- Biotechnology

- Bioactive Peptides Market

Bioactive Peptides Market Size, Share, and Growth Forecast, 2026-2033

Bioactive Peptides Market by Source (Animal, Plant, Marine), Therapeutic Area (Anti-Hypertensive, Cardiovascular System, Nervous System, Gastrointestinal System, Immune System), Application (Foods & Beverages, Nutraceuticals & Dietary Supplements, Pharmaceuticals, Cosmetics & Personal Care, Others), and Regional Analysis for 2026-2033

Bioactive Peptides Market Share and Trends Analysis

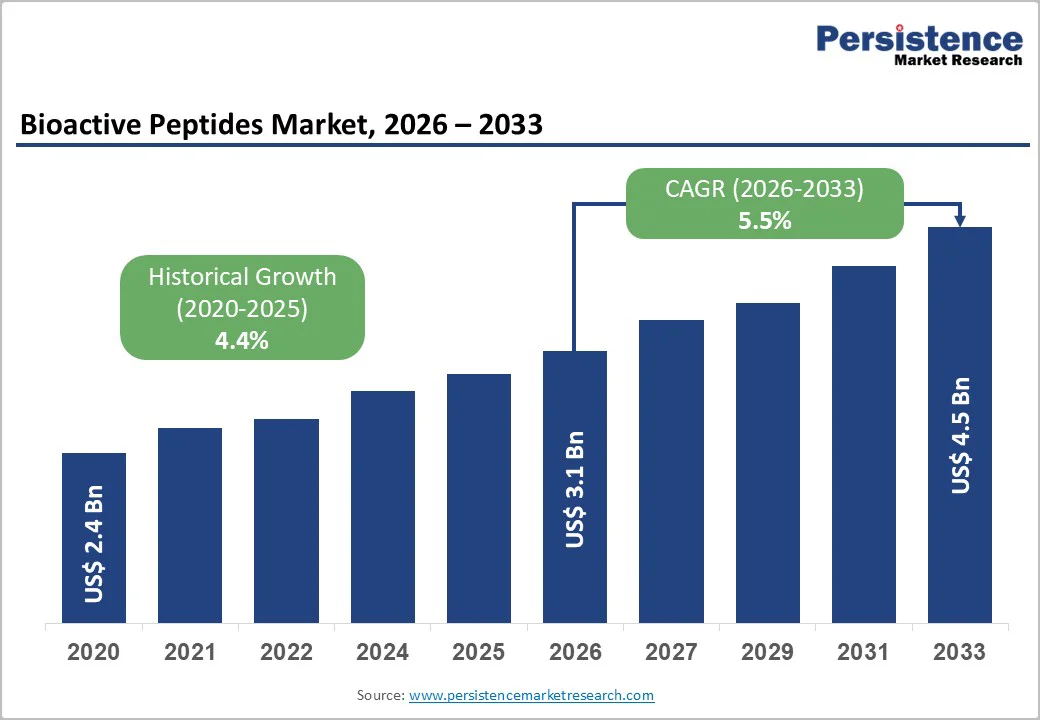

The global bioactive peptides market size is likely to be valued at US$ 3.1 billion in 2026, and is projected to reach US$ 4.5 billion by 2033, growing at a CAGR of 5.5% during the forecast period 2026 – 2033. Market expansion is primarily driven by the rising demand for functional foods, increasing prevalence of cardiovascular and metabolic disorders, and growing incorporation of bioactive peptides in nutraceuticals and pharmaceuticals. Advances in peptide extraction technologies, coupled with supportive regulatory recognition for health claims in major economies, are strengthening commercialization. Demographic aging, along with the growing adoption of preventive healthcare practices, is accelerating the uptake of peptide-based ingredients across food, dietary supplements, and clinical nutrition applications.

Key Industry Highlights

- Dominant Source: Animal-based peptides are estimated to account for 45% of the market share in 2026, supported by strong clinical validation and established supply chains.

- Fastest-growing Source: Plant-based peptides are projected to expand at a CAGR of 6.2% between 2026 and 2033, due to rising demand for clean-label, vegan, and sustainable ingredients.

- Leading Therapeutic Area: Cardiovascular peptides are expected to represent about 42% of the revenue share 2026, based on the high prevalence of cardiovascular disorders worldwide.

- Dominant Application: Pharmaceutical applications are anticipated to account for approximately 38% of market revenue in 2026, supported by increasing investment in peptide-based therapeutics and growing adoption in prescription formulations and clinical nutrition.

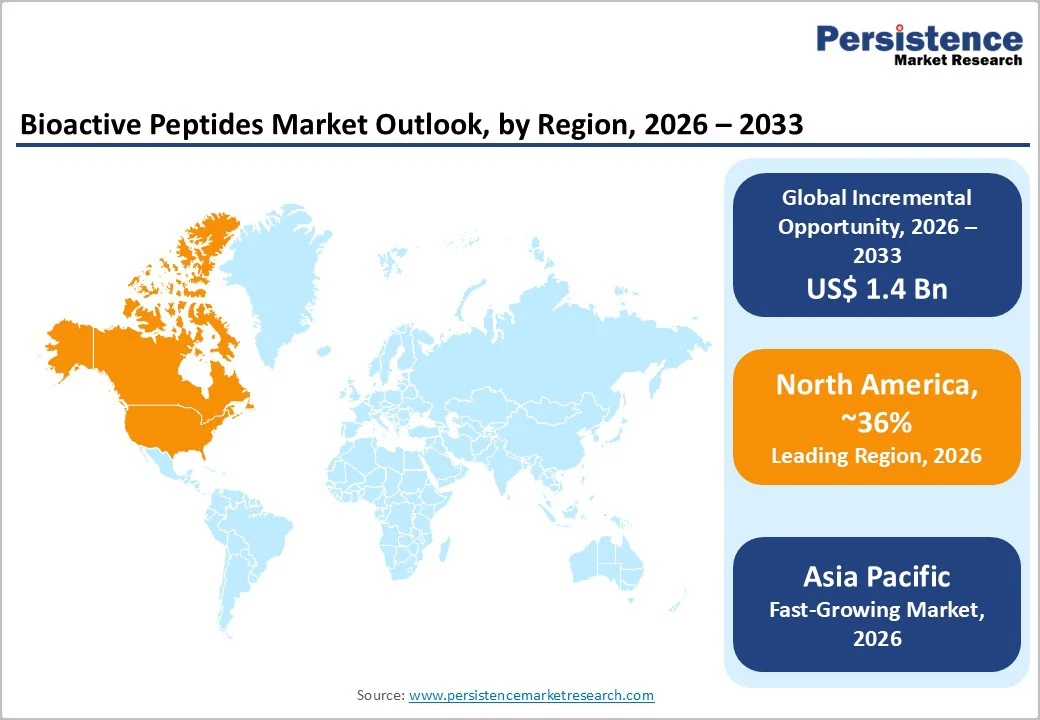

- Regional Dynamics: North America is expected to lead the market in 2026 with a 36% share, driven by high functional food consumption, while Asia Pacific is projected to record the fastest growth at around 6.5% CAGR through 2033, fueled by rapid urbanization.

- June 2025: Israeli startup Lembas introduced GLP-1 Edge, a food-grade bioactive peptide designed to naturally regulate appetite and metabolism.

| Key Insights | Details |

|---|---|

| Bioactive Peptides Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 4.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Health Awareness and Enhanced Peptide Technology

The bioactive peptides market growth is being strongly propelled by increasing health consciousness and the growing prevalence of chronic and lifestyle diseases. With cardiovascular disorders, hypertension, and metabolic syndromes affecting a significant portion of the population, consumers and healthcare providers are seeking preventive and functional nutrition solutions. Bioactive peptides, known for their ACE-inhibitory, antioxidant, and anti-inflammatory properties, are increasingly incorporated into functional foods, beverages, and dietary supplements, bridging the gap between nutrition and therapeutic benefits. Rising disposable incomes and shifting dietary patterns toward health-enhancing products further accelerate adoption across developed and emerging economies.

Technological advancements in peptide extraction and processing, including enzymatic hydrolysis and improved purification methods, have enhanced yield efficiency, peptide purity, and bioavailability. Companies are scaling up production capabilities, as exemplified by BioDuro’s fully automated solid-phase peptide synthesis facility in Shanghai, which reinforces global manufacturing and scalability for diverse peptide molecules. These innovations enable cost-effective, scalable production and facilitate broader application across food, nutraceutical, and pharmaceutical sectors. Improved manufacturing processes also support higher product consistency and faster commercialization, allowing companies to introduce peptide-based ingredients into new formulations and markets efficiently. As a result, the market is witnessing steady growth driven by both consumer demand for health-focused products and enhanced production capabilities.

Production and Regulatory Challenges

The market faces significant restraints due to high production costs and process complexity. Manufacturing involves enzyme sourcing, downstream purification, and rigorous quality validation, which can account for 30–40% of total ingredient costs. These expenses limit adoption among price-sensitive food and nutraceutical manufacturers, particularly in developing economies. The capital-intensive nature of peptide production makes large-scale penetration challenging, slowing the expansion of mass-market applications despite rising demand for functional and therapeutic products.

In addition to this, stringent regulatory requirements pose a considerable barrier to market growth. Agencies such as the U.S. Food and Drug Administration (FDA) and European Food Safety Authority (EFSA) require extensive clinical substantiation for health claims, resulting in lengthy approval timelines and potential compliance risks, including product recalls or withdrawal. Smaller manufacturers may find it difficult to meet these standards, discouraging investment in pharmaceutical-grade and therapeutic peptides.

Expanding Applicability of Peptides and Regional Growth Prospects

Significant growth opportunities in the market are emerging from the rising demand for bioactive ingredients in developing economies with shifting consumer preferences. Rapid urbanization, higher disposable incomes, and a growing middle class in Asia Pacific and Latin America are driving the adoption of functional foods and dietary supplements. Customizing peptides to regional dietary habits, particularly through plant-based and sustainable sources, enables companies to tap into a multi-billion-dollar market while meeting consumer demand for clean-label ingredients. For instance, scientists developed natural peptides from shrimp waste showing strong antioxidant and cellular activity, highlighting the potential of sustainable raw materials for functional applications.

At the same time, integrating bioactive peptides into medical nutrition and personalized healthcare is opening high-margin avenues. Aging populations and increasing focus on preventive healthcare are fueling demand for clinical nutrition products with targeted health benefits. Broader applications across food, cosmetics, and supplements enhance scalability, while plant-derived peptides minimize regulatory constraints, supporting faster commercialization and wider market reach. The combination of regional adoption, sustainable sourcing, and diversified applications positions the market for sustained long-term growth.

Category-wise Analysis

Source Insights

Animal-derived bioactive peptides are expected to dominate the market, accounting for an estimated 48% share in 2026. This leadership is supported by well-established supply chains for dairy and meat proteins and extensive clinical validation of milk-derived peptides such as casein and whey, which are widely incorporated into anti-hypertensive and cardiovascular formulations. Arla’s 2025 Nutrilac® HighYield initiative, which achieves zero acid whey waste while optimizing milk protein extraction, exemplifies ongoing innovation in animal-based peptide production. Proven efficacy in blood pressure regulation and vascular health ensures sustained demand across functional foods, nutraceuticals, and therapeutic applications, reinforcing the position of animal-based peptides as the primary revenue generator.

Plant-based peptides are slated to represent the fastest-growing source segment, projected to expand at a CAGR of 6.2% from 2026 to 2033. Growth is fueled by rising veganism, sustainability concerns, and the preference for clean-label ingredients. Innovations such as PEPDOO®’s Sirutide™ Oat Nutrient Burn Drink and Hemp Seed Fiber Bomb, launched at the 2025 Food & Beverage Innovation Forum in Shanghai, highlight the rapid commercialization of plant-derived peptides in functional beverages and nutrition products. Advances in the hydrolysis of soy, wheat, pea, and rice proteins enhance bioavailability and broaden applications, establishing plant-derived peptides as a key driver of future market expansion.

Therapeutic Area Insights

The cardiovascular system segment is likely to lead the therapeutic-area category in 2026, commanding approximately 40% of the bioactive peptides market revenue share. Its dominance is fueled by the high global prevalence of heart-related disorders and strong clinical evidence supporting the efficacy of peptides in blood pressure regulation. Anti-hypertensive peptides are the most commercially established class, widely incorporated into functional foods, nutraceuticals, and supplements. Initiatives such as CordenPharma’s € 500 million investment in a large-scale peptide manufacturing facility in Switzerland underscore the growing industrial focus on cardiovascular peptides, including GLP-1 analogs for diabetes and heart health. Consistent consumer awareness campaigns and preventive healthcare adoption further reinforce demand, making cardiovascular-focused peptides the primary therapeutic contributor to market revenues.

The immune system segment is projected to grow at the fastest rate, displaying an estimated CAGR of 6.5% from 2026 to 2033, driven by heightened consumer focus on immunity post-pandemic. Peptides with antimicrobial and immunomodulatory functions are increasingly used in dietary supplements, functional beverages, and clinical nutrition formulas. Research from the International Journal of Peptide Research and Therapeutics in 2025 showed that bovine thymic peptides modulate immune function, and Hericium erinaceus peptides enhance immune responses after digestion, validating their applications in immunity-focused products. Rising health awareness, preventive healthcare adoption, and the expanding elderly population are key factors accelerating growth.

Application Insights

Pharmaceutical applications are expected to dominate in 2026, accounting for approximately 38% of the segmental revenue share. This leadership is driven by rising R&D investment in peptide-based therapeutics, increasing clinical validation, and expanding use of bioactive peptides in cardiovascular, metabolic, and immune-related treatments. Prescription formulations and clinical nutrition products are gaining wider adoption across hospitals and specialty care settings. High product value, advanced drug-delivery technologies, and strong demand for targeted therapies reinforce pharmaceuticals as the primary revenue-generating application in the bioactive peptides market.

Nutraceuticals and dietary supplements are likely to constitute the fastest-growing application segment, projected to expand at a CAGR of approximately 6.8% through 2033. Strong consumer preference for preventive healthcare, recurring consumption patterns, and comparatively lower regulatory complexity support rapid adoption. Peptide-based supplements targeting heart health, immunity, digestion, and healthy aging are increasingly commercialized across global markets. Growing awareness of functional nutrition, clean-label products, and personalized wellness solutions continues to accelerate growth, positioning nutraceuticals and dietary supplements as a key driver of future market expansion.

Regional Insights

North America Bioactive Peptides Market Trends

North America is expected to be the leading regional market for bioactive peptides, accounting for approximately 36% of the market share in 2026, with the United States as the primary contributor. Strong regulatory clarity from the FDA, robust clinical research infrastructure, and high consumer adoption of functional foods and nutraceuticals support this leadership. Preventive healthcare initiatives and an aging population are driving demand for peptide-based dietary supplements and clinical nutrition products. Investment in peptide innovation, clinical validation, and pharmaceutical partnerships continues to strengthen market positioning and sustain revenue growth.

The regional market also benefits from well-established supply chains and high consumer awareness of health-enhancing products. Functional beverages, fortified foods, and prescription-based peptide formulations are widely commercialized. Recent launches such as Freemen Nutra Group and RAWGA Inc.’s VC?H1, a hibiscus-derived plant collagen peptide, highlight the growing adoption of sustainable, plant-based peptide ingredients in North America. Urbanized populations with higher disposable incomes further accelerate demand, while ongoing research and development efforts focus on improving peptide bioavailability and efficacy. These factors collectively reinforce North America’s dominance in the global bioactive peptides market, ensuring consistent growth and innovation-driven expansion.

Europe Bioactive Peptides Market Trends

Europe is expected to represent a mature, innovation-driven market from 2026 to 2033. Key countries include Germany, the U.K., France, and Spain, where harmonized regulatory frameworks ensure standardized approval of health claims while maintaining strict substantiation requirements. Established dairy industries and a strong functional food sector support sustained adoption of animal-derived and plant-based peptides. Rising interest in plant-based diets and clean-label ingredients is expanding market opportunities across nutraceuticals, dietary supplements, and functional foods.

Bioactive peptides market growth in Europe is supported by increasing healthcare awareness and preventive nutrition adoption among aging populations. Investment in clinical research and peptide-focused product development is driving innovation in formulations and therapeutic applications. Regional players are focusing on product differentiation through enhanced bioavailability, targeted health benefits, and novel delivery systems. Combined, these factors contribute to steady market expansion, making Europe a significant yet stable contributor to the bioactive peptides landscape.

Asia Pacific Bioactive Peptides Market Trends

Asia Pacific is projected to be the fastest-growing regional market, expanding at a CAGR of 6.5% from 2026 to 2033, driven by China, India, and ASEAN countries. Unprecedented scale and pace of urbanization, rising disposable incomes, and a growing middle-class population are accelerating demand for functional foods and dietary supplements. Bioactive peptides tailored to regional dietary habits, particularly plant-based formulations, are gaining popularity. Government-backed nutrition programs and initiatives to improve public health further support market adoption. Increasing awareness of preventive nutrition and chronic disease management is driving higher consumption of peptide-based products. Functional beverages, fortified foods, and clinical nutrition formulas are also increasingly commercialized across the region.

The market here also benefits from manufacturing cost advantages and expanding domestic production capacities. Investment in peptide R&D is rising to meet growing demand for functional and clinical applications. Urbanized populations with higher disposable incomes further accelerate adoption. Plant-based and culturally tailored peptide products are creating new market opportunities. Strengthened supply chains support efficient distribution across key Asia Pacific countries. Government programs and regulatory support enhance product availability and acceptance. With scalable production and strong innovation pipelines, Asia Pacific is positioned as a long-term growth engine for the bioactive peptides market.

Competitive Landscape

The global bioactive peptides market structure is moderately consolidated, with major players including Arla Foods Ingredients, Royal DSM-Firmenich, Kerry Group, FrieslandCampina Ingredients, and Fonterra holding a significant portion of the market share. These established companies leverage their strong R&D capabilities, regulatory expertise, and well-integrated supply chains for dairy, meat, and plant-based proteins. Continuous investment in clinical validation, peptide extraction technologies, and formulation innovation enables them to maintain leadership in functional foods, nutraceuticals, and pharmaceutical applications.

Regional and niche manufacturers are focusing on specialized peptide applications, including plant-based formulations and immune-supporting peptides, to capture local demand and emerging markets. Barriers such as regulatory compliance, production costs, and complex manufacturing processes limit new entrants. However, advances in scalable extraction technologies and partnerships with clinical nutrition and pharmaceutical companies are enabling smaller players to expand their footprint. Market consolidation is expected to increase gradually as leading companies acquire specialized peptide manufacturers and form strategic collaborations to strengthen product portfolios and geographic reach.

Key Industry Developments

- In August 2025, Evolved By Nature partnered with French skincare brand Doré to launch two products featuring silk peptide technology: Peptides Bouclier Intégral Barrier Boost Essence and Peptides Extreme Fermeté Collagen Firming Serum. The collaboration blends biotech peptide innovation with clean French skincare principles, with ongoing R&D for future product launches.

- In April 2025, Rousselot’s Peptan collagen peptides received Upcycled Certified® status from Where Food Comes From, validating that the peptides are produced from ingredients that would otherwise go to waste. This certification supports sustainability and circular economy initiatives within the bioactive peptides industry.

- In March 2025, Roche and Zealand Pharma entered a co-development and licensing agreement to advance peptide-based obesity and metabolic therapies, including Zealand’s amylin analog, petrelintide. The deal, valued up to US$ 5.3 billion, includes profit/loss sharing in the U.S. and Europe, with Roche handling global commercialization and manufacturing, signaling a major strategic move in therapeutic peptide innovation.

Companies Covered in Bioactive Peptides Market

- Arla Foods Ingredients Group P/S

- Royal DSM N.V.

- Glanbia plc

- BASF SE

- Fonterra Co‑operative Group Limited

- Kerry Group plc

- Cargill, Inc.

- Ingredion Incorporated

- Archer Daniels Midland Company (ADM)

- Peptan

- Hilmar Ingredients

- Arlak Biotech Pvt. Ltd.

Frequently Asked Questions

The global bioactive peptides market is projected to reach approximately US$ 3.1 billion in 2026.

Increasing prevalence of chronic and lifestyle diseases, rising adoption of functional foods and nutraceuticals, and technological advancements in peptide extraction and hydrolysis are key growth drivers.

The market is expected to grow at a CAGR of 5.5% from 2026 to 2033.

Expansion into emerging markets in Asia Pacific and Latin America, rising demand for plant-based and clean-label ingredients, and integration into medical nutrition and personalized healthcare represent major opportunities.

Arla Foods Ingredients, Royal DSM-Firmenich, Kerry Group, Glanbia plc, and BASF SE are some of the leading players in the market.