- Semiconductor Materials & Components

- Automation-as-a-Service Market

Automation-as-a-Service Market Size, Share, and Growth Forecast 2026 – 2033

Automation-as-a-Service Market by Component (Solutions, Services), Business Function (Information Technology, Finance, Sales and Marketing), Vertical (Industrial, BFSI, Retail and Consumer Goods), and Regional Analysis, 2026 – 2033

Automation-as-a-Service Market Size and Trends Analysis

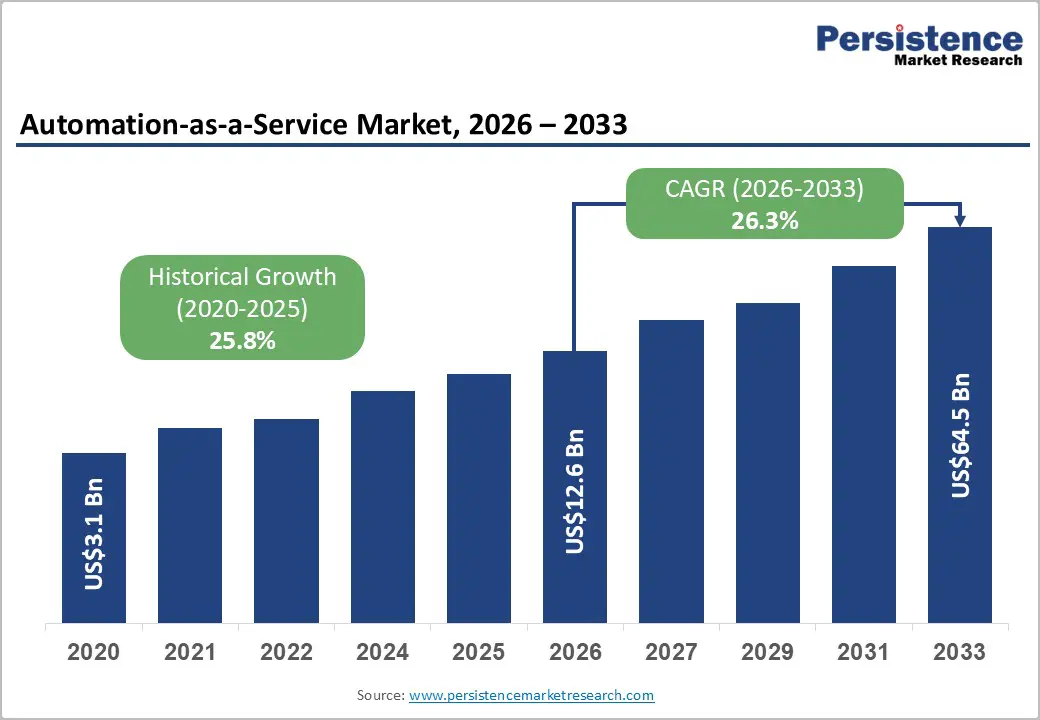

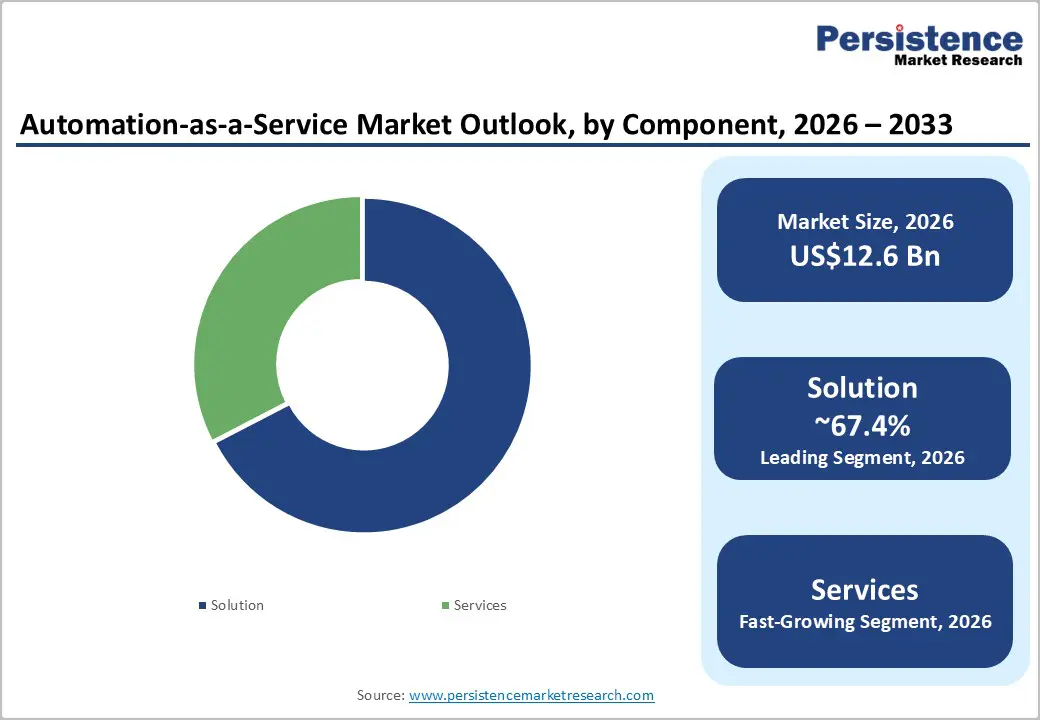

The global automation-as-a-service market size is likely to be valued at US$12.6 billion in 2026 and is expected to reach US$64.5 billion by 2033, growing at a CAGR of 26.3% during the forecast period from 2026 to 2033, driven by the ongoing integration of AI-supported automation across enterprise workflows and the rising shift toward cloud-based, subscription-driven IT models. Increasing adoption among mid-sized enterprises is further pushing market expansion.

Key Industry Highlights:

- New Launch: In May 2026, at its annual Knowledge 2026 event, ServiceNow announced a major expansion of its Autonomous Workforce, launching new AI specialists for IT, CRM, employee services, and security and risk. Each AI specialist is built to autonomously resolve cases, contain threats, handle high-volume employee requests, and escalate complex issues to humans.

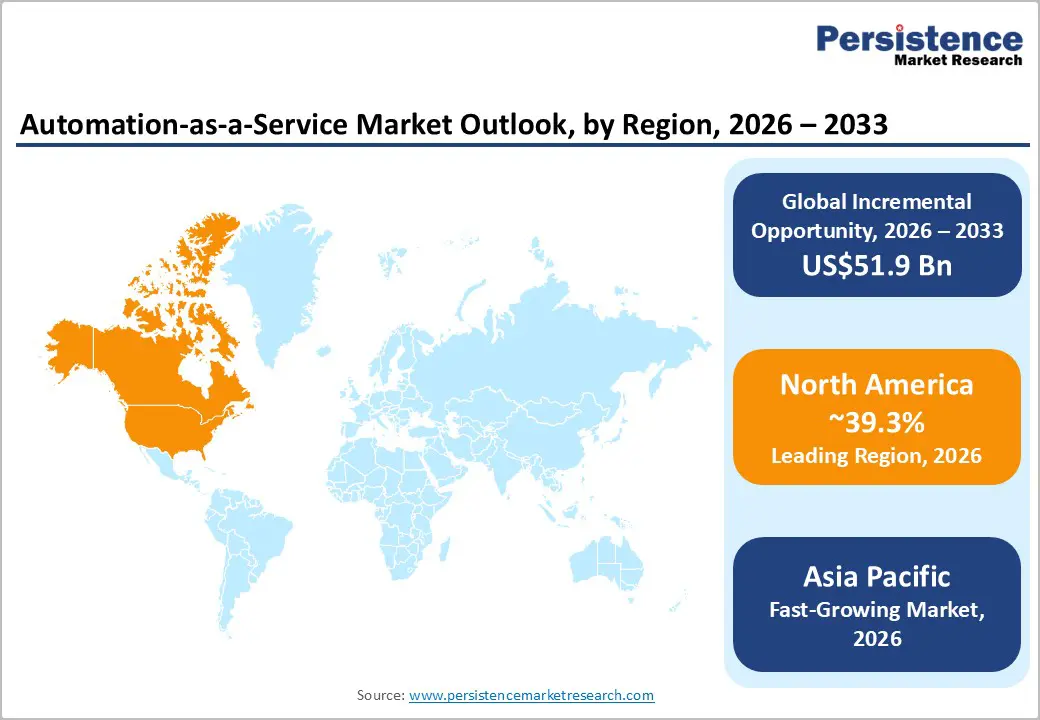

- Leading Region: North America, with about a 39.3% share in 2026, due to early adoption of AI-driven automation and the presence of key vendors such as Microsoft.

- Fast-growing Region: Asia Pacific, owing to rapid digital transformation and government-backed automation initiatives.

- Leading Component: Solutions, approximately 67.4% share in 2026, as enterprises prefer integrated platforms that combine RPA, AI, and analytics in one system.

- Dominant Vertical: Telecom and IT, nearly 25.7% in 2026, due to their heavy reliance on high-volume and repetitive digital processes such as network management.

DRO Analysis

Driver - Increasing Demand for Cost Savings and Efficiency

Automating rule-based processes removes a key source of operational drag, i.e., human error on high-volume and repetitive tasks. When bots handle these tasks, turnaround times drop sharply and processing quality stays consistent. A 2024 survey found that 52% of financial services firms saved at least US$100,000 annually through automation. The U.S. federal government has seen similar gains.

Government agencies are using Robotic Process Automation (RPA) to streamline day-to-day operations, freeing employees' time for work that demands close attention. Beyond labor savings, organizations using RPA tools report 3x to 10x Return on Investment (ROI) in the first year, with 80% of institutions confirming reduced manual workloads and error rates. These are not just cost reductions, but they represent a steady shift in how work gets done.

Rise of Industry-Specific Bot Marketplaces

Purpose-built automation marketplaces are changing how enterprises discover and deploy bots. Rather than building agents in-house from scratch, businesses can now browse, buy, and activate pre-validated agents customized to their industry, much like downloading an app. In July 2025, AWS launched a dedicated AI Agents and Tools category within AWS Marketplace, debuting with over 900 agents from providers, including Anthropic and Salesforce. The same month, Automation Anywhere made its AI agents available in that category, allowing customers to discover, buy, and deploy agents directly through their AWS accounts.

Two months later, Oracle launched the Fusion Applications AI Agent Marketplace in October 2025, featuring over 100 validated agents from partners, including Accenture, Deloitte, IBM, Box, and Stripe. All are deployable with a single click inside Oracle's finance, HR, supply chain, and CRM applications. These storefronts are cutting deployment time and reducing procurement friction, making specialized automation accessible to enterprises of all sizes.

Restraint - Subscription Costs That Gradually Surge

AaaS platforms often appear cost-effective during initial deployment, but expenses can rise significantly as automation adoption expands. Costs typically increase through user-based pricing models, workflow execution fees, API call charges, environment-specific expenses for development, testing, staging, and production, as well as overage fees and premium feature add-ons. Additional expenditures may arise from integration requirements, including connector licenses, custom API development, and middleware subscriptions. These costs are frequently overlooked during vendor demonstrations, leading organizations to underestimate the total cost of ownership.

Automation Total Cost of Ownership (TCO) includes not just the purchase cost, but also maintenance, spare parts, engineering, and utility costs. This full picture is what ROI alone does not capture. Organizations that constantly expand without modeling long-term consumption patterns often find that their AaaS spend exceeds what an in-house solution would have cost over a three-to-five-year horizon. Without a proper TCO review before signing multi-year contracts, businesses can lock themselves into pricing structures that punish growth.

Opportunity - AI-Backed Agents to Take Over Complex Workflows

Agentic automation is moving beyond scripted bots toward systems that can reason, decide, and adapt. In April 2025, for instance, UiPath launched its next-generation platform for agentic automation, designed to unify AI agents, robots, and people on a single intelligent system, with open orchestration, scalability, and compliance at its core. The platform's Maestro layer is central to this.

In insurance claims, Maestro orchestrates robots and AI agents to validate claim data, check policy coverage, initiate payments for straightforward cases, and escalate ambiguous ones to human review- all with full auditability. Governance is built in by design. UiPath also became one of the first enterprise agentic automation platforms to achieve ISO/IEC 42001 certification. It is the world's first global standard for responsible AI governance. For businesses dealing with regulated processes, this level of auditable control is a meaningful shift from legacy automation.

Merging Multiple Technologies for End-to-End Automation

Hyperautomation moves past single-task bots to connect entire business workflows. It integrates AI, RPA, and advanced technologies to automate complex processes end-to-end, enabling smarter systems that adapt using data-driven insights. Hyperautomation has recently seen a resurgence in interest since the rise of generative AI and is now a staple discipline for various large enterprises. It is augmented by the mandate for operational excellence and resilience.

Supply chains are an early proving ground. Chief supply chain officers are now moving toward building multi-year hyperautomation strategies, with transactional processes such as order-to-cash and complex decisions, including supply chain planning, cited as leading use cases. Unlike siloed RPA deployments, hyperautomation creates feedback loops, where process mining identifies bottlenecks, and AI continuously improves how work flows through the system.

Category-wise Analysis

Component Insights

Solutions are predicted to lead with a share of approximately 67.4% in 2026, as enterprises prefer ready-to-deploy automation platforms instead of building tools from scratch. These platforms combine RPA, AI, analytics, and workflow orchestration in one system, which reduces integration effort. For example, Microsoft has embedded automation into its Power Platform, allowing companies to automate tasks directly in tools such as Excel and Teams. This tight integration increases adoption.

Services are estimated to be the fastest-growing segment over the forecast period, as several companies lack in-house expertise to implement automation. Deploying automation across departments requires process redesign, integration, and change management. This creates demand for consulting and managed services. A 2023 report by the World Economic Forum noted that skill gaps remain a key barrier to automation adoption, especially in emerging markets.

Vertical Insights

Telecom and IT are anticipated to dominate with a share of nearly 25.7% in 2026, as they handle massive volumes of repetitive digital processes. These include network monitoring, customer onboarding, billing, and ticket resolution. Automation helps reduce manual workload and improve response time. For example, AT&T uses automation to manage network operations and detect faults in real time. The sector is also highly data-driven. Automation tools can analyze logs, predict failures, and trigger actions without human input.

The BFSI segment is expected to remain in the second position in 2026, as it deals with high transaction volumes and strict regulatory requirements. Automation helps in processing payments, loan approvals, and compliance checks faster and with fewer errors. For instance, the Reserve Bank of India has encouraged banks to adopt digital and automated systems to improve efficiency and transparency in financial operations. Fraud detection is another key driver. Automation tools use AI to monitor transactions and flag suspicious activity in real time. A 2024 report by the Bank for International Settlements highlighted that AI-based monitoring systems can significantly reduce financial fraud losses. This makes automation important for banks and insurers.

Regional Insights

North America Automation-as-a-Service Market Trends

North America is predicted to dominate in 2026 with a share of approximately 39.3%, as it has early adoption of automation technologies and superior enterprise spending power. Several global automation vendors such as UiPath and Automation Anywhere are headquartered here, which speeds up innovation and deployment. The region also benefits from a well-established cloud infrastructure. According to a 2024 report by the National Institute of Standards and Technology, U.S. enterprises are constantly shifting to cloud-native systems, which directly supports automation adoption. Large firms in finance, healthcare, and retail are integrating AI-backed automation into daily operations, making the region dominant.

U.S. Automation-as-a-Service Market Trends

A share of nearly 64.3% is expected to be held by the U.S. in 2026. Companies in the country are moving from basic RPA to AI-led automation. A 2024 whitepaper states that over 60% of U.S. enterprises are already piloting or extending AI automation use cases. The federal government is also fueling adoption. The White House AI Executive Order (2023) encourages responsible AI deployment across industries. This has led to increased automation use in public services, defense, and healthcare systems. Private firms such as JPMorgan Chase are using automation for fraud detection and contract analysis, showing superior real-world adoption.

Asia Pacific Automation-as-a-Service Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026, with a share of nearly 30.2%, owing to speedy digital transformation and large-scale enterprise digitization. Countries are investing heavily in automation to improve productivity and reduce labor dependency. A 2024 report by the Asian Development Bank shows that digital technologies, including automation, are key to improving industrial efficiency in Asia Pacific. Another factor is cost pressure. Various companies in manufacturing and IT services are adopting automation to stay competitive globally. Governments are also supporting this shift through digital economy programs, which are fueling adoption across sectors.

China Automation-as-a-Service Market Trends

China will likely lead Asia Pacific in 2026 with a share of around 32.4%. It is focusing on industrial automation and AI integration. The government’s Made in China 2025 initiative promotes smart manufacturing and automation. This is pushing companies to adopt advanced automation tools across factories and supply chains. According to a report from the Ministry of Industry and Information Technology, local manufacturers are increasing the use of industrial robots and AI systems to improve efficiency. Tech firms such as Alibaba Cloud are also providing automation platforms, which are strengthening the market outlook.

India Automation-as-a-Service Market Trends

In 2026, India is projected to account for a share of approximately 14.7%, backed by its large IT services sector. Automation is widely used in business process outsourcing and IT operations. Companies are adopting automation to handle repetitive tasks and improve service delivery. Government initiatives such as Digital India are also supporting adoption. According to the Ministry of Electronics and Information Technology, digital transformation projects in public services are increasing the use of automation tools. Firms such as Tata Consultancy Services are actively deploying automation solutions for global clients, which is boosting market growth.

Europe Automation-as-a-Service Market Trends

Europe will likely see decent growth over the forecast period, with a share of nearly 16.5% in 2026, owing to its increased focus on regulation and quality. Companies are adopting automation carefully to meet compliance standards such as GDPR. This slows speedy adoption but ensures long-term stability. The European Union is also promoting digital transformation. A 2024 update from the European Commission highlights investments in AI and automation under its Digital Europe Program. This is encouraging businesses to adopt automation in a structured way, supporting steady growth.

Germany Automation-as-a-Service Market Trends

Germany will likely register a substantial share of approximately 36.7% in 2026, spurred by its well-established manufacturing base. The Industry 4.0 initiative promotes smart factories and connected systems. This fosters high demand for automation technologies. According to the Federal Ministry for Economic Affairs and Climate Action, domestic industries are investing in digital production tools to improve efficiency and reduce downtime. Companies are integrating automation with IoT and AI, which supports long-term growth.

U.K. Automation-as-a-Service Market Trends

A share of around 25.8% is predicted to be held by the U.K. in 2026, owing to rising adoption in financial services and public sector projects. Automation is widely used in banking for compliance, reporting, and fraud detection. The government is also supporting AI and automation. A 2023 policy paper from the U.K. Government outlines plans to extend AI adoption across industries. This is encouraging businesses to invest in automation tools, leading to consistent growth in the market.

Competitive Landscape

The global automation-as-a-service market is moderately fragmented with the presence of pure-play automation vendors, cloud hyperscalers, enterprise software companies, IT service providers, and emerging AI-native automation firms. While leading players such as UiPath, Microsoft, Automation Anywhere, IBM, and Google Cloud hold significant positions, various niche vendors continue to gain traction through industry-specific solutions and AI-supported automation portfolios.

Competition is no longer centered solely on RPA. Vendors are increasingly differentiating themselves through end-to-end automation ecosystems that combine process mining, intelligent document processing, workflow orchestration, conversational AI, and autonomous AI agents. Hence, companies are moving beyond simple task automation toward enterprise-wide business transformation platforms.

Key Industry Developments:

- In June 2026, IBM and Google Cloud announced a strategic partnership to jointly extend enterprise AI and automation. The two companies launched a new Google Cloud Practice combining IBM Consulting's industry expertise and its AI-backed IBM Consulting Advantage platform with Google Cloud's Gemini Enterprise Agent Platform.

- In May 2026, ServiceNow and Lenovo announced a collaboration to combine AI-native workflow automation with device intelligence, targeting end-to-end automation across the full IT device lifecycle. The companies indicated the integrated solution is expected to deliver around 30% lower IT support costs for enterprises managing large device fleets.

- In May 2026, UiPath announced the release of on-premises agentic AI capabilities within its Automation Suite, targeting government agencies and regulated industries. The update was designed to address strict data sovereignty and compliance requirements, allowing agencies to deploy agentic AI in their own infrastructure using cloud-hosted or self-hosted large language models.

Companies Covered in Automation-as-a-Service Market

- Automation Anywhere Inc.

- Blue Prism Limited

- HCL Technologies Limited

- Hewlett Packard Enterprise Development LP

- Microsoft Corporation

- International Business Machines Corporation (IBM)

- Kofax Inc.

- NICE

- Pegasystems Inc.

- UiPath

- Others

Frequently Asked Questions

The global automation-as-a-service market is projected to be valued at US$12.6 billion in 2026.

The automation-as-a-service market is expected to reach US$64.5 billion by 2033.

Key market trends include the rise of AI-powered automation and the shift toward hyperautomation platforms.

Solutions are expected to be the leading component with a share of nearly 67.4% in 2026, as they provide ready-to-deploy tools with built-in governance and compliance features.

The automation-as-a-service market is expected to grow at a CAGR of 26.3% from 2026 to 2033.

Automation Anywhere Inc., Blue Prism Limited, and HCL Technologies Limited are a few key market players.