- Non-food Packaging

- Blister Packaging Market

Blister Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Blister Packaging Market by Material (Plastic Films, Aluminum, Paper & Paperboard), by Technology (Thermoforming, Cold Forming), Product Type (Clamshell Blisters, Carded Blisters, Full-face Seal Blisters, Others), End-user (Pharmaceuticals, Consumer Goods, Food, Electronics, Others), and Regional Analysis, 2026 - 2033

Blister Packaging Market Size and Trend Analysis

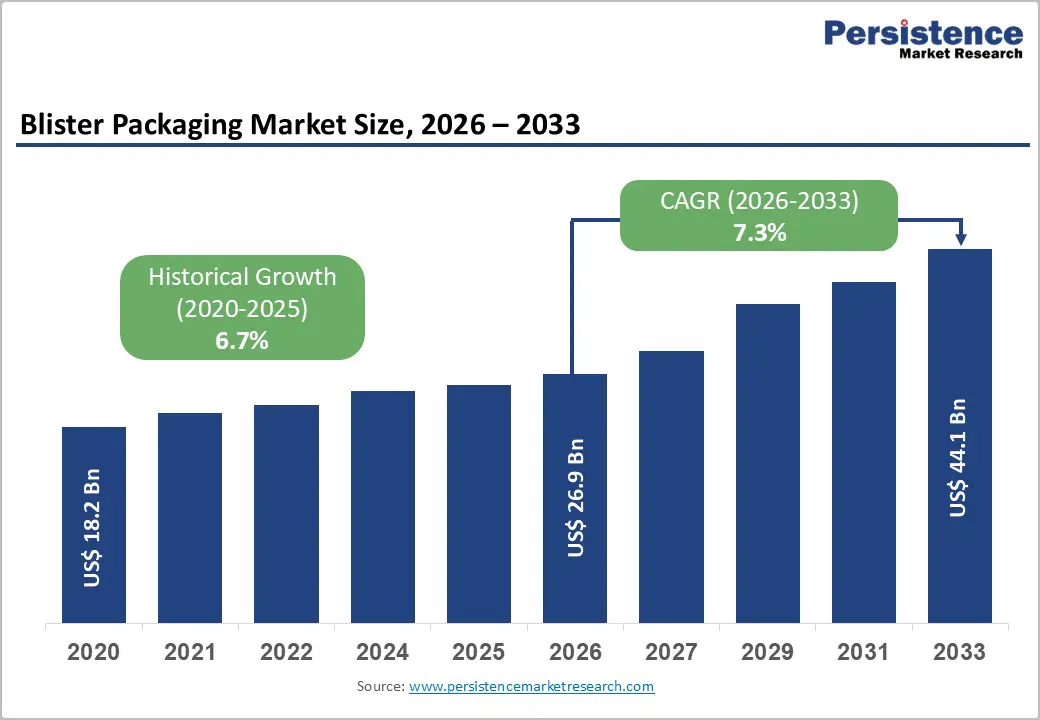

The global blister packaging market is projected to grow from US$ 26.9 billion in 2026 to US$ 44.1 billion by 2033, advancing at a CAGR of 7.3% during the forecast period. Blister packaging has emerged as a preferred format for pharmaceuticals, consumer goods, food, and electronics, owing to its superior product protection, tamper evidence, and unit-dose convenience.

Expanding pharmaceutical production, rising demand for child-resistant and barrier-protective packaging, and growing consumer preference for visually appealing retail-ready formats are key growth catalysts. Additionally, regulatory mandates promoting traceability, serialization, and patient compliance continue to reinforce blister packaging adoption across both developed and emerging economies worldwide.

Key Industry Highlights:

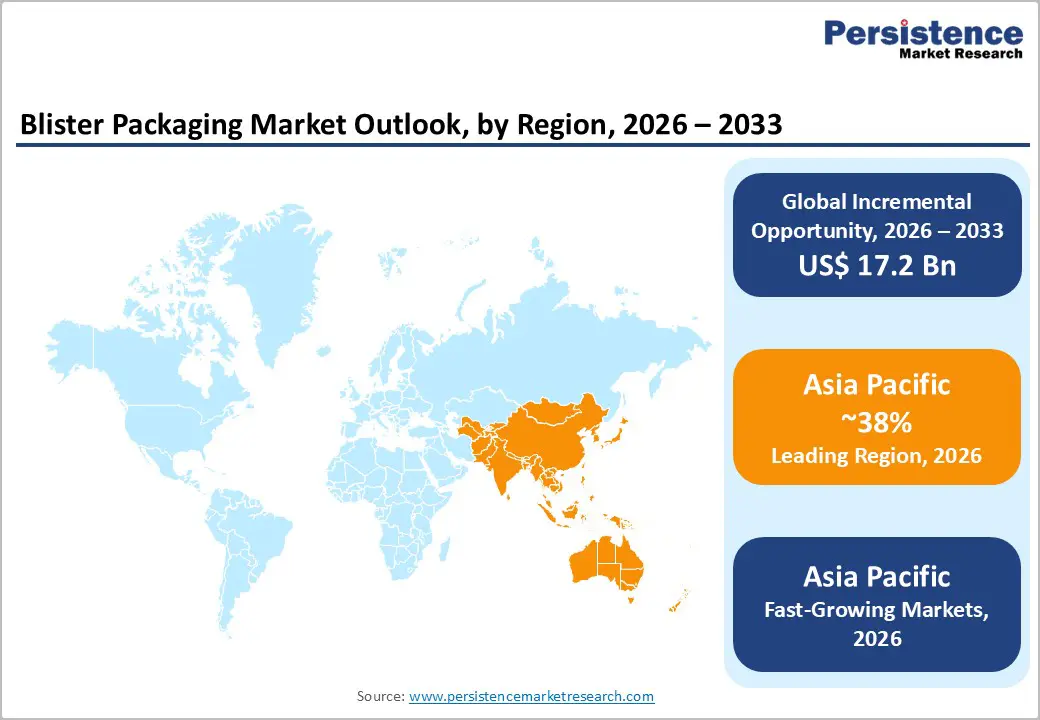

- Leading Region: Asia Pacific dominates with a 38% share in 2026, anchored by China and India's pharmaceutical output.

- Fast-Growing Market: Asia Pacific also leads the growth, propelled by generics scale-up and rising FMCG penetration.

- Dominant Segment: Pharmaceuticals lead end-use with around 60% share in 2026, driven by FDA and EMA tamper-evident mandates.

- Fastest Growing Segment: Paper & paperboard leads material growth, fueled by EU PPWR sustainability mandates.

- Key Opportunity: Smart serialized blisters with QR, RFID, and NFC address the WHO-estimated US$ 30 billion counterfeit drug problem.

Market Dynamics

Drivers - Expanding Pharmaceutical Production Fueling Demand for Unit-dose Blister Formats

Growing global pharmaceutical production is one of the most consequential demand engines for blister formats. European pharmaceutical production reached EUR 340 billion in 2023, with exports increasing year-on-year, while India produces over 60% of the world's vaccines and supplies nearly 20% of global generics, the bulk of which are dispensed in blister packs across both domestic and international supply chains.

Regulators including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) continue to favor unit-dose packaging for tamper evidence, patient compliance, and accurate traceability. The structural shift toward solid-dose generics, biosimilars, and chronic-disease therapies, combined with mandatory serialization frameworks, is reinforcing blister pack adoption across developed and emerging pharmaceutical manufacturing hubs worldwide.

Rising Safety Standards Drive Tamper-evident Child-resistant Blister Adoption

Heightened consumer awareness around product safety and the proliferation of over-the-counter (OTC) drugs are pushing brand owners toward tamper-evident and child-resistant blister designs. The U.S. Consumer Product Safety Commission (CPSC) enforces the Poison Prevention Packaging Act of 1970, which mandates child-resistant packaging for prescription drugs and several household substances, with non-compliance penalties intensifying year over year.

More than 85% of solid-dose pharmaceuticals in North America are dispensed in blister or strip packs, reflecting the format's compliance-friendly design. This regulatory and behavioral pull is also influencing the nutraceutical packaging market, where the same child-resistance and tamper-evidence benefits are accelerating the shift from bottles to blisters, further widening the addressable consumer-health opportunity.

Restraints - Plastic Waste Regulations Pressuring Conventional Blister Material Choices

Mounting regulatory and consumer scrutiny on single-use plastics presents a structural headwind for blister packaging. The European Commission's Packaging and Packaging Waste Regulation (PPWR), adopted in 2024, targets a 15% reduction in packaging waste per capita by 2040 versus 2018 levels and mandates that all packaging placed on the EU market be recyclable by 2030, raising compliance pressure across pharmaceutical and consumer-goods value chains.

Multi-layer PVC and PVdC blister structures are notoriously difficult to recycle due to chlorinated content and laminate complexity, prompting brand owners across the European Union to reassess material choices. This regulatory friction can slow short-term blister adoption among sustainability-led consumer goods players and force converters to invest heavily in mono-material redesign, delaying ROI on existing thermoforming assets.

Raw Material Price Volatility Squeezing Converter Profit Margins

Polymer and aluminum price swings continue to pressure converters' operating margins across the blister packaging value chain. According to the U.S. Energy Information Administration (EIA), crude-oil-linked feedstock prices have fluctuated by more than 25% in 2024, directly impacting input costs for PVC, PET, and PP films, which together account for the majority of thermoformed blister production worldwide.

Aluminum prices tracked by the London Metal Exchange (LME) remained above US$ 2,400 per tonne through 2024, raising cold-form foil costs and disrupting procurement budgets. These input swings make long-term contract pricing difficult and erode profitability for small and mid-size packaging converters, slowing capacity expansion in price-sensitive end-use industries such as food, electronics, and household consumer goods.

Opportunities - Recyclable Mono-material and Paper-based Blisters Unlocking New Growth

Material innovation is the most promising avenue for differentiation in the blister packaging market. Amcor plc launched its AmSky recyclable polyethylene blister system, while Constantia Flexibles introduced EcoLam mono-material laminates aligned with the CEFLEX recyclability guidelines. Paper-based blisters from Huhtamaki and Pulpex are also gaining traction with leading consumer-goods and pharmaceutical brands evaluating fiber-first packaging architectures.

With Ellen MacArthur Foundation Plastics Pact signatories committing to 100% reusable, recyclable, or compostable packaging by 2025, paper and paperboard blisters represent the fastest-growing material segment and an attractive incremental opportunity. This trend also strengthens the broader sustainable packaging market, opening cross-sell potential for converters offering integrated mono-material, fiber-based, and recycle-ready blister solutions to global brands.

Smart Serialized Blisters Powering Anti-counterfeit and Patient Adherence

Integration of QR codes, RFID tags, and NFC chips into blister packs is unlocking a new value layer for the industry. The World Health Organization (WHO) estimates that 1 in 10 medical products in low- and middle-income countries are substandard or falsified, costing global economies more than US$ 30 billion annually, creating a powerful regulatory and commercial incentive for connected packaging investments worldwide.

The U.S. Drug Supply Chain Security Act (DSCSA), fully enforced from November 2024, requires unit-level traceability across the pharmaceutical supply chain. Companies including Schreiner MediPharm and Körber are commercializing connected blister solutions that combine serialization with patient-adherence tracking, opening a high-margin growth pocket across pharmaceutical, clinical-trial, and specialty drug packaging applications globally.

Category-wise Analysis

Material Insights

Plastic films dominate the global blister packaging market with approximately 45% share in 2026, driven by their cost-effectiveness, formability, and superior barrier performance. PVC remains the workhorse polymer due to its excellent thermoformability, while PVdC and Aclar coatings deliver moisture and oxygen barriers required for sensitive pharmaceutical products. U.S. Pharmacopeia (USP) recognized standards for PVC and PVdC continue to anchor pharmaceutical demand, while plastic films enable high-speed automated thermoforming exceeding 600 blisters per minute, reinforcing cost competitiveness.

Paper and paperboard are the fastest-growing material segments, propelled by European Union PPWR recyclability mandates and global brand commitments to fiber-based packaging. Pharmaceutical and consumer-goods companies are piloting molded-fiber and paper-backed blisters to replace conventional plastic structures, supported by curbside recyclability and a lower carbon footprint. Investments by leading converters in barrier-coated paperboard and home-compostable substrates are unlocking new applications across OTC drugs, nutraceuticals, and personal care.

Technology Insights

Thermoforming leads the technology segment with approximately 70% market share in 2026, supported by lower capital expenditure, higher throughput, and broader compatibility with polymer films such as PVC, PET, and PP. Leading equipment suppliers, including Uhlmann Pac-Systeme, IMA Group, and Romaco Noack offer machines that deliver 400-700 cycles per minute, making thermoforming the technology of choice for high-volume pharmaceutical, FMCG, and electronics blister production globally.

Cold forming is the fastest-growing technology segment, fueled by surging demand for high-barrier packaging of moisture- and oxygen-sensitive APIs, biologics, and hygroscopic generics. Aluminum-aluminum (Alu-Alu) cold-form blisters offer near-zero permeability, ensuring extended shelf life for chronic-disease therapies and tropical-climate distribution. Expanding pharmaceutical manufacturing capacity in India and Southeast Asia, combined with rising biosimilar approvals, is accelerating cold-form adoption across specialty and contract manufacturing operations.

Product Type Insights

Carded blisters lead the product type segment with around 42% share in 2026, owing to widespread use in OTC pharmaceuticals, healthcare consumables, hardware, batteries, and stationery products. Their structural advantage lies in cost-efficient retail display, hang-tab compatibility, and ease of branding via printed paperboard backings. Major retailers, including Walmart and CVS Health, prefer carded blisters for shelf merchandising, reducing shoplifting and improving product visibility across point-of-sale environments.

Clamshell blisters are the fastest-growing product-type segment, supported by rising e-commerce shipments, premium electronics packaging, and demand for tamper-evident retail formats. Their two-piece sealed design protects high-value goods during last-mile delivery and enables 360-degree product visibility, which strengthens shelf appeal. Adoption is expanding across cosmetics, power tools, accessories, and gourmet food categories, with brands favoring recyclable PET and bio-based clamshell variants aligned to global sustainability commitments.

End-user Insights

Pharmaceuticals dominate the end-use segment, accounting for approximately 60% of the global blister packaging market in 2025. Leadership is driven by stringent regulatory mandates from the U.S. FDA, EMA, and Central Drugs Standard Control Organization (CDSCO) of India regarding tamper-evident, child-resistant, and unit-dose packaging. The World Health Organization (WHO) reports global medicine consumption volume growing at over 3% annually, with solid oral dose forms representing the majority of dispensed therapies.

Consumer goods is the fastest-growing end-use segment, propelled by booming demand for cosmetics, personal-care accessories, batteries, and small electronics in emerging markets. Brand owners increasingly favor blister formats for premium shelf presentation, anti-pilferage protection, and supply-chain efficiency in modern retail channels. Rising disposable incomes across Asia Pacific and Latin America, along with rapid e-commerce penetration, are reinforcing blister adoption across nutraceutical, household, and DIY consumer product categories.

Regional Insights

North America Blister Packaging Market Trends and Insights

North America holds nearly 26% share of the global blister packaging market in 2026, supported by mature pharmaceutical and healthcare ecosystems, a strong OTC retail channel, and stringent FDA tamper-evident regulations. Sustainability-driven reformulation, paper-based blister adoption, and unit-level serialization mandates under the U.S. Drug Supply Chain Security Act (DSCSA) are the leading trends shaping the regional landscape in 2025.

- U.S. Blister Packaging Market Size

The U.S. accounts for over 85% of North American blister packaging demand in 2026, driven by a USD-trillion-scale pharmaceutical sector tracked by the U.S. Bureau of Economic Analysis, robust OTC category expansion supported by the Consumer Healthcare Products Association, and rising adoption of recyclable mono-material blister designs by leading retailers and pharmacy chains responding to consumer sustainability expectations and serialization compliance requirements.

Europe Blister Packaging Market Trends and Insights

Europe holds around 24% share of the global blister packaging market in 2026, anchored by Germany, France, Italy, and the U.K. Regional growth is shaped by the EU Packaging and Packaging Waste Regulation (PPWR), EMA serialization rules under the Falsified Medicines Directive, and a strong industry push toward mono-material recyclable structures, with pharmaceutical contract manufacturing and premium consumer goods further sustaining demand.

- Germany Blister Packaging Market Size

Germany leads the European blister packaging market with an estimated 25% regional share in 2026. As reported by the German Federal Statistical Office (Destatis), the pharmaceutical sector generated record exports in 2024, fueling demand for high-barrier cold-form aluminum blisters and recyclable paper-based formats. Strong contract manufacturing presence and stringent national pharmacovigilance standards further reinforce Germany's leadership across high-value therapeutic packaging.

- U.K. Blister Packaging Market Size

The U.K. represents nearly 14% of the European blister packaging market in 2026. According to the Association of The British Pharmaceutical Industry (ABPI), U.K. pharma R&D investment exceeded GBP 8.9 billion in 2023, fueling demand for serialized, child-resistant blister formats across NHS supply contracts. Rising OTC consumption, growing generics dispensing, and sustainability commitments by leading retailers further strengthen the country's regional position.

- France Blister Packaging Market Size

France contributes around 12% of the European blister packaging market in 2026. The Leem (Les Entreprises du Médicament) reports France as Europe's third-largest pharmaceutical producer, with strong generics output and a national strategy to repatriate API production, fueling sustained demand for blister packaging. Growing investment in domestic manufacturing capacity and rising chronic-disease prevalence further reinforce blister format adoption across hospital and retail channels.

Asia Pacific Blister Packaging Market Trends and Insights

Asia Pacific is the leading and fastest-growing region, commanding a 38% share of the global blister packaging market in 2026. Rapid pharmaceutical capacity expansion in China and India, rising healthcare spending, and growing FMCG penetration are key drivers. China alone produces over 40% of global APIs, per the China Chamber of Commerce for Import & Export of Medicines & Health Products (CCCMHPIE), anchoring sustained regional demand.

- India Blister Packaging Market Size

India accounts for roughly 18% of the Asia Pacific blister packaging market in 2026. The Pharmaceuticals Export Promotion Council of India (Pharmexcil) reported pharmaceutical exports of US$ 27.9 billion in FY2024, with most solid-dose products packaged in cost-effective PVC and aluminum blisters. Government initiatives like Production Linked Incentive (PLI) schemes for pharma manufacturing further accelerate blister demand growth nationwide.

- Japan Blister Packaging Market Size

Japan holds approximately 16% of Asia Pacific blister packaging demand in 2026. The Japan Pharmaceutical Manufacturers Association (JPMA) indicates strong demand for press-through-package (PTP) blisters driven by an aging population, with adults aged 65+ representing nearly 29% of the population per the Statistics Bureau of Japan. Rising chronic-disease therapies and high-quality packaging standards further reinforce Japan's premium blister market position.

- Southeast Asia Blister Packaging Market Size

Southeast Asia contributes nearly 14% of the Asia Pacific blister packaging market in 2026. The ASEAN Pharmaceutical Industry outlook indicates strong double-digit growth in generics manufacturing across Vietnam, Indonesia, and Thailand, with government-led universal healthcare expansion and rising OTC consumption supporting blister packaging volumes. Expanding contract manufacturing investments and rapid retail pharmacy growth further reinforce regional demand trends.

Competitive Landscape

The global blister packaging market is moderately fragmented, with a mix of multinational packaging conglomerates, specialized pharmaceutical packaging converters, and regional film and foil suppliers competing across material, technology, and end-use verticals. Market leaders differentiate through recyclable mono-material innovation, vertically integrated film and foil production, serialization-ready formats, and proprietary high-barrier coatings tailored for pharmaceutical, FMCG, and electronics applications.

Strategic levers include mergers and acquisitions targeting regional converters, capacity expansion across Asia Pacific, R&D investment in paper-based and bio-derived blisters, and partnerships with pharma OEMs to co-develop child-resistant, smart, and anti-counterfeit blister formats aligned with PPWR and DSCSA mandates.

Key Market Developments

- In March 2025, Amcor plc completed its merger with Berry Global Group, creating a USD 24 billion global packaging leader with an expanded healthcare and consumer blister packaging portfolio across more than 140 countries.

- In September 2024, Constantia Flexibles launched its EcoPharm Blue PVC-free blister lidding foil, designed to meet upcoming EU PPWR recyclability targets and reduce pharmaceutical packaging carbon footprint by up to 30%.

- In June 2024, Huhtamaki introduced a fiber-based push-through blister for OTC pharmaceuticals in partnership with a leading European pharma brand, replacing conventional plastic backing with recyclable molded fiber.

Companies Covered in Blister Packaging Market

- Amcor

- Sonoco Products Company

- Constantia Flexibles

- WestRock

- Honeywell International

- Klockner Pentaplast

- DuPont

- Tekni-Plex

- Bemis Company

- UFlex

- Winpak

- Bilcare

- Display Pack

- Pharma Packaging Solutions

- Rohrer Corporation

Frequently Asked Questions

The global blister packaging market is valued at US$ 26.9 billion in 2026, projected to reach US$ 44.1 billion by 2033 at a 7.3% CAGR.

Rising pharmaceutical output and stringent U.S. FDA and EMA tamper-evident and child-resistant packaging mandates drive global blister adoption.

Asia Pacific leads with a 38% share in 2025, supported by large-scale pharmaceutical manufacturing in China and India.

Recyclable mono-material, paper-based blisters, and smart serialized packaging using QR, RFID, and NFC offer the most lucrative growth opportunities.

Key players include Amcor plc, Constantia Flexibles, Sonoco Products Company, Klöckner Pentaplast, Huhtamaki Oyj, and Berry Global Inc.