Comprehensive Snapshot for Cargo Drone Market Including Regional and Country Analysis in Brief.

Industry: Industrial Automation

Published Date: April-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 140

Report ID: PMRREP35210

The global cargo drone market size is anticipated to rise from US$ 2,134.5 Mn in 2025 to US$ 16,561.2 Mn to witness a CAGR of 34.1% till 2032. The increasing need for faster and more efficient delivery solutions encourages the adoption of cargo drones. Logistical companies are turning to cargo drones to improve their shipping operations especially in remote areas that are inaccessible with traditional transportation methods. Drones offer a cost-effective and quick way to transport goods making them a practical choice for remote locations.

Key Industry Highlights:

|

Global Market Attribute |

Key Insights |

|

Cargo Drone Market Size (2025E) |

US$ 2,134.5 Mn |

|

Market Value Forecast (2032F) |

US$ 16,561.2 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

34.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

29.8% |

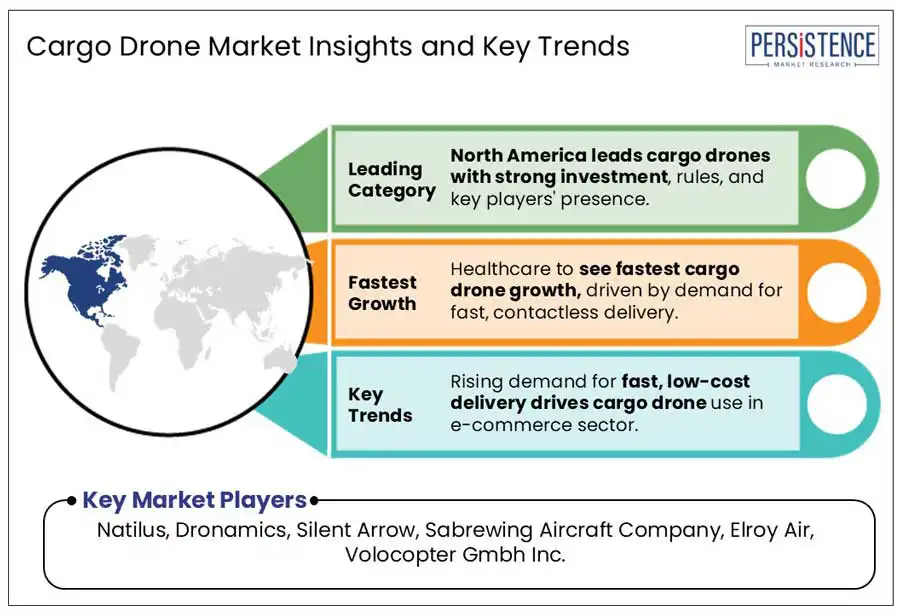

The growing need for fast, low-cost, and efficient package delivery boosts the cargo drone market. E-commerce companies are turning to drones to meet this demand. Drones help speed up deliveries by avoiding traffic and flying directly to their destinations. Walmart has expanded its drone delivery service to cover 1.8 million homes in the Dallas-Fort Worth area, showing how drones can improve delivery times. Drones also help cut costs related to vehicle maintenance, fuel, and labor. In December 2024, DroneUp received FAA approval to fly drones beyond the operator’s line of sight, helping reduce costs and expand operations. In February 2024, Zipline partnered with WellSpan Health in Pennsylvania to deliver prescriptions and medical samples. Similarly, Skyports Drone Services teamed up with the Port Authority of New York and New Jersey to test drone deliveries in busy urban areas.

High prevalence of cybersecurity risks and a shortage of skilled drone operators are challenging factors. As drones become more common in delivery and transport, there is a growing need for trained pilots. Drones are used by the government agencies to track weather, security surveillance, and manage disaster response. Since, they transact volumes of video and audio data, they are susceptible to cybersecurity risks. Moreover, the devices can be hacked to spread disruption, especially if the drones use weak security layers. Many cargo drones possess design flaws and lack basic features such as encrypted video feeds or secure wireless systems. Therefore, their vulnerability to attack creates a bottleneck for large-scale operations.

The application of cargo drones in middle-mile logistics is emerging as a pivotal growth opportunity within the broader drone delivery ecosystem. Traditionally overshadowed by last-mile delivery solutions, the middle-mile segment referring to the transportation of goods between key logistics hubs such as ports, distribution centers, and retail facilities is now receiving increased industry focus.

Drones specifically engineered for middle-mile operations are equipped with greater payload capacities and extended flight ranges, positioning them as viable alternatives to conventional ground transport. For example,

The 50–149 Kg payload segment is projected to witness a high growth in the cargo drone market in the forecast period. This strikes a balance between range, cost-efficiency, and operational versatility, making it suitable for a wide range of industries such as healthcare, retail, logistics, and agriculture. Leading manufacturers such as Elroy Air and Dronamics are investing heavily in this space. For instance, Elroy Air’s Chaparral drone supports a payload capacity of up to 136 Kg (300 lbs) with a range of 300 miles, positioning it perfectly for cost-effective cargo transport. Similarly, Dronamics’ Black Swan cargo drone offers a payload of 350 Kg although a volume of operations is still categorized under the 150 Kg mark due to regional regulations.

The healthcare sector is expected to experience the fast-growth in the cargo drone market in the coming years. The growing need for rapid, reliable, and contactless delivery of medical supplies, vaccines, blood samples, and prescription drugs especially in remote or underserved regions is a major driving factor. Cargo drones are proving to be game-changers for healthcare logistics by significantly reducing delivery times and improving access to critical medical resources. The COVID-19 pandemic further accelerated the adoption of drones in this space, highlighting their potential in crisis response and routine healthcare delivery.

North America is expected to lead the global industry thanks to large investments, advanced technology, and strong government support. The U.S. and Canada are home to several major companies and startups that are changing how goods are delivered using drones. A major reason for this growth is the rapid development of drone technology.

The U.S. plays a key role, with leading manufacturers such as Natilus, Sabrewing Aircraft Company, Elroy Air, and Silent Arrow. In 2021, the U.S. Aviation Authority (FAA) approved drone for military tactics, commercial, and personal use. Big companies such as Boeing are pushing drone technology further.

In January 2024, Drone Delivery Canada (DDC) signed new deals worth $417,000, with help from Air Canada. These contracts added a new delivery site at a medical clinic in Leduc, Alberta, and built on DDC’s existing drone delivery route in the area. This shows how drones are being used for real-world solutions like delivering medical supplies efficiently.

Europe is quickly establishing itself as a major player in the global cargo drone market, driven by increasing demand for efficient logistics, strong regulatory support, and a focus on sustainability. The European Union’s commitment to green transportation solutions has accelerated the adoption of cargo drones, especially in urban logistics and remote area connectivity. Additionally, the region benefits from advanced infrastructure and growing investment in drone technology.

Key players such as Dufour Aerospace (Switzerland), Wingcopter (Germany), and Drone Delivery Services (UK) are at the forefront of innovation. In September 2024, Dufour Aerospace renewed its partnership with Areion Group (U.S.), confirming the sale of 40 Aero2 drones with the option to purchase 100 more, highlighting growing global trust in European drone solutions. Similarly, Wingcopter has launched several pilot projects across Germany and the UK to deliver medical and e-commerce goods in hard-to-reach areas.

Asia Pacific cargo drone market is rapidly expanding, driven by rising e-commerce demand, government-backed drone policies, and investments in next-generation logistics infrastructure. Countries such as China, Japan, South Korea, and India are emerging as major contributors to the region's drone ecosystem, with both local startups and global manufacturers tapping into the high-growth potential.

China leads the region with companies such as JD Logistics and EHang actively using drones for last-mile and middle-mile deliveries. JD.com, through JD Logistics, has successfully deployed drone delivery services across rural China, completing thousands of deliveries in hard-to-reach areas. Meanwhile, EHang focuses on autonomous aerial cargo platforms and has received multiple certifications for urban logistics use.

In India, startups such as Skye Air Mobility are collaborating with government healthcare initiatives, delivering medical supplies and vaccines to remote regions under the Medicines from the Sky project.

The global cargo drone market is rapidly evolving and highly competitive, characterized by the presence of numerous established players and emerging startups aiming to secure market share through technological innovation, strategic alliances, and international expansion. Leading companies such as Zipline, Amazon Prime Air, UPS Flight Forward, and DHL are at the forefront, with strong operational footprints, extensive R&D investments, and a focus on autonomous and electric drone models to address growing demand in the logistics and healthcare sectors.

Smaller and regional players such as Wingcopter, Elroy Air, and Dronamics are enriching market diversity by delivering cost-effective, mid-range payload drones tailored to specific use-cases such as rural healthcare logistics, industrial supply chains, and military support. Their agility and customization capabilities are helping them carve out niche segments within the competitive landscape.

|

Report Attribute |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

|

Customization and Pricing |

Available upon request |

By Payload

By Type

By Industry

By Region

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 2,134.5 Mn in 2025.

The cargo drone market is driven by rising demand for efficient last-mile delivery, and technological advancements in drone capabilities.

The industry is estimated to rise at a CAGR of 34.1% from 2025 to 2032.

Expansion of drone delivery in remote and rural areas, and integration of AI and IoT for smart logistics are the key market opportunities.

Natilus, Dronamics, Silent Arrow, Sabrewing Aircraft Company, Elroy Air, Volocopter Gmbh Inc. are a few leading players.