Industry: Automotive & Transportation

Published Date: February-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 174

Report ID: PMRREP28033

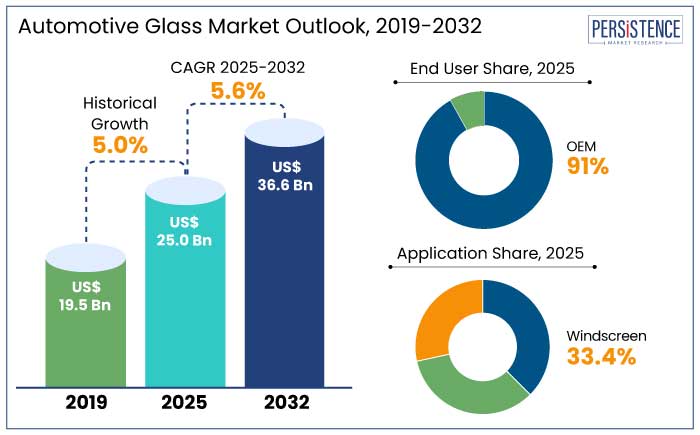

The global automotive glass demand is estimated to grow from US$ 25.0 Bn in 2025 to US$ 36.6 Bn by the end of 2032. The market is projected to expand with 5.6% CAGR during this period.

Persistence Market Research anticipates that the growing sales of new automobiles is expected to drive the automotive glass market. With a growing preference for larger windows and sunroofs in passenger vehicles, the demand for automotive glass will thrive during the forecast period.

Key Highlights of the Market

|

Attributes |

Key Insights |

|

Market Size (2025E) |

US$ 25.0 Bn |

|

Projected Market Value (2032F) |

US$ 36.6 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

5.0% |

The automotive glass market is an essential segment of the automotive industry, contributing to vehicle safety, comfort, and visibility. It encompasses critical components like windshields, side windows (sidelites), and rear windows (backlites), all designed to enhance structural strength and protect passengers.

The market is expanding due to rising disposable incomes, advancements in glass technology, and the growing preference for premium vehicle features that improve aesthetics and comfort. Innovations such as smart glass, heads-up displays (HUDs), and advanced thermal insulation are further transforming the industry, aligning with safety standards and evolving consumer expectations.

In particular, manufacturers are investing in the development of smart glass with embedded technology. These type of glass can have multiple features such as adjustable light blocking, image projections, etc. This trend is expected to fuel market growth in the long term.

Additionally, increased safety regulations on automotive glass in passenger cars are positively impacting the market. These regulations are driving the penetration of gorilla glass in automotive production. Moreover, the increased replacement and repair activities of automotive glass in passenger vehicles is further augmenting market demand.

During the historical span of 2019 to 2024, automotive glass experienced varying demand. Due to the COVID-19 pandemic, the demand from OEMs decreased, negatively impacting automotive glass demand. However, by 2022, with the restoration of the automotive market and significant growth in per capita earnings in urban regions, the automotive glass market registered 5.0% CAGR between 2019 and 2024.

Between 2025 to 2032, the automotive glass market is set to expand with 5.6% CAGR. The growing emphasis on lightweight cars supports the development of lightweight glass, particularly in electric vehicles. As the adoption of electric and autonomous vehicles increases, the demand for automotive glass is expected to grow.

Additionally, stringent regulations regarding the use of automotive glass in vehicles are expected to shape the market. Compliance with safety standards and regulations will be crucial for market players to ensure the quality and safety of their glass products. These market trends are driving the penetration of sales in the industry.

Increasing Demand for Electric and Hybrid Vehicles

The demand for electric and hybrid vehicles has been growing rapidly in recent years. Factors such as favorable government policies, innovations in electric vehicle technology, and the need for sustainable transportation have contributed to this growth.

Between 2023 and 2024, the global EVs sales grew by 25% Y-o-Y, with monthly sales approaching the mark of 2 million units. The lightweight glass, which is a key component in reducing the overall weight of the vehicle has witnessed surged demand from the sector. These vehicles require specialized glass components, such as sunroofs and wide-angle windshields, which drive the market demand.

Advancements in Glass Technology

Technological advancements in automotive glass have played a significant role in driving market growth. Manufacturers are developing glass products that offer improved safety features, such as laminated glass that stays intact even after accidents, protecting vehicle occupants from injuries.

Additionally, advancements in smart glass technology, including features like tinting and defrosting, are attracting consumer interest and resulting in automotive glass market expansion.

High Manufacturing Costs

One key disadvantage in the market expansion is the high manufacturing costs. The float glass process, which is used to manufacture over 90% of the world's automotive glass, requires significant capital investment and operates profitably at a capacity utilization of over 70%.

The raw material and energy consumption contribute to a major share of the overall cost structure of automotive glass. These high manufacturing costs pose challenges for pricing strategies and can impact on the profitability of manufacturers

Limited Adoption in Developing Nations

The market faces challenges in terms of limited adoption in developing nations. Factors such as high manufacturing costs, poor infrastructure, and lower purchasing power in these regions can restrict the market's growth.

The prices of raw materials used in automotive glass production, such as silica, soda ash, and natural gas, can also fluctuate due to changes in demand, supply, and geopolitical factors. These factors can impact pricing strategies and hinder market expansion.

Rise of Self-Driving Cars

The emergence of self-driving cars presents a significant opportunity for the automotive glass market demand. With the increasing adoption of autonomous vehicles, the need for advanced glass technologies, such as head-up displays, augmented reality windshields, and integrated sensors, will rise.

Such technologies can enhance safety, visibility, and overall driving experience in self-driving cars. The automotive glass industry can capitalize on this opportunity by developing innovative glass solutions tailored to the specific requirements of autonomous vehicles.

Shift Towards Sustainable and Smart Glass Solutions

The growing focus on sustainability and environmental consciousness opens doors for the automotive glass market to explore energy-efficient and sustainable glass solutions. Manufacturers can develop glass products that are lighter in weight, energy-efficient, and recyclable, incorporating advanced coatings and materials that enhance thermal insulation and reduce energy consumption.

The integration of smart glass technologies, such as electrochromic and photovoltaic glass, presents an opportunity to improve vehicle efficiency and contribute to sustainable mobility. This shift towards sustainable glass solutions aligns with global efforts to reduce carbon emissions, promote a greener future, and meet stringent environmental regulations.

Tempered Glass Takes the Lead in Product Segment

Based on product, tempered glass dominated the automotive glass market shares with a 60% revenue share in 2024 due to its affordability, strength, and durability. It is four to five times stronger than float glass and more cost-effective than laminated glass, making it the preferred choice for side windows and backlights.

Its ability to shatter into small, blunt fragments upon impact enhances passenger safety, reducing the risk of severe injuries. Additionally, tempered glass is widely used due to its ease of manufacturing and installation, further contributing to its dominance in the market.

The laminated glass segment is projected to grow at a rapid CAGR of 5.3%. Laminated glass is also popular for sunroofs, driving segment growth. Prominent car manufacturers like Volvo, Ferrari, and Tesla incorporate laminated glass in vehicles featuring panoramic sunroofs.

Passenger Cars Take the Wheel in Global Market

Based on vehicle type, in 2024, passenger cars dominated the market with a 64% revenue share, driven by changing consumer trends, a growing middle-class population, and environmental concerns favoring low-emission and lightweight vehicles.

To meet the rising demand, automotive manufacturers are investing in production expansion. For example, VE Commercial Vehicles Ltd established a new plant in India to comply with BS-VI standards, while GM invested US$150 Mn to enhance heavy-duty pick-up truck production in the U.S.

OEMs Continue to Take the Charge

Based on end-use, in 2024, the OEM segment dominated the market with a 91.0% revenue share, driven by the use of automotive glass in vehicle production.

With the establishment of new automotive plants, particularly for electric vehicles like Tesla's factory in Shanghai, the OEM segment is expected to experience significant automotive glass market growth. On the other hand, the aftermarket segment is fueled by factors such as the high usage of old vehicles, maintenance and upgrades, and increasing road accidents.

Windscreen Reigns Supreme in Application Segment

Based on application, the windscreen segment held a significant 33.4% revenue share in 2024, driving automotive and glass manufacturers to develop new technologies for improved appearance and features.

The introduction of self-cleaning glass in windshields is expected to boost segment growth. The sidelight segment is projected to grow at a CAGR of 5.4% and surpass windscreen in volume demand by 2032. Increased usage of tempered glass in sidelights, particularly in the aftermarket, will drive market expansion.

Asia Pacific Sets the Stage for Rapid Market Growth

Asia Pacific emerged as the dominant automotive glass market, capturing a significant 54.2% revenue share in 2024. This can be attributed to the region's robust economic growth, increasing disposable income, and rising demand for commercial vehicles. The automotive industry in Asia Pacific is witnessing substantial investments, further driving the growth of the market.

Countries like China, and India are experiencing changing consumer demands, leading manufacturers to focus on enhancing efficiency to meet the growing vehicle demand. Additionally, the demand for premium vehicles with sunroofs is on the rise in Asia Pacific, contributing to increasing automotive glass market sales.

North America Witnesses Accelerating Sales

North America is projected to grow at a 3.4% CAGR, driven by the rising sales of commercial vehicles, which will boost the demand for automotive glass. Manufacturers are incorporating value-added features like solar control, de-icing, integrated antennas, and rain/light sensors to offer unique products and increase profitability.

In February 2023, US auto glass shops experienced a surge in demand due to increased vehicle break-ins and supply shortages caused by the COVID-19 pandemic.

Companies in the automotive glass market are actively pursuing growth through acquisitions and innovation. The presence of startups introducing fresh offerings adds to the competitive landscape.

To stay ahead, companies are investing in expanding production capabilities and enhancing technological features. Their aim is to develop innovative functionalities and seamlessly integrate technologies into this ever-changing sector, enabling successful market entry and widespread adoption.

Recent Developments

Corning’s Collaborations with Taiwanese giants AUO and CarUX highlight its commitment to fostering innovation and progress. These partnerships leverage Taiwan's expertise and capabilities within the tech industry, fueling advances in automotive design and materials. Corning's Fusion5™ Glass is engineered to meet the rigorous demands of modern automobiles, offering a 4x increase in impact resistance and 2x improvements in optics for Advanced Driver Assistance Systems (ADAS).

|

Attributes |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2024 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Key Country Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled |

|

| Report Highlights |

|

|

Customization & Pricing |

Available upon request |

By Product

By Vehicle Type

By Application

By End User

By Geographical Regions

To know more about delivery timeline for this report Contact Sales

The market is predicted to rise from US$25.0 Bn in 2025 to US$36.6 Bn by 2032.

Growing sales of passenger and commercial vehicles is driving the demand for Automotive glass.

Xinyi Glass Holdings Limited, Vitro, Central Glass Co., Ltd., and Corning Incorporated are some examples of key industry players.

Challenges like the limited adoption of automotive glasses in developing nations and high manufacturing costs are restraining market expansion.

The emergence of self-driving cars and growing focus on sustainability and environmental consciousness are the major factors creating opportunity.