Industry: Automotive & Transportation

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 183

Report ID: PMRREP35086

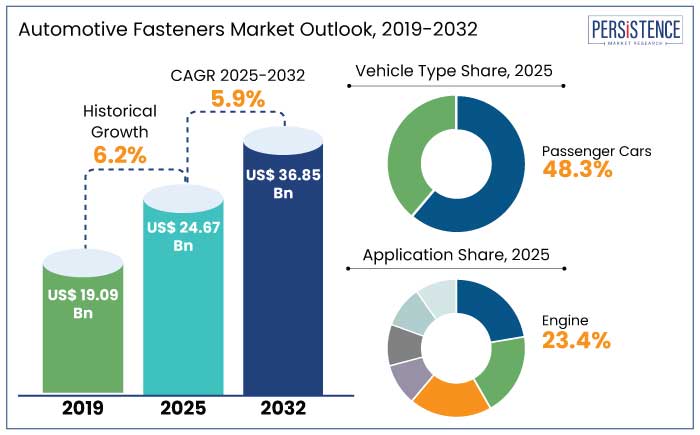

The global automotive fasteners market is estimated to reach a size of US$ 24.67 Bn in 2025. It is predicted to rise at a CAGR of 5.9% through the assessment period to attain a value of US$ 36.85 Bn by 2032.

Improvements in lightweight technology, incorporation of electronics into cars, and high vehicle manufacturing rate are set to propel the global automotive fastener industry. Demand for lightweight fasteners, especially in passenger vehicles, is increasing due to strict government regulations on fuel efficiency and emissions. For instance, manufacturers are adopting plastic and aluminum fasteners for interior trims to reduce vehicle weight and enhance performance.

In 2024, market players like Stanley Black & Decker and Bulten AB initiated working on cutting-edge fastening solutions for electric cars, supported by government grants and incentives. Fasteners play a vital part in contemporary vehicle design. Asia Pacific, which is dominated by China and India, is a key development hub supported by increased automotive production and rising disposable incomes.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Automotive Fasteners Market Size (2025E) |

US$ 24.67 Bn |

|

Projected Market Value (2032F) |

US$ 36.85 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.9% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

6.2% |

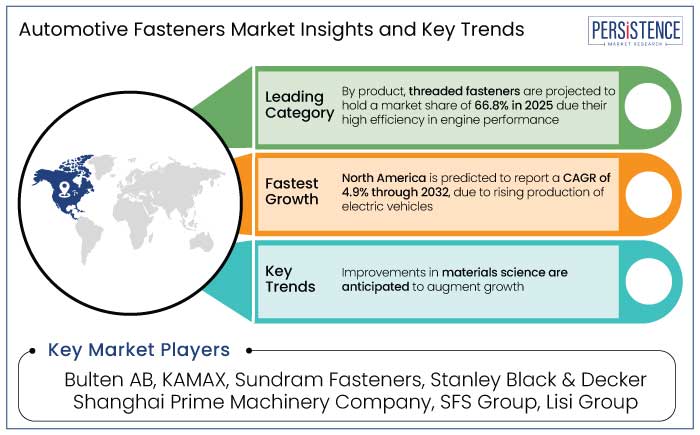

North America is predicted to experience significant growth in the automotive fasteners market, accounting for 28.3% of share in 2025. The region is estimated to record a CAGR of 4.9% from 2025 to 2032. For instance,

Unique technologies, such as smart fasteners with embedded sensors, are transforming the market for electric vehicles (EVs) and autonomous vehicles. Companies like Illinois Tool Works and Stanley Black & Decker are investing in innovations, while government incentives like the U.S. Inflation Reduction Act support domestic manufacturing.

Asia Pacific is projected to dominate on the global scale in 2025, holding a market share of 37.9% in 2025. The region is likely to register a CAGR of 4.8% from 2025 to 2032, driven by increasing localization efforts and sustainability initiatives in the automotive sector.

The automotive industry's dominance is due to rapid growth in China, Japan, and India, which collectively account for a significant portion of global vehicle production. For example,

The need for lightweight and specialized fasteners is increasing due to the region's rapid expansion in electric car production, which is being pushed by BYD and Tata Motors. Regional growth is also being aided by Denso Corporation's latest modular car designs, sophisticated manufacturing processes, and investments in research and development.

In 2025, the threaded segment is set to lead the global market, accounting for 66.8% of the total share. The popularity of threaded fasteners is due to their versatility and widespread use in critical automotive applications like engine assembly, drivetrain systems, and structural components. Key manufacturers like Bulten AB and Stanley Black & Decker are driving developments in threaded fasteners for the auto industry. For instance,

The worldwide trend toward electric vehicles and greater vehicle personalization is projected to keep the threaded fastener category at the top of the automotive fasteners market.

The automotive fasteners market is projected to be dominated by the passenger cars category in 2025, with a 48.3% worldwide share. Urbanization, increased demand, and disposable income in emerging nations are likely to be the main drivers of the development.

The need for specialty fasteners has increased due to the automobile industry's move to lightweight materials like steel and aluminum. Governments worldwide are implementing strict regulations on fuel efficiency and emissions, urging automakers to use novel fastening solutions for lightweight construction. For example,

Demand for automotive fasteners is rising owing to increasing car production and improvements in assembly technology. The adoption of lightweight materials like aluminum and composites aligns with stringent safety and fuel-efficiency standards. For example,

Modular vehicle designs and customization trends are driving growth of the aftermarket business, which, in turn, is increasing demand for adaptable fastening solutions. The engine is the most common application for automotive fasteners, accounting for 23.4% of the market in 2025.

Regionalization of supply chains in North America and Europe is driving localized production. This is because companies like Bulten AB are focusing on reducing lead times and aligning with sustainable manufacturing practices.

The global automotive fasteners market recorded a CAGR of 6.2% in the historical period from 2019 to 2023. The need for lightweight, strong, and high-performing materials in the production of automobiles drove the market's consistent growth in the observed period.

Demand for specialized fasteners for new battery systems, electric drivetrains, and intricate sensor integrations has increased due to the move toward electric vehicles and autonomous driving technologies. Innovations in materials such as composites, aluminum, and high-strength steel have made it possible to produce fasteners for automobiles that are lighter and use less energy.

The industry is anticipated to surge quickly owing to improvements in vehicle design, more stringent safety regulations, as well as increasing popularity of electric and driverless cars. Demand for fastening systems is estimated to record a considerable CAGR of 5.9% during the forecast period between 2025 and 2032.

Surging Production of Electric Vehicles to Fuel Modernization in Industry

Increasing production of electric vehicles (EVs) necessitates the use of specialized fastener designs for battery systems and electrical components, ensuring efficient and lightweight security. For example,

Improvements in Materials Science to Augment Demand

Specialized fastening solutions for aluminum, composites, and plastics are becoming immensely popular as the automotive industry moves toward lightweight materials to increase fuel efficiency and lower emissions. For instance,

Corrosion resistance, structural integrity, and material compatibility are addressed by specialized fasteners made for certain materials. Companies like Stanley Engineered Fastening, Bulten AB, and PennEngineering have developed innovative solutions for fastening composite materials, aluminum, and lightweight plastic components using self-clinching fasteners. This development in fastening technology is driving innovation and ensuring robust, reliable, and efficient assembly processes in the automotive industry.

Disruptions in Supply Chain May Hamper the Industry

The automotive fasteners market is grappling with rising raw material costs, supply chain disruptions, and stringent regulations, prompting manufacturers to explore alternative materials and innovative solutions. For instance,

Companies are embracing sustainable materials and processes due to evolving regulations on carbon footprints and recyclability, highlighting the industry's commitment to innovation and resilience.

Manufacturers to Benefit from Integrating AI in Production Processes

The automotive industry is leveraging AI to enhance manufacturing processes, resulting in increased efficiency, accuracy, and cost savings, while minimizing human error and downtime. For instance,

NVIDIA facilitates virtual testing for autonomous cars, and AI is essential for product design and customization. This is because it allows manufacturers to refine designs and replicate real-world applications. For instance,

Surging Modification of Vehicles to Present Lucrative Prospects

The customer base for automotive fasteners is developing due to the rising demand for customized vehicle modifications, which call for cutting-edge fastening solutions to accommodate distinctive designs and high-performance requirements.

Specialized fasteners are in high demand in the aftermarket industry for a variety of modifications, including improved interior trims and aerodynamic components.

The automotive fastener industry is seeing technical breakthroughs that improve accuracy, durability, and flexibility. Aluminum and titanium alloys are examples of lightweight fasteners that are becoming increasingly popular because of their low weight. Critical applications such as engines and suspension systems are using high-strength fasteners, such as Grade 10.9 and 12.9 bolts.

Micro-thread screws and self-locking nuts are two innovations that are increasing the safety and efficiency of assembly. Zinc-flake or PTFE-coated fasteners provide improved resistance to corrosion. Pre-assembled fastener systems have become immensely popular due to automated production processes, which lowers assembly costs and time.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2025 to 2032 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Product

By Application

By Characteristics

By Material Type

By Vehicle Type

By Region

To know more about delivery timeline for this report Contact Sales

The market size is set to reach US$ 36.85 Bn by 2032.

Hex nuts and flange nuts are common automotive fasteners with hexagonal heads and wide flanges, respectively, used in automobiles.

In 2025, North America is set to attain a market share of 28.3%.

In 2025, the market is estimated to be valued at US$ 24.67 Bn.

Bulten AB, KAMAX, Sundram Fasteners, Stanley Black & Decker, and Shanghai Prime Machinery Company are a few key players.