- Executive Summary

- Global Baked Food and Cereals Market Snapshot, 2025 and 2033

- Market Opportunity Assessment, 2025 – 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors – Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2025A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Product

- Global Baked Food and Cereals Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2025-2025

- Market Size (US$ Bn) Analysis and Forecast, 2025 – 2033

- Global Baked Food and Cereals Market Outlook: Product

- Introduction / Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Product, 2025 – 2025

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025 – 2033

- Bread

- Biscuits & Cookies

- Cakes & Pastries

- Breakfast Cereals

- Cereal Bars

- Market Attractiveness Analysis: Product

- Global Baked Food and Cereals Market Outlook: Sales Channel

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Sales Channel, 2025 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Sales Channel, 2025 – 2033

- Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Market Attractiveness Analysis: Sales Channel

- Global Baked Food and Cereals Market Outlook: Attribute

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Attribute, 2025 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Attribute, 2025 – 2033

- Conventional

- Organic

- Gluten-Free

- High-Protein

- High-Fiber

- No Added Sugar

- Clean Label

- Market Attractiveness Analysis: Attribute

- Key Highlights

- Global Baked Food and Cereals Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2025 – 2025

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2025 – 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Baked Food and Cereals Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product

- By Sales Channel

- By Attribute

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- U.S.

- Canada

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025 – 2033

- Bread

- Biscuits & Cookies

- Cakes & Pastries

- Breakfast Cereals

- Cereal Bars

- Market Size (US$ Bn) Analysis and Forecast, By Sales Channel, 2025 – 2033

- Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Market Size (US$ Bn) Analysis and Forecast, By Attribute, 2025-2033

- Conventional

- Organic

- Gluten-Free

- High-Protein

- High-Fiber

- No Added Sugar

- Clean Label

- Market Attractiveness Analysis

- Europe Baked Food and Cereals Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product

- By Sales Channel

- Attribute

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025 – 2033

- Bread

- Biscuits & Cookies

- Cakes & Pastries

- Breakfast Cereals

- Cereal Bars

- Market Size (US$ Bn) Analysis and Forecast, By Sales Channel, 2025 – 2033

- Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Market Size (US$ Bn) Analysis and Forecast, By Attribute, 2025-2033

- Conventional

- Organic

- Gluten-Free

- High-Protein

- High-Fiber

- No Added Sugar

- Clean Label

- Market Attractiveness Analysis

- East Asia Baked Food and Cereals Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product

- By Sales Channel

- By Attribute

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025 – 2033

- Bread

- Biscuits & Cookies

- Cakes & Pastries

- Breakfast Cereals

- Cereal Bars

- Market Size (US$ Bn) Analysis and Forecast, By Sales Channel, 2025 – 2033

- Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Market Size (US$ Bn) Analysis and Forecast, By Attribute, 2025-2033

- Conventional

- Organic

- Gluten-Free

- High-Protein

- High-Fiber

- No Added Sugar

- Clean Label

- Market Attractiveness Analysis

- South Asia & Oceania Baked Food and Cereals Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product

- By Sales Channel

- By Attribute

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025 – 2033

- Bread

- Biscuits & Cookies

- Cakes & Pastries

- Breakfast Cereals

- Cereal Bars

- Market Size (US$ Bn) Analysis and Forecast, By Sales Channel, 2025 – 2033

- Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Market Size (US$ Bn) Analysis and Forecast, By Attribute, 2025-2033

- Conventional

- Organic

- Gluten-Free

- High-Protein

- High-Fiber

- No Added Sugar

- Clean Label

- Market Attractiveness Analysis

- Latin America Baked Food and Cereals Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product

- By Sales Channel

- By Attribute

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025 – 2033

- Bread

- Biscuits & Cookies

- Cakes & Pastries

- Breakfast Cereals

- Cereal Bars

- Market Size (US$ Bn) Analysis and Forecast, By Sales Channel, 2025 – 2033

- Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Market Size (US$ Bn) Analysis and Forecast, By Attribute, 2025-2033

- Conventional

- Organic

- Gluten-Free

- High-Protein

- High-Fiber

- No Added Sugar

- Clean Label

- Market Attractiveness Analysis

- Middle East & Africa Baked Food and Cereals Market Outlook

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2025 – 2025

- By Country

- By Product

- By Sales Channel

- By Attribute

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Product, 2025 – 2033

- Bread

- Biscuits & Cookies

- Cakes & Pastries

- Breakfast Cereals

- Cereal Bars

- Market Size (US$ Bn) Analysis and Forecast, By Sales Channel, 2025 – 2033

- Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Market Size (US$ Bn) Analysis and Forecast, By Attribute, 2025-2033

- Conventional

- Organic

- Gluten-Free

- High-Protein

- High-Fiber

- No Added Sugar

- Clean Label

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- Nestlé S.A.

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- General Mills

- Kellanova

- Mondelez International

- Grupo Bimbo

- Associated British Foods

- Yamazaki Baking

- Barilla Group

- ITC Limited

- Britannia Industries

- PepsiCo

- Kraft Heinz

- Nestlé S.A.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Processed Food

- Baked Food and Cereals Market

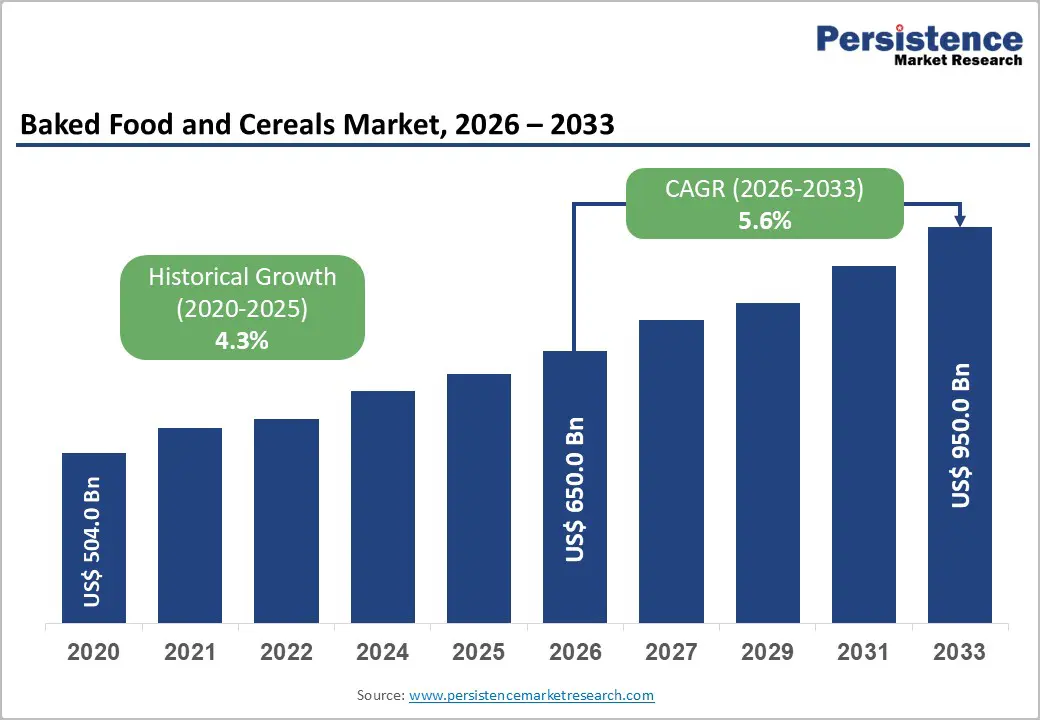

Baked Food and Cereals Market Size, Share, and Growth Forecast, 2026-2033

Baked Food and Cereals Market by Product (Bread, Biscuits & Cookies, Cakes & Pastries, Breakfast Cereals, Cereal Bars), Sales Channel (Supermarkets, Convenience Stores, Specialty Stores, Online), Attribute (Conventional, Organic, Gluten-Free, High-Protein, High-Fiber, No Added Sugar, Clean Label), and Regional Analysis for 2026-2033

Key Industry Highlights

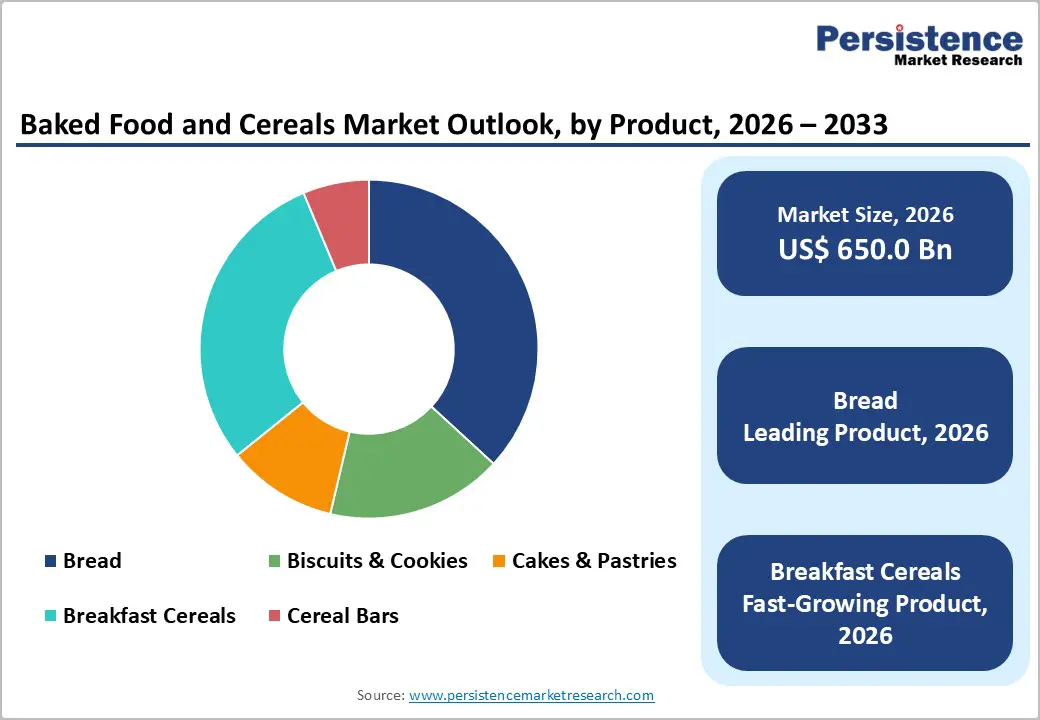

- Dominant Product: Bread is set to command around 35% of revenue share in 2026, while breakfast cereals are likely to grow the fastest at 6.8% CAGR through 2033, driven by fortification and convenience demand.

- Leading Sales Channel: Supermarkets are projected to hold approximately 46% share in 2026, whereas online retail is expected to expand the fastest during 2026–2033, supported by digital grocery penetration.

- Dominant Attributes: Conventional products are anticipated to account for about 63% revenue share in 2026, while gluten-free and high-protein variants are forecast to grow the fastest through 2033, reflecting health-driven purchasing behavior.

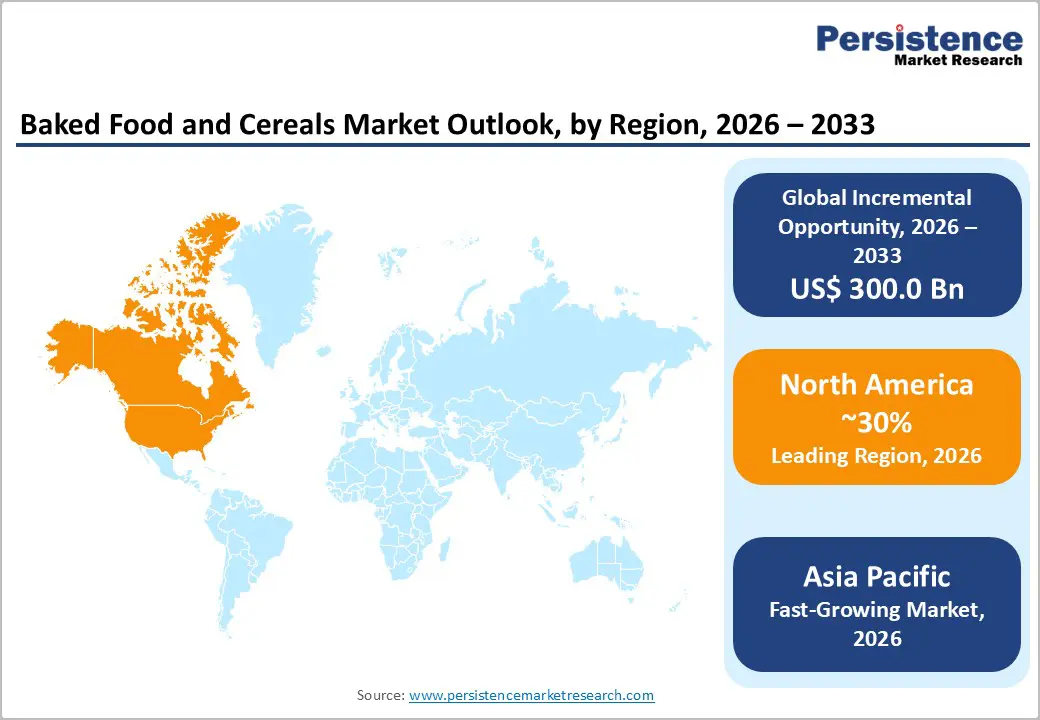

- Regional Leadership: North America is poised to represent nearly 30% of global revenue in 2026, and the Asia Pacific market is slated to register the fastest expansion at about 7.2% CAGR through 2033, led by middle-class income growth.

- Industry Focus: Health-focused reformulations, clean-label innovation, and sugar reduction compliance remain central to competitive strategy, shaping R&D investments and portfolio restructuring.

- January 2026: Nature’s Own introduced Life Wheat + Protein bread, a keto-friendly, protein-enriched loaf that packs considerably higher protein and fiber density per two-slice serving.

| Key Insights | Details |

|---|---|

| Baked Food and Cereals Market Size (2026E) | US$ 650.0 Bn |

| Market Value Forecast (2033F) | US$ 950.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Urbanization, Workforce Participation, and Convenience-Led Consumption

According to the United Nations Department of Economic and Social Affairs (UN DESA), around 68% of the global population will be living in urban areas by 2050. Urban consumers are likely to drive the demand for convenient, ready-to-eat food formats, prioritizing quick meals and portable snacks amid rising dual-income households and compressed mealtimes. This transition is expected to reshape daily food choices toward packaged baked foods and cereals. Recent data from the Indian FMCG sector shows urban sales growth outpacing rural markets in 2025, a clear indicator that city consumption patterns are strengthening demand for convenience staples.

This shift is also reflected in wider retail and delivery trends, with major grocery delivery providers reporting accelerated online grocery growth in late 2025 and early 2026. Notably, a leading U.S. delivery platform saw a 32% year-over-year increase in grocery and retail orders in the fourth quarter of 2025, highlighting increasing reliance on digital channels for food purchases. As digital adoption rises alongside organized retail expansion, improved access and convenience are becoming core drivers of baked foods and cereals consumption, reinforcing mid-to-long-term growth prospects.

Health-Focused Reformulation and Regulatory-Driven Product Innovation

The World Health Organization (WHO) recommends limiting free sugar intake to less than 10% of total energy consumption, and in 2025–2026 several countries have strengthened nutrition policy frameworks to support these targets. Regulatory changes in the UK that came into force in January 2026 impose advertising restrictions on products high in fat, sugar, and salt, including baked goods and cereals, compelling manufacturers to enhance nutrient profiles to remain marketable. Public health agendas are increasingly prioritizing fibre, protein, and reduced sugars, altering product positioning and consumer expectations globally.

Strategic reformulation is becoming an industry imperative, with ingredient and nutrition groups advocating bold recipe adjustments to meet regulatory scoring systems that reward fortified and balanced formulations. In this environment, manufacturers actively reformulate products to improve health credentials, expand nutrient density, and comply with tightening standards, resulting in broader availability of high-fibre, gluten-free, and protein-fortified baked foods and cereals. These regulatory and innovation pressures not only protect public health but also unlock premium segments and strengthen manufacturer competitiveness.

Raw Material Price Volatility and Margin Pressure

The Food and Agriculture Organization (FAO) Food Price Index continued to reflect volatility in staple commodity prices through late 2025 and into early 2026, with the overall index showing mixed movements as cereal prices rise even while some food prices decline, underscoring unpredictable market conditions. The FAO reported that in January 2026, the Food Price Index fell for the fifth consecutive month, but cereal prices remained firm, signaling underlying volatility in grain costs.

Simultaneously, national data from India’s Wholesale Price Index (WPI) indicates that food inflation rebounded in early 2026, with year-on-year food price movements marking sharper increases, a sign of cost pressure re-emerging in key food components. These ongoing shifts in global commodity trends create uncertainty for baked food manufacturers, who face fluctuating wheat, corn, and sugar costs that compress margins. Smaller players with limited hedging capacity are particularly exposed, forcing strategic price adjustments that risk dampening consumer demand in price-sensitive markets.

Regulatory Pressure on Sugar and Ultra-Processed Foods

Regulatory scrutiny of sugar and ultra-processed foods continued to intensify in 2025 and 2026, with several countries introducing or debating new policy measures targeting product labeling and advertising. In Chile in early 2026, the Senate Health Committee approved a bill to label ultra-processed foods and restrict advertising to minors under 14, building on existing front-of-pack requirements aimed at reducing obesity and unhealthy diet prevalence.

In Indonesia, the government is preparing a sugar labeling policy and food safety task force, signaling increased emphasis on consumer awareness and reformulation mandates targeted at reducing excessive sugar consumption in packaged foods. These regulatory shifts require manufacturers to invest in labeling compliance, adjust recipes, and rethink marketing strategies, particularly for sweetened bakery and cereal products. As a result, companies face elevated operational costs and potential demand moderation in traditional high-sugar segments, heightening the need for competitive adaptation through healthier product innovation.

Functional Nutrition and Clean-Label Premiumization

The global shift toward preventive healthcare continues to boost demand for fortified and functionally enhanced products. The WHO has reiterated the urgency of addressing micronutrient deficiencies globally, particularly iron and protein shortfalls in developing regions. In late 2025, the European Commission (EC) reinforced front-of-pack nutrition labeling requirements, prompting food producers to spotlight health benefits such as added vitamins and protein content on packaging, a move that increases consumer clarity and encourages healthier purchasing behavior.

The consumer preference for clean-label products is gaining verifiable traction. In early 2026, Canadian regulators updated guidelines on food additive transparency, requiring clearer declaration of preservatives and sweeteners. These policy shifts support fortified, minimally processed baked foods and cereals that emphasize recognizable ingredients, driving investment in high-protein, whole-grain, and organic offerings. As a result, product portfolios with functional and clean-label benefits are expanding shelf presence and commanding consumer preference in health-oriented channels.

Emerging Market Penetration and Affordable Localization

Emerging markets continue to represent a core strategic growth frontier for baked foods and cereals, supported by both economic expansion and policy initiatives. The World Bank identifies sustained middle-class growth across India and ASEAN nations through 2025, with consumer spending on packaged foods rising steadily. In October 2025, the Indian Ministry of Consumer Affairs reported double-digit growth in packaged breakfast cereals across tier-1 and tier-2 cities, driven by improved retail distribution and consumer awareness.

Moreover, government-led digital commerce initiatives in countries such as Vietnam and Indonesia are expanding market reach for food brands. In early 2026, Indonesia’s Ministry of Trade announced subsidies and logistics support for small food producers selling via e-commerce platforms, making it easier for baked goods and cereal brands to enter untapped rural and peri-urban markets. These developments bolster the case for affordable, localized flavors and small-pack strategies that cater to diverse preferences and purchasing power, unlocking meaningful incremental demand.

Category-wise Analysis

Product Insights

Bread is projected to dominate in 2026, expected to command an estimated 35% of the baked food and cereals market revenue share, reflecting its staple role in daily diets globally. Consumer demand continues to be supported by consistent consumption patterns across age groups and regions. In mid 2025, Grupo Bimbo announced a plan to eliminate artificial colorings from all bread products by the end of 2026, aligning its portfolio with health and natural ingredient trends and reinforcing bread’s relevance in nutrition focused markets. Bread also benefits from institutional demand, in schools, workplaces, and food service — especially for fortified and whole grain variants that cater to both traditional taste preferences and modern health criteria.

Breakfast cereals are expected to grow at an approximate 6.8% CAGR during the 2026-2033 forecast period, outpacing the overall market. This growth is driven by convenience demand and rising health awareness among busy consumers. In 2026, leading cereal brands are launching protein rich variants, for example, Honey Bunches of Oats introduced two new high protein cereal flavors launching nationwide starting January 1, 2026, with 9 g of protein per serving, illustrating category innovation and functional appeal. Consumer expectations for nutritious breakfasts with enhanced protein and fiber content are reshaping category dynamics, encouraging product line extensions that bridge taste and health needs across age segments.

Attribute Insights

Conventional baked foods and cereals are expected to account for approximately 63% revenue share in 2026 due to their affordability, broad accessibility, and mainstream acceptance. These products dominate in price sensitive markets, particularly across developing economies where value oriented purchasing drives market share. Conventional variants also benefit from established supply chains and production scale efficiencies that sustain competitive pricing. Historical consumption patterns reinforce their prominence across family households and daily breakfast occasions.

Gluten-free and high-protein offerings are forecast to grow at an 8.1% CAGR from 2026 to 2033, reflecting strong consumer interest in digestive health, lifestyle nutrition, and fitness oriented diets. Supporting this trend, an ingredient supplier launched a certified gluten-free premix with rice and quinoa blends in 2025 that captured 31% of customer trial share in bakery applications, demonstrating real industry uptake of gluten free solutions. Simultaneously, protein enriched product launches in late 2025 and early 2026 are broadening functional choices for consumers seeking high nutrient breakfast and snack options. These segments are expanding retail penetration and commanding attention across both traditional and digital channels.

Regional Market Insights

North America Baked Food and Cereals Market Trends

North America is a leading market, with the United States expected to contribute approximately 30% of global revenue in 2026. Strong breakfast cereal penetration and mature retail ecosystems sustain stable demand, while consumer preferences increasingly shift toward health enhanced products. A major industry development in late 2025 was the high profile acquisition of WK Kellogg Co by Ferrero Group, strengthening cereal portfolio positioning across the U.S., Canada, and Caribbean markets and indicating continued corporate investment in the region’s cereal segment.

The growth trajectory is supported by both conventional and health centric product innovation. Retailers are expanding gluten free and clean label bakery offerings, reflecting rising dietary awareness among North American consumers, for example, the North American gluten free bakery market reached USD 2.54 billion in 2025 with continued expansion into 2026, driven by demand for allergen free foods. Regulatory changes such as mandatory front of package nutrition warnings introduced in Canada in January 2026 are also shaping product portfolios and enhancing consumer transparency.

Europe Baked Food and Cereals Market Trends

Europe accounts for approximately 28% of global baked foods and cereals revenue in 2026, with Germany, the U.K., France, and Spain leading the region. Recent policy direction in 2025–2026 reflects a strong emphasis on healthier food offerings. European policymakers are progressively urging improvements in nutritional quality beyond beverages and snacks, with breakfast cereals and mueslis included in broader nutrition initiatives aimed at reducing sugar content and enhancing ingredient transparency.

Bread and traditional cereal products benefit from high per capita consumption, but innovation and health trends are reshaping the landscape. For example, consumer and regulatory attention to healthier options is pushing manufacturers to reformulate products with higher whole grain content and lower sugar, aligning with evolving Nutri Score and labeling expectations across the EU. Meanwhile, Europe is balancing food safety with growth strategies as producers innovate in low sugar and high fiber formulations to meet both regulatory and consumer demands. These developments reinforce Europe’s role as a high value, quality driven regional market.

Asia Pacific Baked Food and Cereals Market Trends

Asia Pacific is projected to be the fastest growing regional market for baked food and cereals, with a strong forecast CAGR of 7.2% through 2033. Rapid urbanization, rising disposable incomes, and modern retail expansion in China, India, Japan, and ASEAN countries are key drivers. The Asia Pacific baked food and cereals market is projected to surpass US$ 13.86 billion in 2026, reflecting significant expansion over 2025 levels as consumer preferences shift toward convenient, nutrient rich products.

Market modernization and product innovation are prevalent, supported by digital commerce growth and evolving lifestyle needs. Ready to eat formats, breakfast cereals, and packaged snacks are increasingly popular among urban consumers. Functional foods with enhanced nutrition profiles are gaining traction alongside retail channel diversification. Digital grocery platforms and modern retail infrastructure improvements are enabling widespread distribution outside traditional urban cores. These structural trends underscore Asia Pacific’s dynamic growth momentum in baked foods and cereals.

Competitive Landscape

The global baked food and cereals market exhibits a moderately consolidated structure, with top players such as Nestlé, Kellogg’s, Grupo Bimbo, General Mills, and Mondelez International collectively controlling over 55% of total revenue in 2026. These established players leverage extensive retail and distribution networks, brand equity, and product portfolio breadth to maintain market dominance. Heavy investment in research and development enables innovation in high-protein, gluten-free, fortified, and clean-label products, aligning with evolving consumer preferences and regulatory requirements. Sustainability initiatives and digital marketing strategies further reinforce competitive positioning.

Regional and niche players, including Britannia, Weetabix, Yamazaki, and Intersnack, are targeting specialized product segments or geographic strongholds. These companies often focus on local tastes, affordable pricing, and functional food innovations to differentiate themselves. Barriers such as compliance with international nutrition labeling standards, complex supply chains, and raw material volatility limit new entrants. However, the rise of direct-to-consumer models and e-commerce platforms enables smaller or software-enabled brands to reach targeted audiences. Market consolidation is expected to continue gradually, as global leaders acquire regional companies to expand geographically and technologically, while partnerships and collaborations drive innovation in functional, health-focused baked foods and cereals.

Key Industry Developments

- In September 2025, GoodMills Innovation launched High-MAC brans, a micronized and thermally stabilized cereal ingredient made from wheat, rye, and spelt that enables bakeries to increase fibre and mineral content in baked goods while maintaining texture, taste, and processing performance.

- In September 2025, Meala FoodTech expanded into the baked goods sector with Groundbaker™, a clean-label, single-ingredient pea protein that replicates the binding, gelling, foaming, and emulsifying functions of eggs, enabling manufacturers to reduce costs and dependence on volatile egg supplies.

- In May 2025, La Americana Gourmet by Bonn Group widened its clean-label bakery portfolio with Zero Maida Protein Bread and Zero Maida Ragi Millet Bread, targeting health-conscious consumers with high-protein, fiber-rich formulations made without refined flour, preservatives, or palm oil.

Companies Covered in Baked Food and Cereals Market

- Nestlé S.A.

- General Mills

- Kellanova

- Mondelez International

- Grupo Bimbo

- Associated British Foods

- Yamazaki Baking

- Barilla Group

- ITC Limited

- Britannia Industries

- PepsiCo

- Kraft Heinz

Frequently Asked Questions

The global baked food and cereals market is projected to reach US$ 650.0 billion in 2026.

Rising urbanization, growing dual-income households, and increasing demand for convenient, fortified, and health-oriented products are driving market growth.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Functional nutrition, gluten-free and high-protein innovations, and expansion into emerging markets offer significant growth potential.

Nestlé, Kellogg’s, Grupo Bimbo, General Mills, and Mondelez International are some of the leading players in the market.