- Sensors & Controls

- Articulated Robot Market

Articulated Robot Market Size, Share, and Growth Forecast 2026 - 2033

Articulated Robot Market by Payload Capacity (Up to 16 Kg, 16 Kg – 60 Kg, 60 Kg – 225 Kg, More than 225 Kg), by Robot Type (4-Axis or Less, 5-Axis, 6-Axis or More), by Function Type (Handling, Welding, Assembly, Dispensing, Processing, Others), Industry (Automotive, Electrical & Electronics, Metal & Machinery, Chemicals, Rubber & Plastics, Food & Beverages, Pharmaceuticals & Cosmetics, Precision Engineering & Optics, Others), and Regional Analysis, 2026 - 2033

Global Articulated Robot Market Size and Trend Analysis

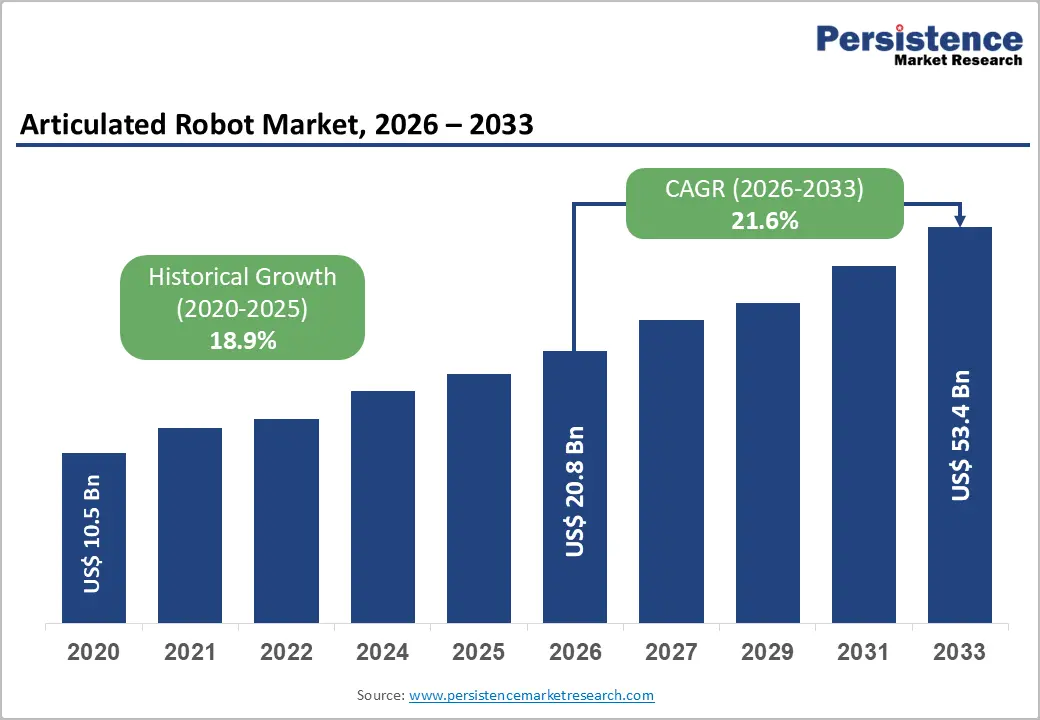

The global articulated robot market size is expected to be valued at US$ 20.8 billion in 2026 and projected to reach US$ 53.4 billion by 2033, growing at a CAGR of 14.4% between 2026 and 2033. The market is experiencing accelerated expansion as manufacturers worldwide deploy multi-axis robotic arms to address persistent labor shortages, rising wage pressures, and production flexibility.

According to the International Federation of Robotics (IFR), the global average robot density reached 162 units per 10,000 employees in the manufacturing sector in 2023. Growing adoption across automotive electrification programs, electronics miniaturization, and food packaging automation, combined with falling unit costs and improved AI-enabled vision systems, is driving sustained capital investment in articulated robotic solutions across both developed and emerging economies.

Key Industry Highlights:

- Leading Region: Asia Pacific dominates the global articulated robot market with a 47.5% share in 2025, anchored by China's EV manufacturing, electronics ecosystems, and Made in China 2025 policy-led automation incentives.

- Fast-Growing Market: Asia Pacific is also the fastest-growing region, with India and Southeast Asia accelerating sharply, supported by PLI schemes, supply-chain diversification, and rising robot density across automotive and electronics clusters.

- Dominant Payload Capacity: The Up to 16 Kg payload segment leads with 40% share in 2025, reflecting widespread deployment in electronics assembly, machine tending, and small-parts handling across global automotive and consumer electronics manufacturing.

- Fastest Growing Payload Capacity: The 60 Kg – 225 Kg payload class is the fastest-growing segment with 21% share in 2025, propelled by mid-weight automotive handling, EV battery module assembly, and rising palletizing automation in logistics.

- Key Opportunity: AI-enabled vision and adaptive control unlock significant opportunities, as articulated robots evolve into autonomous bin-pickers and defect inspectors, supported by CHIPS Act, K-Robot, and Made in China 2025 funding.

Market Dynamics

Drivers - Accelerating Automotive Electrification and EV Manufacturing Investments

The global pivot toward electric vehicles is acting as a powerful tailwind for articulated robot demand. According to the International Energy Agency (IEA), global EV sales surpassed 17 million units in 2024, representing more than 20% of total new car sales worldwide.

EV battery pack assembly, e-motor production, and lightweight body welding require high-precision multi-axis robotic systems with repeatability under 0.05 mm. Major OEMs, including Tesla, BYD, Volkswagen, and Hyundai, are investing heavily in greenfield gigafactories where articulated robots dominate spot welding, sealing, and battery module handling lines, sustaining double-digit demand growth across the global automotive robot ecosystem.

Labor Shortages and Rising Manufacturing Wage Inflation

Persistent workforce gaps in industrial economies are compelling manufacturers to substitute manual labor with articulated robotic systems. The U.S. Bureau of Labor Statistics reported approximately 622,000 unfilled manufacturing job openings in early 2024, while Eurostat recorded manufacturing labor cost growth of 5.1% year-on-year in the EU during 2024.

In Japan, the Ministry of Health, Labour and Welfare highlights that the working-age population is projected to shrink by nearly 20% by 2040. These structural shortages, coupled with payback periods for industrial robots now falling below 2 years for many applications, are accelerating articulated robot installations across high-mix, low-volume production environments.

Restraints - High Initial Capital Outlay and Integration Complexity

The total cost of ownership for an articulated robotic cell, including end-effectors, safety systems, vision modules, and PLC integration, typically ranges between US$ 80,000 and US$ 250,000 per workstation, a significant barrier for small and medium-sized manufacturers.

According to the U.S. Census Bureau, only about 15% of manufacturers with fewer than 100 employees have deployed industrial robots. System integration timelines often exceed 6–9 months, creating productivity disruptions and demanding specialized engineering talent that remains in short supply across emerging markets, slowing adoption.

Cybersecurity Vulnerabilities in Networked Robotic Systems

The proliferation of Industry 4.0 connectivity has exposed articulated robots to mounting cybersecurity threats. The European Union Agency for Cybersecurity (ENISA) reported a 52% rise in cyberattacks targeting industrial control systems between 2022 and 2024. Compromised robotic controllers can cause production halts, intellectual property theft, and physical safety hazards.

Compliance burdens under frameworks such as the EU Cyber Resilience Act and NIST SP 800-82 are increasing engineering overhead, deterring some manufacturers from full-scale robotic deployment, particularly in sectors with sensitive intellectual property like semiconductors and pharmaceuticals.

Opportunities - Expansion of Collaborative and Mid-Payload Robots in Electronics and Logistics

The fastest-expanding opportunity lies in mid-payload articulated robots in the 60 Kg – 225 Kg range, increasingly deployed alongside humans in semi-structured environments. According to the International Federation of Robotics, collaborative robot installations grew by approximately 31% in 2023, outpacing the broader industrial robot market.

The boom in lithium-ion battery assembly, semiconductor back-end packaging, and e-commerce fulfillment is creating sustained demand for flexible 6-axis arms with integrated force-torque sensing. Companies such as FANUC, ABB, and Universal Robots are launching cobot-style articulated platforms with payloads up to 30 Kg, opening previously untapped customer segments, including contract electronics manufacturers and third-party logistics providers in Southeast Asia and Eastern Europe.

AI-Driven Vision Systems and Government Automation Incentives

Artificial intelligence integration is transforming articulated robots from rigid pre-programmed machines into adaptive systems capable of bin-picking, defect detection, and autonomous path planning. The Government of China, under its Made in China 2025 and 14th Five-Year Plan, has earmarked subsidies exceeding US$ 1.4 billion for industrial robot adoption through 2025.

South Korea's K-Robot Economy Plan targets 1 million robot installations by 2030, while the U.S. CHIPS and Science Act is channeling capital into highly automated semiconductor fabs. These public-policy tailwinds, combined with rapid advancements in vision-language models for robotics, are unlocking new applications in pharmaceuticals, precision optics, and food handling.

Category-wise Analysis

Payload Capacity Insights

Upto 16 Kg segment leads the global articulated robot market, accounting for approximately 40% share in 2025. Its dominance stems from widespread deployment in electronics assembly, small-parts handling, machine tending, and light material handling tasks where speed, footprint efficiency, and energy consumption matter more than brute force.

According to the International Federation of Robotics, electronics manufacturing accounted for nearly 27% of global industrial robot installations in 2023, with the majority requiring sub-16 Kg payload classes. The proliferation of consumer electronics, EV battery cell assembly, and medical device production in countries like China, Vietnam, and Mexico continues to reinforce demand. The 60 Kg – 225 Kg segment, holding around 21% share, is the fastest-growing category, propelled by mid-weight automotive component handling and palletizing.

Robot Type Insights

The 6-Axis or More segment commands the leading position in the articulated robot market, capturing approximately 62% market share in 2025. Six-axis architectures provide full spatial dexterity, enabling complex motion paths required for arc welding, spray painting, sealing, and intricate assembly. According to data from the International Federation of Robotics, articulated 6-axis robots represent the largest installed base in automotive paint shops and body-in-white lines globally.

The segment benefits from a mature ecosystem of programming tools, simulation software, and standardized end-effectors offered by major suppliers such as FANUC, KUKA, Yaskawa, and ABB. Continued innovation in lightweight composite arm structures, energy-efficient servo drives, and integrated AI controllers is expected to sustain its leadership through 2033, especially as factories pursue greater process flexibility.

Function Type Insights

The handling segment leads to the articulated robot market by function type, accounting for approximately 38% share in 2025. Material handling encompasses pick-and-place operations, machine loading and unloading, palletizing, depalletizing, and packaging tasks that span virtually every manufacturing sector. The International Federation of Robotics reports that handling applications consistently represents the largest single application category in annual industrial robot installations, with over 200,000 units shipped globally for these tasks in 2023.

Surging e-commerce volumes, warehouse automation by retailers such as Amazon and JD.com, and the growing standardization of robotic palletizing in food and beverage plants continue to support its leadership. Although welding accounts for fewer units, it remains a high-value segment, driven by automotive and shipbuilding demand across East Asia.

Industry Insights

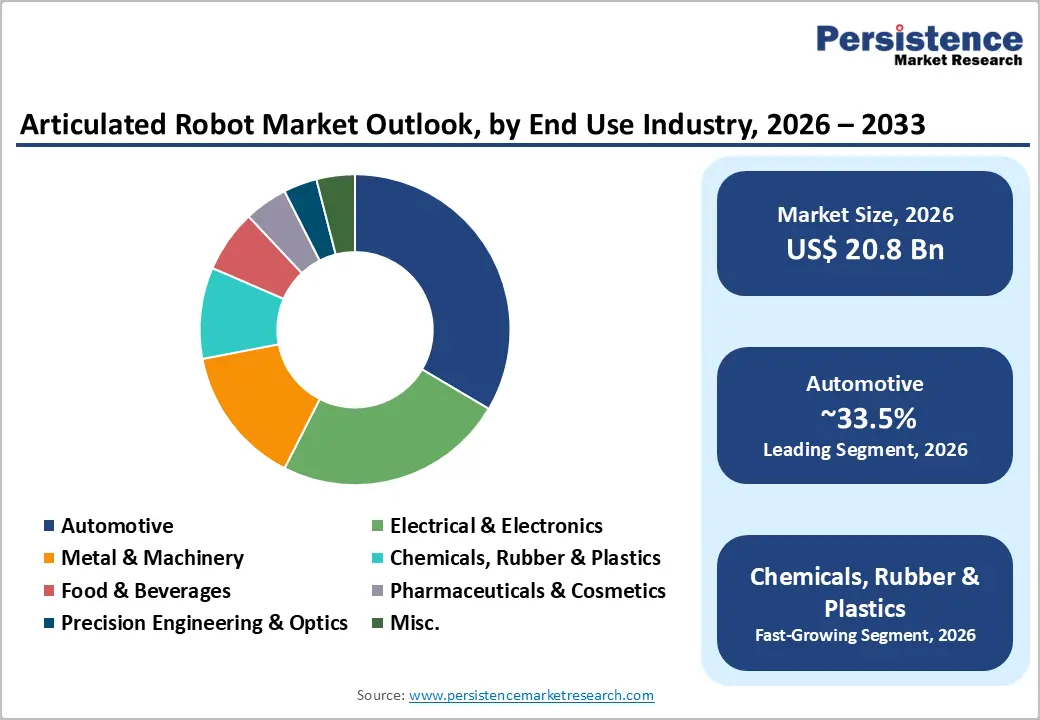

The Automotive sector remains the dominant end-use industry for articulated robots, capturing roughly 31% market share in 2025. Automotive manufacturing has historically anchored industrial robotics, leveraging multi-axis arms for spot welding, body assembly, painting, and powertrain machining. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached approximately 75.5 million units in 2024, with strong manufacturing concentration in China, Japan, Germany, and the United States.

The accelerating shift toward electric vehicles is amplifying robotic intensity per vehicle, as battery pack assembly, e-axle production, and gigacasting cells require even higher levels of automation than internal combustion engine plants. Continued capacity expansion by Toyota, BYD, Volkswagen, and Hyundai-Kia ensures that automotive remains the cornerstone of articulated robot demand.

Regional Insights

North America Articulated Robot Market Trends and Insights

North America holds a share of 20.0% in 2025, supported by reshoring initiatives, semiconductor fab investments under the CHIPS and Science Act, and EV manufacturing expansion. The region is witnessing strong demand for AI-enabled articulated robots in automotive, aerospace, and warehouse automation. Persistent labor shortages and elevated manufacturing wages continue to incentivize capital substitution toward robotic systems, while Mexico is emerging as a high-growth nearshoring hub for North American supply chains.

U.S. Articulated Robot Market Size

The U.S. articulated robot market value stood at US$ 3,075.8 million in 2025, driven by aggressive EV gigafactory rollouts from Tesla, Ford, and General Motors, alongside semiconductor fab construction by Intel, TSMC Arizona, and Micron. According to the U.S. Bureau of Labor Statistics, manufacturing job openings exceeded 600,000 in 2024, accelerating robotic deployment across automotive, food processing, and logistics distribution centers concentrated in Michigan, Texas, and the Midwest industrial corridor.

Europe Articulated Robot Market Trends and Insights

Europe holds a share of 21.5% in 2025, anchored by Germany's automotive engineering ecosystem, Italy's machinery cluster, and rising defense and aerospace automation across France and the U.K. The European Commission's push for digital and green transition under the EU Industrial Strategy is accelerating robotic adoption, particularly in mid-sized manufacturers. Rising energy costs and the need to maintain global competitiveness against Asian rivals are also driving high-mix, flexible automation investments.

Germany Articulated Robot Market Size

Germany's articulated robot market value reached US$ 1,232.6 Million in 2025, driven by deep automation requirements in premium automotive manufacturing by Volkswagen, BMW, Mercedes-Benz, and Porsche. According to the Verband Deutscher Maschinen- und Anlagenbau (VDMA), Germany hosts more than 270,000 mechanical engineering employees engaged in robotics and automation. The country's transition toward EV production, combined with home-grown technology leaders such as KUKA, sustains its position as Europe's leading articulated robot consumer.

U.K. Articulated Robot Market Size

The U.K. articulated robot market is benefiting from automation incentives under the UK Advanced Manufacturing Plan, with rising deployments in automotive, food processing, and pharmaceuticals. According to the Office for National Statistics, U.K. manufacturing output grew modestly in 2024, with companies including Jaguar Land Rover and Nissan Sunderland investing in EV-ready robotic body shops. Robotics adoption in life sciences and contract food manufacturing also continues to expand steadily.

France Articulated Robot Market Size

France's articulated robot market value reached US$ 469.6 Million in 2025, driven by aerospace robotization at Airbus, expanding EV production by Stellantis and Renault, and government support under the France 2030 plan, which earmarked over €54 billion for advanced manufacturing and green industries. Defense contractors including Thales and Dassault are also incorporating articulated robotics into composite layup and aerostructure assembly cells.

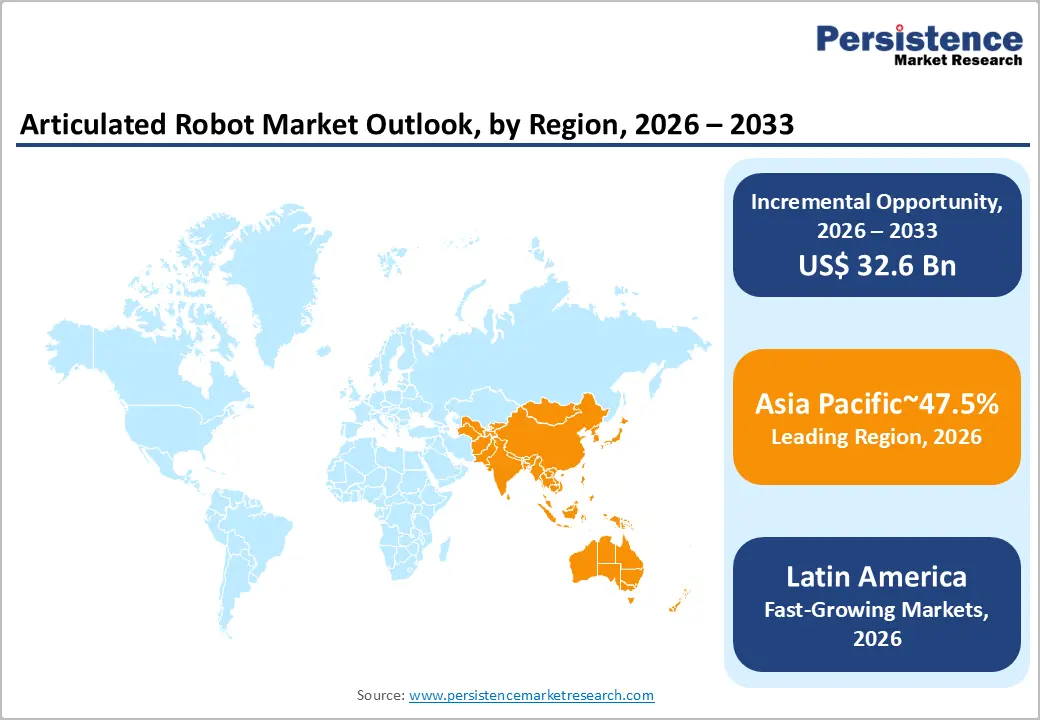

Asia Pacific Articulated Robot Market Trends and Insights

Asia Pacific holds a share of 47.5% in 2025, by far the dominant global region. China alone accounts for the majority of Asian demand, accelerated by Made in China 2025 policy support, EV battery manufacturing, and consumer electronics. According to the International Federation of Robotics, Asia accounted for over 70% of global industrial robot installations in 2023. Japan, South Korea, and India are reinforcing the region's leadership through aggressive automation in semiconductors, automotive, and emerging electronics manufacturing clusters.

China Articulated Robot Market Size

China's articulated robot market value reached US$ 3,803.8 Million in 2025, driven by record-scale investments in EV manufacturing by BYD, CATL, Geely, and NIO, alongside dominant electronics assembly capacity. According to the National Bureau of Statistics of China, the country produced more than 556,000 industrial robots in 2024, registering double-digit year-on-year growth. Domestic robot makers such as Estun, Inovance, and Siasun continue to gain share, supported by government procurement and aggressive cost competitiveness.

India Articulated Robot Market Size

India's articulated robot market value reached US$ 734.8 Million in 2025, driven by rapid expansion of automotive manufacturing under the Production Linked Incentive (PLI) scheme, with investments by Tata Motors, Maruti Suzuki, and Mahindra Electric. According to the Society of Indian Automobile Manufacturers (SIAM), India produced over 5.4 million passenger vehicles in 2024, fueling robotic adoption in body shops and weld lines. Growing electronics contract manufacturing for Apple suppliers also lifts demand.

Japan Articulated Robot Market Size

Japan represents one of the world's most mature articulated robot markets, anchored by domestic giants FANUC, Yaskawa, Kawasaki Robotics, and Mitsubishi Electric. According to the Japan Robot Association (JARA), robot production exceeded JPY 900 billion in shipment value in 2023, with strong export orientation toward China, the U.S., and Europe. Domestic demand is sustained by automotive electrification at Toyota and Honda, plus advanced semiconductor equipment manufacturing.

Competitive Landscape

The global articulated robot market exhibits a moderately consolidated structure, with the top five players capturing an estimated 55–60% of global revenue. Industry leaders such as FANUC, ABB, KUKA, Yaskawa Electric, and Kawasaki Heavy Industries differentiate through proprietary motion control software, AI-enabled vision integration, and global service networks.

Emerging Chinese players including Estun Automation and Inovance are gaining share through cost-competitive offerings and government-backed procurement. Strategic priorities include expanding cobot-style articulated platforms, deepening AI partnerships with NVIDIA and hyperscale cloud providers, and developing as-a-service business models that lower customer entry costs and accelerate factory adoption.

Key Developments

- In September 2025, FANUC: The company expanded its articulated robot portfolio with the launch of the M-1000/550F-46A, a six-axis high-payload robot featuring a 550 kg capacity and 4.6 m reach, designed for heavy-duty applications such as automotive giga casting, battery handling, and large workpiece manipulation, offering enhanced speed, extended work envelope, and advanced smart factory integration through the R-50iA controller, strengthening FANUC’s position in the high-payload articulated robot segment.

- In May 2024, ABB company expanded its articulated robot portfolio with the launch of the IRB 7710 and IRB 7720 modular large robots, offering 16 new variants within a broader lineup of 46 configurations supporting payloads from 70 kg to 620 kg, delivering up to 30% energy savings and enhanced flexibility for high-payload applications such as automotive manufacturing, EV battery production, press automation, palletizing, and precision machining, strengthening ABB’s position in the articulated robot market.

Companies Covered in Articulated Robot Market

- FANUC Corporation

- ABB Ltd.

- KUKA AG

- Yaskawa Electric Corporation

- Kawasaki Heavy Industries, Ltd.

- Mitsubishi Electric Corporation

- DENSO Corporation

- Universal Robots A/S

- Stäubli International AG

- Comau S.p.A.

- Nachi-Fujikoshi Corp.

- Epson Robots (Seiko Epson Corporation)

- Estun Automation Co., Ltd.

- Inovance Technology Co., Ltd.

- Siasun Robot & Automation Co., Ltd.

- Hyundai Robotics

- OMRON Corporation

- Techman Robot Inc.

Frequently Asked Questions

The global articulated robot market is projected to reach US$ 20.8 Billion in 2026, expanding to US$ 53.4 Billion by 2033 at a 14.4% CAGR, supported by automotive electrification and electronics automation.

The accelerating shift to electric vehicles and persistent manufacturing labor shortages, with the U.S. Bureau of Labor Statistics reporting over 600,000 unfilled manufacturing roles, are the primary demand drivers fueling articulated robot adoption globally.

Asia Pacific leads with a 47.5% share in 2025, driven by China's massive EV and electronics manufacturing base, supportive Made in China 2025 policy, and rapidly growing demand from India and Southeast Asia.

AI-enabled vision systems, collaborative mid-payload robots, and government automation incentives such as the CHIPS Act and K-Robot Economy Plan present major opportunities for adaptive bin-picking, palletizing, and electronics applications.