- Technology

- Barcode Scanner Market

Barcode Scanner Market Size, Share, and Growth Forecast 2026 – 2033

Barcode Scanner Market by Product Type (Portable/Handheld, Fixed Position), Technology (Pen Type Reader, Laser Scanner, CCD Readers), End-user (Retail and Commercial, General Manufacturing), and Regional Analysis, 2026 – 2033

Barcode Scanner Market Size and Trends Analysis

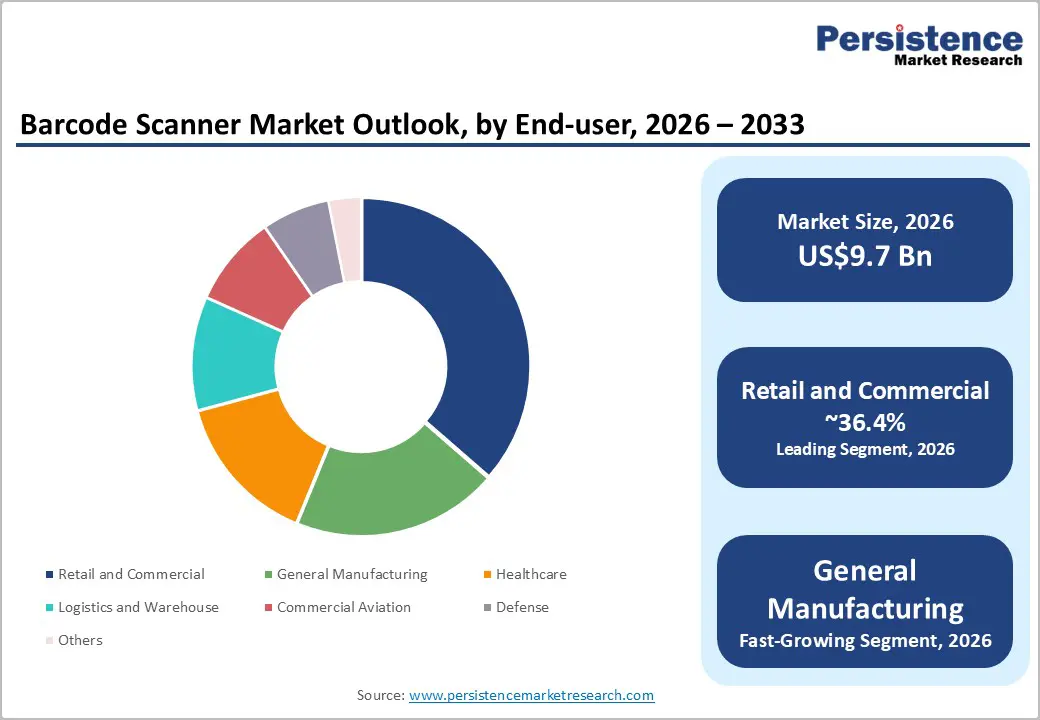

The global barcode scanner market size is likely to be valued at US$9.7 billion in 2026 and is expected to reach US$15.9 billion by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 to 2033, driven by the ongoing expansion of e-commerce and warehouse automation, which is increasing the requirement for fast and accurate inventory tracking.

Growth is further boosted by rising adoption of self-checkout systems and contactless retail technologies, as retailers focus on improving customer experience.

Key Industry Highlights:

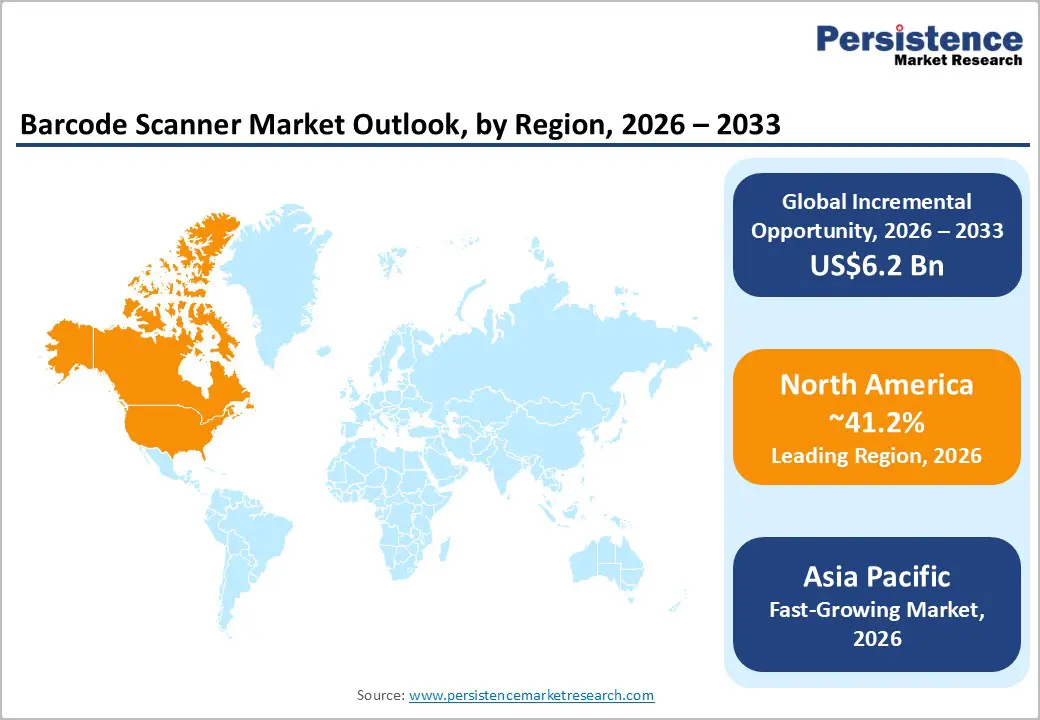

- Leading Region: North America, with about a 41.2% share in 2026, owing to early adoption of retail automation and high deployment of warehouse scanning systems.

- Fast-growing Region: Asia Pacific, backed by rising investments in logistics infrastructure and increasing adoption of automation by regional e-commerce players.

- New Product: In January 2025, Datalogic introduced its AI Loss Prevention Suite for the Magellan scanner platform. The solution integrates machine-learning capabilities into barcode scanning systems to help retailers reduce shrinkage, improve checkout accuracy, and enhance operational efficiency. The launch reflects the high convergence of barcode scanning and AI in retail environments.

- Leading Product Type: Portable/Handheld, approximately 73.2% share in 2026, as they help improve operational speed without requiring fixed infrastructure.

- Dominant End-user: Retail and commercial, nearly 36.4% in 2026, because barcode scanners are essential for billing, inventory control, and omnichannel order management across physical stores and online retail networks.

DRO Analysis

Driver - Online Retail to Fuel Smart Warehouse Scanning

The surge in e-commerce is pushing warehouses to upgrade their scanning infrastructure. Traditional handheld laser scanners struggle to keep pace with high-order volumes and tight delivery windows. Hence, fulfillment centers are moving toward wearable and AI-integrated scanning devices. At MODEX 2024, Zebra Technologies launched the RS2100 back-of-hand scanner and the WT6400 wearable computer, both engineered for hands-free picking, sorting, and inventory management in demanding environments, including freezer operations.

In January 2025, Zebra further extended its Symmetry Fulfillment solution, combining autonomous mobile robots, wearable technologies, and analytics to increase productivity and cut costs in warehouse operations. Wearable ring-type scanners are seeing a steady growth rate in e-commerce fulfillment, showcasing how warehouses are rethinking the entire pick-and-pack process around hands-free and connected scanning.

Retail Checkout Modernization and Self-Service Expansion

Retailers are actively replacing attended checkout lanes with smart self-checkout systems to cut labor costs and improve transaction speed. A 2024 survey found that 43% of shoppers prefer self-service, with that figure climbing to 60% among adults aged 18 to 44. This shift is pushing demand for presentation scanners and bi-optic imagers embedded in kiosks. Leading retailers such as Walmart, Kroger, and Target are deploying self-checkout, with scanner procurement often managed by kiosk manufacturers such as NCR and Diebold Nixdorf.

In February 2024, Carrefour rolled out upgraded self-checkout kiosks across Europe, enabling payments via digital wallets such as Apple Pay and Google Pay. Beyond grocery, self-checkout is now extending into mass merchandise, drugstores, and convenience stores, further widening the addressable market for embedded barcode scanning hardware.

Restraint - Direct Line-of-Sight Dependency to Limit Bulk Scanning Use Cases

Barcode scanners rely on optical visibility. Every item must be individually aimed at the scanner, which creates a key throughput bottleneck in high-volume logistics settings. In high-volume or high-velocity environments such as warehouses and manufacturing plants, this creates a bottleneck, as workers must physically locate the barcode, point the scanner, and verify the scan. Typical inventory accuracy using barcode systems hovers between 65% and 80%. Pallet-level bulk scanning is simply not feasible with standard barcode technology.

RFID scanners, by contrast, can read multiple codes at once without requiring a direct line of sight, making RFID systems much more efficient for high-volume scanning. This gap becomes more critical as logistics operations expand. RAIN RFID alone saw 52.8 billion tag chips shipped in 2024, powering fast and no-line-of-sight inventory tracking. While barcodes remain dominant due to low cost and universal infrastructure, their physical scanning constraint remains a structural disadvantage that RFID and hybrid systems are increasingly being adopted to work around.

Opportunity - AI-Assisted Decoding for Challenging Label Conditions

Traditional laser-based scanners fail on smudged, torn, or low-contrast labels, compelling workers to manually reprint or re-scan. AI-based camera scanners are solving this directly. In January 2025, Cognex launched the DataMan 290 and 390 barcode readers, using advanced AI technology to reliably decode damaged and low-quality codes across manufacturing and logistics applications. Cognex's DataMan image-based readers, powered by AI-assisted decoding algorithms, ensure up to 99.9% read rates even on smudged, torn, or reflective labels.

This reduces label reprint costs and manual intervention time. Machine learning also enables scanners to read damaged, poorly printed, or low-contrast barcodes in real time, ensuring operational continuity even in challenging warehouse and production floor conditions. As logistics throughput demands rise, AI decoding is shifting from a premium feature to a baseline requirement for fixed-mount and handheld scanner deployments.

Shift from 1D to 2D Codes to Create New Scanner Hardware Demand.

The move away from traditional UPC barcodes is creating a hardware refresh cycle across global retail. GS1 Sunrise 2027, led by GS1 US, requires retailers to install optical scanners capable of reading 2D barcodes and extracting the GTIN at point of sale. This is not a minor firmware update. Several existing POS scanners are incompatible. The core requirement is that by December 31, 2027, retail POS systems must be capable of reading and processing a GTIN contained in a QR code encoded with a GS1 Digital Link URI or a GS1 DataMatrix code.

The transition is already live across 48 countries, touching 88% of global GDP. For scanner manufacturers, this represents a procurement trigger. 2D barcodes allow for surgical product recalls by identifying the specific batch or lot affected, rather than pulling all stock. It is a traceability benefit pushing both brands and retailers to accelerate compliance. The 2027 deadline is, in effect, a mandated scanner upgrade cycle at global scale.

Category-wise Analysis

Product Type Insights

Portable/Handheld barcode scanners are predicted to lead with a share of approximately 73.2% in 2026, as they provide mobility that fixed systems cannot match. Workers can move freely across warehouses, retail aisles, hospitals, and distribution centers without bringing products to a scanning station. This is especially important in e-commerce fulfillment centers where employees scan products stored on high racks, pallets, and loading docks. Industry studies show that handheld scanners significantly improve picking and inventory management efficiency as they allow scanning directly at the point of activity.

Fixed-position barcode scanners are estimated to be the fastest-growing segment over the forecast period, owing to the ongoing expansion of industrial automation. Unlike handheld devices, these scanners operate continuously without human intervention. They are installed on conveyor belts, sorting systems, packaging lines, and production equipment where products move at high speed. This allows manufacturers and logistics companies to automate identification and tracking processes while reducing labor requirements.

End-user Insights

The retail and commercial segment is anticipated to dominate with a share of nearly 36.4% in 2026, as barcode scanners are integrated into nearly every stage of store operations. They are used for checkout, inventory tracking, shelf replenishment, pricing updates, returns processing, and loss prevention. Few retail technologies deliver such broad operational benefits at a relatively low cost, making barcode scanners a standard infrastructure investment for retailers worldwide.

The general manufacturing segment is expected to remain in the second position in 2026 as manufacturers are under increasing pressure to improve traceability and production visibility. Barcode scanners enable companies to track raw materials, components, work-in-progress items, and finished goods throughout the production cycle. This helps manufacturers identify bottlenecks, reduce errors, and improve quality control.

Regional Insights

North America Barcode Scanner Market Trends

North America is predicted to be the leading region in 2026 with a share of approximately 41.2%, backed by a well-established retail infrastructure, early adoption of advanced automation technologies, and the presence of leading barcode scanner manufacturers and solution providers. The healthcare sector is a particularly strong demand anchor. Regulatory mandates such as the Food and Drug Administration’s (FDA) Unique Device Identification (UDI) system are compelling healthcare providers and manufacturers to adopt barcode systems for better compliance and traceability. The region also benefits from a superior replacement cycle culture. Businesses routinely upgrade scanner fleets to keep pace with rising throughput demands, creating a consistent base of procurement even in mature deployments.

U.S. Barcode Scanner Market Trends

In 2026, the U.S. is predicted to account for a share of nearly 66.2%, owing to the convergence of regulatory mandates, healthcare digitization, and the world's most advanced e-commerce infrastructure. The U.S. market thrives on mature IoT infrastructure and SME adoption via cloud-subscription models. A key compliance driver is the Drug Supply Chain Security Act (DSCSA). The DSCSA requires every prescription drug package to carry a unique product identifier embedded in a 2D barcode, compelling manufacturers, distributors, and dispensers to upgrade their scanning infrastructure. With full enforcement now in effect as of November 27, 2024, all pharmaceutical trading partners must comply with improved serialization, interoperability, and verification mandates. This has triggered a wave of scanner procurement across pharmacies, hospitals, and distribution centers that had previously been running on outdated systems.

Asia Pacific Barcode Scanner Market Trends

Asia Pacific is anticipated to be the fastest-growing market in 2026 with a share of nearly 30.8%, fueled by ongoing expansion in e-commerce, warehousing, and manufacturing across the region. The region is not just a consumer, but it is also a production hub. The influx of regional manufacturers such as Shenzhen Sunlux Technology and international players strengthening their local presence enhances product availability and affordability. India is emerging as a standout within the region. The country is being propelled by swift e-commerce and retail expansion and the government's initiatives to promote Industry 4.0 and digitalization.

China Barcode Scanner Market Trends

China is anticipated to account for a share of around 33.7% in 2026, supported by its expansion in manufacturing, cross-border e-commerce, and government-driven automation policy. Its key market drivers also include its booming e-commerce sector, extensive logistics networks, and large-scale manufacturing sector. The government's industrial policy plays a key role. Government initiatives promoting digitalization and smart manufacturing, such as Made in China 2025, provide additional tailwinds, and the country is also a major production hub for scanner components and finished goods.

Japan Barcode Scanner Market Trends

In 2026, Japan will likely hold a share of approximately 27.4%, due to its focus on precision, efficiency, and innovation. The widespread adoption of barcode scanning devices in manufacturing, retail, and healthcare, where advanced technological integration is a priority, is also creating new avenues. The more powerful driver is the country’s labor crisis. According to Japan's Ministry of Health, Labor and Welfare, the number of foreign workers reached a record 2.57 million as of October 2025, pushed by a declining domestic population. This is augmenting warehouses and manufacturers to automate operations, with barcode scanning deeply integrated into automated workflows.

Europe Barcode Scanner Market Trends

Europe will likely see steady growth in the forecast period with a share of nearly 20.5% in 2026, boosted by compliance requirements and steady Industry 4.0 adoption rather than infrastructure build-outs. The continent prioritizes sustainable and regulation-compliant devices over constant expansion. Buyers are focused on scanners that meet data protection and compliance standards while prioritizing reliability over steady upgrades. Regulatory dynamics are a key demand trigger. In May 2025, the European Union passed a new Data Protection Regulation that includes provisions for the secure handling of barcode data, aimed at protecting consumer privacy while enabling businesses to utilize barcode technology more effectively.

Germany Barcode Scanner Market Trends

Germany is one of Europe's most strategic markets for industrial barcode scanners, given its dense manufacturing base and deep commitment to automation. It will likely account for a share of nearly 32.1% in 2026. The country is a significant market for 2D barcode readers, with widespread adoption in industrial automation, production lines, and warehouse management, reflecting its focus on efficiency and precision. The pharmaceutical sector is also adding momentum. Traceability mandates in the food, beverage, and pharmaceutical industries require 2D scanning capabilities at multiple points in the supply chain, creating a steady hardware replacement cycle. Germany's outlook is positive and consistent, backed by industrial upgrade cycles and compliance timelines rather than new market formation.

U.K. Barcode Scanner Market Trends

In 2026, the U.K. is estimated to account for a share of approximately 19.4%, boosted in large part by a government healthcare mandate and continued e-commerce expansion. In June 2023, the government mandated that all National Health Service (NHS) trusts in England adopt barcode scanning of high-risk medical devices by March 2024. It was a part of a broad push to digitally transform the NHS and improve patient safety. This is a significant procurement trigger. Every NHS trust now requires GS1-compliant scanning hardware and workflows in place.

Competitive Landscape

The global barcode scanner market is moderately consolidated with the presence of a handful of multinational companies controlling a significant share of revenues. Leading players such as Zebra Technologies, Honeywell, and Datalogic dominate enterprise deployments across retail, logistics, healthcare, and manufacturing due to their extensive product portfolios, global distribution networks, and integrated software ecosystems. Industry estimates suggest that the top five companies account for more than half of global market revenues, showcasing the superior influence of established vendors.

Competition is increasingly shifting beyond hardware specifications toward complete automation ecosystems. Vendors are differentiating themselves through warehouse management system integration, cloud-based device management, AI-enabled scanning capabilities, predictive maintenance tools, and analytics platforms that help customers improve workforce productivity. Companies delivering end-to-end solutions are gaining an advantage over those selling standalone scanners.

Key Industry Developments:

- In April 2026, Honeywell announced the sale of its Productivity Solutions and Services (PSS) business to Brady Corporation for US$1.4 billion. The PSS unit includes barcode scanners, mobile computers, and printing solutions used across logistics, warehousing, manufacturing, and retail environments.

- In January 2026, GE introduced a new refrigerator model with a built-in kitchen assistant function. The Profile Smart Refrigerator has a built-in barcode scanner, aiming to make restocking as simple as checking out at a supermarket.

- In October 2025, Zebra Technologies completed its acquisition of Elo Touch Solutions following a US$1.3 billion agreement announced in August 2025. Zebra stated that the acquisition would improve its connected frontline solutions portfolio by combining barcode scanning, mobile computing, kiosks, touchscreen displays, and self-service technologies on a unified platform.

Companies Covered in Barcode Scanner Market

- Honeywell International Inc.

- Zebra Technologies Corporation

- Datalogic S.p.A.

- Wasp Barcode Technologies

- Symbol Technologies Inc.

- Opticon Sensors Europe BV

- Code Corporation

- SATO Holdings Corporation

- CipherLab Co. Ltd.

- Axicon Auto ID Ltd.

- Microscan Systems Inc.

- Cognex Corporation

- Newland AIDC

- Bluebird Inc.

- Others

Frequently Asked Questions

The global barcode scanner market is projected to be valued at US$9.7 billion in 2026.

The barcode scanner market is expected to reach US$15.9 billion by 2033.

Key market trends include the integration of barcode scanning with AI and the rising use of mobile-based scanning solutions.

Portable/Handheld barcode scanners are expected to be the leading product type with a share of nearly 73.2% in 2026, owing to their ability to read damaged or low-quality barcodes quickly.

The barcode scanner market is expected to grow at a CAGR of 7.5% from 2026 to 2033.

Honeywell International Inc., Zebra Technologies Corporation, and Datalogic S.p.A. are a few key market players.