scandinavian Tobacco Group, Imperial Brands plc, Altria Group, Swedish Match (PMI), Habanos S.A., and Japan Tobacco Inc.