- Beverages

- Caffeinated Beverage Market

Caffeinated Beverage Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Caffeinated Beverage Market by Product Type (Carbonated Soft Drinks, Coffee-based Beverages, Tea-based Beverages, Energy Drinks, Sports Drinks, Others), by Flavor (Natural, Artificial), by Distribution Channel (HoReCa, Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, Others), by Regional Analysis, 2026 - 2033

Caffeinated Beverage Market Share and Trends Analysis

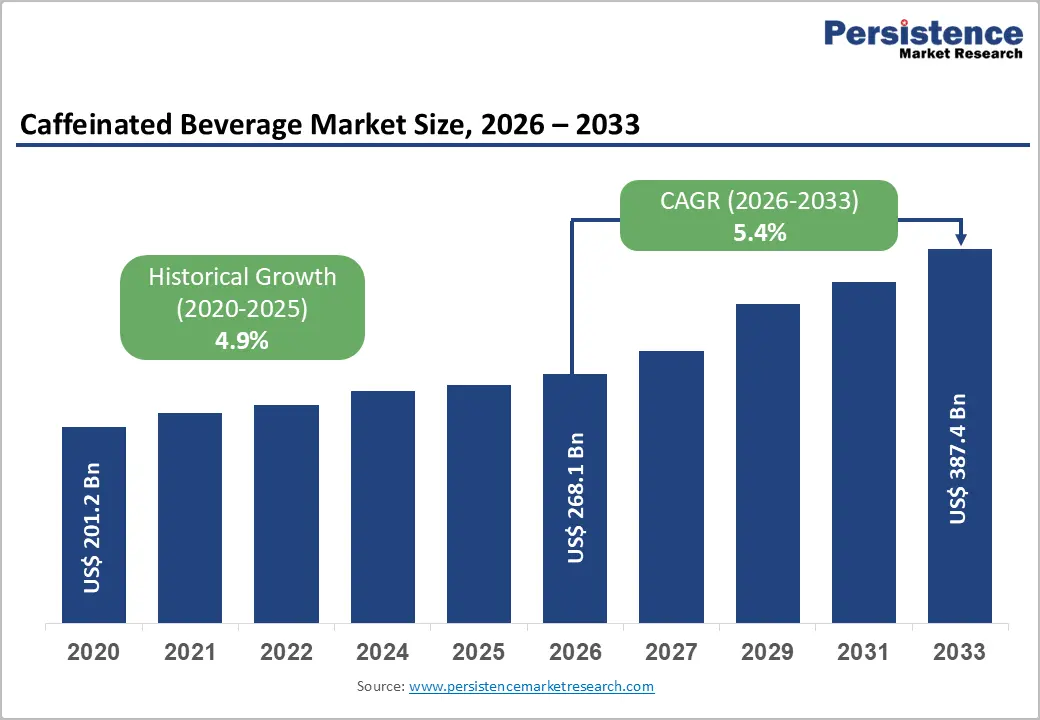

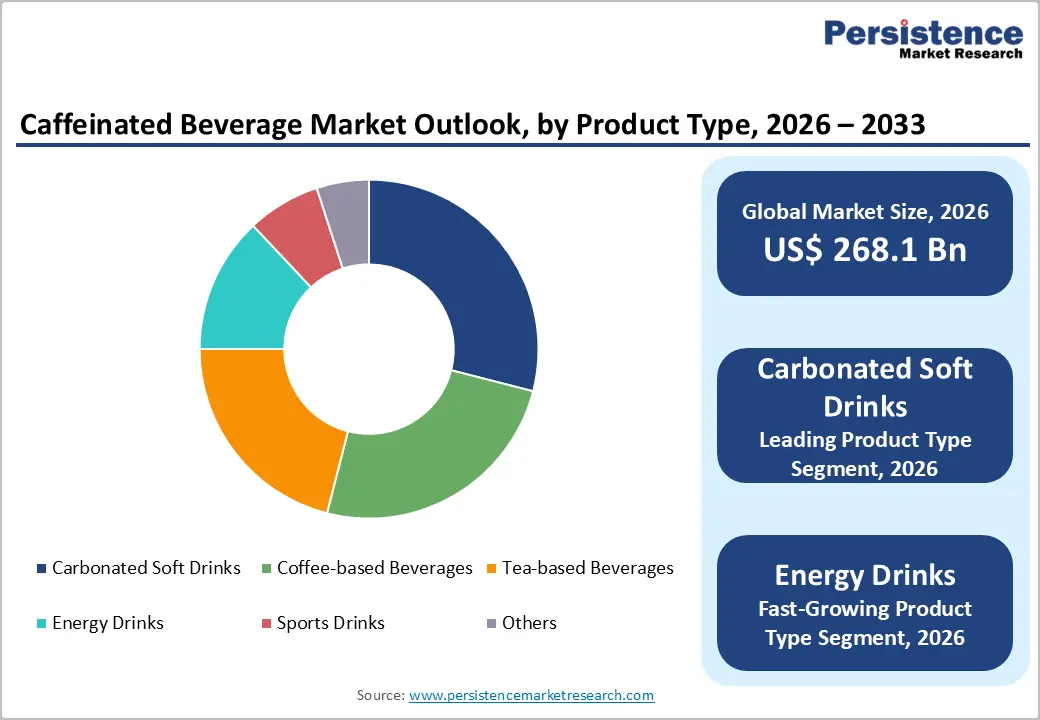

The global caffeinated beverage market is estimated to grow from US$ 268.1 billion in 2026 to US$ 387.4 billion, projected to record a CAGR of 5.4% during the forecast period from 2026 to 2033.

The market is evolving beyond traditional coffee and carbonated drinks as consumers increasingly prioritize functionality, portability, wellness, and flavor innovation. Rapid urbanization, demanding work schedules, fitness-oriented lifestyles, and growing demand for convenient energy solutions are accelerating category expansion across developed and emerging economies.

Beverage manufacturers are actively reshaping portfolios through clean-label ingredients, natural caffeine sources, reduced sugar formulations, and premium ready-to-drink offerings. Consumer purchasing behavior is also shifting toward functional beverages that support mental alertness, productivity, hydration, and active lifestyles.

Key Industry Highlights

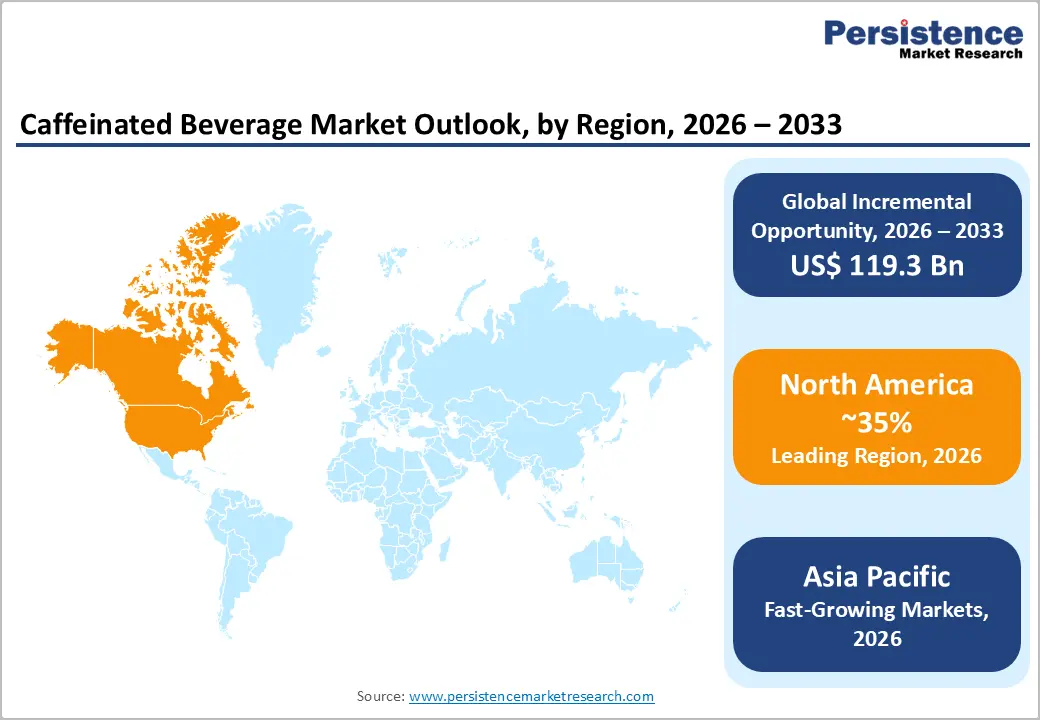

- Leading Region: North America, holding approximately 36% market share, driven by strong demand for premium energy drinks, ready-to-drink coffee, clean-label beverages, and convenience-focused consumption patterns.

- Fastest-Growing Region: Asia Pacific, expected to grow at a CAGR of 7.2%, fueled by urbanization, expanding café culture, rising youth population, and increasing adoption of functional caffeinated beverages.

- Fastest-Growing Product Type Segment: Energy Drinks, projected to grow at a CAGR of 6.8% during the forecast period, supported by rising demand for instant energy, fitness-focused consumption, gaming culture, and portable stimulation beverages.

- Leading Nature Segment: Natural Flavors, accounting for approximately 64% market share in 2025, driven by increasing preference for clean-label ingredients, authentic taste profiles, and reduced reliance on artificial additives.

- Market Drivers: Ready-to-drink caffeinated beverages are gaining strong traction due to convenience-led consumption, on-the-go lifestyles, expanding retail accessibility, and growing preference for functional refreshment solutions.

- Consumer Trends: Consumers are increasingly shifting toward low-sugar, plant-based, vitamin-enriched, and wellness-oriented caffeinated beverages with transparent ingredient labeling and sustainable packaging formats.

- Opportunities: Growing demand for low-sugar and clean-label caffeine drinks is creating opportunities for companies to develop botanical, organic, and naturally functional beverage portfolios targeting health-conscious consumers.

Market Dynamics

Driver: Ready-to-drink Caffeinated Beverages Boost Convenience-led Demand Across Markets

Busy consumer lifestyles and increasing preference for instant refreshment are significantly driving demand for ready-to-drink caffeinated beverages across global markets. Consumers are increasingly choosing portable beverages that provide energy, alertness, and convenience during commuting, work, fitness, and travel activities. Products such as ready-to-drink coffee, energy drinks, caffeinated teas, and sparkling beverages are gaining strong popularity due to their easy availability and no-preparation format.

Younger demographics, particularly urban millennials and Gen Z consumers, are contributing substantially to category growth as they seek quick and functional beverage options suited to fast-paced routines. Beverage manufacturers are expanding product portfolios with low-sugar, clean-label, plant-based, and vitamin-enriched variants to align with evolving health preferences. In addition, wider availability through supermarkets, convenience stores, vending machines, online retail platforms, and food delivery channels is improving product accessibility, encouraging impulse purchases, and strengthening overall market penetration worldwide.

Restraint: Health Concerns Over Excessive Caffeine Intake Limit Consumption

Rising consumer awareness regarding the health effects of excessive caffeine consumption is emerging as a significant restraint for the caffeinated beverage market. High intake of caffeine is increasingly associated with sleep disturbances, anxiety, elevated heart rate, dehydration, and blood pressure concerns, encouraging many consumers to moderate their consumption habits. Parents and healthcare professionals are also raising concerns regarding caffeine intake among teenagers and young adults, particularly through energy drinks and highly concentrated beverages.

Regulatory scrutiny over caffeine content labeling, marketing practices, and age-related consumption guidelines is further creating challenges for manufacturers. In response, several consumers are shifting toward caffeine-free beverages, herbal drinks, and naturally functional alternatives perceived as healthier options. Growing preference for balanced wellness lifestyles and reduced stimulant dependency is expected to limit consumption frequency and restrain long-term market expansion across several consumer demographics globally.

Opportunity: Low-sugar and clean-label caffeine drinks for wellness consumers

Wellness-driven beverage choices are opening strong growth opportunities for companies operating in the global caffeinated beverage market. Consumers are increasingly seeking low-sugar, natural, and clean-label caffeine drinks that deliver energy support without excessive artificial ingredients, preservatives, or high-calorie formulations. This shift is encouraging key players and startups to develop beverages containing plant-based caffeine sources, botanical extracts, functional ingredients, and natural sweeteners such as stevia and monk fruit.

Products positioned around transparency, reduced sugar content, and recognizable ingredient lists are gaining stronger acceptance among fitness-focused and health-conscious consumers. Demand is particularly increasing for functional coffees, organic teas, adaptogenic energy drinks, and sparkling caffeinated waters targeting balanced lifestyles. Emerging brands are leveraging innovative flavors, sustainable packaging, and digital-first marketing strategies to differentiate themselves in competitive markets, while established manufacturers are expanding premium wellness-oriented product portfolios to capture evolving consumer preferences globally.

Category-wise Analysis

By Product Type, Energy Drinks are expected to show lucrative growth during forecast period

Energy Drinks are expected to show promising growth of CAGR 6.8% during forecast period as consumption shifts toward instant energy solutions. Fast-paced routines, extended screen exposure, and irregular sleep patterns are increasing reliance on functional stimulation. Energy drinks deliver predictable caffeine doses combined with taurine, B-vitamins, and sugars or alternatives, appealing to performance-oriented users. Their availability across retail, vending, gyms, and convenience channels reinforces impulse purchasing and frequent consumption occasions, especially among younger demographics seeking rapid alertness.

Growth is further supported by continuous product reinvention and broader usage positioning. Brands are introducing sugar-free variants, natural caffeine sources, and performance-focused packaging to address evolving wellness expectations. Energy drinks are increasingly associated with sports, gaming, nightlife, and fitness cultures, expanding relevance beyond workday fatigue. Compact portability, aggressive branding, and experiential marketing strengthen emotional connections, supporting competitive momentum against traditional beverages.

By Nature, natural flavors dominate the global caffeinated beverage market

Natural flavors hold approximately 64% market share as of 2025, highlighting a clear consumer shift toward transparency and ingredient familiarity. Buyers increasingly associate fruit essences, botanical extracts, and plant-derived flavorings with cleaner labels and a more wholesome image. In caffeinated beverages, natural flavors complement coffee, tea, yerba mate, and guarana bases, helping preserve authentic taste profiles. This natural alignment improves consumer trust, encourages repeat purchases, and supports broader acceptance among demographics that are cautious about artificial additives.

The dominance of natural flavors is further strengthened by regulatory considerations and innovation-led strategies. Familiar flavor sources reduce formulation complexity and ease compliance across multiple regions. Natural flavor profiles enhance premium appeal in ready-to-drink coffees, energy drinks, and functional beverages. As wellness-oriented purchasing grows, these flavor systems enable low-sugar, organic, and functional launches without sacrificing taste consistency, supporting differentiation and global scalability.

Regional Insights

North America Caffeinated Beverage Market Trends

North America holds approximately 36% market share in the global caffeinated beverage market, supported by strong consumer preference for functional drinks, premium coffee products, and convenient ready-to-drink beverages. The region continues to witness growing demand for energy drinks, cold brew coffee, caffeinated sparkling water, and wellness-focused formulations with clean-label ingredients. Increasing health awareness is encouraging beverage manufacturers to introduce low-sugar, organic, and plant-based caffeine alternatives. Expanding café culture, digital retailing, and product innovation in flavors and functional ingredients are further strengthening regional market growth.

U.S. Caffeinated Beverage Market Trends

The U.S. caffeinated beverage market is experiencing strong demand for premium energy drinks, functional coffees, and protein-infused caffeinated beverages among fitness-focused and working consumers. The rising popularity of on-the-go consumption, subscription beverage services, and healthier caffeine formulations is driving continuous product innovation across retail and e-commerce channels.

Canada Caffeinated Beverage Market Trends

Canada caffeinated beverage market is witnessing increasing interest in natural and sustainably sourced beverages with transparent ingredient labeling. Consumers are increasingly preferring low-calorie energy drinks, organic teas, and plant-based caffeine products aligned with wellness-oriented lifestyles and environmentally conscious purchasing behavior.

Asia Pacific Caffeinated Beverage Market Trends

Asia Pacific Caffeinated Beverage Market is expected to grow at a CAGR of 7.2%, fueled by rapid urbanization, evolving work cultures, and rising demand for convenient energy-boosting beverages. Consumers across the region are increasingly adopting ready-to-drink coffee, functional teas, and flavored energy beverages suited to fast-paced lifestyles. Expanding convenience retail networks, café chains, and digital food delivery platforms are further supporting product accessibility and consumption growth. Manufacturers are also introducing fruit-infused, herbal, and low-sugar caffeinated beverages tailored to regional taste preferences and wellness trends.

China Caffeinated Beverage Market Trends

China caffeinated beverage market is witnessing rising demand for premium coffee, canned energy drinks, and innovative tea-based caffeine products among younger urban consumers. Social media-driven beverage trends, expanding café culture, and growing interest in functional wellness drinks are accelerating product innovation and brand competition.

India Caffeinated Beverage Market Trends

India caffeinated beverage market is benefiting from increasing youth population, longer working hours, and rising consumption of affordable ready-to-drink beverages. Expanding modern retail infrastructure and the growing popularity of energy drinks among students and fitness-conscious consumers are supporting sustained market growth.

Competitive Landscape

The global caffeinated beverage market is moderately fragmented, with established beverage companies, regional brands, and startups competing through continuous product innovation and lifestyle-focused marketing strategies. Leading companies are emphasizing clean-label sourcing, natural caffeine ingredients, recyclable packaging designs, and low-sugar formulations to attract health-conscious consumers. Innovation across ready-to-drink coffee, functional teas, botanical energy drinks, and flavored sparkling beverages is strengthening competitive differentiation in the market.

Companies are increasingly targeting the B2C segment through e-commerce expansion, social media campaigns, subscription beverage models, and convenience-driven retail strategies. Government regulations related to caffeine disclosure, sugar reduction, and ingredient transparency are encouraging manufacturers to improve labeling practices and reformulate products. Fruit-infused flavors, exotic blends, and wellness-oriented beverages are gaining popularity among younger consumers. Brands are also investing in consumer education initiatives promoting responsible caffeine intake and healthier beverage choices.

Key Industry Developments:

- In April 2026, Starbucks introduced Energy Refreshers in U.S. stores, offering a new year-round caffeinated beverage option targeting energy-seeking consumers.

- In January 2026, The Coca-Cola Company expanded its Bodyarmor portfolio with Flash I.V. Caffeine Zero Sugar, strengthening its presence in the functional hydration and energy beverage segment.

- In January 2026, BLU Energy Drink announced the full-scale launch of its brand and product lineup in the United States, including a Zero Sugar variant targeting health-conscious energy drink consumers.

- In December 2025, Celsius Holdings, Inc. introduced four new zero-sugar, fruit-forward flavors across the UK and Ireland, expanding its portfolio in line with growing demand for healthier energy beverages.

Companies Covered in Caffeinated Beverage Market

- The Coca-Cola Company

- PepsiCo, Inc.

- Keurig Dr Pepper

- Nestlé S.A.

- National Beverage Corp.

- Red Bull GmbH

- Monster Beverage Corporation

- Asahi Group Holdings Ltd.

- Britvic plc

- Suntory Beverage and Food Limited

- Danone S.A.

- The Kraft Heinz Company

- Unilever

- Jones Soda Co.

- Others

Frequently Asked Questions

The global caffeinated beverage market is projected to be valued at US$ 268.1 Bn in 2026.

The growing demand for convenient ready-to-drink caffeinated beverages is driving the global caffeinated beverage market.

The global caffeinated beverage market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Low-sugar and clean-label caffeinated beverages targeting wellness-focused consumers are emerging as key growth opportunities in the global caffeinated beverage market.

The Coca-Cola Company, PepsiCo, Inc., Keurig Dr Pepper, National Beverage Corp., Red Bull GmbH, and Monster Beverage Corporation.