Industry: Automotive & Transportation

Published Date: January-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 194

Report ID: PMRREP35026

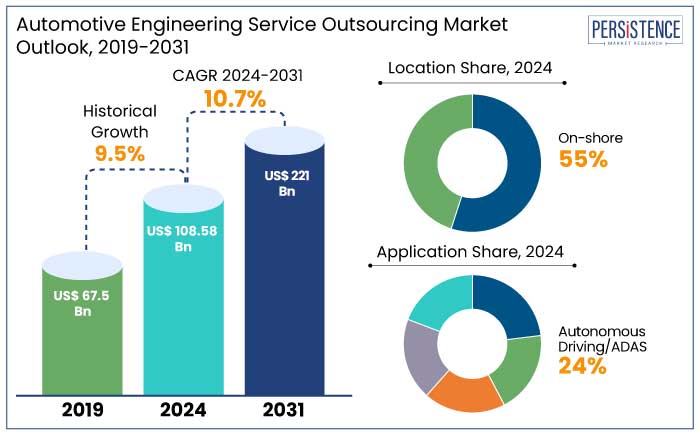

The global automotive engineering service outsourcing market is estimated to reach a size of US$ 108.58 Bn in 2024. It is predicted to rise at a CAGR of 10.7% through the assessment period to attain a value of US$ 221 Bn by 2031.

Demand for automotive Engineering Service Outsourcing (ESO) is skyrocketing as automakers use more sophisticated connectivity technologies to satisfy changing customer needs. Adoption of IoT and AI technologies is driving demand for features such as navigation systems, smart infotainment, passenger safety enhancements, and remote diagnostics.

Companies such as Capgemini and Tata Technologies are collaborating with Original Equipment Manufacturers (OEMs) to provide cutting-edge digital solutions. For instance, in January 2024, Tata Technologies announced a partnership with a leading Europe-based automaker to develop AI-driven ADAS systems.

Government initiatives promoting green vehicles, such as subsidies and tax incentives, have further encouraged the deployment of electric and hybrid vehicles, accelerating ESO demand. Use of lightweight materials and unique manufacturing techniques like 3D printing is gaining popularity, thereby reducing vehicle weight and emissions. Automakers are enhancing their autonomous driving technologies and Advanced Driver-Assistance Systems (ADAS) to remain competitive in the evolving automotive industry.

Key Highlights of the Market

|

Market Attributes |

Key Insights |

|

Automotive Engineering Service Outsourcing Market Size (2024E) |

US$ 108.58 Bn |

|

Projected Market Value (2031F) |

US$ 221 Bn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

10.7% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

9.5% |

The automotive engineering services outsourcing market in North America is a competitive and dynamic sector, accounting for 27% of the total share in 2024. Leading companies in the region, such as Altran, HCL Technologies, and Capgemini, provide a broad variety of technical services. These include system integration, prototyping, and the creation of autonomous vehicles.

Companies are utilizing novel technologies like AI, IoT, and 5G to streamline vehicle systems and improve operational efficiency. The region's market is also influenced by increasing demand for electric and autonomous vehicles, strict emission regulations, and the need for unique connectivity solutions. For instance,

The market is anticipated to record a CAGR of 8.4% from 2024 to 2031, driven by continuous research and development investments and the launch of innovative solutions.

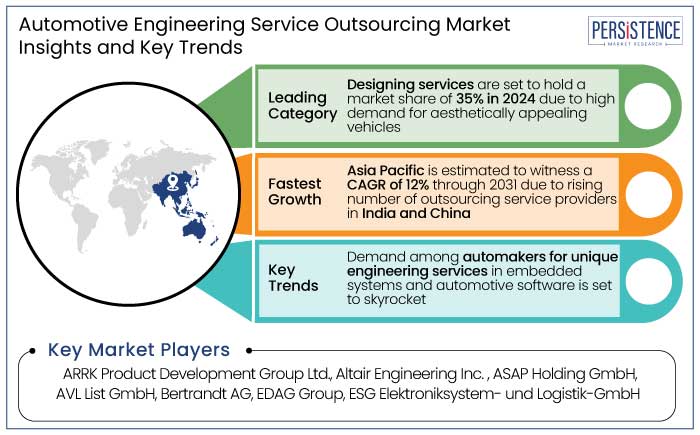

In 2024, the Asia Pacific automotive engineering service outsourcing market accounted for 38.5% of global share. This is due to the presence of key automobile OEMs and the region's competitive edge in outsourcing backed by low-cost labor and skilled workforce. The industry is anticipated to report a CAGR of 12% from 2024 to 2031.

Asia Pacific is further witnessing a surge in electric and connected vehicle adoption. Leading companies like Hyundai and Tata Motors are constantly investing in research and development as well as digitalization. For instance,

China and South Korea are leading in technological developments, accelerating the growth of autonomous and connected vehicle engineering services.

In 2024, designing services dominated the automotive engineering service outsourcing market, accounting for 35% share. This is due to the automotive industry's focus on innovative aesthetics and functional designs. OEMs are prioritizing novel design capabilities in the electric and autonomous vehicle markets to adapt to changing consumer preferences. For example,

Growth of this segment is also being fueled by increasing demand for lightweight materials, ergonomic interiors, and energy-efficient designs. Rise of platform-based vehicle architectures and shared mobility solutions is prompting OEMs to collaborate with ESPs. This strategy aims to optimize designs for versatility and cost efficiency in the era of connected, autonomous, shared, and electric vehicles.

In 2024, the on-shore segment accounted for 55% of the global automotive engineering service outsourcing market share. This indicates a preference for proximity and streamlined collaboration between OEMs and ESPs.

Demand for on-shore services is increasing in North America and Europe due to regulatory requirements, intellectual property concerns, and need for coordination in complex engineering projects. For instance,

On-shore ESO for automotive companies offers quick feedback, reduced cultural barriers, and better alignment with local standards. It is mainly driven by government incentives for innovation and job creation.

Increasing complexity of contemporary automobiles, which calls for specialized knowledge, is driving growth in the global automotive engineering service outsourcing market. In 2024, automakers prioritized electric, autonomous, and connected vehicles, outsourcing engineering services to cut costs and expedite time-to-market. For instance,

Surging electric vehicle production has raised the need for novel engineering in powertrain and battery systems, as companies prioritize range optimization and energy efficiency. Rising platform sharing and modular vehicle architectures has surged the need for engineering services that offer design optimization and flexibility.

Rising software-defined vehicles necessitates expertise in AI, IoT, and big data analytics. Automakers are hence leveraging partnerships with engineering service providers like AVL and Bertrandt to maintain innovation and tackle evolving technological challenges.

The global ESO for automotive market recorded a CAGR of 9.5% in the historical period from 2019 to 2023. To handle the rising complexity of automobiles, including software engineering, end-to-end product development, and electric and autonomous technologies, the automotive industry is seeing a sharp increase in demand for engineering services providers.

While outsourcing engineering services to less expensive countries like China and India, manufacturers are concentrating on quality and cost reduction. As a result, they are able to focus on their primary skills, such as branding and design, while still producing work of excellent quality in other areas. Demand for ESO services is estimated to record a considerable CAGR of 10.7% during the forecast period between 2024 and 2031.

Trend of Platform Sharing and Modular Auto Architecture to Augment Demand

The popularity of platform sharing and modular vehicle architecture is altering the automotive ESO industry. Automakers are increasingly utilizing these strategies to decrease production costs, expedite development, and improve flexibility across various vehicle models. For example,

Modular designs enable the integration of unique technologies like EV powertrains and autonomous systems, increasing the need for specialized engineering services. For instance,

Engineering service providers are crucial in optimizing aerodynamics, weight reduction, and regulatory compliance in the automotive industry, promoting innovation and sustainability.

Focus on EV Development to Spur Demand for Specialized Engineering Services

The focus on Electric Vehicle (EV) development is boosting the need for specialized engineering expertise in powertrain and battery systems. Global automakers are focusing on sustainable mobility, requiring innovative engineering solutions for EV powertrains. These often include electric motors, inverters, and control systems.

Battery systems, crucial for range, safety, and performance, necessitate developments in thermal management, energy density, and charging efficiency. For instance,

Governments are setting ambitious EV adoption targets, prompting engineering service providers to support OEMs with unique designs, testing, and manufacturing technologies.

Complexity of Software and Delays in Outsourcing May Hinder Growth

The complexity of designing transmission systems, powertrains, and engine components demands novel expertise. Engineering service providers often struggle to match this, particularly in the transition to electric vehicles and hybrid systems.

OEMs mainly opt for in-house design to maintain control over proprietary technologies, causing delays in outsourcing and impacting market growth. Also, high service costs pose a barrier in price-sensitive markets.

The automotive sector's economic slowdown and fluctuating demand in 2023 and early 2024 have delayed investments in ESO. Technological limitations like interoperability in autonomous systems may hinder adoption, emphasizing the need for innovative, cost-effective, and specialized solutions.

High Demand for ADAS in Electric Vehicles Creates Prospects for Growth

The autonomous driving/ADAS segment is predicted to dominate the automotive engineering service outsourcing market in 2024. This is due to the rapid adoption of novel driver-assistance systems and ongoing autonomous driving developments. The market share for ADAS in 2024 is estimated to be 24%.

Growing demand for ADAS and autonomous vehicle technologies is prompting automakers to invest in novel sensor systems, AI algorithms, and machine learning for real-time decision-making. Engineering service providers are playing a key role in developing these systems, focusing on sensor integration, testing, and regulatory compliance. For example,

Increasing integration of ADAS features like lane-keeping assist and automatic emergency braking in consumer vehicles is boosting the need for specialized engineering services.

Adoption of Digital Technologies in Automotive Designing Propels Investments

Rising adoption of digital technologies like AI, IoT, and big data analytics is revolutionizing automotive design. It is also improving efficiency and safety, as well as providing personalized driving experience. For instance,

Integration of IoT is enabling real-time vehicle diagnostics, improved connectivity, and seamless infotainment experiences. For example,

Big data analytics is revolutionizing vehicle design by processing vast data and enhancing performance and consumer preferences. The industry is likely to continue evolving with digital solutions.

Companies that offer ESO services are extending their offerings and implementing growth tactics like product launches, mergers, partnerships, and collaborations into practice. They aim to increase market share, strengthen their competitive positioning, and deal with the industry's fragmentation.

By launching cutting-edge solutions, they want to attract a wider clientele and provide an all-encompassing defense against new online dangers. They are also raising the scope of their products by focusing on new markets and enhancing their services with sophisticated features for automotive.

Recent Industry Developments

|

Attributes |

Details |

|

Forecast Period |

2024 to 2031 |

|

Historical Data Available for |

2019 to 2023 |

|

Market Analysis |

US$ Billion for Value |

|

Key Regions Covered |

|

|

Key Market Segments Covered |

|

|

Key Companies Profiled in the Report |

|

|

Report Coverage |

|

|

Customization and Pricing |

Available upon request |

By Service

By Application

By Location

By Region

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 221 Bn by 2031.

The market is estimated to record a CAGR of 10.7% through 2031.

In 2024, North America is set to attain a market share of 27%.

In 2024, the market is estimated to be valued at US$ 108.58 Bn.

Some of the leading players in the market are ARRK Product Development Group Ltd, AKKA; Altair Engineering Inc., and ASAP Holding Gmbh.