- Semiconductor Materials & Components

- Chip Antenna Market

Chip Antenna Market Size, Share, and Growth Forecast 2026 - 2033

Chip Antenna Market by Technology (LTCC (Low Temperature Co-fired Ceramic), Dielectric, Others), Connectivity (Cellular (2G/3G/4G/5G), Wi-Fi/Bluetooth, GNSS/GPS, UWB, RFID, LPWAN, Others), Frequency (Below 1 GHz, 1-3 GHz, 3-6 GHz, Above 6 GHz), End-user Industry and Regional Analysis, 2026 - 2033

Chip Antenna Market Size and Trend Analysis

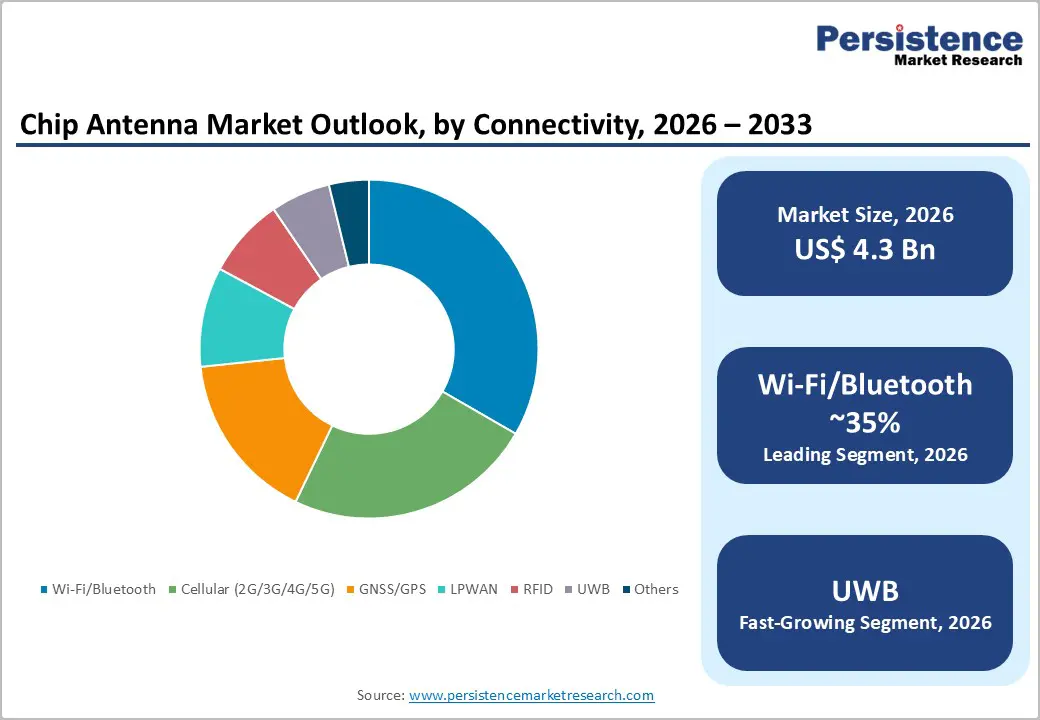

The global chip antenna market is expected to be valued at US$ 4.3 billion in 2026 and is projected to reach US$ 9.8 billion by 2033, growing at a CAGR of 12.5% between 2026 and 2033, driven by ongoing expansion of global 5G infrastructure and mid-band spectrum commercialization is accelerating demand for compact, high-performance chip antennas across smartphones, customer premises equipment (CPE), wearables, and IoT devices.

The Federal Communications Commission's allocation of more than 100 MHz of contiguous spectrum in the 3.45-3.55 GHz band is compelling OEMs to redesign RF front-end architectures and adopt compliant multiband antenna modules, shortening replacement and procurement cycles across the device ecosystem.

Key Industry Highlights:

- Leading Technology: LTCC (Low Temperature Co-fired Ceramic) dominates the global chip antenna market with over 54.0% share in 2026, valued at approximately US$ 2.32 Bn, driven by its superior multi-layer RF integration capability, compact form factor, thermal stability, and suitability for 5G, GNSS, IoT, and automotive telematics applications.

- Leading Connectivity: Wi-Fi/Bluetooth accounts for more than 35.0% of the market share in 2026, exceeding US$ 1.50 billion, supported by rising deployment across smartphones, laptops, smart home devices, wearables, and industrial handheld equipment requiring compact low-power wireless connectivity.

- Leading Frequency: The 1-3 GHz frequency segment holds approximately 38.0% share in 2026, valued above US$ 1.63 billion, owing to its extensive use across LTE, sub-6 GHz 5G, GNSS, Wi-Fi, Bluetooth, and industrial IoT applications requiring balanced signal coverage and energy efficiency.

- Fast-Growing Frequency: The above 6 GHz segment is the fastest-growing, propelled by accelerating deployment of mmWave 5G, UWB communication, wireless backhaul, AR/VR connectivity, and ultra-low latency industrial applications.

- Leading Industry: Consumer electronics dominate the chip antenna market with nearly 40.0% share in 2026, representing around US$ 1.72 billion, driven by the integration of multiple wireless protocols across smartphones, earbuds, gaming devices, smartwatches, and AI-enabled smart home products.

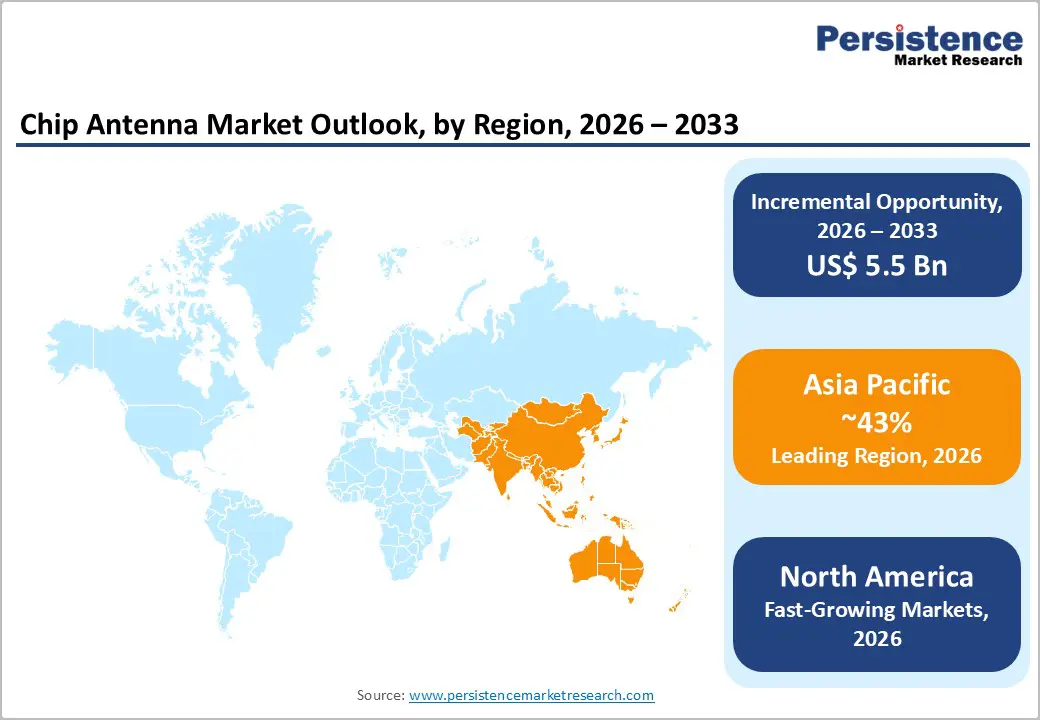

- Leading Region: Asia Pacific is likely to lead the global chip antenna market with over 43.0% share in 2026, valued at approximately US$ 1.85 billion, supported by the concentration of global electronics manufacturing, vertically integrated semiconductor supply chains, aggressive 5G deployment, and large-scale smartphone and IoT production.

Market Dynamics

Drivers - Accelerating 5G Infrastructure Rollout Mandating Multi-Band Chip Antenna Integration

The rapid expansion of 5G-enabled smartphones, customer premises equipment (CPE), wearables, industrial IoT modules, and connected automotive platforms is increasing demand for compact multi-band chip antennas capable of supporting cellular, Wi-Fi 6/6E, Bluetooth, and GNSS connectivity within increasingly space-constrained device architectures.

The European Union’s Digital Decade connectivity targets, alongside national 5G deployment programmes implemented under the European Electronic Communications Code (EECC) framework, are accelerating large-scale 5G network expansion and device ecosystem growth across member states. OEMs are migrating toward higher-frequency sub-6 GHz and Wi-Fi 6E designs that require efficient, miniaturized antenna solutions with broader frequency coverage and improved coexistence performance.

IoT Device Proliferation Driven by Industrial Digitisation Programmes

Industrial digitization programmes and large-scale IoT deployments are accelerating demand for compact embedded antenna solutions across smart manufacturing, utilities, logistics, and infrastructure monitoring applications. Germany’s Industry 4.0 initiative, supported by the Federal Ministry for Economic Affairs and Climate Action, has expanded deployment of connected factory environments incorporating LPWAN, Bluetooth, Wi-Fi, and cellular-enabled sensors, gateways, and asset-tracking systems, many of which integrate embedded chip antennas to support space-constrained device architectures.

Global IoT connections to reach nearly 30 billion by 2030, reinforcing sustained high-volume demand for multiband and miniaturized chip antenna components across industrial and commercial IoT ecosystems.

Restraints - Raw Material Concentration and Ceramic Supply Chain Fragility

The LTCC chip antenna manufacturing ecosystem depends on high-purity ceramic dielectric materials such as barium titanate and alumina composites sourced through a concentrated global supply chain, exposing manufacturers to raw material cost volatility and procurement risks. China accounts for nearly 60-70% of global advanced ceramic oxide and electronic material refining capacity, creating supply-side dependence for antenna vendors during periods of export regulation tightening and geopolitical disruption.

Fluctuations in silver and palladium paste pricing increase production costs for multilayer high-frequency antenna designs. These pressures disproportionately affect fabless and Tier-2 suppliers that lack vertically integrated ceramic processing and long-term raw material procurement agreements, constraining margin stability and production scalability.

Stringent RF Certification Requirements Extending Time-to-Market

Mandatory RF conformance certification, including FCC Part 15 in the United States, CE RED (Radio Equipment Directive 2014/53/EU) in Europe, and TELEC in Japan, adds 12-26 weeks of testing and documentation lead time per product variant, creating a disadvantage for new entrants attempting to compete on product velocity. Recertification costs for frequency band amendments reach US$ 50,000-US$ 120,000 per SKU according to accredited test laboratory published fee schedules, a burden that disproportionately affects smaller design houses bringing novel form-factor chip antennas to market against established players with pre-certified platform designs.

Opportunities - Automotive V2X and ADAS Connectivity Creating a High-Value, Recurring Antenna Demand Pool

The growing deployment of connected vehicles, ADAS platforms, and V2X communication systems is creating sustained demand for automotive-grade chip antennas operating in the 5.9 GHz spectrum band. Suppliers capable of meeting AEC AEC-Q200 reliability standards and maintaining IATF 16949-certified manufacturing facilities are well-positioned to secure long-term automotive sourcing contracts with higher margins than consumer electronics applications.

The updated C-ITS framework under the European Commission ITS Directive 2010/40/EU is accelerating connected mobility deployments across Europe, supporting broader adoption of ITS-G5 and Cellular Vehicle-to-Everything (C-V2X) technologies. In parallel, Robert Bosch GmbH continues expanding its connected mobility and V2X module ecosystem, increasing demand for compact, high-reliability multiband chip antenna solutions across next-generation vehicle platforms.

Smart Healthcare Wearables and Implantable Device Connectivity: Unlocking a Premium Margin Segment

Smart healthcare wearables and connected implantable devices are creating a premium-margin growth opportunity for chip antenna manufacturers. Medical OEMs developing FDA 510(k)-cleared and EU MDR-compliant devices require ultra-miniaturised antennas with ultra-low power consumption and validated MICS (402-405 MHz) and BLE connectivity performance.

These medical-grade antenna solutions command significantly higher pricing than standard \consumer variants due to stringent reliability, traceability, and biocompatibility requirements. Apple Inc. further demonstrated demand for compact multi-protocol antenna integration through the launch of the Apple Watch Series 9 with enhanced BLE 5.3 and UWB capabilities.

Category-wise Analysis

Technology Insights

LTCC (Low Temperature Co-fired Ceramic) is likely to command over 54% of the global chip antenna market in 2026, equivalent to US$ 2.32 billion, due to its ability to integrate multiple RF layers, passive components, and shielding structures into a compact footprint required for modern wireless electronics. Smartphone, IoT, and automotive OEMs increasingly need highly stable antenna performance across multiple frequency bands while maintaining ultra-small device dimensions. LTCC technology also provides superior thermal stability, low signal loss, and high manufacturing consistency, making it suitable for 5G, GNSS, and automotive telematics applications.

Dielectric chip antennas represent the fastest-growing technology, propelled by advances in high-permittivity ceramic materials that enable extremely compact resonant structures for mmWave, UWB, and high-frequency wireless applications. Device manufacturers are demanding antennas capable of operating in smaller form factors without sacrificing bandwidth or efficiency, particularly in wearables, AR/VR devices, asset tracking systems, and next-generation industrial sensors.

Dielectric antennas offer simplified structures and lower design complexity for emerging ultra-high-frequency deployments. Their ability to support miniaturization trends while reducing space consumption inside densely packed electronics is accelerating adoption globally.

Connectivity Insights

Wi-Fi/Bluetooth is likely to register more than 35% of the share in 2026, reaching over US$ 1.50 billion, due to the requirement for short-range wireless connectivity across smartphones, laptops, smart TVs, wearables, smart appliances, and industrial handheld devices. Manufacturers increasingly prefer integrated chip antenna solutions that simultaneously support both protocols while minimizing PCB space and power consumption.

The rapid expansion of smart homes and connected consumer ecosystems continues to increase demand for compact dual-band and multi-band antenna architectures. Enterprise mobility devices and industrial IoT equipment require reliable low-power connectivity, further strengthening long-term demand.

UWB is the fastest-growing segment, driven by rising demand for centimetre-level indoor positioning, secure authentication, and real-time asset tracking capabilities. Automotive digital key systems, smart factory automation, warehouse robotics, and consumer electronics increasingly require highly accurate spatial awareness that traditional Bluetooth or Wi-Fi cannot consistently deliver. Smartphone vendors and automotive OEMs are integrating UWB to enable secure proximity-based access and precision device interaction.

Frequency Insights

The 1-3 GHz band accounts for approximately 38% share in 2026, exceeding US$ 1.63 billion, as this spectrum range supports the majority of mainstream wireless communication standards, including LTE, sub-6 GHz 5G, GNSS, Wi-Fi, Bluetooth, and industrial IoT connectivity. Device manufacturers prioritize this frequency range due to its balanced combination of signal coverage, penetration capability, and power efficiency. Smartphones, automotive telematics units, smart meters, and industrial monitoring systems extensively rely on antennas operating within this spectrum.

Global telecom infrastructure compatibility and mature chipset ecosystems continue to reinforce demand for chip antennas optimized for 1-3 GHz operation.

The Above 6 GHz frequency segment is the fastest growing due to increasing deployment of mmWave 5G networks, high-speed wireless backhaul, UWB communication, and next-generation low-latency connectivity applications. Electronics manufacturers are investing in compact high-frequency antenna architectures capable of supporting extremely high data throughput in dense urban and industrial environments. AR/VR devices, autonomous vehicles, advanced driver assistance systems, and industrial automation platforms increasingly require ultra-fast short-range communication enabled by higher frequency bands.

Industry Insights

Consumer electronics are likely to account for nearly 40% of the global chip antenna market in 2026, due to the growing number of wireless protocols integrated into smartphones, smartwatches, earbuds, gaming devices, and smart home products. OEMs require chip antennas that offer miniaturization, stable signal efficiency, and low power consumption without increasing device thickness. The rise in adoption of wearable electronics and AI-enabled smart devices further continues to increase antenna density per device globally.

Automotive is the fast-growing segment, propelled by the rapid integration of connected vehicle technologies, advanced driver assistance systems (ADAS), vehicle-to-everything (V2X) communication, telematics, digital key systems, and autonomous driving platforms. Modern vehicles now require multiple high-performance antennas to support navigation, infotainment, real-time diagnostics, over-the-air software updates, and safety communication systems. Electric vehicle manufacturers are especially increasing demand for compact multi-band chip antennas that can operate reliably under harsh thermal and vibration conditions.

Regional Insights

North America Chip Antenna Market Trends and Insights

North America accounts for over 25% of the global chip antenna market in 2026, representing approximately US$ 1.07 billion, driven by the concentration of hyperscale consumer electronics demand and one of the world’s most active 5G spectrum licensing environments. The CHIPS and Science Act of 2022 allocated US$ 52.7 billion toward domestic semiconductor and advanced component manufacturing, indirectly incentivizing chip antenna supply chain localization as OEMs increasingly seek to qualify U.S.- and Mexico-based antenna module assemblers to reduce import dependency.

Regional antenna procurement cycles are expected to accelerate further as commercially shipping Wi-Fi 7-certified devices become increasingly essential for enterprise wireless infrastructure upgrades, thereby sustaining long-term regional demand.

The United States chip antenna market is expected to exceed US$ 890 million by 2026, primarily due to the high density of IoT endpoint deployments in smart building and enterprise networking applications. According to the U.S. Department of Energy’s Building Technologies Office, commercial buildings account for over 35% of total U.S. electricity consumption, accelerating the adoption of wireless sensor networks, where each node requires a chip antenna for energy management and connectivity functions.

As 5G Fixed Wireless Access (FWA) subscriptions scale toward carrier targets exceeding 15 million connections by 2030, according to T-Mobile investor guidance, customer premises equipment (CPE) antenna procurement is expected to create a recurring replacement demand layer alongside the existing consumer electronics base.

Europe Chip Antenna Market Trends and Insights

Europe accounts for nearly 20.0% of the global chip antenna market in 2026, representing US$ 860 million, supported by strict wireless connectivity regulations, automotive digitalization, and semiconductor localization initiatives. The EU’s Radio Equipment Directive (RED) cybersecurity requirements, effective from August 2025, are increasing the need for highly reliable and compliant antenna-integrated RF modules across connected consumer and industrial devices. Germany remains the largest market within Europe, holding over 25.0% regional share value exceeding US$ 210 million in 2026, driven by connected vehicle production, Industry 4.0 deployments, and expanding private 5G infrastructure across industrial facilities.

The United Kingdom chip antenna market is expected to surpass US$ 150 million by 2026, benefiting from aggressive 5G network densification and rural wireless broadband expansion. Nationwide 5G rollout by major telecom operators is accelerating the deployment of small cells, routers, IoT gateways, and FWA equipment that require compact multi-band chip antennas. France's growth is supported by software-defined vehicle platforms, EV connectivity architectures, and sovereign semiconductor investments under the France 2030 programme.

The Rest of Europe market is led by strong telecom infrastructure and industrial automation activity across Nordic and Central European countries. Sweden and Finland continue to generate disproportionate demand due to the presence of major telecom ecosystem players and advanced industrial IoT adoption, while Denmark is witnessing rising wireless integration across smart manufacturing systems. In Central and Eastern Europe, particularly Poland, large-scale smart metering deployments and energy digitalization programmes are creating significant LPWAN and sub-GHz chip antenna demand.

Asia Pacific Chip Antenna Market Trends and Insights

Asia Pacific accounts for over 43% of the global chip antenna market in 2026, representing US$ 1.85 billion, and remains the fast-growing regional market with a CAGR of 17.1%. The region benefits from the concentration of global electronics manufacturing across China, Japan, South Korea, India, and Southeast Asia, which collectively support the majority of worldwide smartphone, IoT, and connected device production. The region’s dominance is further reinforced by its vertically integrated semiconductor and electronics supply chains, making Asia Pacific the global center for chip antenna design, sourcing, and large-scale manufacturing.

China's chip antenna market is expected to reach over US$ 830 million by 2026, supported by aggressive 5G base station deployment, strong domestic smartphone production, and government-backed semiconductor localization initiatives. Japan accounts for over 16.0% of the regional market, driven by Murata Manufacturing’s leadership in LTCC and ceramic antenna innovation, along with long-term IoT expansion under the Society 5.0 strategy.

South Korea's chip Antenna market value is expected to surpass the US$ 0.24 billion, where Samsung Electronics and LG Electronics continue to accelerate demand for high-density multi-protocol antennas integrated into premium smartphones, wearables, and connected consumer devices.

India is expected to achieve a substantial CAGR, supported by the government’s Production-Linked Incentive (PLI) scheme, rapid 5G rollout, and increasing domestic assembly of smartphones, routers, and telecom equipment. In Southeast Asia, Vietnam, Malaysia, and Thailand are emerging as key electronics manufacturing hubs under the China-plus-one diversification strategy adopted by global OEMs. Rising investments in semiconductor packaging, consumer electronics assembly, and industrial IoT infrastructure are expanding regional procurement of chip antennas across smartphones.

Competitive Landscape

The global chip antenna market is a consolidated competitive structure where leading players compete primarily through proprietary material science, miniaturization capabilities, broad frequency-band coverage, and automotive-grade reliability certifications.

Mid-tier manufacturers are differentiating through pricing flexibility, faster customization cycles, and resilient regional supply chain networks targeting IoT module makers and consumer electronics OEMs. A major emerging competitive strategy involves software-configurable and tunable antenna architectures that allow post-assembly frequency optimization, reducing SKU complexity and enabling OEMs to accelerate product design cycles while improving inventory efficiency.

Key Developments:

- In December 2025, SkyMirr announced that it will showcase its next-generation wireless technologies at CES 2026, including high-efficiency RF antennas, MuLCAT intelligent antenna architecture, and advanced 5G/Wi-Fi connectivity solutions. The innovations target IoT devices, enterprise wireless systems, and compact communication modules, supporting demand growth for advanced chip antenna technologies.

- In July 2025, Johanson Technology launched the new 0900AT47A0063001E SMD ceramic chip antenna designed for 868 MHz and 902-928 MHz ISM band applications. The compact antenna targets LPWAN and IoT devices such as LoRaWAN modules, smart meters, asset tracking systems, and industrial monitoring equipment, strengthening the company’s portfolio.

Companies Covered in Chip Antenna Market

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Yageo Corporation

- Johanson Technology, Inc.

- TAIYO YUDEN Co., Ltd.

- KYOCERA AVX Components Corporation

- Vishay Intertechnology, Inc.

- TE Connectivity Ltd.

- Abracon LLC

- Pulse Electronics Corporation

- Antenova Ltd.

- Partron Co., Ltd.

- Quectel

- Amphenol Communications Solutions

- Others

Frequently Asked Questions

The global chip antenna market is valued at US$4.3 billion in 2026 and is projected to reach US$9.8 billion by 2033, growing at a CAGR of 12.5%, driven by rising integration of chip antennas in 5G devices, Wi-Fi 7 platforms, and connected vehicles.

The rapid expansion of IoT connections and increasing regulatory mandates for connected automotive systems. Rising adoption of smart devices, C-V2X technology, and industrial IoT applications is creating sustained demand for embedded chip antennas.

LTCC (Low Temperature Co-fired Ceramic) technology holds the largest market share at 54.0% due to its superior thermal stability, low signal loss, and reliability in automotive and high-frequency applications. Its strong qualification standards also create high entry barriers for competing materials.

Asia Pacific dominates the chip antenna market with holding over 43.0% share in 2026, supported by strong smartphone manufacturing ecosystems and extensive 5G infrastructure deployment. The growth is further fueled by rising IoT adoption and smart city projects across China and Southeast Asia.

The automotive C-V2X and ADAS applications are likely to create additional opportunities where connected vehicle regulations are increasing demand for automotive-grade chip antennas. Companies with certified manufacturing capabilities and long-term partnerships with automotive suppliers are expected to benefit the most.

The leading companies include Murata Manufacturing Co., Ltd., TDK Corporation, Yageo Corporation, Johanson Technology, Inc., TAIYO YUDEN Co., Ltd., KYOCERA AVX Components Corporation, TE Connectivity Ltd., among others.