- Sensors & Controls

- Ceramic Transducers Market

Ceramic Transducers Market Size, Share, and Growth Forecast, 2026 - 2033

Ceramic Transducers Market by Product Type (Piezoelectric, Capacitive, Magnetostrictive, Others), Application (Ultrasonic Cleaning, Medical Imaging, Industrial Non-Destructive Testing (NDT), Automotive Sensors), End-User (Healthcare, Automotive, Industrial, Consumer Electronics), and Regional Analysis for 2026 - 2033

Ceramic Transducers Market Share and Trends Analysis

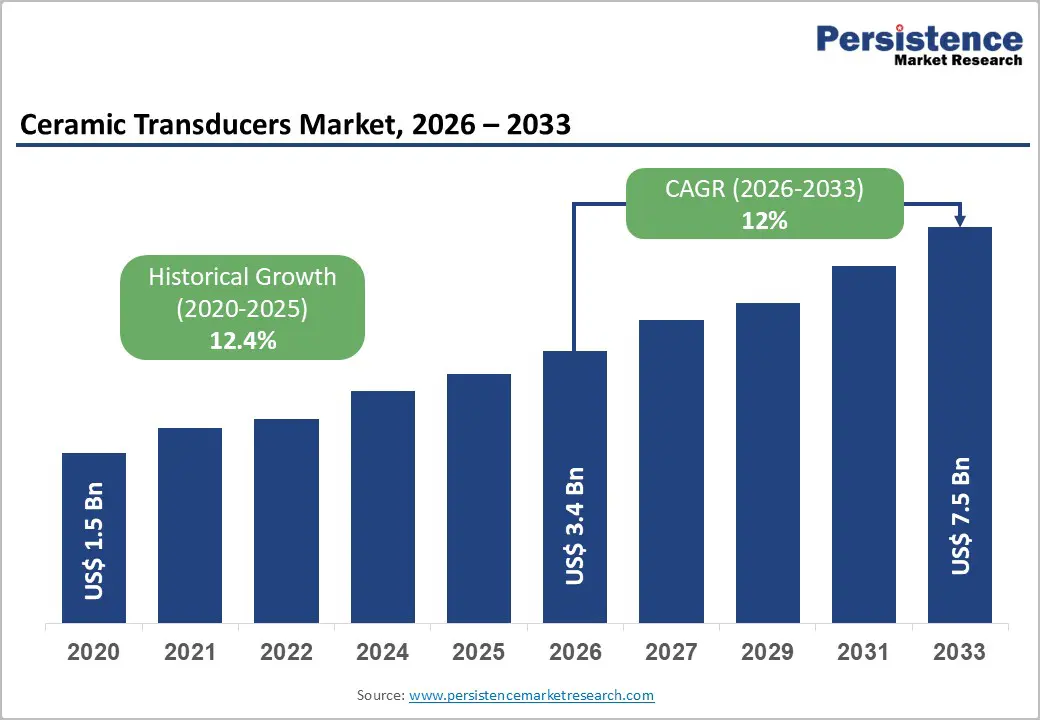

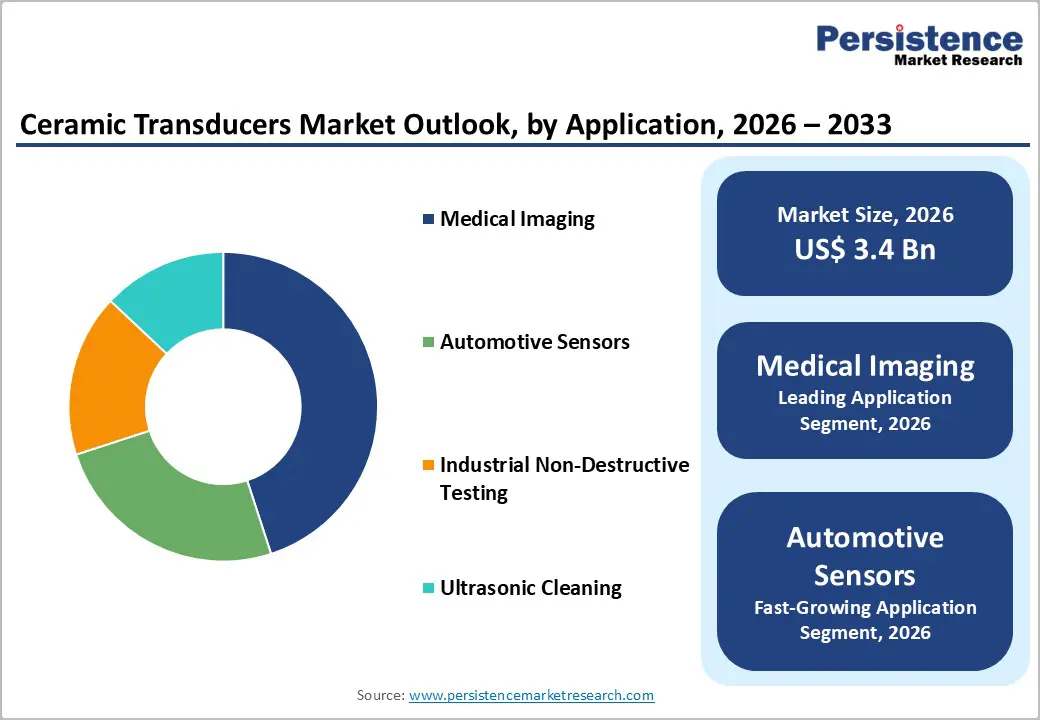

The global ceramic transducers market size is likely to be valued at US$ 3.4 billion in 2026, and is projected to reach US$ 7.5 billion by 2033, growing at a CAGR of 12% during the forecast period 2026 - 2033.

The projected growth of the market reflects a maturing yet highly innovative sector where ceramic-based piezoelectric materials are becoming the standard for high-precision sensing and ultrasonic applications. Primary growth factors include the global transition to electric vehicles (EVs), which requires extensive sensor arrays, and the integration of Industry 4.0 automation in manufacturing hubs across Asia and North America.

Key Industry Highlights

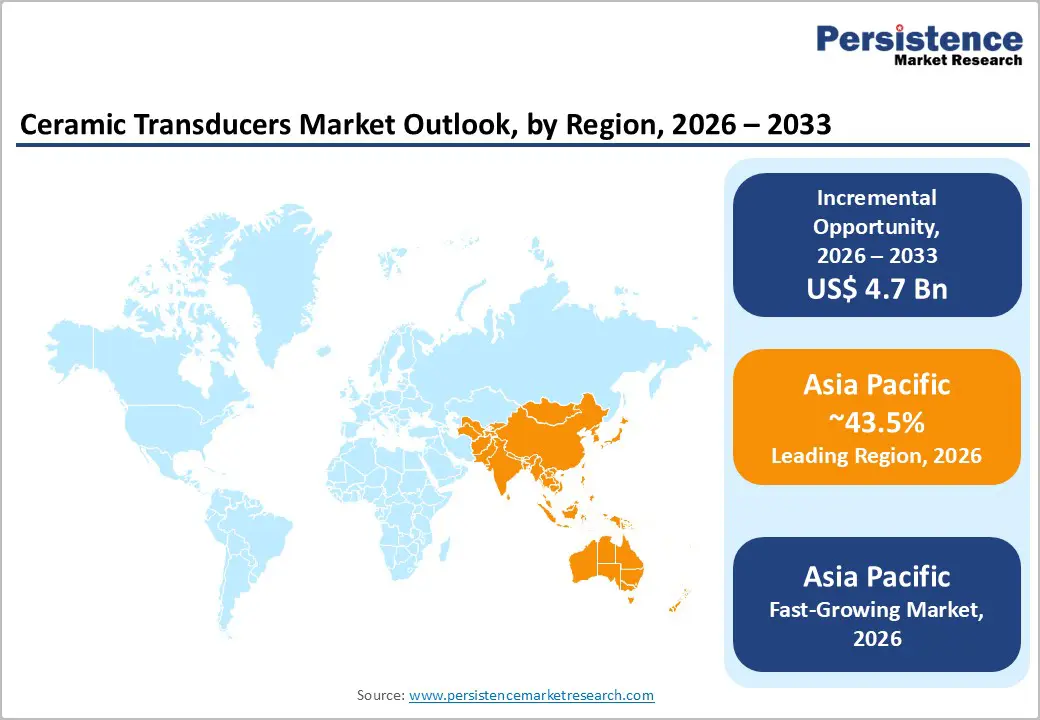

- Dominant & Fastest-growing Market: Asia Pacific is likely to be both the leading and fastest-growing regional market through 2033, accounting for approximately 43.5% revenue share in 2026, driven by continued innovation and rising demand for smart technologies.

- Leading & Fastest-growing Product Type: Piezoelectric is slated to capture approximately 55% revenue share in 2026, while capacitive is likely to be the fastest-growing segment during the 2026 - 2033 forecast period.

- Leading & Fastest-growing Application: Medical imaging is poised to lead with nearly 42% revenue share in 2026, with automotive sensors growing the fastest over 2026 - 2033.

- Prime Driver: The automotive sector will continue to drive the demand for ceramic transducers as EV deployment proliferates worldwide.

- Major Opportunity: Companies need to embrace the worldwide push for sustainability by developing high-performance lead-free piezoelectric ceramics.

| Key Insights | Details |

|---|---|

| Ceramic Transducers Market Size (2026E) | US$ 3.4 Bn |

| Market Value Forecast (2033F) | US$ 7.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of the EV and Autonomous Systems Sector

The automotive industry is increasing demand for ceramic transducers as EV deployment expands globally. Manufacturers are integrating these components into systems such as battery management systems (BMS), ultrasonic parking assistance, and structural monitoring platforms. Ceramic materials provide piezoelectric properties that allow precise vibration sensing and energy conversion under demanding operating conditions. These characteristics support accurate diagnostics and stable performance within modern electric vehicle architectures. Automotive engineers are prioritizing reliable transducer technology to maintain safety and operational efficiency in high-performance mobility platforms.

Growth in electric mobility and autonomous vehicle development is further strengthening this demand. Government incentives and consumer interest in low emission transportation are accelerating EV adoption worldwide. Automakers are preparing vehicles with advanced driver support and higher autonomy levels that rely on sensing technologies such as light detection and ranging (LiDAR) and ultrasonic proximity systems. Ceramic transducers enable a high-frequency signal response that supports accurate object detection and vehicle positioning in complex driving environments. As intelligent vehicle systems expand, these components are becoming critical elements within next-generation automotive sensor architectures.

Miniaturization in Consumer Electronics and Wearable Technology

Consumer electronics manufacturers are increasingly adopting ceramic transducers due to their compact dimensions and superior energy efficiency compared with conventional metallic components. These devices support miniaturization while maintaining high functional performance in modern electronics. Engineers integrate ceramic transducers into smartphones, wearable devices, and portable gadgets to enable precise haptic feedback systems that enhance tactile user interaction. Micro-scale ceramic actuators and sensors also support reliable operation within tightly engineered electronic designs. This design flexibility is encouraging innovation across portable consumer technology.

The expansion of 5G is strengthening demand for precise sensing and actuation components in next-generation electronics. Advanced haptic systems rely on ceramic piezoelectric layers that convert electrical energy into mechanical motion with high speed and accuracy. Developers are combining these materials with microelectromechanical systems (MEMS) to improve sensitivity for sound and pressure detection. Wearable electronics are benefiting from these capabilities through improved environmental sensing and health-monitoring capabilities. Designers are also pursuing smaller component footprints to support emerging technologies such as augmented reality devices and intelligent accessories. Ceramic transducers are therefore becoming central components in compact, high-performance consumer electronics systems.

High Manufacturing Costs and Technical Complexity

Production of high purity piezoelectric ceramics such as lead zirconate titanate (PZT) requires complex sintering processes and tightly controlled high temperature environments. Manufacturers must use specialized furnaces and maintain precise thermal cycles to achieve consistent material properties. These technical requirements demand significant capital investment in manufacturing infrastructure. As a result, large companies with established facilities maintain a competitive advantage, while small and medium enterprises (SMEs) often face financial barriers to entry. Although engineers are optimizing production workflows, ceramic fabrication remains resource intensive.

Ceramic materials also present manufacturing challenges because they exhibit inherent brittleness during machining and assembly. Cutting, shaping, and integration processes can cause fractures, increasing material waste and production rework. Manufacturers apply protective coatings and advanced handling techniques to reduce structural damage, yet these measures add operational complexity. Researchers are exploring hybrid ceramic composites that improve mechanical resilience while preserving piezoelectric performance. As manufacturing techniques advance, producers are improving yield efficiency and simplifying component integration, which strengthens supply reliability for industries that depend on high-performance ceramic transducers.

Stringent Environmental Regulations on Lead-Based Materials

Regulatory frameworks are increasing pressure on manufacturers to reduce hazardous materials in electronic components. Policies such as the European Union (EU) Restriction of Hazardous Substances (RoHS) Directive place strict limits on lead content in electronics. PZT remains widely used because it provides strong electromechanical performance in sensors and actuators. However, producers are actively researching alternatives such as barium titanate and bismuth sodium titanate to comply with environmental requirements. These development programs require extensive testing and material optimization, which increases research costs across the ceramic transducer sector.

The transition toward lead free ceramic materials is creating temporary supply and development challenges. Engineers must refine new ceramic formulations to achieve performance levels comparable to PZT. This process requires repeated laboratory trials and material validation. In some cases, inconsistent availability of new raw materials also affects production schedules. Manufacturers are responding by diversifying supply sources and investing in scalable synthesis processes that maintain sensitivity and durability. Companies that succeed in commercializing reliable lead-free piezoelectric materials are likely to gain long-term advantages in highly regulated global electronics markets.

Growth in Medical Ultrasound and Diagnostic Imaging

Healthcare providers are increasing the use of ceramic transducers in non-invasive diagnostic equipment such as point-of-care ultrasound (POCUS) and high-intensity focused ultrasound (HIFU) therapy systems. These devices rely on piezoelectric ceramics to generate precise acoustic signals for real-time imaging and targeted therapeutic procedures. Clinicians value this technology because it enables accurate visualization of internal structures without the need for surgical intervention. Medical engineers are refining ceramic transducer design to improve image clarity, penetration depth, and signal stability. These capabilities allow healthcare professionals to diagnose conditions earlier and deliver more precise treatment across clinical and remote care environments.

Demand for advanced imaging technologies is rising as healthcare systems respond to the growing prevalence of chronic diseases and the aging population. Medical device manufacturers are developing ceramic components that tolerate repeated sterilization while maintaining consistent performance. Research teams are also improving the material composition to enhance contrast detection in soft-tissue imaging. Hospitals are adopting compact ultrasound systems that integrate easily into clinical workflows and expand access to diagnostic services. Equipment suppliers are collaborating with original equipment manufacturers (OEMs) to design specialized transducers for applications such as cardiovascular diagnostics and oncology therapies. Improved biocompatibility and reliability are positioning ceramic transducers as critical components in modern medical imaging and therapeutic systems.

Pioneering Lead-Free Ceramic Material Innovation

Manufacturers are developing high-performance lead-free piezoelectric ceramics to align with global sustainability initiatives. Environmental regulations such as the EU RoHS Directive are encouraging companies to replace lead-based materials used in sensors and actuators. Researchers are investigating alternatives such as potassium sodium niobate (KNN) compounds that offer strong electromechanical properties without hazardous elements. Industry laboratories and academic institutions are collaborating to refine synthesis processes that maintain reliability under operational stress. Early testing in commercial devices is demonstrating that these materials can support environmentally responsible electronic and medical technologies.

Companies that scale lead-free ceramic production are strengthening their competitive position in regulated markets. Engineers are optimizing KNN formulations to achieve sensitivity and performance levels comparable to conventional materials. Suppliers are also securing intellectual property rights and long term supply agreements with device manufacturers. Investment in scalable manufacturing techniques is helping reduce production costs while maintaining material quality. This transition allows companies to meet environmental compliance requirements while supporting sustainable product development. Manufacturers that successfully commercialize reliable lead-free ceramics are likely to expand market share and access premium applications focused on environmentally responsible technologies.

Category-wise Analysis

Product Type Insights

Piezoelectric transducers are expected to represent about 55% of the market revenue share in 2026. These devices convert mechanical energy into electrical signals and perform the reverse function with high efficiency. Their capability supports applications that require precise sensing and actuation. Industries use them widely in medical imaging equipment, industrial automation systems, and ultrasonic cleaning devices. Advances in ceramic material engineering and manufacturing techniques are improving sensitivity, durability, and compact device design. These improvements are reinforcing their role in sectors that demand accurate signal conversion and reliable performance.

Capacitive transducers are projected to record the fastest growth during 2026-2033. Manufacturers are integrating these components into consumer electronics that require touch-sensing interfaces and compact sensor systems. Automotive technologies are also adopting them for proximity detection and driver assistance features. Internet of Things (IoT) devices benefit from their small size and low energy consumption, which suits battery-powered electronics. Their cost-efficient production and fast signal response support broad use across emerging technologies such as wearable devices and smart home equipment. Ongoing design improvements are enhancing stability and responsiveness in dynamic operating environments.

Application Insights

Medical imaging is poised to dominate with roughly 42% of the ceramic transducers market revenue share in 2026. Ultrasound diagnostic systems rely on ceramic transducers to produce high-resolution images of internal organs and tissues. Piezoelectric signals convert electrical energy into acoustic waves that allow real-time visualization during clinical examinations. Healthcare providers depend on this technology to support early detection of medical conditions and guide treatment decisions. Hospitals and diagnostic centers integrate these devices into routine imaging procedures because they provide consistent performance and support non-invasive diagnostic methods. Ongoing engineering improvements are enhancing image clarity and penetration depth, which strengthens their role in modern medical diagnostics.

Automotive sensor applications are expected to exhibit the fastest growth from 2026 to 2033. Electric vehicles are incorporating ceramic transducers in systems that monitor battery performance and structural conditions. Parking assistance technologies also rely on ultrasonic sensing to measure distance accurately during vehicle maneuvering. Advanced driver assistance and autonomous driving systems depend on precise sensors that support navigation and collision avoidance. Automotive manufacturers are selecting compact ceramic components designed to withstand constant vibration and elevated temperatures. These materials deliver durable sensing performance, supporting the expansion of connected vehicle technologies.

Regional Insights

Asia Pacific Ceramic Transducers Market Trends

Asia Pacific is anticipated to lead in 2026 with an estimated 43.5% of the ceramic transducer market share. Rapid industrial development in China and India is strengthening regional demand for precision sensing components. Manufacturing sectors are expanding production of consumer electronics, automotive systems, and medical devices that depend on ceramic transducers for sensing and actuation functions. Local supply chains support large-scale integration of these components into products such as smartphones, hybrid vehicles, and diagnostic imaging equipment. Government initiatives that promote advanced manufacturing clusters and industrial innovation are also attracting international investment in materials research and electronics production.

Regional growth is supported by expanding research ecosystems and strong export oriented manufacturing. Governments are investing in infrastructure such as smart factories and digital healthcare networks that rely on sensor technologies. Collaboration between universities and industrial companies is accelerating development of durable piezoelectric ceramic materials that meet international quality standards. Asia Pacific manufacturers are also supplying components for global automotive, consumer electronics, and renewable energy industries. Increasing healthcare demand linked to aging populations is strengthening the adoption of ultrasound diagnostic equipment that uses ceramic transducers. These combined factors are positioning the region as a major center for innovation and large-scale production in advanced sensing technologies.

Europe Ceramic Transducers Market Trends

Europe maintains a prominent position in the global market for ceramic transducers, aided by its advanced industrial base and expertise in precision engineering. Germany, France, and the United Kingdom are leading adoption across automotive manufacturing, healthcare technology, and industrial automation. Manufacturers are integrating ceramic transducers into applications such as electric vehicles, medical diagnostic equipment, and smart manufacturing systems. Regulatory frameworks including the EU RoHS Directive are guiding material selection and encouraging safer production processes. Companies are strengthening quality control practices to ensure compliance with these environmental and safety standards.

Regional market growth is supported by investment in research and sustainable technology development. Governments are promoting renewable energy systems that use sensor technologies to monitor equipment performance and reliability. Universities and industrial partners are collaborating to develop lead-free ceramic materials that deliver strong electromechanical performance. Automotive manufacturers are incorporating advanced sensing systems within autonomous vehicle platforms to improve operational safety. Healthcare providers are expanding the use of portable ultrasound systems that rely on ceramic transducers for diagnostic imaging. Industrial facilities are also adopting vibration monitoring technologies to improve equipment reliability and reduce downtime. These initiatives are strengthening Europe’s role in developing sustainable and high performance sensing technologies.

North America Ceramic Transducers Market Trends

North America represents the second-largest market for ceramic transducers due to its strong technology ecosystem and advanced research capabilities. Companies in the region invest heavily in R&D to design high-performance sensing technologies. Healthcare providers use ceramic transducers in diagnostic imaging systems and medical monitoring equipment. Automotive manufacturers also incorporate these components into vehicle safety systems and driver assistance technologies. Early testing and pilot deployments across industrial environments accelerate the commercialization of new sensor solutions. Regulatory frameworks that promote sustainable manufacturing practices further support steady demand across healthcare, automotive, and industrial sectors.

Manufacturers differentiate products through advanced engineering and compact sensor designs that support emerging technologies. Automotive developers are integrating high-precision transducers into autonomous driving platforms and collision avoidance systems. Healthcare organizations are expanding the use of portable diagnostic devices that enable remote patient monitoring. Industrial facilities are adopting smart manufacturing systems that improve efficiency and reduce production costs. Government funding programs are supporting research projects that connect sensor technologies with renewable energy infrastructure and environmental monitoring. Collaboration among large technology firms, startups, and research institutions is driving improvements in durability, sensitivity, and operational reliability for next-generation ceramic transducer technologies.

Competitive Landscape

The global ceramic transducers market structure is moderately consolidated, with Murata Manufacturing, TDK Corporation, Kyocera, CTS Corporation, and CeramTec collectively holding about 48% of total market share. The industry presents high barriers to entry because production requires specialized expertise in material science and precise control of piezoelectric ceramic processing. Manufacturing processes involve complex sintering stages that demand advanced equipment and strict quality management. As a result, new entrants face substantial capital investment requirements and technical challenges before achieving consistent product performance.

Competitive positioning is defined by the ability to deliver miniaturized and high sensitivity transducers that meet demanding requirements in sectors such as medical technology and aerospace systems. Leading manufacturers are also differentiating themselves through innovation in environmentally compliant materials. Companies are investing in research that supports the transition toward lead free piezoelectric ceramics while maintaining strong electromechanical performance. This balance between regulatory compliance and technical capability is strengthening the market position of established suppliers and reinforcing long term industry consolidation.

Key Industry Developments

- In February 2026, NASA began developing high-temperature ceramic sensors for future Venus missions as conventional silicon electronics fail under the planet’s extreme conditions. These advanced ceramic-based devices can operate in temperatures approaching 600 °C, enabling longer surface exploration where standard electronics quickly degrade.

- In September 2025, Airmar Technology launched two new 1 kW dual-frequency ultra-wide Chirp transducers, the bronze thru-hull B275MWHW and urethane transom-mount TM275MWHW, featuring a concave ceramic array for exceptional sonar coverage.

- In September 2025, PI introduced an online Piezo Component/Transducer Calculator to streamline the design of piezoceramic elements for ultrasonic transducers, enabling quick estimation of static and resonant performance parameters based on user inputs. The tool supports various shapes such as disks, plates, and composites, including lead-free bismuth sodium titanate options.

Companies Covered in Ceramic Transducers Market

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Kyocera Corporation

- CTS Corporation

- CeramTec GmbH

- APC International, Ltd.

- Morgan Advanced Materials

- PI Ceramic GmbH

- Saint-Gobain

- Fuji Ceramics Corporation

- L3Harris Technologies

- Sensor Technology Ltd.

- Channel Technologies Group

- Piezosystem Jena GmbH

- Boston Piezo-Optics Inc.

Frequently Asked Questions

The global ceramic transducers market is projected to reach US$ 3.4 billion in 2026.

The market is driven by the widening applicability of ceramic transducers in automotive electrification and medical imaging.

The market is poised to witness a CAGR of 12% from 2026 to 2033.

Major opportunities lie in lead-free ceramics that address regulatory shifts toward sustainability in electronics.

Murata Manufacturing, TDK Corporation, Kyocera, CTS Corporation, and CeramTec are some of the key players in the market.