Industry: Chemicals and Materials

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 192

Report ID: PMRREP35028

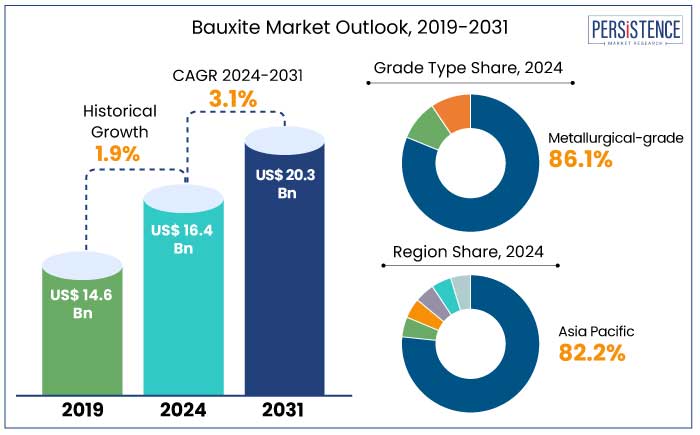

The global bauxite market is projected to reach a size of US$ 16.4 Bn by 2024. It is anticipated to witness a CAGR of 3.1% during the forecast period to attain a value of US$ 20.3 Bn by 2031.

The Electric Vehicle (EV) industry is estimated to witness exponential growth with aluminum playing a key role in lightweight vehicle development and battery components. Based on a study, global EV sales are predicted to reach 40 million units annually by 2031. This growth is estimated to drive significant demand for aluminum as well as bauxite.

Use of aluminum in renewable energy projects like solar panels and wind turbines is anticipated to witness significant expansion. By 2031, aluminum demand for renewable energy projects is likely to rise by over 30%.

Mining companies are under constant pressure to adopt sustainable practices. Companies like Rio Tinto and Alcoa have already initiated green mining projects. For instance, Alcoa’s ‘Elysis’ project aims to produce carbon-free aluminum by 2030, indirectly reducing the environmental impact of bauxite mining

Key Highlights of the Industry

|

Market Attributes |

Key Insights |

|

Bauxite Market Size (2024E) |

US$ 16.4 Bn |

|

Projected Market Value (2031F) |

US$ 20.3 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

3.1% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

1.9% |

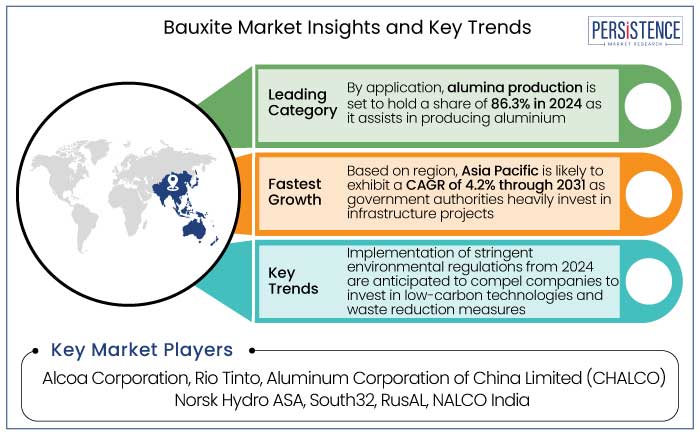

Robust Government Support Across Asia Pacific to Spur Demand

Asia Pacific is estimated to hold a robust share of 82.2% in 2024. China is one of the world's most significant producers and consumers of aluminum. The country accounted for 60% of global aluminum production in 2022. This dominance translates to massive demand for bauxite, as it is the primary raw material for producing aluminum. For example,

Asia Pacific is experiencing rapid industrial growth, particularly in emerging economies, which rely heavily on aluminum-based products. Governments in the region are investing heavily in infrastructure projects, further increasing demand for aluminum. For instance,

China has invested heavily in Guinea’s bauxite mining sector to secure long-term supply. For example,

North America's Bauxite Dependency and the Shift Towards Alternative Alumina Sources

North America is one of the major importers of bauxite globally. Very negligible amounts of bauxite are mined in the region with no bauxite mining in Canada and both the U.S. and Canada have to rely heavily on Brazil, China, Guinea, and the Netherlands. Over 95% of the bauxite imported into the region is used for the production of alumina, a critical mineral to produce aluminum. Canada is one of the largest producers of aluminum in the world and exports the majority of its aluminum production to the U.S.

A decline in bauxite demand has been observed within the U.S., as the country has very few alumina manufacturing facilities. At present, the U.S. has only one alumina refinery in operation thus putting an additional burden on a country that only produces 15% of its aluminum requirements.

In 2025, Brimstone announced a novel cement-making technique that creates raw smelter-grade alumina, a core raw material for aluminum smelters. The company replaces bauxite with carbon-free calcium silicate rocks, thereby minimizing imported bauxite dependency on the U.S. alumina industry.

Metallurgical-grade bauxite is estimated to hold a share of 86.1% in 2024. It contains 45% to 60% alumina and is primarily used to produce alumina through the Bayer process, which is then smelted into aluminum. Around 85% of the world’s bauxite is used to produce aluminum, making metallurgical-grade bauxite indispensable.

India and the Middle East are the emerging hubs for aluminum production due to increasing industrialization and government support.

Alumina production is estimated to account for a share of 86.3% in 2024. Around 90% of the world’s bauxite is processed into alumina using the Bayer process. Alumina is then smelted into aluminum through the Hall-Héroult process.

Aluminum’s crucial role in key industries undergoing expansion further fuels alumina production. For example,

Developments in the Bayer process, such as energy-efficient technologies and waste reduction systems, have lowered production costs and made alumina production sustainable.

Potential growth in the global bauxite industry is predicted to be driven by high emphasis on sustainability and recycling. The recycling of aluminum is estimated to play a key role in mitigating some of the pressures on the bauxite market. However, it is unlikely to fully replace primary bauxite production in the near future.

The bauxite industry is likely to continue to experience price fluctuations due to geopolitical events, supply chain disruptions, and changes in global demand for aluminum. Price volatility is anticipated to remain a key characteristic of the market in the forecast period.

The bauxite market growth was average at a CAGR of 1.9% during the historical period from 2019 to 2023. The market was characterized by stable growth driven by robust demand for aluminum which is a key industrial metal used in sectors like construction, automotive, packaging, and aerospace. For instance,

The COVID-19 pandemic severely disrupted global supply chains, including the bauxite market. Despite this, demand for aluminum remained relatively stable due to its use in critical sectors.

Bauxite production continued to rise globally in the post-pandemic period, with Guinea and Australia maintaining their positions as the leading producers. The global bauxite industry was heavily impacted by geopolitical events, particularly in Guinea, where political instability and military coups affected bauxite exports. This contributed to price volatility and supply shortages.

Emerging economies, especially in Asia Pacific and Africa, are likely to witness increased infrastructure development and industrialization, resulting in a high demand for aluminum and bauxite. Innovations in mining technologies, such as the development of green and energy-efficient mining methods, can assist in decreasing costs. These can also help in mitigating environmental challenges associated with bauxite extraction. It is further likely to assist in maintaining long-term supply stability.

Ongoing Infrastructure Development in Emerging Economies to Spur Sales

By 2030, around 60% of the world’s population is estimated to live in cities. Growth in urban population surges demand for housing, roads, bridges, and public transport systems. As urban transportation systems broaden, aluminum demand rises, particularly in Electric Vehicles (EVs) and public transport systems.

The booming construction industry in emerging markets, particularly in Asia Pacific, increases the demand for aluminum, as it is extensively used in building materials. The transition to renewable energy and the expansion of power grids are key drivers of aluminum demand. Demand for aluminum in infrastructure is especially strong in Asia Pacific, which is set to be the fastest-growing region for aluminum consumption due to rapid urbanization and infrastructure expansion.

Recycling and Secondary Production Activities to Skyrocket Demand

The most significant advantage of aluminum is its recyclability. It can be recycled indefinitely without losing its property. For example,

Recycling aluminum saves up to 95% of the energy required to produce new aluminum from bauxite, which has significant environmental benefits, such as reducing greenhouse gas emissions.

Fluctuating Bauxite Prices May Hamper Growth Avenues

As bauxite is a key raw material for aluminum, fluctuations in aluminum prices can directly affect demand for bauxite. Global aluminum demand has been on the rise, especially due to its increased usage in sectors such as transportation, construction, and packaging.

The supply of bauxite is concentrated in a few countries, and hence disruptions in production or supply chains from these regions can result in volatility in bauxite prices. For instance,

Sustainability and Green Mining Practices to Open the Door to Success

Bauxite mining often involves large-scale land clearing which results in the destruction of forests and natural habitats, contributing to the loss of biodiversity. In Indonesia, deforestation linked to bauxite mining has been a significant concern, as large areas of tropical forests are cleared to access bauxite reserves. The Bayer process is highly energy-intensive, and the production of primary aluminum generates high carbon emissions, contributing to climate change.

Bauxite mining uses large quantities of water, and the process can lead to water contamination. For example, bauxite residue or red mud, a byproduct of aluminum production, can leach harmful chemicals into water sources. According to the World Bank, land reclamation and biodiversity restoration have been key strategies for bauxite mining companies to meet sustainability standards.

Rising Use in Battery Electric Vehicles to Create Lucrative Prospects

Aluminum is widely used in Electric Vehicles (EVs) because of its light weight, which contributes to improving vehicle efficiency and range. Aluminum is used in various EV components, including battery casings, chassis, wheels, and body panels.

It assists in decreasing the weight of the vehicle, making it more energy efficient. Aluminum consumption in the automotive sector, including electric vehicles, is set to increase by more than 9% annually in the coming years, with much of the growth concentrated in electric mobility and light-weighting trends.

As EV adoption rises, so does the demand for charging stations, several of which incorporate aluminum components. The aluminum used in battery casings and chargers is likely to drive further demand in the next ten years. For instance,

Companies in the bauxite industry are aiming to integrate their operations by controlling the entire supply chain, thereby helping in cost reduction while ensuring a steady supply of raw materials. A few businesses are entering in strategic partnerships or long-term contracts with aluminum producers to secure stable demand for aluminum ore. They are focusing on adopting cutting-edge technologies and efficient mining methods to decrease extraction costs and enhance productivity.

The use of AI, big data, and IoT technologies in mining operations can assist in improving efficiency and decreasing downtime, resulting in cost reductions. By implementing sustainable mining practices, companies can decrease environmental remediation costs, as well as enhance their public image, attracting investors and customers who value sustainability.

Recent Industry Developments

|

Attributes |

Detail |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Grade Type

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market is anticipated to reach a value of US$ 20.3 Bn by 2031.

Australia is the world’s most prominent bauxite producer.

The aluminum ore is transported to refineries by conveyor, rail, or ship.

Prominent players in the market include Alcoa Corporation, Rio Tinto, and Aluminum Corporation of China Limited (CHALCO)

The market is predicted to witness a CAGR of 3.1% through 2031.