- Automotive Components & Materials

- Automotive Steering Wheel Market

Automotive Steering Wheel Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Steering Wheel Market by Product Type (Magnesium Steering Wheel, Aluminum Steering Wheel, Steel Steering Wheel, Others, Sales Channel (OEM, Aftermarket, Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, Technology (Normal, Control Embedded, and Regional Analysis for 2026 - 2033

Automotive Steering Wheel Market Size and Trend Analysis

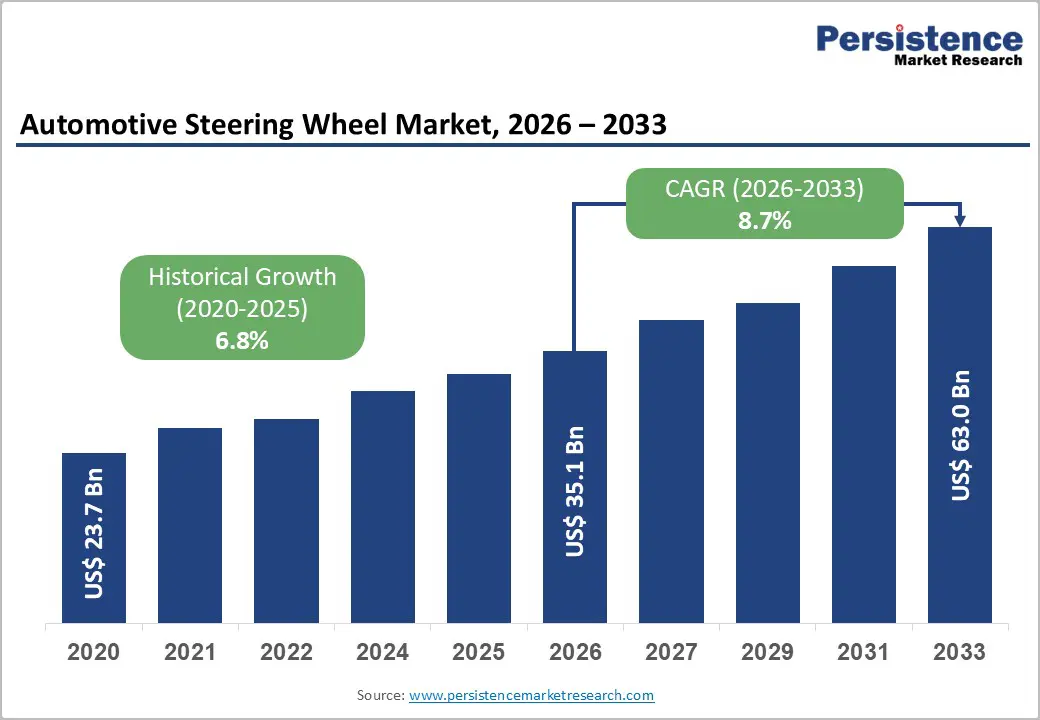

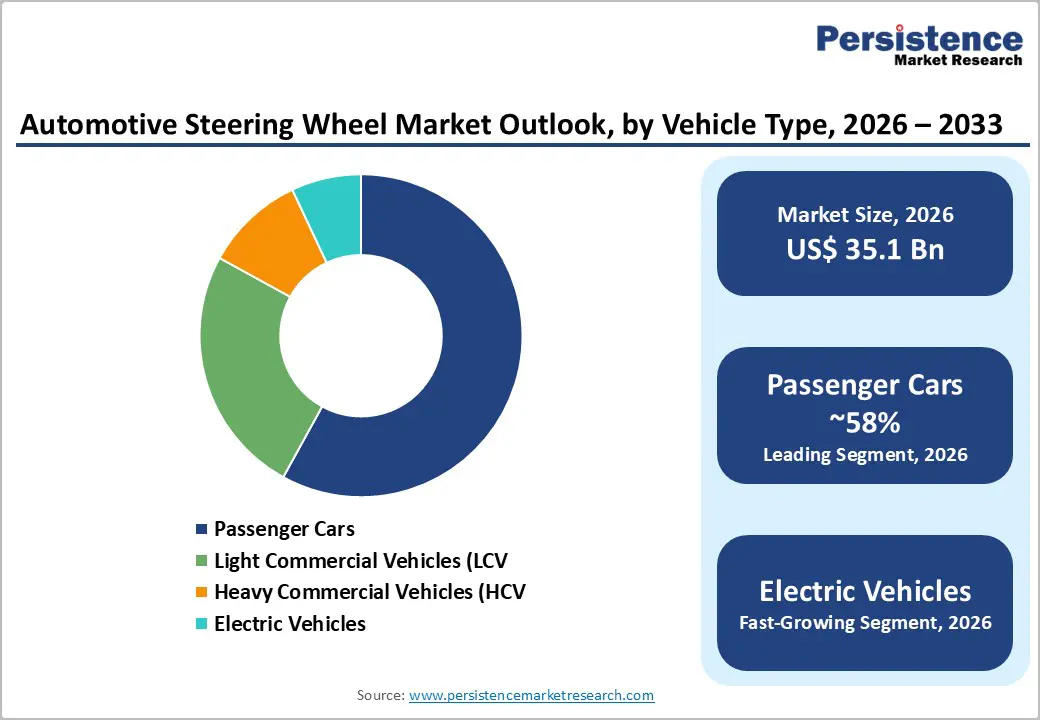

The global automotive steering wheel market size is expected to be valued at US$ 35.2 billion in 2026 and is projected to reach US$ 63.0 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

This strong growth is driven by the accelerating global transition to electric vehicles, the rapid adoption of control-embedded steering wheels integrating driver assistance and infotainment controls, and OEM premiumization strategies elevating steering wheel specifications across passenger and commercial vehicle segments.

Key Industry Highlights:

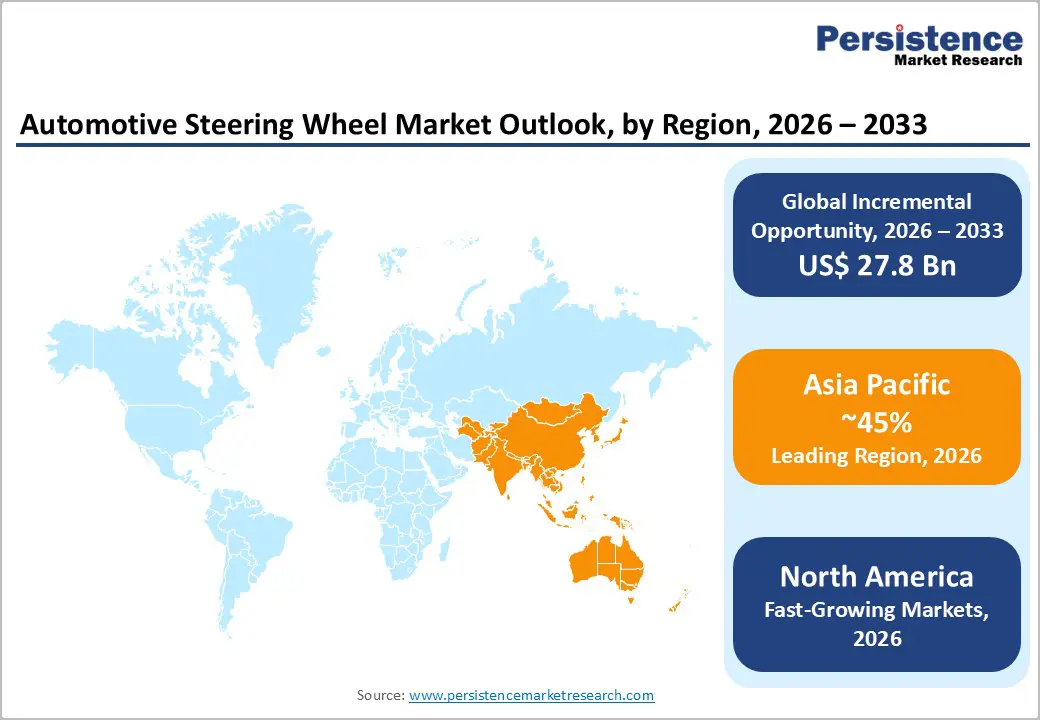

- Leading Region - Asia Pacific leads the global automotive steering wheel market, with China's CAAM-documented 30M+ annual vehicle production, including 9M+ NEVs driving the world's largest steering wheel procurement volumes, complemented by India's SIAM-confirmed 4M+ annual passenger car sales and Japan's advanced OEM steering wheel technology programs.

- Fastest Growing Region - North America is a mature, premiumization-led automotive steering wheel market characterized by high per-vehicle content value, active EV program steering wheel specification upgrades, and growing ADAS integration requirements driving control-embedded steering wheel adoption.

- Dominant Product Segment - Magnesium steering wheels hold 42% market share of the product type in 2025, dominating with the lowest metal density (1.74 g/cm³), FMVSS 203/UNECE R12-compliant impact energy absorption, and universal specification across BMW, Mercedes-Benz, and the VW Group in their premium passenger car global model programs.

- Fastest Growing Product Segment - Control-embedded steering wheels are the fastest growing technology segment, driven by EU GSR 2019/2144 mandating ADAS controls in all new EU vehicles from 2024, Euro NCAP safety rating pressure, and IEA-documented 14M+ global EV sales requiring redesigned steering control architecture.

- Key Opportunity - IEA's projection of 300M+ EVs globally by 2030 creates a structurally growing premium EV steering wheel market where Tesla's yoke and BMW's iDrive-integrated designs command 30-50% per-unit premiums over ICE counterparts, with biometric sensor integration by Bosch and Continental enabling additional technology value layering through 2033.

DRO Analysis

Drivers - EV Adoption and Vehicle Electrification Driving Steering Wheel Redesign and Premiumization

The global electric vehicle revolution is profoundly reshaping automotive steering wheel design and specifications, driving a premium product transformation that is elevating per-unit steering wheel content value above that of conventional ICE vehicle counterparts. In EVs where the driver interface defines the vehicle experience in the absence of engine sound and traditional gear interactions, steering wheel design has become a primary brand differentiation surface, integrating advanced controls for one-pedal driving, regenerative braking adjustment, and digital cockpit management.

The International Energy Agency (IEA reported global EV sales exceeding 14 million units in 2023, with every EV requiring a purpose-designed steering wheel assembly. Premium EV manufacturers, including Tesla, BMW, and Mercedes-Benz EQ, are specifying yoke-style, flat-bottom, and technology-integrated steering wheel designs that carry substantially higher per-unit values than conventional ICE vehicle steering wheels.

Control-Embedded Steering Wheel Adoption Driven by ADAS Integration and Driver Connectivity

The integration of advanced driver assistance systems (ADAS and connected cockpit technologies is compelling OEMs to transition from conventional steering wheels to sophisticated control-embedded assemblies incorporating multifunction paddle shifters, touch-sensitive capacitive controls, voice activation buttons, heated rim elements, and lane-keep-assist sensors that deliver significantly higher per-unit value and margin versus traditional steering wheel designs.

The SAE International autonomous driving level taxonomy and the Euro NCAP safety rating framework both require steering wheel-mounted ADAS activation and override controls in vehicles incorporating Level 1 and Level 2 driving automation features. The European Commission's General Safety Regulation (GSR 2019/2144), mandating ISA (Intelligent Speed Assistance, Emergency Lane Keeping, and other ADAS features) in new EU vehicles from 2024, has directly driven OEM investment in advanced steering wheel control integration programs.

Restraints - Autonomous Driving Development Potentially Eliminating Conventional Steering Wheel Applications

The long-term trajectory of Level 4-5 autonomous vehicle development poses a structural existential question for the conventional steering wheel market: fully autonomous vehicles do not require human-operated steering wheels, potentially rendering this component a permanent vehicle element rather than an optional transitional feature.

While commercially deployed Level 4 robotaxis remain nascent with Waymo and Cruise operating limited commercial fleets, the trajectory of autonomous development creates medium-term specification uncertainty for premium steering wheel programs in vehicles designed for Level 3+ automation, where retractable or removable steering wheel solutions complicate component sourcing decisions.

Raw Material Cost Volatility for Magnesium and Aluminum Die-Cast Components

Automotive steering wheel cores, particularly the growing premium magnesium and aluminum die-cast segments, are exposed to significant raw material price volatility that can compress OEM and Tier 1 supplier margins. Magnesium, the highest-specification steering wheel core material, has experienced price fluctuations documented by the U.S.

Geological Survey (USGS of over 40% between supply/demand cycle extremes, driven by Chinese export policy and global demand competition. Aluminum pricing cycles add further volatility to input costs, particularly given automotive steering wheel die-casting's sensitivity to energy costs in European and North American manufacturing environments.

Opportunities - Electric Vehicle Steering Wheel Innovation: Yoke, Heated, and Biometric Integration

The EV-driven transformation of steering wheel design is creating a sustained premium product innovation cycle that rewards steering wheel manufacturers and OEM engineering teams that invest proactively in next-generation specifications. Tesla's yoke steering wheel in the Model S Plaid, BMW's heated steering wheel with iDrive integration across the i-series lineup, and Mercedes-Benz EQ's capacitive touch-sensitive rim controls demonstrate that EV steering wheel specifications command 30-50% per-unit price premiums over conventional ICE counterparts.

The IEA's Net Zero Scenario projecting 300+ million EVs globally by 2030 implies that the premium EV steering wheel market will scale to an enormous addressable opportunity. Biometric integration, embedding heart rate and drowsiness detection sensors into the steering wheel rim, materializes an emerging premium technology being developed by suppliers, including Bosch and Continental, that will further elevate steering wheel per-unit content value in ADAS-equipped vehicles.

Asia Pacific EV and Commercial Vehicle Production Expansion

Asia Pacific, particularly China and India, represents the largest growth opportunity for automotive steering wheel manufacturers, driven by the world's largest EV production scale and rapidly expanding commercial vehicle fleets that require upgraded steering wheel specifications. China's NEV (New Energy Vehicle) production exceeded 9 million units in 2023, per the China Association of Automobile Manufacturers (CAAM), with every NEV requiring a premium steering wheel system.

India's rapidly expanding passenger vehicle market, as documented by the Society of Indian Automobile Manufacturers (SIAM), is approaching 4 million annual passenger car sales, and growing commercial vehicle production is generating large-volume steering wheel procurement programs. Japanese and Korean premium OEM programs from Toyota, Honda, Hyundai, and Kia require sophisticated control-embedded steering wheel assemblies that sustain high-value regional demand growth.

Category-wise Analysis

Product Type Insights

Magnesium steering wheels represent the leading Product Type segment, accounting for approximately 42% market share in 2025. Magnesium die-cast steering wheel cores have displaced traditional steel in the premium and mid-premium vehicle segments globally due to magnesium's combination of the lowest density of all structural metals (1.74 g/cm³, excellent energy absorption characteristics meeting FMVSS 203 and UNECE Regulation No. 12 impact energy absorption requirements, and superior NVH (Noise, Vibration, and Harshness damping properties that contribute to premium cabin refinement.

The Magnesium Association documents automotive applications as the primary global market for die-cast magnesium components, with steering wheel cores among the highest-volume individual applications.

Sales Channel Insights

OEM (Original Equipment Manufacturer channel is the dominant Sales Channel, accounting for approximately 78% market share in 2025. Automotive steering wheels are safety-critical, vehicle-specific components whose design, mass, inertia, and airbag integration are precisely engineered for each vehicle platform, making aftermarket substitution technically complex and commercially rare in modern vehicles.

The OICA-documented 90 million+ global annual vehicle production represents a structural OEM procurement volume that sustains OEM channel dominance. Steering wheel OEM supply relationships are typically multi-year, model-cycle-aligned programs that provide Tier 1 suppliers with stable revenue visibility. The aftermarket channel serves primarily older vehicle models and customization applications, remaining a smaller but steady revenue stream for steering wheel covers, sport steering wheels, and restoration parts segments.

Vehicle Type Insights

Passenger Cars represent the dominant Vehicle Type segment, accounting for approximately 58% of the global automotive steering wheel market share in 2025. Passenger cars generate the highest absolute volume of steering wheel procurement, reflecting the OICA-documented 70 million+ annual passenger car production globally and additionally command the highest per-unit steering wheel content values through premium feature integration, including heated rims, multifunction controls, leather and alcantara trim, and advanced electronics.

The EV segment within passenger cars is the fastest-growing vehicle type subcategory, and each BEV requires a specialized steering wheel design, driving per-unit value premiumization significantly above the average ICE passenger car steering wheel.

Technology Insights

Control-Embedded steering wheels are the leading technology segment, accounting for approximately 54% market share in 2025, and are the fastest-growing segment, driven by ADAS mandate expansion and connected vehicle feature proliferation. Control-embedded steering wheels integrate multifunction switches, paddle shifters, audio and phone controls, cruise control, and increasingly advanced ADAS override and activation buttons within the steering wheel rim and spoke structure.

The European Commission's GSR 2019/2144, mandating ISA and Emergency Lane Keeping as standard equipment in new EU vehicles from 2024, has made embedded ADAS control architecture a regulatory compliance requirement for European OEM programs, directly mandating a control-embedded steering wheel specification across all new European vehicle programs. Steering wheel-mounted biometric sensor integration for driver drowsiness and health monitoring is the emerging next frontier for this dominant and growing technology segment.

Regional Analysis

North America Automotive Steering Wheel Market Trends & Analysis

North America is a mature, premiumization-led automotive steering wheel market characterized by high per-vehicle content value, active EV program steering wheel specification upgrades, and growing ADAS integration requirements driving control-embedded steering wheel adoption. The U.S. NHTSA's ongoing FMVSS and advanced safety equipment mandates are driving OEM investment in steering wheel technology integration, while Tesla's yoke steering wheel programs and Ford's heated steering wheel standard specification across F-Series trucks are elevating the regional per-unit steering wheel value.

North American EV production investments by GM, Ford, and Stellantis are creating new procurement cycles for premium steering wheel programs.

U.S. Automotive Steering Wheel Market Size

The United States accounts for approximately 79% of the North American automotive steering wheel market revenue in 2025. The U.S. is the world's largest premium automotive steering wheel market by per-unit value, with OICA-documented annual vehicle production of 15-16 million across passenger cars, trucks, and SUVs. Tesla's premium EV steering wheel designs and GM's Ultium EV platform programs are driving innovation. U.S. CAGR is projected at approximately 8.3% through 2033.

Europe Automotive Steering Wheel Market Trends, Drivers & Insights

Europe is the world's most technically demanding automotive steering wheel market, shaped by the GSR 2019/2144 ADAS mandate, Euro NCAP safety rating pressure driving advanced steering wheel control integration, and premium German OEM programs specifying the world's most sophisticated steering wheel assemblies. BMW, Mercedes-Benz, and Volkswagen Group cumulatively represent the world's highest-specification premium steering wheel procurement programs, sustaining above-average per-unit value growth in European OEM channels.

Germany Automotive Steering Wheel Market Size

Germany holds approximately 28% of the European automotive steering wheel market in 2025. Germany's dominant OEM cluster, BMW, Mercedes-Benz, and Volkswagen Group, specifies the world's premium magnesium control-embedded steering wheel programs. Takata Europe (now Joyson Safety Systems and Autoliv) serves German OEM programs.

U.K. Automotive Steering Wheel Market Size

The United Kingdom represents approximately 12% of the European automotive steering wheel market in 2025. UK luxury OEM programs from Rolls-Royce, Bentley, Land Rover, and Aston Martin specify the world's highest-specification bespoke steering wheel assemblies with custom leather, wood, and carbon fiber trim.

France Automotive Steering Wheel Market Size

France accounts for approximately 10% of the European automotive steering wheel market in 2025. Stellantis and Renault Group domestic production drives consistent OEM steering wheel procurement, with EV platform launches including Renault Megane E-Tech and Peugeot e-Series driving premium steering wheel specification upgrades.

Asia Pacific Automotive Steering Wheel Market Drivers & Analysis

Asia Pacific is the fastest-growing and largest automotive steering wheel market, anchored by China's 9 million+ NEV production per CAAM data, driving premium EV steering wheel procurement, India's SIAM-documented 4 million passenger car sales annually sustaining OEM volume demand, and Japan's advanced OEM steering wheel technology programs from Toyota, Honda, and Nissan that maintain premium specification standards. South Korea's Hyundai-Kia Group's global EV platform programs including the Ioniq and EV6 series are driving demand for advanced steering wheel assemblies.

China Automotive Steering Wheel Market Size

China holds approximately 45% of the Asia Pacific automotive steering wheel revenue in 2025 as the world's largest single vehicle production market. CAAM-documented 30+ million annual vehicle production, including 9+ million NEVs, sustains the world's largest steering wheel procurement volumes. Domestic EV brands BYD, NIO, and Li Auto specify advanced control-embedded steering wheel assemblies. China is projected at approximately 9.8% CAGR through 2033.

India Automotive Steering Wheel Market Size

India represents approximately 13% of the Asia Pacific automotive steering wheel revenue in 2025. SIAM-documented 4 million+ annual passenger car sales and growing SUV and EV penetration are elevating per-unit steering wheel specifications. Maruti Suzuki, Hyundai India, and Tata Motors are progressively upgrading to heated steering wheel specifications with control embedded. India is projected at approximately 10.5% CAGR through 2033.

Japan Automotive Steering Wheel Market Size

Japan contributes approximately 11% of the Asia Pacific automotive steering wheel revenue in 2025. Japan is the world headquarters of leading steering wheel manufacturers, including Toyoda Gosei and Autoliv Japan, serving domestic OEM programs requiring the highest quality magnesium diecast and control-embedded steering assemblies for Toyota, Honda, and Nissan. Japan is projected at approximately 8.0% CAGR through 2033.

Competitive Landscape

The global automotive steering wheel market exhibits a moderately consolidated competitive structure at the premium Tier 1 level, with a small number of specialized steering wheel and safety systems companies including Autoliv, Joyson Safety Systems, Toyoda Gosei, Nihon Plast, and Shengkai Industries controlling significant OEM program volumes globally.

Key competitive differentiators include magnesium and aluminum die-casting precision, airbag module integration expertise, control-embedded electronics development capability, and leather/trim craftsmanship for premium specifications. Emerging trends include steering wheel-integrated biometric sensing, EV-specific yoke design development, and modular steering wheel platforms enabling rapid variant customization across OEM model derivatives. Active participation in OEM ADAS integration programs is a prerequisite for new steering wheel program awards.

Key Developments:

- In April 2025, Nexteer Automotive introduced its High-Output Column-Assist Electric Power Steering (HO CEPS). This new addition enhances Nexteer's leading steering portfolio and offers OEMs exceptional flexibility.

- In February 2025, ZF started series production of steer-by-wire systems for the NIO ET9, the market’s first full-SbW deployment. These systems enable variable ratio control without mechanical linkage.

Automotive Steering Wheel Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 23.7 Bn |

| Current Market Value (2026) | US$ 35.1 Bn |

| Projected Market Value (2033) | US$ 63.0 Bn |

| CAGR (2026 - 2033) | 8.7% |

| Leading Region | Magnesium steering wheels, 42% share |

| Dominant Application | Oil Filters, 32% share |

| Top-ranking Product | Passenger Cars, 58% |

| Incremental Opportunity | US$ 27.8 Bn |

Companies Covered in Automotive Steering Wheel Market

- Autoliv Inc.

- Joyson Safety Systems

- Toyoda Gosei Co. Ltd.

- Nihon Plast Co. Ltd.

- Shengkai Industries

- ZF Friedrichshafen AG

- JTEKT Corporation

- Robert Bosch GmbH

- Continental AG

- Delphi Technologies (BorgWarner

- Visteon Corporation

- Martur Fompak International

Frequently Asked Questions

The global automotive steering wheel market is projected to reach US$ 63.0 billion by 2033, growing from an estimated US$ 35.2 billion in 2026 at a CAGR of 8.7%. This accelerating growth reflects EV-driven steering wheel premiumization, control-embedded technology adoption mandated by EU GSR 2019/2144, and China's CAAM-documented 9M+ annual NEV production requiring purpose-designed steering wheel assemblies.

Primary drivers include IEA-documented 14 million global EV sales in 2023 requiring redesigned premium steering systems and Tesla/BMW/Mercedes yoke and control-embedded programs commanding 30-50% per-unit premiums over ICE counterparts.

Magnesium steering wheels lead with approximately 42% product type market share in 2025, dominating through the material's 1.74 g/cm³ lowest metal density enabling maximum weight reduction, compliance with FMVSS 203 and UNECE R12 impact energy absorption standards, and universal specification by BMW, Mercedes-Benz, and Volkswagen Group across their premium passenger car programs globally.

Asia Pacific leads the automotive steering wheel market, anchored by China which accounts for 45% of Asia Pacific revenue through CAAM-documented 30M+ annual vehicle production including 9M+ NEVs from BYD, NIO, and Li Auto.

Key companies include Autoliv Inc. (world's largest automotive safety supplier, US$ 9B+ revenue, Joyson Safety Systems, Toyoda Gosei (Toyota Group integration, highest-volume Japanese OEM program access, Nihon Plast, Shengkai Industries, ZF Friedrichshafen, JTEKT Corporation, Robert Bosch, Continental AG, and Visteon Corporation.