- Medical Devices

- Blood Collection Tubes Market

Blood Collection Tubes Market Size, Share and Growth Forecast, 2026 - 2033

Blood Collection Tubes Market by Product (Serum Separating Tube, EDTA Tube, Plasma Separation Tube, Serum Tube), Material (Glass, Plastics), End-user (Diagnostic Center, Healthcare Center, Research & Development Centers), and Regional Analysis for 2026 - 2033

Blood Collection Tubes Market Share and Trends Analysis

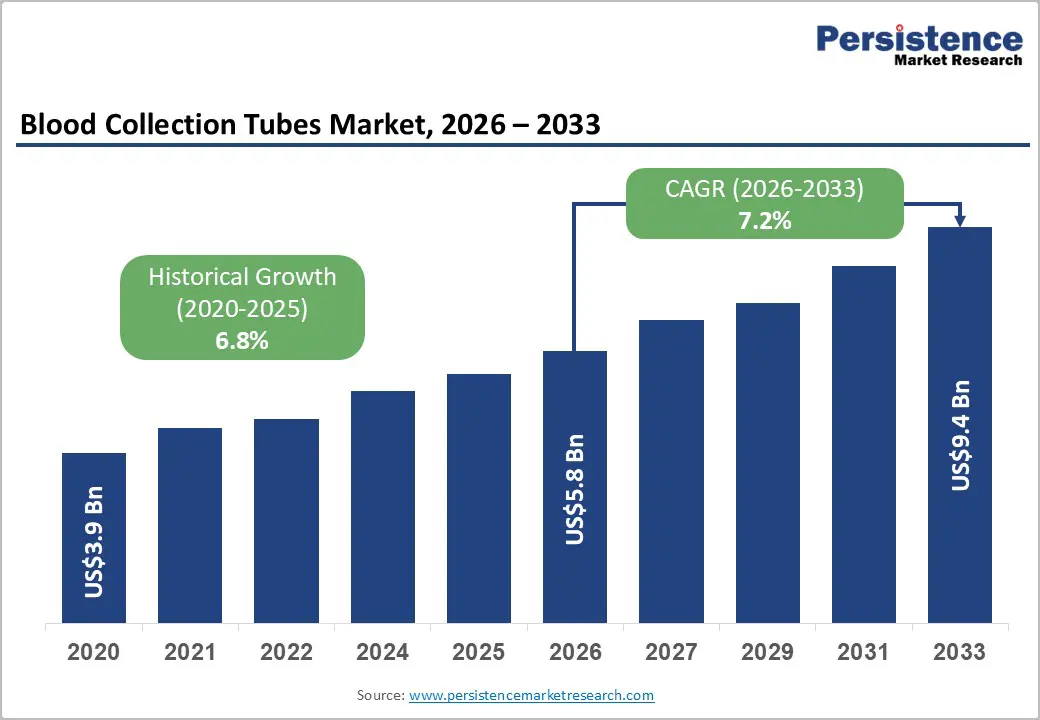

The global blood collection tubes market size is likely to be valued at US$5.8 billion in 2026 and is projected to reach US$9.4 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by rising global diagnostic testing volumes, increasing prevalence of chronic diseases such as diabetes and cardiovascular disorders, and expanding laboratory infrastructure in emerging economies.

According to the World Health Organization (WHO), diagnostic testing accounts for over 70% of clinical decision-making processes, reinforcing demand for consumables such as vacutainer tubes, EDTA (Ethylenediaminetetraacetic Acid) tubes, and serum separator tubes. Additionally, regulatory emphasis on safe blood collection practices is increasing adoption of standardized collection systems.

Key Industry Highlights:

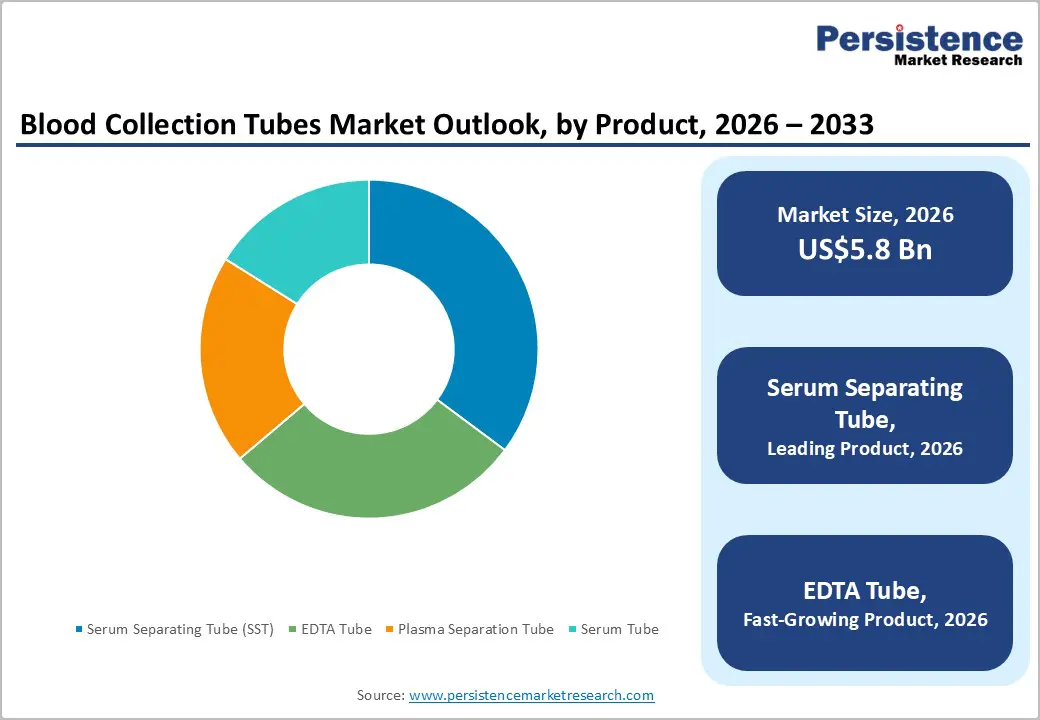

- Dominant Product Type: Serum separating tubes are expected to command approximately 35% of the market share in 2026, while EDTA tubes are projected to be the fastest-growing product segment through 2033, driven by rising hematology testing volumes and increasing blood disorder diagnostics.

- Leading Material: Plastics are anticipated to dominate with an estimated 78% share in 2026 owing to their safety, durability, and compatibility with automated laboratory systems, while glass tubes are expected to witness comparatively slower growth during the forecast period.

- Dominant End-user: Diagnostic Centers are set to account for approximately 46% of market revenue in 2026, supported by growing diagnostic workloads and preventive health screening programs. Research & Development Centers are likely to register the fastest growth through 2033, fueled by expanding clinical research and biotechnology investments.

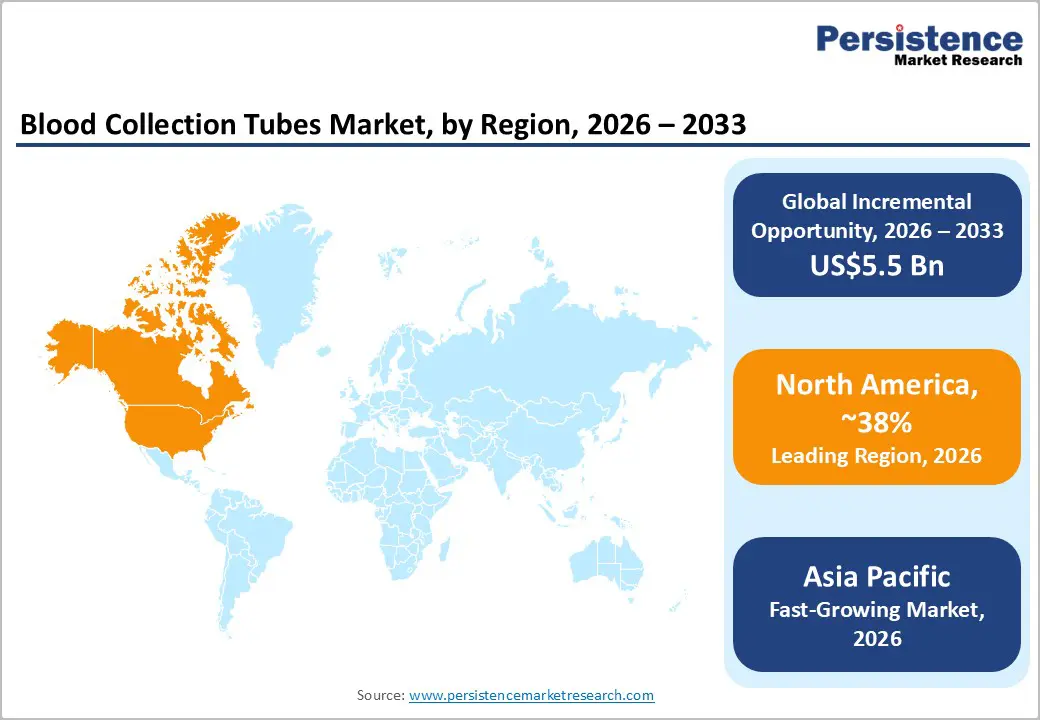

- Regional Leadership: North America is anticipated to lead with an estimated 38% share in 2026, supported by advanced diagnostic infrastructure and high laboratory testing volumes, while Asia Pacific is projected to be the fastest-growing regional market through 2033, driven by healthcare expansion, aging populations, and increasing government healthcare investments.

- Competitive Environment: Market competition is centered on automation-compatible product innovation, regulatory compliance, manufacturing expansion, and strategic partnerships aimed at strengthening global distribution networks and laboratory workflow integration.

DRO Analysis

Driver - Rising Global Burden of Chronic and Infectious Diseases Driving Diagnostic Testing Demand

The increasing prevalence of chronic and infectious diseases is a major structural driver for the blood collection tubes market. According to the WHO and CDC, non-communicable diseases (NCDs) account for nearly 74% of global deaths, with diabetes and cardiovascular diseases requiring frequent blood monitoring. The U.S. CDC also reports that over 37 million Americans have diabetes, significantly increasing routine diagnostic testing requirements. Similarly, tuberculosis and hepatitis screening programs in Asia and Africa are expanding laboratory testing volumes.

This rising diagnostic workload directly increases demand for blood collection tubes, especially EDTA and serum separator tubes used in hematology and biochemistry testing. Hospitals, diagnostic centers, and pathology labs are expanding capacity, particularly in urban healthcare ecosystems. The market impact is reflected in higher procurement cycles and recurring consumable usage, reinforcing steady revenue growth for manufacturers such as Becton Dickinson and Greiner Bio-One.

Restraint - Strict Regulatory Compliance and Waste Management Challenges Limiting Market Scalability

A key restraint in the blood collection tubes market is stringent regulatory oversight combined with biomedical waste disposal challenges. Regulatory bodies such as the U.S. FDA, the European Union's IVDR framework, and India's CDSCO enforce strict quality and safety standards for blood collection devices. Compliance with ISO 6710 standards for single-use tubes increases production complexity and cost.

Plastic-based blood collection tubes also generate significant biomedical waste, raising environmental concerns. Hospitals and diagnostic labs face increasing pressure to adopt sustainable waste management practices, particularly in Europe under the EU Medical Waste Framework. Disposal costs can account for up to 8-12% of total laboratory operational expenses. These factors increase procurement costs and limit adoption in price-sensitive regions, impacting smaller manufacturers and slowing market penetration in rural healthcare systems.

Opportunity - Expansion of Automated Diagnostic Laboratories and Emerging Market Healthcare Infrastructure

A significant opportunity in the blood collection tubes market lies in the expansion of automated diagnostic laboratories and healthcare infrastructure in emerging economies. Countries such as India, Brazil, Vietnam, and Indonesia are investing heavily in diagnostic capacity under national health programs. India’s Ayushman Bharat initiative and China’s healthcare modernization programs are expanding laboratory testing networks across tier-2 and tier-3 cities.

The global diagnostic laboratory market is projected to expand rapidly, directly driving demand for consumables like serum separating tubes, plasma separation tubes, and EDTA tubes. Automation in pre-analytical workflows is increasing tube standardization requirements, further strengthening demand. This opportunity is estimated to represent multi-billion-dollar incremental demand potential by 2033, particularly in Asia Pacific. Manufacturers are increasingly investing in localized production facilities and distribution networks to capture cost-efficient growth.

Category-wise Analysis

Product Insights

Serum Separating Tubes (SSTs) are projected to account for approximately 35% of the blood collection tubes market in 2026, making them the leading product segment. Their dominance is driven by extensive use in clinical chemistry testing, one of the largest categories of laboratory diagnostics worldwide. According to the WHO, non-communicable diseases account for nearly 74% of global deaths, sustaining demand for routine monitoring of diabetes, kidney, liver, and cardiovascular conditions. SSTs remain the preferred choice due to their ability to improve serum yield, reduce processing time, and enhance laboratory efficiency.

EDTA tubes are expected to be the fastest-growing product segment, registering a CAGR of 8.1% from 2026 to 2033. Growth is supported by rising hematology testing volumes, with the WHO estimating that 1.9 billion people globally suffer from anemia. Increasing screening for leukemia, infectious diseases, and blood disorders, along with national programs targeting HIV, malaria, and dengue, continues to expand demand. Their compatibility with automated hematology analyzers further accelerates adoption across diagnostic laboratories.

Material Insights

Plastic tubes are anticipated to hold nearly 78% of the market share in 2026, establishing them as the dominant material segment. Their leadership is supported by growing adoption of safer specimen collection systems and regulatory initiatives from organizations such as OSHA and the European Union aimed at reducing laboratory injuries. Plastic tubes offer superior durability, lower transportation costs, and compatibility with automated laboratory workflows, making them the preferred option for high-volume diagnostic facilities.

Glass tubes are expected to witness modest growth through 2033, supported by specialized laboratory applications requiring high chemical stability and minimal sample interaction. Certain research institutions and reference laboratories continue to rely on glass tubes for specific analytical procedures where material purity is critical. However, increasing emphasis on laboratory safety and broader adoption of automation-compatible plastic alternatives continue to limit their overall market expansion.

End-user Insights

Diagnostic centers are projected to capture approximately 46% of market revenue in 2026, making them the largest end-user segment. Their dominance reflects the continued expansion of global diagnostic testing, with the CDC reporting that laboratory tests influence nearly 70% of medical decisions. Rising preventive health screening, growing chronic disease monitoring, and the expansion of organized diagnostic chains have significantly increased blood sample collection volumes worldwide.

Research & development centers are forecast to be the fastest-growing end-user segment, registering a CAGR of 8.5% through 2033. Growth is fueled by increasing investments in biotechnology and life sciences, with the biopharmaceutical industry investing more than US$100 billion annually in R&D, according to PhRMA. Expanding clinical trials, genomics research, precision medicine programs, and biomarker discovery initiatives are driving demand for high-quality blood collection tubes across research and biopharmaceutical facilities.

Regional Insights

North America Blood Collection Tubes Market Trends

North America is expected to account for approximately 38% of the global blood collection tubes market in 2026, supported by one of the world's most advanced diagnostic ecosystems. According to the U.S. Centers for Disease Control and Prevention (CDC), laboratory testing influences nearly 70% of medical decisions, while the region records billions of blood-based diagnostic procedures annually. High prevalence of chronic diseases, including cardiovascular disorders and diabetes, coupled with widespread adoption of automated laboratory systems, continues to drive demand for blood collection consumables.

U.S. Blood Collection Tubes Market Trends

The U.S. is projected to hold nearly 82% of the North American market in 2026. The CDC estimates that more than 38 million Americans live with diabetes, while the American Heart Association reports that nearly 48% of U.S. adults have some form of cardiovascular disease, creating sustained demand for routine blood testing. In addition, ongoing investments in precision medicine, clinical laboratories, and outpatient diagnostic services continue to strengthen consumption of advanced blood collection tubes across the country.

Canada Blood Collection Tubes Market Trends

Canada is estimated to account for approximately 18% of the regional market in 2026. According to the Canadian Institute for Health Information (CIHI), healthcare expenditure exceeded CAD 372 billion in 2024, with diagnostic services representing a growing component of healthcare delivery. Expansion of community-based laboratory services, increasing chronic disease screening programs, and investments in laboratory modernization are contributing to rising demand for blood collection products throughout the country.

Europe Blood Collection Tubes Market Trends

Europe is anticipated to represent approximately 27% of the global blood collection tubes market in 2026. The region benefits from universal healthcare systems, aging demographics, and strong preventive healthcare programs. According to Eurostat, individuals aged 65 years and older account for more than 21% of the EU population, increasing the frequency of diagnostic monitoring and blood testing. Implementation of the EU In Vitro Diagnostic Regulation (IVDR) is also encouraging adoption of standardized and high-quality blood collection systems across healthcare facilities.

Germany Blood Collection Tubes Market Trends

Germany is expected to command around 34% of the European market in 2026, making it the regional leader. Germany has the largest healthcare expenditure in Europe, exceeding €500 billion annually, and maintains one of the region's highest levels of laboratory automation. The country's growing burden of chronic diseases and strong emphasis on preventive diagnostics continue to support demand for blood collection consumables. Germany also serves as a major manufacturing base for laboratory and diagnostic equipment within Europe.

U.K. Blood Collection Tubes Market Trends

The U.K. is projected to account for approximately 17% of the European market in 2026. NHS England continues to expand community diagnostic centers (CDCs), which surpassed 170 operational facilities by 2025, significantly increasing access to blood testing services. Rising demand for cancer screening, cardiovascular monitoring, and preventive health assessments is contributing to higher specimen collection volumes, strengthening long-term demand for blood collection tubes across the country.

Asia Pacific Blood Collection Tubes Market Trends

Asia Pacific is projected to account for approximately 24% of the global blood collection tubes market in 2026 and is expected to register the fastest growth through 2033. The region's growth is supported by increasing healthcare expenditure, expanding diagnostic infrastructure, and a rapidly aging population. According to the United Nations, Asia Pacific is home to more than 60% of the global population, creating substantial demand for healthcare services and laboratory testing. Government-led healthcare expansion programs are further accelerating access to diagnostics across emerging economies.

China Blood Collection Tubes Market Trends

China is estimated to hold nearly 38% of the Asia Pacific market in 2026. The country continues to expand healthcare capacity under its Healthy China initiatives, while healthcare expenditure has surpassed CNY 9 trillion (US$1.25 trillion) annually. Rising prevalence of diabetes, cancer, and cardiovascular diseases is increasing laboratory testing volumes nationwide. China also remains one of the world's largest medical consumables manufacturing hubs, strengthening both domestic supply and export capabilities for blood collection products.

India Blood Collection Tubes Market Trends

India is expected to account for approximately 19% of the regional market in 2026 and is among the fastest-growing country markets. Government initiatives such as Ayushman Bharat, which aim to provide healthcare coverage to more than 500 million people, are expanding access to diagnostic services across the country. The rapid growth of organized diagnostic chains, increasing prevalence of lifestyle-related diseases, and rising healthcare expenditure are driving substantial increases in blood sample collection and laboratory testing volumes, supporting strong market growth.

Competitive Landscape

The global blood collection tubes market is moderately consolidated, with leading players such as Becton Dickinson, Greiner Bio-One, Sarstedt, and Terumo Corporation accounting for a substantial share of global revenue. These companies leverage strong distribution networks, established relationships with healthcare providers, and continuous investments in automation-compatible blood collection systems, specimen preservation technologies, and manufacturing expansion to maintain their market positions.

Regional manufacturers, particularly in Asia Pacific, are gaining traction through cost-effective production and localized supply capabilities. However, stringent regulatory requirements, quality standards, and large-scale manufacturing investments remain key barriers to entry. Going forward, the market is expected to witness gradual consolidation through acquisitions, capacity expansions, and strategic partnerships aimed at strengthening geographic presence and product portfolios.

Key Industry Developments:

- In July 2025, Becton Dickinson and Waters Corporation announced a US$17.5 billion transaction combining BD's Biosciences & Diagnostic Solutions business with Waters. The transaction strengthens the broader diagnostics ecosystem that supports laboratory testing growth.

- In October 2025, Terumo Corporation completed the US$1.5 billion acquisition of OrganOx. The acquisition strengthens Terumo's blood and transplant technology portfolio while supporting innovation in blood management and diagnostic workflows.

Companies Covered in Blood Collection Tubes Market

- Becton Dickinson

- Greiner Bio-One

- Sarstedt

- Terumo Corporation

- Nipro Corporation

- FL Medical S.r.l.

- Improve Medical Instruments Co. Ltd.

- TUD

- Hindustan Syringes & Medical Devices

- Abdos Labtech

- Sekisui Chemical Co. Ltd.

- Narang Medical Ltd.

- Cardinal Health

- Medline Industries

- Labtech Disposables

Frequently Asked Questions

The global blood collection tubes market is projected to reach US$5.8 billion in 2026.

Rising diagnostic testing volumes, increasing chronic disease prevalence, and expanding laboratory infrastructure drive market growth.

The market is expected to grow at a CAGR of 7.2% from 2026 to 2033.

Emerging healthcare markets, laboratory automation, and expanding preventive screening programs create significant growth opportunities.

Major market participants include Becton Dickinson, Greiner Bio-One, Sarstedt, and Terumo Corporation.