Automotive Powertrain Sensors Market

Industry: Automotive & Transportation

Published Date: November-2024

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 169

Report ID: PMRREP34908

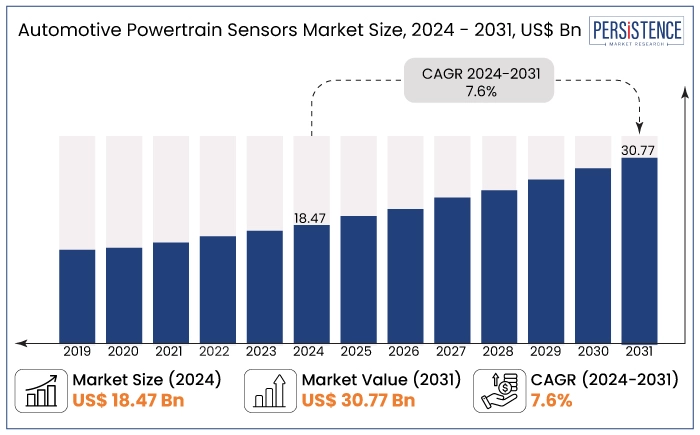

The automotive powertrain sensors market is estimated to increase from US$ 18.47 Bn in 2024 to US$ 30.77 Bn by 2031. The market is projected to record a CAGR of 7.6% during the forecast period from 2024 to 2031. It will likely witness considerable growth due to increasing demand for fuel-efficient and environment-friendly vehicles. Also, stringent emissions regulations and advancements in sensor technology are set to create opportunities.

Emerging applications of Artificial Intelligence (AI) and Machine Learning (ML) in automotive sensors are set to enhance capabilities. These include predictive maintenance, adaptive control, and autonomous driving, thereby adding to the market's growth trajectory.

Growing production and sales of Electric Vehicles (EVs) is another key factor augmenting demand. As per the International Energy Agency (IEA), about 14 million EVs were sold worldwide in 2023, accounting for 18% of total automobile sales. This is more than six times higher than in 2018 and a 35% rise over 2022. In 2023, 95% of EV sales came from China, Europe, and the U.S.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Market Size (2024E) |

US$ 18.47 Bn |

|

Projected Market Value (2031F) |

US$ 30.77 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

7.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

6.8% |

|

Region |

Market Share in 2024 |

|

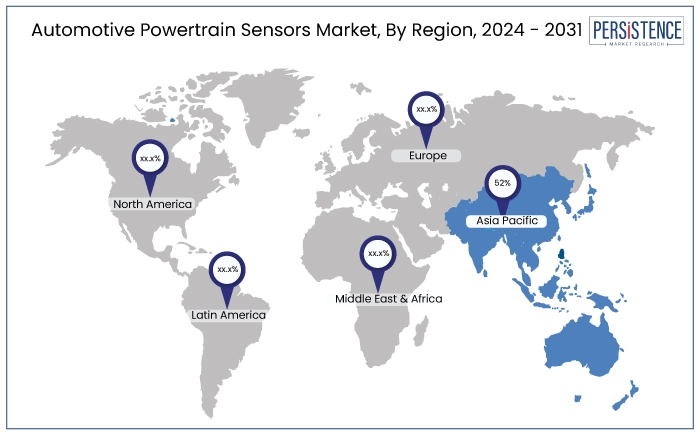

Asia Pacific |

52% |

Asia Pacific is projected to accumulate around 52% of the automotive powertrain sensors market share, followed by Europe, North America, and Latin America. A substantial portion of this regional market is primarily ascribed to the high production levels of automobiles. It is propelled by significant demand from China, India, and Japan.

Enhancement of powertrain systems due to growing consumer awareness of the environmental impacts of automotive emissions is also projected to fuel growth. Escalation of infrastructural developments in the region is another key growth driving factor.

Presence of rapidly expanding economies, including India, China, Indonesia, and Thailand, is resulting in increasing disposable income for consumers. It is further enhancing purchasing power and stimulating demand for automotive. China is anticipated to dominate worldwide automobile manufacturing during the projection period, significantly contributing to high market share.

|

Category |

Market Share in 2024 |

|

Sensor Type- Temperature Sensors |

26% |

Based on sensor type, the market is classified into position, temperature, exhaust, current, voltage, speed, torque, and pressure sensors. Out of these, the temperature sensors segment dominates the market. Temperature sensors are deployed to monitor the temperature of electric motors and inverters. These are mainly used to prevent thermal damage and ensure optimal performance.

In electric and hybrid vehicles, temperature sensors are important for monitoring battery temperature to avert overheating and guarantee optimal performance. Effective management of engine temperature is crucial for minimizing emissions and enhancing fuel efficiency. These sensors also assist in keeping the engine within the ideal temperature range.

|

Category |

Market Share in 2024 |

|

Vehicle Type- ICE Vehicles |

75% |

Based on vehicle type, the market is divided into ICE vehicles, hybrid vehicles, and electric vehicles. Among these, the ICE vehicles segment leads the market. This is owing to the increasing demand for fuel efficiency in Internal Combustion Engine (ICE) vehicles. Rigorous emission regulations to mitigate greenhouse gas emissions and the prevalence of ICE powertrains in emerging economies are also projected to boost demand.

The internal combustion engine powertrain, encompassing diesel and gasoline variants, will likely remain the predominant propulsion technology for the next decade. Powertrain sensors are significantly utilized in automobiles with internal combustion engines.

Sensors monitor and gather data, including temperature, pressure, position, and fluid concentration from different components of the powertrain. These help in transmitting this information to the vehicle's electronic control unit. Then, these are used for the dynamic adjustment of the combustion process, gear shift timing, air-fuel mixture, vehicle steering, and engine operation.

Automotive powertrain consists of components such as the gearbox, drive wheels, engine, driveshaft, track, and propeller, collectively producing energy for vehicle propulsion. Innovations in powertrains are needed for effectively competing in developing transportation markets for motorcycles, automobiles, trucks, ATVs, off-highway vehicles, and vessels.

Automotive powertrain components operate autonomously through various sensors and control systems, optimizing engine efficiency via accurate monitoring. It further helps in improving the combustion process and decreasing emissions. These sensors provide precise air quality, speed, and pressure measurements for the electronic control unit to maintain optimal vehicle drive functions.

The swift expansion of global vehicle sales and production is anticipated to foster advancement of the global automotive powertrain sensors industry. Rising demand for electric vehicles equipped with various sensors, such as voltage sensors to enhance transmission system efficiency, is set to drive growth of the global automotive powertrain sensor market. For instance,

The automotive powertrain sensors market showed steady growth from 2019 to 2023 at a CAGR of 6.8%. It was largely driven by increased demand for fuel-efficient and emissions-compliant vehicles. Up to this point, traditional Internal Combustion Engine (ICE) vehicles were the primary market drivers. These required sensors to monitor fuel usage, emissions, temperature, and engine pressure.

Demand surged for advanced powertrain sensors as the automotive industry adapted to more stringent emissions regulations, contributing to consistent growth. Rising global vehicle production as well as the need for enhanced fuel economy and environmental compliance solidified growth across regions, especially in Asia Pacific and Europe.

The market is set to evolve rapidly with the increasing penetration of EVs and HEVs. Sensor technology is adapting to the demands of electric powertrains, which rely on high-voltage sensors for battery management, temperature control, and energy monitoring.

Innovations in predictive maintenance and autonomous driving technologies are set to further extend sensor applications in vehicles. The shift toward electrification, alongside ADAS, is anticipated to propel growth in the automotive powertrain sensors industry.

Demand for Sensors to Surge in Hybrid Powertrains

A powertrain system consists of multiple components, whether for enhancing the efficiency of a combustion engine or for designing EVs or Hybrid Electric Vehicles (HEVs). Each module functions independently, utilizing distinct sensors and feedback control systems.

The efficiency of a vehicle mainly relies on the accuracy, precision, and response time of its powertrain sensors and actuators. Strict emission regulations and fuel efficiency criteria position hybrid powertrain systems as a viable choice for sustainable and efficient personal transportation.

Leading global automotive manufacturers are either advancing or introducing their hybrid vehicle platforms. HEVs are engineered to enhance the efficiency of internal combustion engines.

Hybrid vehicles are also equipped with start-stop combustion engines that deactivate the motor for several seconds at a red light before initiating a cold start. Powertrain sensors observe the engine's motion as it halts. Upon engine initiation, these help assess the crankshaft's positioning and the ignition cylinder. Companies are coming up with new product launches to compete with their rivals. For instance,

The plug-in hybrid may seamlessly alternate between all-electric and combustion engine modes by briefly operating in all-electric mode for a few kilometers. It also smoothly activates the combustion engine when the battery depletes, enhancing the vehicle's fuel economy and efficiency.

Increasing Awareness of Fuel Efficiency to Boost Sales

Fuel efficiency is a critical determinant of global energy use. Enhanced fuel economy can be attained by optimizing powertrain efficiency by precisely identifying driving circumstances. The powertrain system comprises the engine and transmission, which regulate the vehicle's propulsion and braking force.

The primary elements utilized for assessing driving conditions and enhancing fuel efficiency are the Engine Control Module (ECM), Transmission Control Unit (TCU), and Brake Control Unit (BCU). Fuel economy can be enhanced by increasing powertrain efficiency through the judicious use of engine and battery power.

The quest for improved real-world fuel efficiency has generated a significant need for powertrain sensors that monitor and regulate the engine according to driving conditions. It further helps in optimizing engine performance to enhance fuel economy.

Enhanced fuel efficiency will likely contribute to decreased fossil fuel usage, thereby mitigating vehicle emissions and facilitating the attainment of carbon reduction objectives. Several leading companies are focusing on upgrading their portfolios to attract a large consumer base. For example,

Absence of Harmonization in System Integration May Limit Growth

The demand for sensors in powertrain monitoring and diagnostic applications is rising due to more rigorous fuel economy and emission requirements. In addition, the growing use of hybrid powertrains is set to increase at a fast pace.

A significant impediment to their acceptance and integration with other components arises from the absence of standards among various sensor manufacturers. Moreover, sensors produce vast amounts of data. But, the computational capacity of onboard automobile computers is significantly constrained.

Automotive manufacturers have integration challenges with sensors obtained from various producers. Furthermore, sensors must be optimally located to deliver feedback on the vehicle's powertrain performance.

Improper selection of working circumstances and data loss can significantly impair the sensor's performance. It can result in diminished sensitivity, decreased accuracy, or erroneous positional measurements. Moreover, the power consumption of these sensors presents a significant challenge.

Need to Reduce Vehicle Carbon Footprint to Create Fresh Prospects

Automobiles constitute the predominant source of CO2 emissions. Automotive emissions in the European Union (EU) have risen by 25% since 1990. To fulfil the 2050 Paris climate pledges, the automotive industry must reduce its carbon emissions.

Mitigating vehicle emissions and fuel consumption in long-haul transportation is a primary challenge that must be tackled to lower the carbon footprint of cars. Powertrain sensors are crucial for minimizing emissions in internal combustion engine vehicles and enhancing performance efficiency.

The energy management system utilizes data regarding the upcoming road conditions and other traffic entities to propose a driving and control strategy for the powertrain and its components. It includes the combustion engine, electric motor, battery, transmission, and transmission auxiliaries.

The velocity optimizer maximizes kinetic energy use and enhances fuel efficiency by augmenting the vehicle's kinetic energy and minimizing braking force. The Predictive Gearshift Module (PGS) offers gear shift recommendations derived from the road profile and the optimal vehicle speed generated by the velocity optimizer.

The primary aim of predictive shifting is to prevent a decrease in vehicle speed that results in increased fuel consumption. Control systems, including energy management systems, velocity optimizers, predictive gearshifts, and predictive engine and exhaust after-treatment controls, enhance the combustion system. These enable the optimization of fuel efficiency and diminishing of the carbon footprint of cars. These aspects are anticipated to enhance their adoption in various areas, creating growth potential for market participants. For instance,

The automotive powertrain sensors industry is highly competitive, with a strong presence of established companies such as Bosch, Continental AG, DENSO Corporation, HELLA (now part of Faurecia), and Sensata Technologies. These companies lead the market due to their extensive research and development, wide product portfolios, and partnerships with key automakers.

Bosch and Continental, for instance, are recognized for their advancements in fuel efficiency and emissions reduction technologies. They have integrated sensors with energy management systems. Mid-sized firms and emerging players are also gaining traction by focusing on niche segments like Electric Vehicle (EV) powertrain sensors. They have shown robust growth due to the surge in EV adoption globally.

Innovations in predictive analytics and AI-integrated powertrain sensors have become key differentiators in the market. Companies are enhancing products to meet strict emissions regulations as well as the evolving needs of hybrid and electric vehicles.

Recent Industry Developments in Automotive Powertrain Sensors Market

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Sensor Type

By Powertrain Subsystem

By Vehicle Type

By Region

To know more about delivery timeline for this report Contact Sales

The market is estimated to be valued at US$ 30.77 Bn by 2031.

It evaluates parameters like throttle position, engine speed, oxygen levels, and coolant temperature in the exhaust.

It is a system of components in a vehicle that generates power and propels it forward.

NOx, oxygen, voltage, and throttle position are a few main sensors.

Differential, engine, axles, driveshaft, and transmission are the key components.