- Executive Summary

- Global Automotive Bearing and Clutch Component Aftermarket Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 – 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors – Relevance and Impact

- Value Added Insights

- Regulatory Landscape

- Technology Adoption Analysis

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Global Automotive Bearing and Clutch Component Aftermarket Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026–2033

- Global Automotive Bearing and Clutch Component Aftermarket Market Outlook: Vehicle Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Vehicle Type, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Vehicle Type, 2026 – 2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Market Attractiveness Analysis: Vehicle Type

- Global Automotive Bearing and Clutch Component Aftermarket Market Outlook: Material Type

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Material Type, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Material Type, 2026 – 2033

- Steel/Metallic

- Ceramic

- Market Attractiveness Analysis: Material Type

- Market Attractiveness Analysis and Forecast, Component Type

- Introduction / Key Finding

- Historical Market Size (US$ Bn) Analysis, Component Type, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, Component Type, 2026 – 2033

- Clutch Kits

- Wheel Bearings

- Actuator

- Market Attractive Analysis: Component Type

- Key Highlights

- Global Automotive Bearing and Clutch Component Aftermarket Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region, 2020 – 2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026 – 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Automotive Bearing and Clutch Component Aftermarket Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Vehicle Type

- By Material Type

- By Component Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Vehicle Type, 2026 – 2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Market Size (US$ Bn) Analysis and Forecast, By Material Type, 2026 – 2033

- Steel/Metallic

- Ceramic

- Market Attractiveness Analysis and Forecast, By Component Type, 2026 – 2033

- Clutch Kits

- Wheel Bearings

- Actuator

- Europe Automotive Bearing and Clutch Component Aftermarket Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Vehicle Type

- By Material Type

- By Component Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Vehicle Type, 2026 – 2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Market Size (US$ Bn) Analysis and Forecast, By Material Type, 2026 – 2033

- Steel/Metallic

- Ceramic

- Market Attractiveness Analysis and Forecast, By Component Type, 2026 – 2033

- Clutch Kits

- Wheel Bearings

- Actuator

- East Asia Automotive Bearing and Clutch Component Aftermarket Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Vehicle Type

- By Material Type

- By Component Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Vehicle Type, 2026 – 2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Market Size (US$ Bn) Analysis and Forecast, By Material Type, 2026 – 2033

- Steel/Metallic

- Ceramic

- Market Attractiveness Analysis and Forecast, By Component Type, 2026 – 2033

- Clutch Kits

- Wheel Bearings

- Actuator

- South Asia & Oceania Automotive Bearing and Clutch Component Aftermarket Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Vehicle Type

- By Material Type

- By Component Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Vehicle Type, 2026 – 2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Market Size (US$ Bn) Analysis and Forecast, By Material Type, 2026 – 2033

- Steel/Metallic

- Ceramic

- Market Attractiveness Analysis and Forecast, By Component Type, 2026 – 2033

- Clutch Kits

- Wheel Bearings

- Actuator

- Latin America Automotive Bearing and Clutch Component Aftermarket Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Vehicle Type

- By Material Type

- By Component Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Vehicle Type, 2026 – 2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Market Size (US$ Bn) Analysis and Forecast, By Material Type, 2026 – 2033

- Steel/Metallic

- Ceramic

- Market Attractiveness Analysis and Forecast, By Component Type, 2026 – 2033

- Clutch Kits

- Wheel Bearings

- Actuator

- Middle East & Africa Automotive Bearing and Clutch Component Aftermarket Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 – 2025

- By Country

- By Vehicle Type

- By Material Type

- By Component Type

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 – 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Vehicle Type, 2026 – 2033

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Market Size (US$ Bn) Analysis and Forecast, By Material Type, 2026 – 2033

- Steel/Metallic

- Ceramic

- Market Attractiveness Analysis and Forecast, By Component Type, 2026 – 2033

- Clutch Kits

- Wheel Bearings

- Actuator

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

- Schaeffler AG

- Overview

- Segments and Products

- Key Financials

- Market Developments

- Market Strategy

- ZF Friedrichshafen AG

- Valeo SA

- SKF Group

- Exedy Corporation

- Aisin Corporation

- The Timken Company

- NSK Ltd.

- NTN Corporation

- JTEKT Corporation

- Eaton Corporation plc

- BorgWarner Inc.

- PHC (PHC Valeo)

- NRB Bearings Ltd.

- Dana Incorporated

- RBC Bearings

- Schaeffler AG

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automotive Components & Materials

- Automotive Bearing and Clutch Component Aftermarket Market

Automotive Bearing and Clutch Component Aftermarket Market Size, Share, and Growth Forecast, 2026 – 2033

Automotive Bearing and Clutch Component Aftermarket Market by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), Component Type (Clutch Kits, Others), Material Type (Steel/Metallic, Ceramic), and Regional Analysis 2026 – 2033

Automotive Bearing and Clutch Component Aftermarket Market Size and Trends Analysis

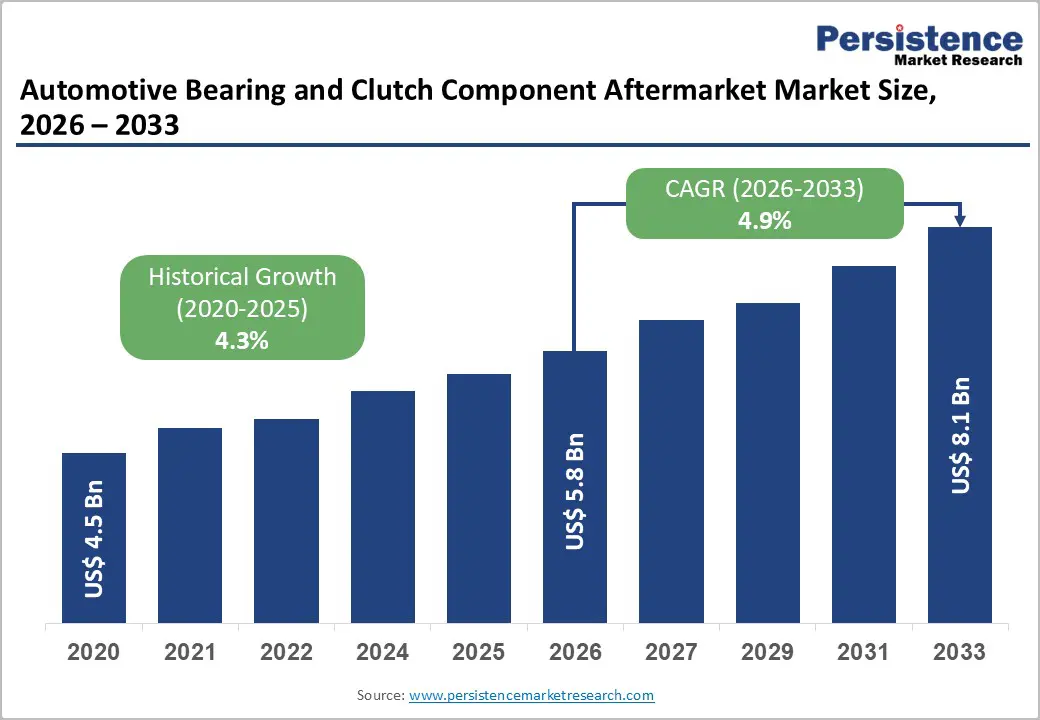

The global automotive bearing and clutch component aftermarket market size is likely to be valued at US$5.8 billion in 2026 and is expected to reach US$8.1 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by aging vehicle fleets worldwide, increasing vehicle kilometers traveled, and rising demand for reliable replacement parts.

Key Industry Highlights:

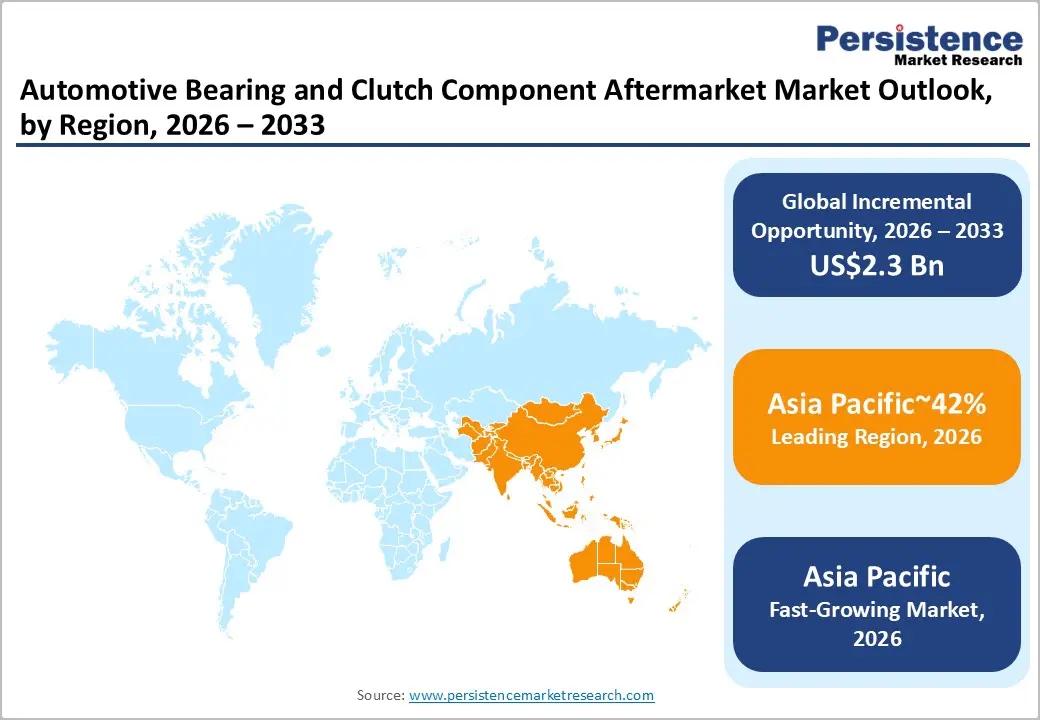

- Leading Region: Asia Pacific is projected to lead due to its large vehicle parc, expanding automotive production base, and strong independent aftermarket networks, accounting for approximately 42% share.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest due to increasing vehicle ownership, rising average vehicle age, and expanding last-mile logistics activity.

- Leading Component Type: Clutch kits/Plates are projected to dominate with approximately 48%, driven by recurring replacement needs, drivetrain performance requirements, and strong penetration across manual transmission vehicles.

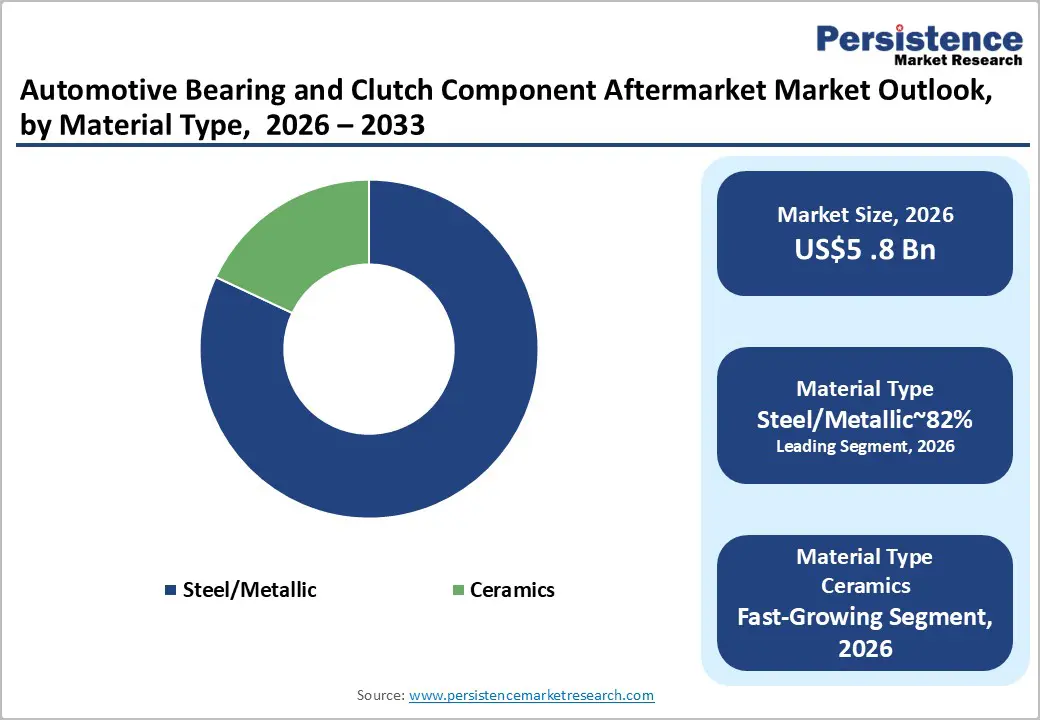

- Leading Material Type Segment: Steel/Metallic components are projected to dominate, accounting for approximately 82%, supported by cost-efficiency, structural strength, and compatibility with high-load automotive systems.

| Key Insights | Details |

|---|---|

| Automotive Bearing and Clutch Component Aftermarket Market Size (2026E) | US$ 5.8 Bn |

| Market Value Forecast (2033F) | US$ 8.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Aging Vehicle Population

The increasing average age of global vehicles is structurally expanding demand within the automotive bearing and clutch aftermarket. Older vehicles exhibit accelerated wear on drivetrain and rotational components, generating recurring replacement cycles that sustain aftermarket procurement. This trend is particularly pronounced in mature markets where regulatory compliance and operational safety requirements mandate timely maintenance, embedding replacement bearings and clutches into standard service workflows. Extended vehicle lifespans amplify cumulative component consumption, influencing inventory planning, supply chain responsiveness, and margin structures across the aftermarket value chain. Aging fleets also drive higher utilization of diagnostic and refurbishment technologies, encouraging integration of predictive maintenance tools and condition-monitoring sensors into service protocols, thereby supporting aftermarket resilience.

The expansion of the vehicle parc enhances structural stability in replacement part consumption, while regulatory oversight ensures component quality and service standards. Component wear accelerates cost pressures on service networks, influencing pricing strategies and operational efficiencies. Simultaneously, aftermarket suppliers adjust production volumes, logistics frameworks, and inventory turnover to accommodate the higher replacement frequency. Technological adaptation in materials, coatings, and design innovations further mitigates failure rates while sustaining revenue generation, establishing aging fleets as a durable driver of aftermarket demand.

Technological Enhancements and AI Integration

Advancements in bearing and clutch design, materials, and manufacturing processes are reshaping the automotive aftermarket landscape. High-performance alloys, surface treatments, and precision machining extend component durability while reducing friction and energy losses, directly affecting replacement cycles and lifecycle costs. Integration of sensors and smart monitoring systems enables predictive maintenance, allowing service providers to anticipate failures and optimize repair schedules. AI-driven analytics enhance fleet-level diagnostics, supporting data-informed inventory management, demand forecasting, and cost allocation across the aftermarket value chain. These technological upgrades create opportunities for higher-margin products while reinforcing operational reliability in service networks and maintenance ecosystems.

AI-enabled platforms and connected component technologies influence procurement, distribution, and aftermarket service strategies. Adoption of predictive maintenance and real-time monitoring shifts demand patterns toward premium, technologically advanced components. Supply chains increasingly incorporate digital tools for quality assurance, fault detection, and adaptive inventory replenishment, improving efficiency and reducing operational risk. Regulatory alignment around component performance and safety further incentivizes innovation, embedding AI and material advancements as structural drivers of aftermarket growth.

Barrier Analysis – OEM Competition and Counterfeits

The presence of original equipment manufacturers (OEMs) and counterfeit components exerts significant constraints on the automotive bearing and clutch aftermarket. OEM parts are often perceived as higher quality and come with manufacturer-backed warranties, creating a structural preference among fleet operators and repair networks. Counterfeit and substandard components undermine market trust, introducing reliability risks, premature failures, and increased warranty claims, which in turn elevate service costs and operational liabilities. These dynamics impact value-chain economics by pressuring margins for certified aftermarket suppliers while increasing quality assurance and inspection requirements throughout procurement, distribution, and installation processes.

Stringent regulatory frameworks around safety and component certification intensify compliance demands, especially in regions with high counterfeit penetration. Aftermarket participants must invest in traceability systems, advanced testing protocols, and supplier vetting to mitigate risk exposure. The dual pressures of OEM dominance and illicit parts proliferation constrain volume growth and segment expansion, while driving cost escalation across inventory management, logistics, and post-sale support. Collectively, these forces create structural barriers to scaling aftermarket penetration and sustaining long-term profitability.

Electronic Clutch-by-Wire Calibration Lockouts

The transition from mechanical and hydraulic clutches to Clutch-by-Wire (CbW) architectures introduces systemic barriers for the aftermarket segment. Component replacement now necessitates proprietary software resets and diagnostic calibrations, which are embedded within OEM control modules. Independent service providers often lack access to required "handshake" protocols, constraining their ability to perform post-installation calibration and limiting repair scope. This technological gatekeeping effectively redirects maintenance demand toward authorized dealerships, altering value-chain dynamics and concentrating revenue and service margins within OEM-aligned networks. The shift also elevates training, tooling, and cybersecurity requirements across aftermarket operations, raising operational complexity and associated costs.

CBW systems influence inventory strategies, service workflows, and component compatibility verification processes. Regulatory standards for electronic safety systems reinforce the necessity of calibrated interventions, further constraining independent repair options. Aftermarket players must contend with restricted data access, increased technical risk, and integration challenges when servicing electrified or software-controlled drivetrains. These structural impediments reduce aftermarket penetration potential, intensify competitive asymmetry, and necessitate investment in diagnostic interoperability to maintain operational relevance within advanced vehicle ecosystems.

Opportunity Analysis – Remanufacturing Services for Heavy-Duty Clutch Assemblies

The increasing emphasis on sustainability and circular economy principles is driving demand for remanufactured heavy-duty clutch assemblies in commercial fleets. OE-standard refurbishment of large-diameter clutch discs and pressure plates enables significant cost efficiency while preserving performance and reliability standards. This structural shift supports fleet operators in optimizing lifecycle expenditure, reducing material consumption, and aligning with regulatory pressures on waste reduction and environmental compliance. The integration of advanced remanufacturing techniques, including precision machining, surface treatment, and quality validation, ensures that refurbished components meet stringent operational and safety requirements, reinforcing aftermarket credibility and adoption potential.

Remanufacturing expands service offerings, creating revenue streams for specialized providers while alleviating procurement pressures on new component production. Supply chains adapt to circular flows, incorporating collection, reconditioning, and redistribution networks. Regulatory frameworks incentivize sustainable practices, shaping technical standards and certification protocols. As adoption grows, remanufacturing services structurally enhance margin efficiency, reduce dependency on raw material procurement, and embed environmentally responsible operations within the broader heavy-duty clutch aftermarket ecosystem.

Digital Health-Monitoring Bearings for Fleet Telematics

The integration of MEMS sensors into wheel bearings is creating a transformative opportunity within the aftermarket ecosystem. These digital bearings enable continuous monitoring of vibration, temperature, and load conditions, providing actionable data to fleet operators and maintenance networks. Predictive maintenance frameworks leverage this intelligence to preempt component failure, optimize service schedules, and reduce unplanned downtime. Collaboration between aftermarket suppliers and telematics providers embeds bearings into connected vehicle systems, enhancing data-driven decision-making across fleet operations while influencing inventory planning, warranty management, and cost allocation. This integration strengthens operational reliability and introduces higher-margin, technologically enhanced components into the aftermarket value chain.

Health-monitoring bearings shift aftermarket dynamics toward proactive, data-enabled maintenance services. Supply chains adapt to real-time analytics and reporting requirements, while service networks must integrate diagnostic and calibration capabilities. Regulatory compliance for operational safety and performance further incentivizes adoption, particularly in commercial fleets. The deployment of sensor-enabled components establishes a recurring demand cycle for analytics, replacements, and upgrades, structurally positioning predictive maintenance technologies as a sustainable growth vector within the automotive bearing aftermarket.

Category–wise Analysis

Component Insights

Clutch kits are expected to lead the market, accounting for approximately 48% share in 2026, underpinned by the convergence of mechanical wear cycles, urban traffic-induced friction, and rising vehicle age across light commercial and passenger vehicle segments. Adoption remains anchored by the high replacement value, modular “3-in-1” kit configuration, and integration with Automated Manual Transmission (AMT) systems, with providers prioritizing operational efficiency, workflow integration, and reduced return rates in high-volume service environments. Ongoing platform evolution, including sensor-ready release bearings, friction material upgrades, and digital catalogue precision for VIN-specific fitment, continues to reinforce replacement cycles and utilization intensity. Schaeffler (LuK), ZF (Sachs), Valeo, and Exedy, and their respective kits and Dual Mass Flywheel offerings further lock in service workflows. This combination of mature infrastructure, ecosystem lock-in, and predictable demand sustains the segment’s dominance within structured aftermarket deployment models.

Actuators are expected to be the fastest-growing segment, driven by the transition from mechanical linkages to electro-hydraulic and clutch-by-wire systems across modern AMT, DCT, and hybrid drivetrains. Growth is being catalyzed by sensor-integrated Concentric Slave Cylinders, high-performance plastic housings, and predictive maintenance integration, which materially improve component reliability, early-failure detection, and unit economics for fleet operators. Accelerating adoption is supported by telematics-enabled diagnostics, advanced calibration tools, and interoperability with electronic control units, lowering operational friction for first-time adopters. FTE automotive (Valeo), Schaeffler (LuK), Aisin, and ZF (Sachs) have introduced high-margin, sensor-ready actuator platforms, embedding switching costs and capturing early-cycle demand. As ASIL compliance and fluid disposal standards shape aftermarket offerings, industrial validation, workforce familiarity, and fleet integration reinforce structural growth potential for this high-tech segment.

Material Insights

Steel/Metallic materials are expected to lead the market, accounting for approximately 82% share in 2026, underpinned by the entrenched role of steel as the backbone material across passenger vehicles, commercial fleets, and industrial drivetrains. Adoption remains anchored by superior mechanical toughness, thermal dissipation, machinability for aftermarket fitments, and cost-to-performance efficiency, with providers prioritizing standardized supply chains, workflow integration, and reliability in high-volume replacement scenarios. Ongoing platform evolution, including high-nitrogen alloys, advanced induction hardening, and anti-friction coatings, continues to reinforce replacement cycles and durability under extreme operational stresses. The Timken Company, NSK Ltd., Exedy Corporation, and JTEKT (Koyo) and their proprietary bearing and friction material portfolios further embed ecosystem lock-in. This combination of mature infrastructure, recyclability, and scalable manufacturing sustains the segment’s dominance while meeting evolving sustainability and performance requirements across global aftermarket networks.

Ceramic/Composite materials are expected to be the fastest-growing segment, driven by the extreme performance demands of high-RPM electric motors, turbocharged engines, and high-torque drivetrains across passenger, commercial, and specialty vehicles. Growth is being catalyzed by hybrid bearings, silicon nitride balls, carbon-ceramic clutch discs, and ceramic thermal-spray coatings, which materially improve friction reduction, thermal stability, weight savings, and electrical insulation for advanced powertrains. Accelerating adoption is supported by predictive maintenance integration, additive manufacturing of complex ceramic cores, and compatibility with high-speed, high-voltage applications, lowering operational risk for first-time adopters. SKF, Brembo (SGL Carbon), Exedy (Cerametallic Series), and CeramTec and their high-performance product lines capture early-cycle demand. As copper-free friction mandates and EV drivetrain standards influence component selection, industrial validation, material performance, and structural reliability reinforce the segment’s rapid growth trajectory.

Regional Insights

Asia Pacific Automotive Bearing and Clutch Component Aftermarket Market Trends

Asia Pacific is expected to remain the leading and fastest-growing region in the global automotive bearing and clutch component aftermarket, approximating 42% of global share in 2026, driven by its unmatched manufacturing capacity, expanding vehicle population, and rapid infrastructure development. Adoption is reinforced by the integration of high-performance bearings for electrified drivetrains, lightweight materials for fuel efficiency, and digital distribution platforms supporting structured aftermarket networks. Leading vendors, including Robert Bosch GmbH, Denso Corporation, ZF Friedrichshafen AG, Aisin Corporation, NSK Ltd., NTN Corporation, and JTEKT Corporation, maintain a strong regional presence, ensuring deep enterprise penetration, consistent part availability, and alignment with emission compliance, fleet maintenance, and technological modernization across the region.

India is positioned to anchor APAC’s aftermarket momentum, shaping regional growth through high vehicle population density, accelerating fleet age, and robust industrial expansion. Government initiatives such as “Make in India” and highway infrastructure programs are expected to stimulate local manufacturing, aftermarket part adoption, and structured distribution networks. Regulatory enforcement on emissions and safety compliance is anticipated to drive demand for durable, high-performance bearings and clutch kits, while regional vendor strategies focus on electrification-ready components, sensor-integrated bearings, and cost-efficient modular clutch systems. Forward-looking trends suggest India will continue to reinforce APAC’s scale-driven growth, supporting both legacy ICE and emerging EV aftermarket needs while maintaining technological competitiveness and regional supply chain resilience.

North America Automotive Bearing and Clutch Component Aftermarket Market Trends

North America is expected to remain a developed and structurally stable market for automotive bearings and clutch components, supported by its entrenched Independent Aftermarket (IAM) ecosystem and a high-average vehicle age that sustains predictable replacement cycles. Supply chains are increasingly anchored by nearshoring strategies under USMCA, ensuring continuity for regional manufacturers and distributors such as The Timken Company and SKF. E-commerce adoption and digital catalog precision further strengthen the aftermarket, enabling fitment-verified offerings for both professional installers and DIY consumers, while predictive maintenance technologies are gradually being integrated into fleet management, reinforcing the resilience of replacement demand and operational reliability across passenger and light commercial vehicles.

The U.S. is positioned to anchor North America’s market stability, driving regional aftermarket dynamics through professional installer adoption, fleet telematics integration, and a strong alignment of industrial capabilities with regulatory frameworks. USMCA rules continue to influence production and sourcing decisions, encouraging domestic manufacturing of bearings and clutch components and supporting enterprise-level distribution hubs. Forward-looking adoption of AI-enabled diagnostics, e-commerce platforms, and predictive maintenance for fleet operators is anticipated to maintain steady aftermarket activity while reinforcing the U.S.’ role as the structural benchmark for North American automotive bearing and clutch operations.

Europe Automotive Bearing and Clutch Component Aftermarket Market Trends

Europe is expected to remain a mature and structurally steady market for automotive bearings and clutch components, anchored by its sophisticated vehicle parc and highly regulated aftermarket environment. Market stability is reinforced by widespread adoption of manual and dual-clutch transmissions, strong remanufacturing networks, and integration of smart sensor technology into bearings and actuators. Germany, France, and the U.K. drive regional demand through consistent replacement cycles and high fleet utilization, while circular economy initiatives and electrification are gradually shifting aftermarket focus toward high-speed e-motor bearings and certified low-emission components. Leading vendors such as Schaeffler AG, ZF Friedrichshafen AG, Valeo, and SKF Group maintain deep enterprise penetration and platform leadership, ensuring continuity of supply, high-quality standards, and alignment with evolving industrial and regulatory expectations.

Germany is positioned to anchor Europe’s market dynamics, sustaining regional aftermarket momentum through its dominant sub-market share and advanced industrial ecosystem. Regulatory frameworks, including Euro 7 and formalized EU data-sharing mandates, are expected to shape component specifications, durability requirements, and independent workshop access to diagnostics. Forward-looking adoption of predictive maintenance technologies, sensor integration, and dual-clutch aftermarket solutions is anticipated to reinforce Germany’s role as the structural benchmark, maintaining Europe’s mature aftermarket stability while supporting incremental innovation across high-value vehicle segments.

Competitive Landscape

The global automotive bearing and clutch component aftermarket market is moderately fragmented, with leadership concentrated among global suppliers such as Robert Bosch GmbH, Denso Corporation, ZF Friedrichshafen AG, Aisin Corporation, NSK Ltd., NTN Corporation, and JTEKT Corporation. These leaders exert significant functional influence through integrated drivetrain solutions, high-performance bearing technology, and advanced clutch system components, shaping procurement standards and aftermarket quality benchmarks.

Competitive positioning varies across horizontal and vertical segments, with firms differentiating through electrification-ready components, sensor-integrated bearings, lightweight materials, and regional specialization in high-volume manufacturing hubs. Industry dynamics reflect ongoing consolidation in high-performance and commercial vehicle segments, expansion of digital distribution platforms, modular product integration, and service-led models that reinforce fleet maintenance contracts and recurring replacement cycles. Forward-looking trends indicate that global vendors will continue to refine technological footprints, optimize platform interoperability, and respond to regulatory mandates, sustaining their centrality in an evolving aftermarket ecosystem.

Key Industry Highlights:

- In February 2026, ZF Aftermarket introduced new SACHS agricultural tractor clutch components in India. Improves local availability of OE-quality parts for demanding agricultural use in India/IMEA.

- In January 2026, EXEDY group implemented a new corporate structure and leadership. It facilitates global decision-making and investment in future mobility. These changes are part of their "REVOLUTION 2026" medium-term management plan, which focuses on investing in new business creation, specifically future mobility (including Electric Vehicles) due to the shrinking Automatic Transmission (AT) business.

- In October 2025, SKF India completed the demerger of its industrial business from automotive. This demerger allowed the automotive entity to focus exclusively on mobility solutions and high-growth aftermarket segments.

Companies Covered in Automotive Bearing and Clutch Component Aftermarket Market

- Schaeffler AG

- ZF Friedrichshafen AG

- Valeo SA

- SKF Group

- Exedy Corporation

- Aisin Corporation

- The Timken Company

- NSK Ltd.

- NTN Corporation

- JTEKT Corporation

- Eaton Corporation plc

- BorgWarner Inc.

- PHC (PHC Valeo)

- NRB Bearings Ltd.

- Dana Incorporated

- RBC Bearings

Frequently Asked Questions

The global automotive bearing and clutch component aftermarket market is projected to be valued at US$5.8 billion in 2026 and is expected to reach US$8.1 billion by 2033, driven by aging vehicle fleets worldwide, increasing vehicle kilometers traveled, and the consequent demand for reliable replacement parts.

Older vehicles exhibit accelerated wear on drivetrain and rotational components, creating recurring and predictable replacement cycles. This structural trend is amplified in mature markets where safety regulations mandate timely maintenance, embedding replacement bearings and clutches into standard service workflows and sustaining aftermarket procurement.

The automotive bearing and clutch component aftermarket market is forecast to grow at a CAGR of 4.9% from 2026 to 2033, reflecting a steady demand from the expanding vehicle parc and the increasing complexity of modern drivetrain systems.

Asia Pacific is both the leading and fastest-growing regional market, accounting for approximately 42% share, underpinned by its large vehicle population, expanding manufacturing base, and strong independent aftermarket networks. Southeast Asia, in particular, is experiencing rapid growth due to increasing vehicle ownership and last-mile logistics activity.

The automotive bearing and clutch component aftermarket market is moderately fragmented, with leadership concentrated among global suppliers such as Schaeffler AG (LuK), ZF Friedrichshafen AG (Sachs), Valeo SA, Aisin Corporation, and SKF Group. These firms compete through integrated drivetrain solutions, high-performance bearing technology, and modular clutch kits, maintaining deep enterprise penetration across both independent aftermarket (IAM) and original equipment service (OES) channels.