- Executive Summary

- Global Central Venous Catheter Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 – 2032, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- COVID-19 Impact Analysis

- Forecast Factors – Relevance and Impact

- Value Added Insights

- Value Chain Analysis

- Technology Assessment

- Product Adoption / Usage Analysis

- Key Market Players

- Regulatory Landscape

- PESTLE Analysis

- Porter’s Five Force Analysis

- Pricing Analysis, 2024

- Key Factors Impacting Prices

- Pricing Analysis by Product Type

- Regional Prices and Product Preferences

- Global Central Venous Catheter Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2019-2023

- Current Market Size (US$ Bn) Analysis and Forecast, 2024–2032

- Global Central Venous Catheter Market Outlook: Product

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product Type, 2019-2023

- Current Market Size (US$ Bn) and Volume (Units) and Forecast Analysis, By Product Type, 2024–2032

- Dialysis Catheters

- Acute Hemodialysis Catheter

- Chronic Hemodialysis Catheter

- Peritoneal Dialysis Catheter

- PICC Catheters

- Implantable Port

- CVC Catheters

- Tunneled Catheters

- Others

- Market Attractiveness Analysis: Product

- Global Central Venous Catheter Market Outlook: Property

- Historical Market Size (US$ Bn) Analysis, By Property, 2019-2023

- Current Market Size (US$ Bn) Analysis and Forecast, By Property, 2024–2032

- Anti-microbial Catheter

- Non-anti-microbial Catheter

- Market Attractiveness Analysis: Property

- Global Central Venous Catheter Market Outlook: Design

- Historical Market Size (US$ Bn) Analysis, By Design, 2019-2023

- Current Market Size (US$ Bn) Analysis and Forecast, By Design, 2024–2032

- Single Lumen

- Double Lumen

- Multiple Lumen

- Global Central Venous Catheter Market Outlook: End-User

- Historical Market Size (US$ Bn) Analysis, By End-User, 2019-2023

- Current Market Size (US$ Bn) Analysis and Forecast, By End-User, 2024–2032

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

- Specialty Clinics

- Others

- Market Attractiveness Analysis: End-User

- Key Highlights

- Global Central Venous Catheter Market Outlook: Region

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2019-2023

- Current Market Size (US$ Bn) and Volume (Units) and Forecast Analysis, by Region, 2024–2032

- North America

- Latin America

- Europe

- East Asia

- South Asia and Oceania

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Central Venous Catheter Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- By Country

- By Product Type

- By Property

- By Design

- By End-User

- Current Market Size (US$ Bn) Analysis and Forecast by Country, 2024–2032

- U.S.

- Canada

- Current Market Size (US$ Bn) and Volume (Units) and Forecast Analysis, By Product Type, 2024–2032

- Dialysis Catheters

- Acute Hemodialysis Catheter

- Chronic Hemodialysis Catheter

- Peritoneal Dialysis Catheter

- PICC Catheters

- Implantable Port

- CVC Catheters

- Tunneled Catheters

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By Property, 2024–2032

- Anti-microbial Catheter

- Non-anti-microbial Catheter

- Current Market Size (US$ Bn) Analysis and Forecast, By Design, 2024–2032

- Single Lumen

- Double Lumen

- Multiple Lumen

- Current Market Size (US$ Bn) Analysis and Forecast, By End-User, 2024–2032

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

- Specialty Clinics

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- Europe Central Venous Catheter Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- By Country

- By Product Type

- By Property

- By Design

- By End-User

- Current Market Size (US$ Bn) Analysis and Forecast by Country, 2024–2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Current Market Size (US$ Bn) and Volume (Units) and Forecast Analysis, By Product Type, 2024–2032

- Dialysis Catheters

- Acute Hemodialysis Catheter

- Chronic Hemodialysis Catheter

- Peritoneal Dialysis Catheter

- PICC Catheters

- Implantable Port

- CVC Catheters

- Tunneled Catheters

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By Property, 2024–2032

- Anti-microbial Catheter

- Non-anti-microbial Catheter

- Current Market Size (US$ Bn) Analysis and Forecast, By Design, 2024–2032

- Single Lumen

- Double Lumen

- Multiple Lumen

- Current Market Size (US$ Bn) Analysis and Forecast, By End-User, 2024–2032

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

- Specialty Clinics

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- East Asia Central Venous Catheter Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- By Country

- By Product Type

- By Property

- By Design

- By End-User

- Current Market Size (US$ Bn) Analysis and Forecast by Country, 2024–2032

- China

- Japan

- South Korea

- Current Market Size (US$ Bn) and Volume (Units) and Forecast Analysis, By Product Type, 2024–2032

- Dialysis Catheters

- Acute Hemodialysis Catheter

- Chronic Hemodialysis Catheter

- Peritoneal Dialysis Catheter

- PICC Catheters

- Implantable Port

- CVC Catheters

- Tunneled Catheters

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By Property, 2024–2032

- Anti-microbial Catheter

- Non-anti-microbial Catheter

- Current Market Size (US$ Bn) Analysis and Forecast, By Design, 2024–2032

- Single Lumen

- Double Lumen

- Multiple Lumen

- Current Market Size (US$ Bn) Analysis and Forecast, By End-User, 2024–2032

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

- Specialty Clinics

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- South Asia & Oceania Central Venous Catheter Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- By Country

- By Product Type

- By Property

- By Design

- By End-User

- Current Market Size (US$ Bn) Analysis and Forecast by Country, 2024–2032

- India

- Indonesia

- Thailand

- Singapore

- ANZ

- Rest of South Asia & Oceania

- Current Market Size (US$ Bn) and Volume (Units) and Forecast Analysis, By Product Type, 2024–2032

- Dialysis Catheters

- Acute Hemodialysis Catheter

- Chronic Hemodialysis Catheter

- Peritoneal Dialysis Catheter

- PICC Catheters

- Implantable Port

- CVC Catheters

- Tunneled Catheters

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By Property, 2024–2032

- Anti-microbial Catheter

- Non-anti-microbial Catheter

- Current Market Size (US$ Bn) Analysis and Forecast, By Design, 2024–2032

- Single Lumen

- Double Lumen

- Multiple Lumen

- Current Market Size (US$ Bn) Analysis and Forecast, By End-User, 2024–2032

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

- Specialty Clinics

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- Latin America Central Venous Catheter Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- By Country

- By Product Type

- By Property

- By Design

- By End-User

- Current Market Size (US$ Bn) Analysis and Forecast by Country, 2024–2032

- Brazil

- Mexico

- Rest of Latin America

- Current Market Size (US$ Bn) and Volume (Units) and Forecast Analysis, By Product Type, 2024–2032

- Dialysis Catheters

- Acute Hemodialysis Catheter

- Chronic Hemodialysis Catheter

- Peritoneal Dialysis Catheter

- PICC Catheters

- Implantable Port

- CVC Catheters

- Tunneled Catheters

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By Property, 2024–2032

- Anti-microbial Catheter

- Non-anti-microbial Catheter

- Current Market Size (US$ Bn) Analysis and Forecast, By Design, 2024–2032

- Single Lumen

- Double Lumen

- Multiple Lumen

- Current Market Size (US$ Bn) Analysis and Forecast, By End-User, 2024–2032

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

- Specialty Clinics

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- Middle East & Africa Central Venous Catheter Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- By Country

- By Product Type

- By Property

- By Design

- By End-User

- Current Market Size (US$ Bn) Analysis and Forecast by Country, 2024–2032

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Current Market Size (US$ Bn) and Volume (Units) and Forecast Analysis, By Product Type, 2024–2032

- Dialysis Catheters

- Acute Hemodialysis Catheter

- Chronic Hemodialysis Catheter

- Peritoneal Dialysis Catheter

- PICC Catheters

- Implantable Port

- CVC Catheters

- Tunneled Catheters

- Others

- Current Market Size (US$ Bn) Analysis and Forecast, By Property, 2024–2032

- Anti-microbial Catheter

- Non-anti-microbial Catheter

- Current Market Size (US$ Bn) Analysis and Forecast, By Design, 2024–2032

- Single Lumen

- Double Lumen

- Multiple Lumen

- Current Market Size (US$ Bn) Analysis and Forecast, By End-User, 2024–2032

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

- Specialty Clinics

- Others

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2023

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping by Market

- Competition Dashboard

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- Angio Dynamics

- Overview

- Segments and Sources

- Key Financials

- Market Developments

- Market Strategy

- C.R. Bard

- Teleflex Incorporated

- B. Braun Melsungen AG

- Kimal Healthcare

- Come B.V.

- Medtronic Plc

- Smiths Medical

- Vygon (UK) Ltd.

- Becton, Dickinson, and Company

- Argon Medical Devices Inc.

- Others

- Angio Dynamics

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Medical Devices

- Central Venous Catheter Market

Central Venous Catheter Market Size, Share, Trends, Growth, and Regional Forecasts 2025 - 2032

Central Venous Catheter Market by Product (Dialysis, Acute Hemodialysis, Chronic Hemodialysis, Peritoneal Dialysis, PICC, Implantable Port, CVC, Tunneled), Property (Anti-microbial, Non-anti-microbial), Design (Single, Double, Multiple), End User (Hospitals, Ambulatory Surgical Centers, Dialysis Centers, Specialty Clinics), and Regional Analysis

Central Venous Catheter Market Size and Share Analysis

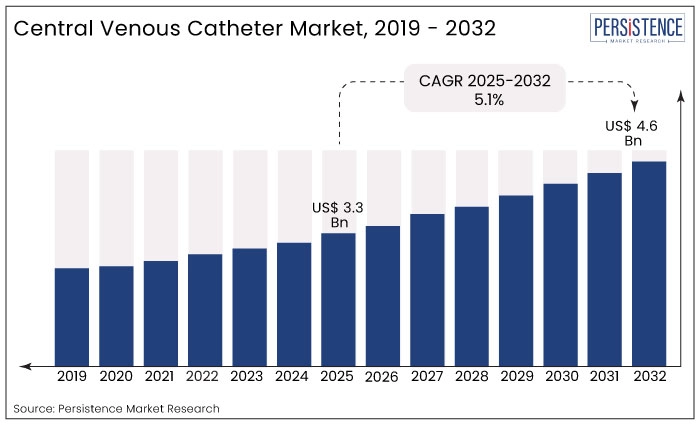

The global central venous catheter market is projected to witness a CAGR of 5.1% during the forecast period from 2025 to 2032. It is anticipated to increase from US$ 3.3 Bn recorded in 2025 to a considerable US$ 4.6 Bn by 2032.

The global central line catheter industry is experiencing significant growth. This growth is driven by the rising incidence of chronic diseases like cancer, kidney failure, and cardiovascular diseases. These conditions require long-term intravenous therapies. The demand for CVCs is also fueled by an increase in surgical procedures across the globe.

Globally, there were about 9.7 million cancer-related deaths and 20.0 million new cases of cancer in 2022. 1 in 5 people are set to have cancer at some point in their lives, and 1 in 9 men, as well as 1 in 12 women will likely pass away from the illness. With non-melanoma skin cancers excluded, the age-standardized global cancer incidence rate (ASR) was 186.5 per 100,000 in 2022.

The need for unique medical devices to manage critically ill patients in intensive care units is growing. Technological developments in catheter materials and infection prevention strategies are supporting wide adoption.

Minimally invasive techniques are further contributing to market growth. The rising geriatric population and the high prevalence of comorbidities are accelerating the market. Increasing healthcare spending and global improvements in medical infrastructure are enhancing market expansion prospects.

Key Highlights of the Market

- Increasing cases of cancer, renal failure, and cardiovascular disorders necessitate long-term intravenous therapies, driving demand for central venous catheters globally.

- Innovations like antimicrobial coatings, bioengineered catheters, and real-time monitoring capabilities enhance safety and efficacy, propelling market growth worldwide.

- In terms of product, CVC catheters are anticipated to showcase a CAGR of 5.6% through 2032 due to rising surgical needs and an aging population globally.

- Based on property, non-anti-microbial catheters are projected to showcase a CAGR of 5.5% through 2032 due to their cost-effectiveness, widespread availability, and suitability for short-term use.

- Middle East and Africa are anticipated to remain at the forefront of the market by witnessing a CAGR of 5.6% through 2032 amid healthcare infrastructure developments.

- Increasing adoption of minimally invasive procedures boosts the use of ultrasound-guided catheter insertions.

- Development of bioengineered catheters offers potential to enhance patient outcomes.

- Partnerships between catheter manufacturers and healthcare providers to improve access in remote areas are set to create opportunities.

|

Market Attributes |

Key Insights |

|

Central Venous Catheter Market Size (2025E) |

US$ 3.3 Bn |

|

Projected Market Value (2032F) |

US$ 4.6 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

4.4% |

North America Central Venous Catheter Market Trends

The North America Central Venous Catheter market is witnessing significant growth, primarily driven by increasing ICU admissions, a rising geriatric population, and a growing burden of chronic illnesses. The U.S. central venous catheter market accounts for the largest share in the region, supported by high healthcare expenditure, widespread use of minimally invasive procedures, and advanced hospital infrastructure. In 2024, the U.S. recorded over 5 million central venous catheter placements annually, reflecting strong clinical demand. Moreover, an increase in cancer-related treatments and dialysis procedures is boosting the use of long-term CVCs such as tunneled catheters and implantable ports. Technological advancements, such as antimicrobial-coated catheters, are further propelling market penetration. Rising hospital-acquired infection concerns are also encouraging the adoption of safety-enhanced CVCs, positioning the U.S. market as a leader.

Middle East and Africa Sees Growth Amid Prevalence of Ischemic Heart Disease

The Middle East and Africa are set to experience rapid growth in the global central venous catheter market, at a CAGR of 5.6% through 2032. The region is growing aware of novel medical procedures and treatments, which has led to a high demand for central venous catheters in healthcare facilities.

Economic growth and improvements in healthcare infrastructure are anticipated in the region. These developments will likely help facilitate the adoption of modern medical technologies, including central venous catheters. Furthermore, the rising prevalence of chronic conditions, such as cardiovascular diseases and diabetes, has increased the need for these catheters, further driving market expansion. For instance,

- In 2022, the prevalence of ischemic heart disease alone was about 5,780 cases per 100,000 persons in North Africa and the Middle East. Stroke and hypertensive heart disease also contributed significantly to this burden. The region's Disability-Adjusted Life Years (DALYs) for hypertensive heart disease were 654.8 per 100,000, suggesting a significant impact on health systems and quality of life.

CVC Catheters Lead due to Surging Cases of Chronic Kidney Disease

|

Category |

CAGR through 2032 |

|

Product- CVC Catheters |

5.6% |

The Central Venous Catheter (CVC) segment is anticipated to hold the most prominent market share in 2025. CVCs, including tunneled and non-tunneled types, are widely used in various medical settings. Their versatility and ability to administer intravenous therapies, monitor blood parameters, and provide long-term access make them essential. The broad range of uses and their critical role in various medical procedures contribute to their dominance in the market.

CVCs are extensively set to be used in peritoneal dialysis. The rising global incidence of chronic kidney diseases has led to an increased demand for peritoneal dialysis as an effective treatment option. Peritoneal dialysis catheters are critical for this procedure, as they facilitate fluid exchange within the abdominal cavity. For instance,

- According to estimates, Chronic Kidney Disease (CKD) affects around 10% of people worldwide, or close to 697 million individuals. As it is associated with consequences, including cardiovascular illnesses and End-Stage Renal Disease (ESRD), the burden is substantial.

Urbanization, aging populations, and the increased frequency of risk factors like diabetes and hypertension have all contributed to a rise in the incidence of CKD. Moreover, it contributes to more than 41.5 million Disability-Adjusted Life Years (DALYs) every year, making it a leading cause of mortality and disability globally.

Non-anti-microbial Catheters Dominate Owing to High-Cost Efficiency

|

Category |

CAGR through 2032 |

|

Property- Non-anti-microbial Catheters |

5.5% |

The non-anti-microbial catheter segment is anticipated to hold the most significant market share in the central venous catheter industry. These catheters are widely used due to their versatility in providing intravenous access across various healthcare settings. Their established safety record and cost-effectiveness further contribute to their dominance in the market.

In contrast, the antimicrobial catheter segment is anticipated to rise at a fast pace. The demand for catheters with built-in antimicrobial properties is increasing. This is because of the urgent need to prevent infections and gain control in healthcare settings.

Market Introduction and Trend Analysis

A Central Venous Catheter (CVC) is a medical device inserted into a large vein, typically in the groin, torso, or neck. It allows for the direct and efficient circulation of substances, fluids, or nutrients into the bloodstream.

CVCs play a key role in patient care by enabling the administration of treatments, monitoring blood parameters, and providing long-term intravenous access. These catheters come in various designs, including peripherally inserted, tunneled, and non-tunneled, each serving different medical purposes. CVCs are especially common in oncology,critical care, and long-term therapies, highlighting their adaptability and importance in modern healthcare systems.

Key players in the global market for triple lumen catheters include BD subsidiaries, Becton, Dickinson and Company, Teleflex Incorporated, and C.R. Bard. These leading healthcare companies have a strong global presence, as demonstrated by the widespread use of CVCs in countries like the U.S., Germany, and Japan.

Historical Growth and Course Ahead

The global central venous catheter industry recorded a decent CAGR of 4.4% in the historical period from 2019 to 2024. This growth was mainly driven by developments in catheter design, materials, and safety features.

Rising number of surgical procedures, increasing prevalence of chronic diseases, and growing demand for long-term vascular access solutions have all played significant roles in the market's expansion. The early adoption of antimicrobial-coated catheters has reduced infection risks, which has helped improve market acceptance.

Growth has been particularly strong in regions with unique healthcare infrastructure, such as North America and Europe. Emerging markets are also showing potential, driven by increased healthcare investments.

The global market is set to continue growing in the next ten years. Technological developments, such as bioengineered catheters and real-time monitoring technologies, will likely support this growth.

Increasing focus on outpatient care, an aging population, and the rise of lifestyle-related diseases are further projected to sustain demand. Emerging markets in Asia Pacific and Latin America present significant opportunities due to improvements in healthcare infrastructure and government support.

Market Growth Drivers

Increasing Prevalence of Chronic Diseases like Diabetes to Propel Demand

The rising prevalence of chronic diseases is a key factor driving the growth of the global central venous catheter market. Chronic conditions like cancer, cardiovascular disorders, and renal failure require long-term medical intervention. As these diseases become more common, the demand for CVCs grows, making them essential in modern healthcare.

Other chronic conditions, such as diabetes, are rising at alarming rates, driving demand for long-term medical interventions like CVCs. For instance,

- The number of people living with diabetes has surged from 200 million in 1990 to over 830 million in 2022, with approximately 589 million adults (20-79 years) living with diabetes.

Cardiovascular diseases and cancers are also prevalent and often require prolonged treatment or monitoring, for which CVCs are essential. As life expectancy increases, so does the risk of chronic illnesses, creating ongoing demand for novel medical devices like CVCs. These catheters are essential for providing intravenous access, administering fluids, and delivering medications in long-term treatments.

Surging Number of Elective Surgeries to Accelerate Demand

One of the main factors driving demand for central venous catheters is the increasing surgical procedures performed worldwide. Mainly in complicated and high-risk procedures, these catheters are essential for patient management before, during, and following surgery.

There has been a noticeable rise in elective surgeries such bariatric operations, orthopedic surgery, and cosmetic procedures due to better access to healthcare, especially in emerging economies. Their demand is further increased by the fact that these surgeries frequently call for CVCs to provide anesthetic, fluids, and post-operative drugs. For instance,

- In 2022, hospitals in China performed more than 82.7 million inpatient surgical procedures. In India, electric procedures, specifically those involving orthopedics, hernia repairs, and C-sections, are projected to rise in the next ten years.

Market Restraining Factors

Rising Concerns Regarding Healthcare-associated Infections to Limit Growth

Despite the significant growth of the global central venous catheter market, there is a key challenge to consider. The rising concern over Healthcare-Associated Infections (HAIs) is anticipated to hamper demand. While Central Venous Catheters (CVCs) are crucial in medical treatments, they are associated with an increased risk of infections, which hinders market growth. For instance,

- The incidence of Central Line-associated Bloodstream Infection (CLABSI) in patients with two CVCs is nearly double compared to those with just one catheter, A study on Peripheral Venous Catheters (PVCs) found that about 6% of healthcare-associated bloodstream infections in hospitals across Europe were related to PVC use.

Bloodstream infections, particularly those related to catheter use, have become a key concern for regulators, policymakers, and healthcare providers. Strict adherence to antiseptic procedures and infection control protocols is essential during catheter insertion and maintenance to prevent infections.

Key Market Opportunities

Constant Innovations in Catheter Design and Materials to Create Prospects

Continuous developments in catheter technology are positively shaping the global central venous catheter market. These innovations enhance healthcare efficiency and improve patient outcomes. The ongoing development of CVC materials, designs, and features has led to safer, more user-friendly devices with a wider range of applications. As a result, CVCs have become essential tools in modern medical practice.

New catheter designs, such as those with antimicrobial coatings, help reduce the risk of infections associated with catheter use. These improvements not only boost patient safety but also reduce the financial burden of catheter-related infections on healthcare systems.

The integration of intelligent technologies, like monitoring devices and sensors, allows for real-time data collection and remote patient monitoring. This enables proactive interventions and aligns with the growing trend of digital health, transforming traditional catheters into novel tools that provide valuable insights into patient health.

Competitive Landscape for the Central Venous Catheter Market

C.R. Bard (a subsidiary of BD), Becton, Dickinson and Company, and Teleflex Incorporated are key players in the central venous access device industry. These companies employ various strategies to maintain and extend their market presence.

They prioritize ongoing technological developments in catheters to meet the evolving needs of healthcare providers and patients. For instance, Becton, Dickinson, and Company often invest heavily in research and development. The company focuses on introducing catheters with novel features such as intelligent monitoring capabilities and antimicrobial coatings. This focus on innovation enhances the safety and effectiveness of its products, establishing it as leader in the industry.

As part of BD, C.R. Bard engages in strategic acquisitions to extend its product offerings and market presence. These acquisitions allow the company to diversify its portfolio by adding complementary businesses. This strategy not only strengthens its market position but also provides healthcare providers worldwide with comprehensive solutions.

Recent Industry Developments

- In July 2024, Teleflex Incorporated, a leading global provider of medical technologies based in the U.S., announced the establishment of the Teleflex Center for Antimicrobial Protection (TCAP) as a strategic branch of its Vascular Access business unit led by Chuck Gartner, Director of Marketing - Strategic Initiatives.

- In February 2024, AngioDynamics, Inc., based in the U.S., announced that it has completed the sale of its Peripherally Inserted Central Catheter (PICC) and midline catheter portfolios to Spectrum Vascular. It is a medical device company focused on vascular access and medication management.

Companies Covered in Central Venous Catheter Market

- Angio Dynamics

- C.R. Bard

- Teleflex Incorporated

- B. Braun Melsungen AG

- Kimal Healthcare

- Come B.V.

- Medtronic Plc

- Smiths Medical

- Vygon (UK) Ltd.

- Becton, Dickinson, and Company

- Argon Medical Devices Inc.

Frequently Asked Questions

The global market is estimated to increase from US$ 3.3 billion in 2025 to US$ 4.6 billion in 2032.

Increasing Prevalence of Chronic Diseases like Diabetes to Propel Demand and Surging Number of Elective Surgeries to Accelerate Demand.

The market is projected to record a CAGR of 5.1% during the forecast period from 2025 to 2032.

Angio Dynamics and C.R. Bard are considered the leading manufacturers.

Market opportunities include Constant Innovations in Catheter Design and Materials to Create Prospects.