- Automotive Components & Materials

- Automotive Catalytic Converter Market

Automotive Catalytic Converter Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Catalytic Converter Market by Component (Two-Way Oxidation, Three-Way Oxidation-Reduction, Diesel Oxidation Catalyst), Material Type (Platinum, Palladium, Rhodium), and Regional Analysis for 2026 - 2033

Automotive Catalytic Converter Market Size and Trend Analysis

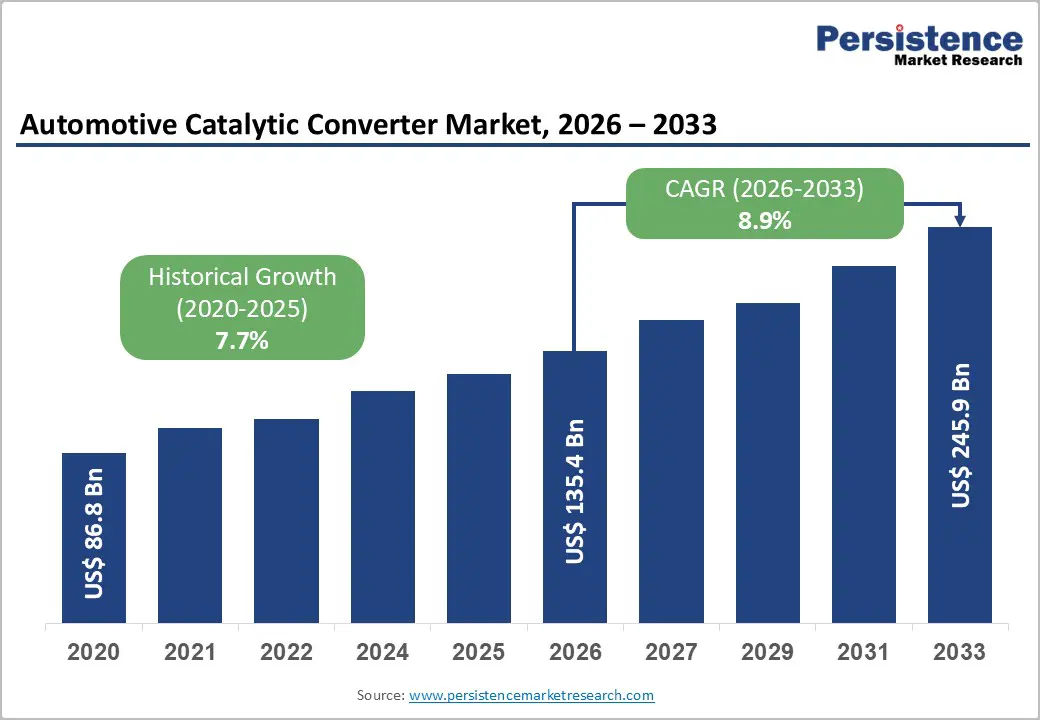

The global automotive catalytic converter market size is supposed to be valued at US$ 135.4 billion in 2026 and is projected to reach US$ 245.9 billion growing at a CAGR of 8.9% between 2026 and 2033.

Tightening tailpipe emission standards across major economies are the principal force lifting demand, supported by record global vehicle production and rising platinum group metal (PGM) loadings per converter. According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle output exceeded 92 million units in 2023, with internal combustion engine (ICE) variants still accounting for over 80% of total volumes.

Key Industry Highlights:

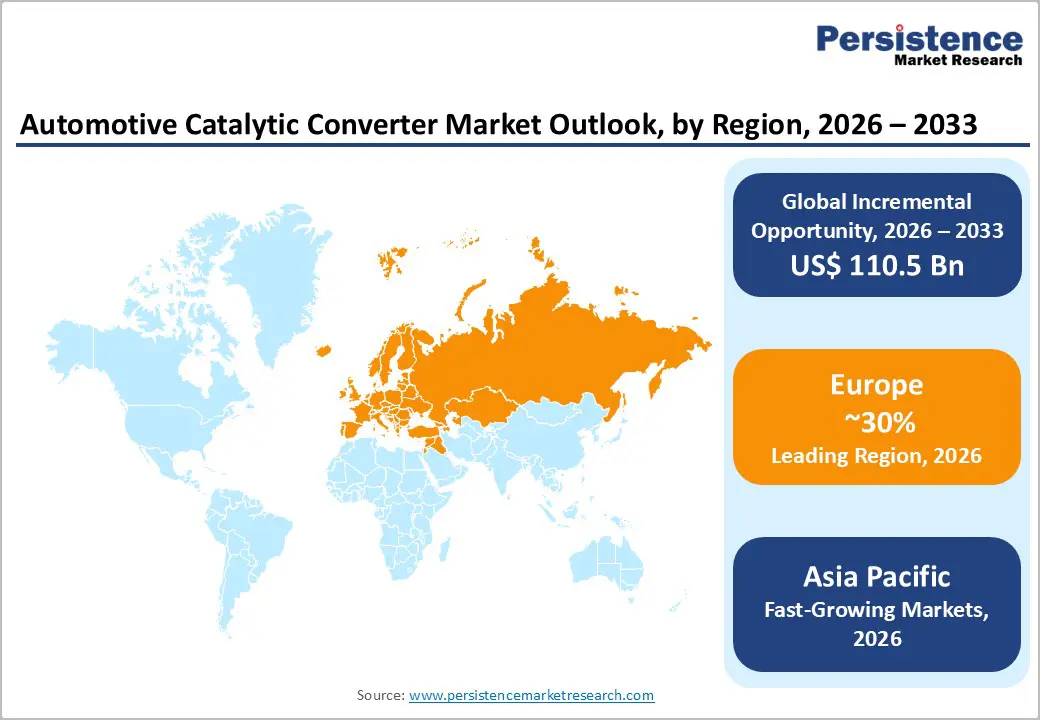

- Leading Region: Europe led the global automotive catalytic converter market with about 28% revenue share in 2026, anchored by Euro 7 implementation, premium vehicle production, and strict periodic vehicle inspection regimes.

- Fast-Growing Market: Asia Pacific is the fastest-growing regional market propelled by China 6b and Bharat Stage VI norms, rising vehicle parc, and the largest combined ICE production base across China, India, Japan, and Korea.

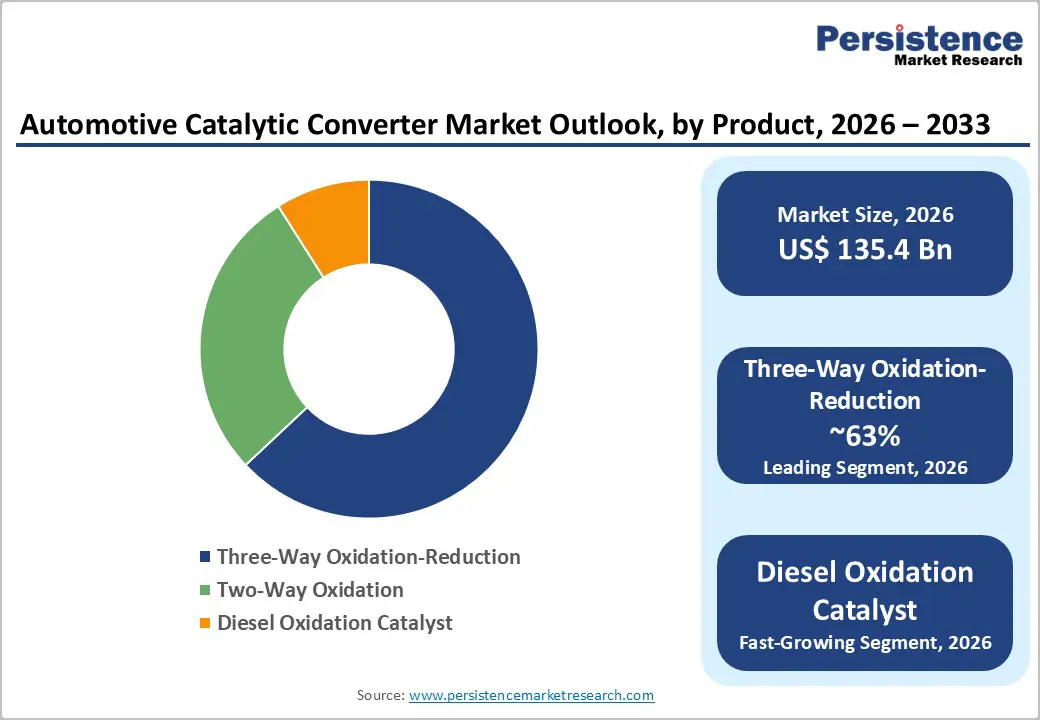

- Leading Component: Three-Way Oxidation-Reduction converters dominated with nearly 63% share in 2025, reflecting the prevalence of petrol passenger cars and stringent NOx, HC, and CO control requirements globally.

- Fastest Growing Component: Diesel Oxidation Catalysts are the fastest-growing component, supported by heavy-duty commercial vehicle retrofit programs, India's vehicle scrappage policy, and tightening Euro 7 NOx norms for diesel powertrains.

- Key Opportunity: Hybrid electric vehicle proliferation creates a multi-decade opportunity for premium converters, as PHEV sales rose 46% in 2023 and Toyota targets over 50% hybrid share of global sales by 2030.

DRO Analysis

Drivers - Stringent Global Emission Norms Mandating Advanced After-Treatment Systems

Regulatory bodies worldwide are progressively narrowing permissible NOx, CO, and particulate matter limits, compelling OEMs to integrate more sophisticated catalytic converter assemblies. The European Commission finalised the Euro 7 framework in April 2024, retaining stringent NOx caps of 60 mg/km for petrol and diesel passenger cars while extending regulatory coverage to brake and tyre particulates for the first time.

The U.S. Environmental Protection Agency’s final rule of March 2024 requires light-duty fleet emissions to drop nearly 50% by 2032 versus 2026 baseline levels. These mandates directly increase per-vehicle PGM loadings, lifting unit values and driving consistent volume demand from the global automotive emission control catalyst market.

Rising Vehicle Parc and Aftermarket Replacement Demand

The expanding global vehicle parc, particularly in emerging economies, is sustaining a robust replacement cycle for catalytic converters. Converters typically degrade after 100,000-150,000 km of operation, creating predictable replacement demand tied to vehicle age distribution across the parc.

OICA data indicates the worldwide vehicle parc surpassed 1.5 billion units in 2023, with India and ASEAN nations recording double-digit annual growth in registrations. The Society of Indian Automobile Manufacturers (SIAM) reported domestic passenger vehicle sales of 4.2 million units in FY24, a record high, adding to the future replacement demand pipeline.

Restraints - Accelerating Electric Vehicle Adoption Eroding Long-Term ICE Demand

Battery electric vehicles (BEVs) do not require catalytic converters, and their rising market share directly compresses the addressable ICE converter base. The International Energy Agency (IEA) reported that global electric car sales reached nearly 14 million units in 2023, representing close to 18% of total new car sales, up from 14% in 2022.

The European Union’s 2035 ban on new ICE passenger car sales and similar legislative pledges from the UK and California Air Resources Board (CARB) are accelerating this structural shift. These regulatory commitments signal a definitive long-term contraction in new ICE vehicle registrations, posing a headwind to converter volumes beyond 2030.

Volatile Platinum Group Metal (PGM) Pricing Pressuring Margins

Catalytic converters depend heavily on platinum, palladium, and rhodium, whose prices remain highly volatile and susceptible to supply disruptions. Rhodium prices peaked above US$ 29,000 per ounce in early 2021 before correcting to approximately US$ 4,500 per ounce by late 2024, illustrating the extreme price swings that converter manufacturers must absorb or pass through.

Such volatility disrupts OEM costing and long-term supply contracting, while supply concentration in South Africa and Russia exposes the industry to geopolitical risk. The U.S. Geological Survey (USGS) notes that South Africa supplies over 70% of mined platinum, amplifying price exposure for converter manufacturers with limited geographic diversification in their raw material sourcing.

Opportunities - Hybrid Electric Vehicle Boom Creating Sustained Demand for Advanced Converters

Hybrid electric vehicles (HEVs) and plug-in hybrids (PHEVs) retain ICE units and therefore require catalytic converters often more sophisticated ones, because cold-start emissions dominate their pollutant profile during the initial warm-up phase before the electric motor takes over. This thermal management challenge drives demand for electrically heated catalyst (EHC) technology and high-cell-density substrates.

The IEA Global EV Outlook 2024 highlighted that PHEV sales rose by 46% year-on-year in 2023, while Toyota, Hyundai, and Stellantis are each expanding their hybrid line-ups across multiple vehicle segments. Toyota alone announced in May 2024 that it expects HEVs to constitute over 50% of its global sales by 2030.

Heavy-Duty Commercial Vehicle Retrofit Programs in Emerging Markets

Governments across Asia and Latin America are launching retrofit and scrappage policies that drive replacement demand for diesel oxidation catalysts (DOCs) and selective catalytic reduction (SCR) systems. India’s Vehicle Scrappage Policy, effective April 2023, mandates fitness testing for commercial vehicles older than 15 years, with the government targeting scrappage of approximately 9 million older vehicles.

Mexico’s federal PROCONVE framework and Brazil’s L-7 norms also require advanced after-treatment retrofitting for heavy commercial vehicles. These policy mandates, combined with rising freight activity driven by e-commerce and infrastructure investment, create durable demand channels for converter suppliers serving the commercial vehicle aftertreatment market.

Category-wise Analysis

Product Type Insights

The Three-Way Oxidation-Reduction (TWC) segment dominated the component category, capturing close to 63% of the global automotive catalytic converter market in 2026. TWCs are the standard after-treatment solution for petrol-fuelled passenger cars, simultaneously reducing carbon monoxide, hydrocarbons, and nitrogen oxides in a single catalyst bed.

According to OICA, petrol vehicles accounted for over 60% of global passenger car production in 2023, anchoring TWC dominance across both OEM and aftermarket channels. Regulatory frameworks such as China 6b and Bharat Stage VI mandate RDE compliance, which TWCs achieve through high PGM loadings and advanced washcoat formulations that maintain conversion efficiency across a wide range of driving conditions.

Material Type Insights

The palladium segment led the material type category, accounting for approximately 55% of the market in 2026. Palladium’s superiority in oxidising hydrocarbons and carbon monoxide at lower temperatures makes it the preferred PGM for petrol-engine TWCs, which dominate global production volumes.

According to the World Platinum Investment Council, auto catalyst demand for palladium reached 8.5 million ounces in 2023, significantly outpacing platinum demand at around 3.0 million ounces. The shift toward palladium-rich formulations began in earnest in the late 2010s when automakers adopted these designs to meet Tier 3 and Euro 6 norms more cost-effectively.

Regional Analysis

North America Automotive Catalytic Converter Market Trends & Analysis

North America held an estimated 22% share of the global market in 2025, supported by stringent EPA standards and a mature aftermarket ecosystem. The U.S. EPA’s March 2024 final rule for light-duty vehicles is projected to prevent 7.2 billion tons of CO2 emissions through 2055, indirectly elevating per-vehicle catalyst content requirements across the fleet.

Regional production hubs in Michigan, Ontario, and Mexico continue to anchor OEM converter demand, while rising catalytic converter theft is fuelling replacement sales. The National Insurance Crime Bureau (NICB) recorded over 64,000 catalytic converter theft incidents in the U.S. in 2022, creating a significant and growing unplanned replacement demand stream in the aftermarket channel.

U.S. Automotive Catalytic Converter Market Size

The U.S. accounted for nearly 83% of North America’s converter revenue in 2025. Light-truck and SUV sales, which represented over 80% of new vehicle registrations per the U.S. Bureau of Transportation Statistics, drive a higher converter content per vehicle compared with sedans due to larger displacement engines and higher PGM loading requirements.

Europe Automotive Catalytic Converter Market Trends, Drivers, & Insights

Europe captured close to 28% of global revenue in 2025, propelled by the rollout of Euro 7 norms and a deeply established premium-vehicle production base. The ACEA reported EU passenger car production of 10.7 million units in 2023, with Germany’s 4.1 million units underpinning the region’s converter demand.

Strict periodic technical inspections under EU Directive 2014/45 ensure consistent aftermarket replacement demand for both TWCs and diesel oxidation catalysts across EU member states. The formal approval of Euro 7 in April 2024 has already prompted FORVIA Faurecia and BASF to accelerate commercialisation of four-way catalyst prototypes integrating gasoline particulate filters.

Germany Automotive Catalytic Converter Market Size

Germany held approximately 32% of European converter revenue in 2025, anchored by the production volumes of Volkswagen Group, BMW Group, and Mercedes-Benz. Germany’s automotive industry employed over 780,000 workers in 2023 per the Verband der Automobil industries (VDA), reflecting the sector’s economic centrality to the national industrial base.

U.K. Automotive Catalytic Converter Market Size

The U.K. represented roughly 11% of European revenue in 2025. The Society of Motor Manufacturers and Traders (SMMT) reported domestic vehicle production of 905,117 units in 2023, with hybrid output growing 44.5% year-on-year, sustaining converter demand.

France Automotive Catalytic Converter Market Size

France contributed nearly 9% of regional revenue in 2025. According to the Comité des Constructeurs Français d'Automobiles (CCFA), France produced 1.5 million vehicles in 2023, with low-emission zones in Paris and Lyon driving converter retrofit demand.

Asia Pacific Automotive Catalytic Converter Market Drivers & Analysis

Asia Pacific is both the fastest-growing regional market and the largest by volume, capturing approximately 38% of global revenue in 2025. The region benefits from massive combined vehicle output, with OICA data showing over 48 million units produced across China, Japan, India, and South Korea in 2023.

Implementation of China 6b and Bharat Stage VI mandates is enabling significant per-unit value escalation by requiring higher PGM loadings and more complex washcoat architectures. This regulatory-driven premiumisation means that revenue growth in Asia Pacific is outpacing unit volume growth, improving the structural economics of the regional market.

China Automotive Catalytic Converter Market Size

China dominated regional revenue with approximately 47% share in 2025. The China Association of Automobile Manufacturers (CAAM) reported domestic vehicle production of 30.16 million units in 2023 globally - anchoring China’s position as the world’s largest converter demand market by volume.

India Automotive Catalytic Converter Market Size

India captured nearly 14% of regional revenue in 2025. Per SIAM, domestic vehicle production reached 28.4 million units in FY24, with two-wheelers and passenger cars together constituting most converter requirements under BS-VI Phase II norms.

Japan Automotive Catalytic Converter Market Size

Japan accounted for approximately 21% of regional revenue in 2025. The Japan Automobile Manufacturers Association (JAMA) reported 8.99 million vehicles produced in 2023, with Japan’s exceptionally high hybrid vehicle penetration led by Toyota and Honda sustaining above-average converter value per vehicle.

Competitive Landscape

The automotive catalytic converter market is moderately consolidated, with the top five players collectively commanding approximately 65% of global revenue. Industry leaders BASF Environmental Catalyst and Metal Solutions, Johnson Matthey, and Umicore focus on PGM-thrifting innovations, electrically heated catalyst designs, and recycling integration as their primary competitive differentiators.

Strategic differentiation centres on washcoat formulation intellectual property, OEM co-development partnerships, and closed-loop PGM recovery capabilities that reduce raw material cost exposure. System integrators including Tenneco, Faurecia (FORVIA), and Ebers ächer combine converter substrates with exhaust system packaging, competing on module-level value engineering for OEM programmes.

Key Developments:

- In August 2024, BASF Environmental Catalyst and Metal Solutions (ECMS) inaugurated a new RD&A laboratory in Chennai, India, focused on developing emission control catalysts tailored to the Indian automotive market and future fuel diversification requirements.

- In April 2024, Euro 7 emission standards were formally approved by EU member states, compelling FORVIA Faurecia and BASF to accelerate commercialization of four-way catalyst prototypes integrating gasoline particulate filters, validated by Volkswagen and Stellantis.

Companies Covered in Automotive Catalytic Converter Market

- UFI Filters

- BASF Environmental Catalyst and Metal Solutions

- Johnson Matthey plc

- Umicore S.A.

- Tenneco Inc.

- Faurecia (FORVIA)

- Eberspächer Group

- Magneti Marelli (Marelli Holdings)

- Boysen Group

- Sango Co., Ltd.

- Yutaka Giken Co., Ltd.

- Katcon Global

- Clariant AG

- Heraeus Holding GmbH

Frequently Asked Questions

The global automotive catalytic converter market is estimated at US$ 135.4 Bn in 2026 and is projected to reach US$ 245.9 Bn by 2033, expanding at a CAGR of 8.9% between 2026 and 2033.

Tightening tailpipe emission norms such as Euro 7, U.S. EPA Tier 3, and China 6b, combined with a global vehicle parc exceeding 1.5 billion units, are driving converter demand.

The Three-Way Oxidation-Reduction (TWC) segment leads with about 63% share, owing to its dominant use in petrol-fuelled passenger cars worldwide and superior multi-pollutant control performance.

Europe leads with around 28% of global revenue in 2025, driven by Euro 7 implementation, premium vehicle output of 10.7 million passenger cars per ACEA, and stringent inspection regimes.

Leading players include BASF Environmental Catalyst and Metal Solutions, Johnson Matthey plc, Umicore S.A., UFI Filters, Tenneco Inc., Faurecia (FORVIA), and Eberspächer Group.